Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available here. Rare cases of sponsored projects are clearly indicated.

One of the central objectives of the second Trump administration has been to pursue a maximalist trade policy toward China. However, that ambition has been blunted by China’s ability to leverage its dominance of the rare earth supply chain, including 91 percent of global rare earth refining production and, together with Myanmar, 83 percent of heavy rare earth mined production. In April 2025, Beijing subjected seven heavy rare earth elements—samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium—to export licensing controls requiring exporters to declare end-users before shipment, including for permanent magnets containing dysprosium and terbium. The Chinese government subsequently added holmium, erbium, thulium, europium, and ytterbium to the export control regime and introduced a Foreign Direct Product Rule-equivalent measure, extending Beijing’s influence over downstream supply chains worldwide. Although China and the United States reached a temporary truce in November that deferred full implementation of the controls, the licensing apparatus remains intact, and Beijing has already demonstrated its willingness to employ it by blacklisting twenty Japanese companies for dual-use concerns in February 2026.

One year after the initial restrictions were announced, China’s General Administration of Customs (GACC) has released the latest export data, offering a glimpse of US dependence on Chinese rare earths. This piece draws on the data from January 2023 through April 2026 to map that dependence and identify segments of the supply chain where US exposure is pronounced. The analysis reinforces the established picture in current US policy debates of heavy reliance on permanent magnets, but suggests that the full extent of US exposure has been understated. The dataset captures only magnets shipped as discrete components, excluding those embedded in finished goods. It also indicates that the current debate obscures US reliance on yttrium and lanthanum. More broadly, the piece shows that US dependence extends well beyond the “mine-to-magnet” supply chain, raising questions for policymakers about how far diversification efforts should reach.

The rare earths policy discussion has concentrated on the permanent magnet supply chain, and for good reason—magnetic rare earths represent 96 percent of consumption by value. Neodymium-iron-boron (NdFeB) magnets account for over 90 percent of the permanent magnet market, and China accounts for 94 percent of global sintered NdFeB production. Between January 2023 and April 2026, the United States was the second-largest destination for Chinese permanent magnet exports by volume, after Germany, receiving 22,600,310 kilograms.

However, before the recent restrictions, the United States imported only trace amounts of dysprosium and terbium, the heavy rare earth elements that are used in NdFeB magnets, reflecting limited domestic processing and manufacturing capacity. Instead, US imports are concentrated in finished products containing these materials.

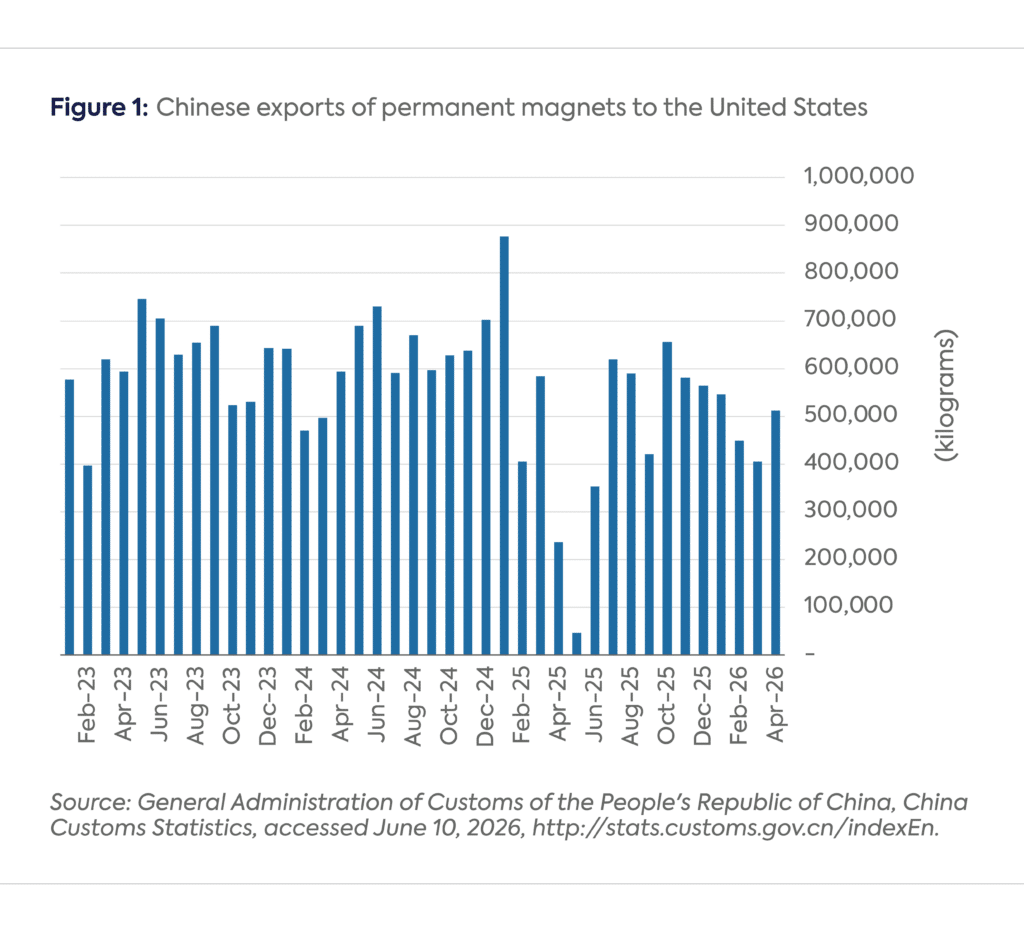

Figure 1 shows that Chinese exports continued to flow following the restrictions as the supply chain adjusted to the new licensing requirements. Nevertheless, shipments to the United States fell by 22 percent in the twelve months ending in April 2026 compared with the prior twelve months. Despite the truce, total magnets exports from December 2025 through April 2026 were still down compared to the same time period over the previous two years.

Yet the export data underestimates US exposure. The permanent magnet Harmonized System (HS) code captures only magnets shipped as discrete products; it does not capture the magnets embedded in finished goods that enter the United States inside vehicles, appliances, and electronics. For example, the Department of Energy estimates that each electric vehicle motor requires approximately 1–2 kg of NdFeB magnet material. The United States imported 451,575 EVs in 2025—251,371 from Mexico, 93,388 from Germany, 56,490 from Japan, 14,552 from South Korea, and 9,833 from Sweden. Outside Japan, none of these countries produces NdFeB magnets at scale and all are leading recipients of Chinese magnets.

Japan is a partial exception as the world’s second-largest NdFeB producer. However, it still relies on China for approximately 70 percent of its rare earth supply chain. The United States and Japan therefore have an interest in working together to diversify upstream production and reduce exposure to further demand shocks arising from their position in the supply chain.

The White House fact sheet published after President Trump’s recent visit to China in May states that “China will address U.S. concerns regarding supply chain shortages related to rare earths and other critical minerals, including yttrium, scandium, neodymium, and indium.” The export data shows why yttrium was included on this list.

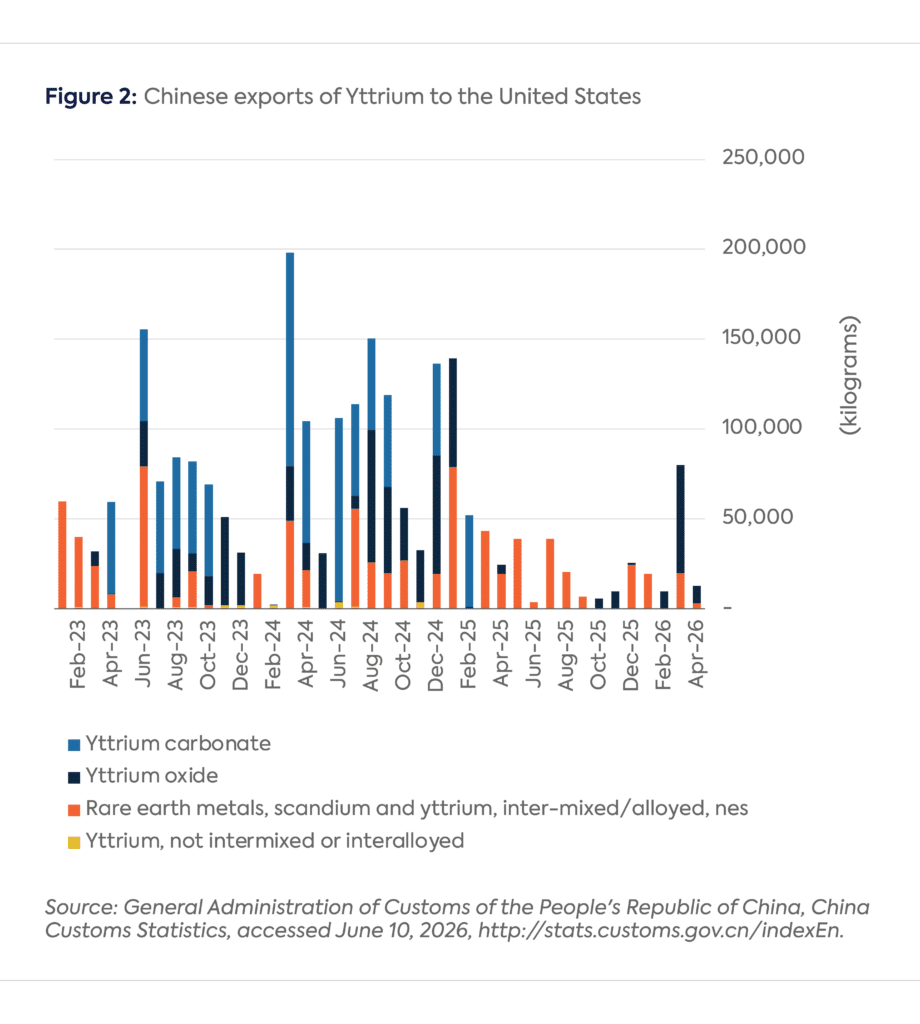

The United States is 100 percent import-reliant for yttrium. The bulk of civilian demand for it derives from ceramics and phosphors for LED lighting and display screens, but the more strategically sensitive applications are in aerospace and defense. Yttrium is used in thermal barrier coatings that protect jet engines from extreme heat and in the production of high-performance lasers. Chinese Yttrium oxide exports to the United States fell by approximately 75 percent in 2025 relative to 2024. Despite the October US–China truce, aerospace organizations warned of industrial shortages as recently as February. Exports only began to recover in March. Yttrium carbonate, a precursor to yttrium oxide, has not recovered (Figure 2).

The most credible near-term source of non-Chinese yttrium is Serra Verde’s Pela Ema deposit in Brazil, which is ramping up production. Yttrium is expected to account for 42 percent of full output. However, Pela Ema produces concentrate rather than separated oxide, and Serra Verde has not yet made a final investment decision on a separation facility. While Serra Verde agreed to a fifteen-year offtake with a US government–backed special purpose vehicle for 100 percent of its production of four magnetic rare earths, yttrium was not included.

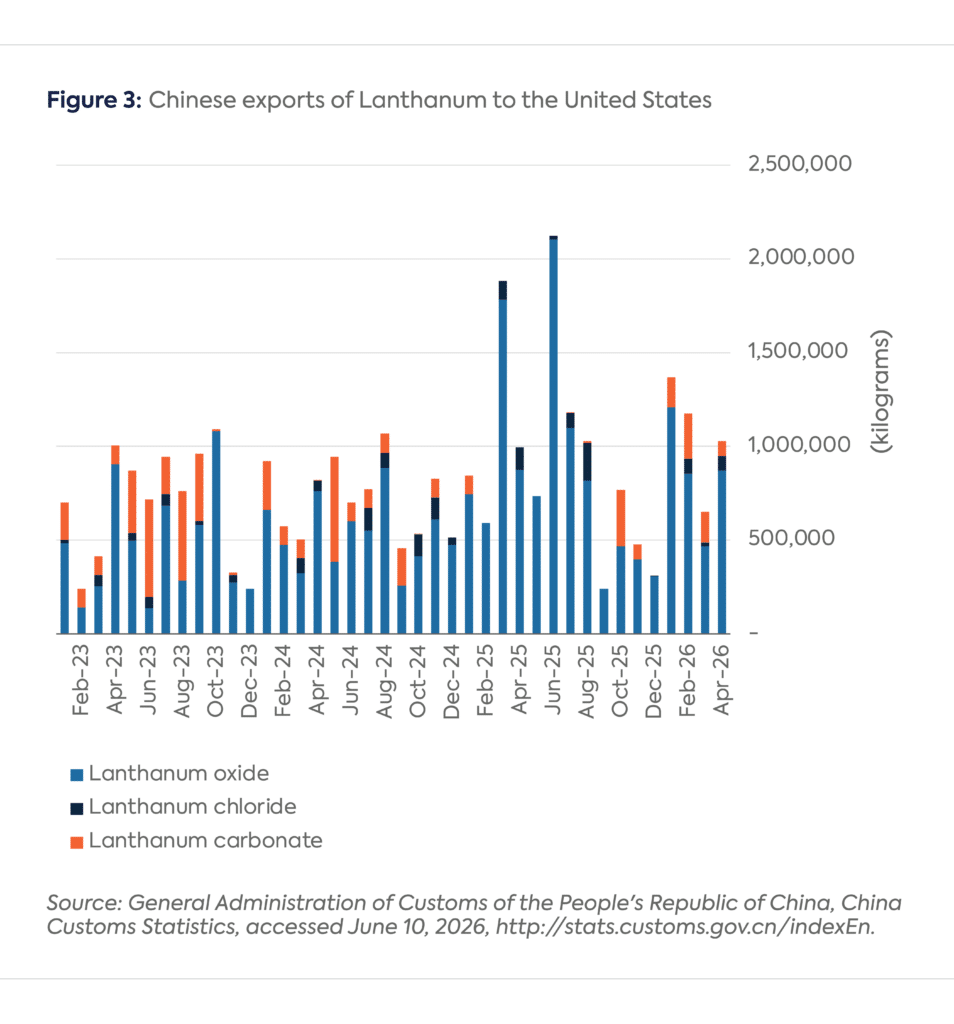

The most traded rare earth oxide between China and the United States is lanthanum—a light rare earth outside the scope of Beijing’s export controls. Lanthanum-based catalysts are the backbone of fluid catalytic cracking, the refinery process that converts crude oil into gasoline, diesel, and military jet fuel.

Since January 2023, the United States has absorbed approximately 64 percent of China’s total global lanthanum oxide exports (Figure 3).

Economics, not geology, accounts for this dependency. Lanthanum oxide averaged just $1 per kilogram in 2025, compared with $69 per kilogram for NdPr oxides. At that price, separation and processing costs are unrecoverable for most producers outside China. China also exports significant quantities of lanthanum carbonate, a precursor to lanthanum oxide, to the United States, extending the dependency further upstream.

There is bipartisan consensus in Washington on the need to support rare earth supply chain projects. However, the export data highlight two important considerations for US policymakers.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

The US Export-Import Bank is preparing to close the first funding tranche of Project Vault, a public-private partnership establishing the US Strategic Critical Minerals Reserve.

Securing critical minerals is a top priority of governments around the world.

This paper proposes a de-risking framework of policy interventions to provide the risk allocation, revenue certainty and delivery confidence required by mainstream private finance.

This paper examines the trade dimensions of the policy instruments employed by the United States to secure critical minerals supply chains. Drawing on policy statements, executive orders, tariff schedules, and six bilateral critical minerals agreements announced in 2025, it assesses how US trade policy has been repurposed to advance supply-chain security objectives. The paper finds that recent US initiatives reflect bipartisan trends in reconfiguring trade policy that predate the Trump administration, even as they introduce new and consequential trade coordination mechanisms that operate outside the World Trade Organization and beyond conventional free trade agreements. Specifically, US critical minerals security strategy now relies on a differentiated set of sector-specific arrangements that combine familiar elements of US international economic engagement with more novel features that increasingly utilize trade policy instruments. What distinguishes these six minerals deals is their systematic coupling with parallel reciprocal trade negotiations, their incorporation of an explicitly ‘America First’ approach to reciprocity, the absence of a clear ideological hierarchy among partner countries, an emphasis on domestic processing and industrialization, and the growing use of exclusion mechanisms targeting third-party actors. The recurrence of these novel elements across diverse minerals deals suggests deliberate design rather than ad hoc experimentation that may have durable restructuring effects across global mineral supply chains. The paper concludes by outlining implications for US policy makers, for partner countries—particularly mineral-producing low- and middle-income economies—and for the architecture of the global trading system.