In the waters off Malaysia, Iranian oil sales continue despite blockade

A large anchorage area off the coast of Malaysia is a major marketplace for sanctioned oil.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the demand for power surges across the US, the debate over how to build energy infrastructure has reached a fever pitch. And while both sides of the...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Commentary by Kevin Brunelli & Tom Moerenhout • May 05, 2026

This commentary represents the research and views of the authors. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. The Center on Global Energy Policy would like to thank Blue Horizons Foundation for its grant in support of CGEP. More information is available at Our Partners.

Refined copper, the product of smelting mined copper concentrate, is essential to the 21st-century economy, including for AI, data centers, electrical grids, and clean energy technologies. Copper is also one of the few critical minerals for which China does not dominate the full supply chain. As of 2024, China accounted for only about 8 percent of copper concentrate production, though it produced 48 percent of smelting output and exerts influence through investments in overseas projects.[1] However, the overexpansion of global smelting capacity, combined with structurally tight concentrate supply, have pushed treatment and refining charges (TC/RCs) to record lows. This has put copper smelters in the United States and allied economies—including the EU, Australia, Japan, Canada, and South Korea—at risk of closure, even as copper demand is estimated to increase by 50 percent from 2025 to 2040.[2]

Leading mining and commodity trader firms have already warned that existing smelters are not profitable[3] and require “government ownership or significant government support.”[4] This pattern is visible across jurisdictions. For example, Glencore halted its smelter in the Philippines[5] and received government assistance to continue operations at its Mount Isa operation in Australia,[6] while its Horne smelter in Canada may also be at risk.[7] In Japan, Mitsubishi and JX Advanced Materials are reviewing operations or scaling back production.[8] Even the Chinese company, Sinomine, has paused smelting in Namibia.[9]

As the United States and allied economies are working to build new critical minerals supply chains, the immediate priority for copper is defensive—protecting existing midstream assets. Rather than building new smelters[10] or investing in overseas copper projects, as the US government is currently considering,[11] this means supporting domestic smelters that may otherwise soon shut down. Any lost capacity would likely be absorbed by Chinese smelters, reinforcing China’s control over the supply chain. The following sections analyze the factors contributing to these trends and outline three potential policy solutions.

Copper smelters convert copper concentrate, the material produced from mined ore, into blister copper, a semi-refined product containing roughly 99 percent pure copper. The semi-refined product is then refined into 99.999 percent copper cathodes and other copper products. Approximately 80 percent of global copper mines produce copper concentrate that needs to be smelted.[12]

Smelters are grouped into two main categories—integrated and custom. Integrated smelters are vertically integrated with a copper mine, whether co-located or part of the same company, though some purchase copper concentrate from smaller mines to increase utilization rates and improve economics. Custom smelters are standalone operations, sourcing copper concentrate from a variety of copper mines. Given these differences, the two types require distinct forms of government intervention to keep facilities open.

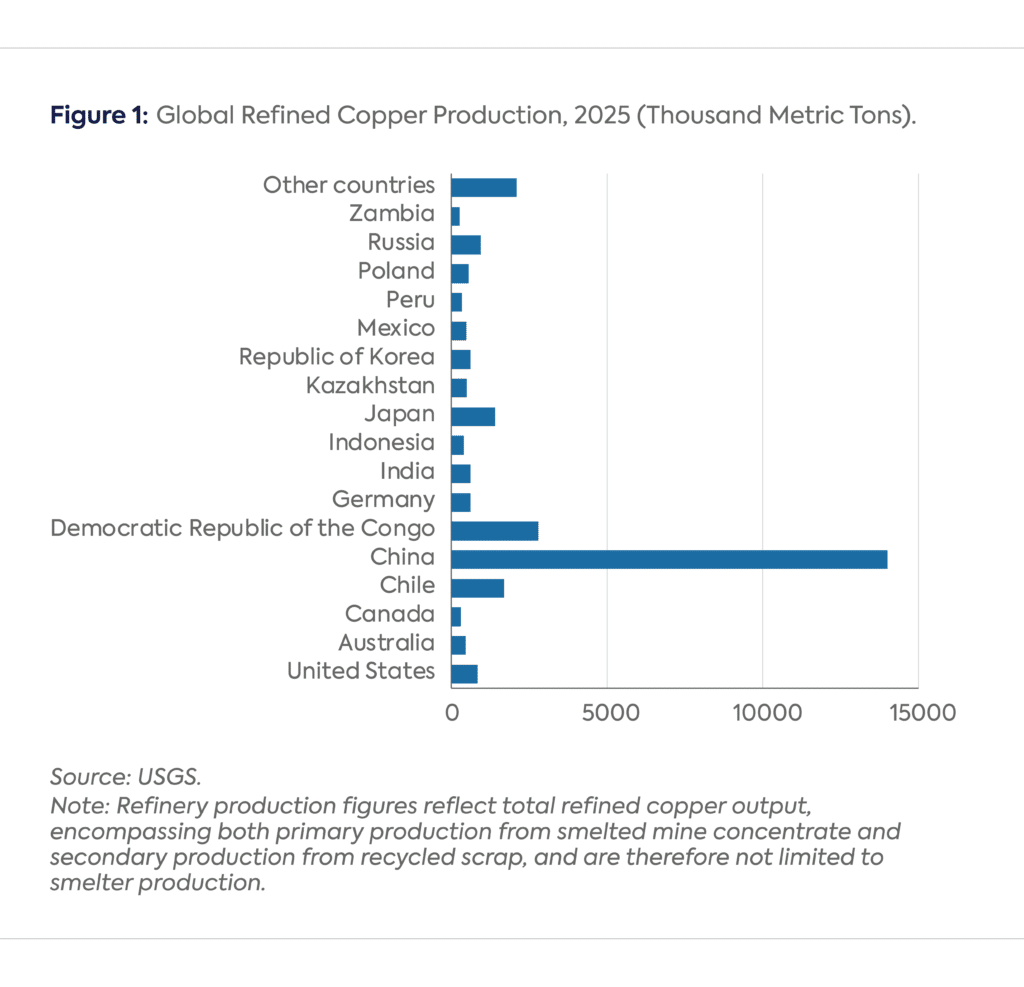

Figure 1shows copper production by country. The United States has only two active copper smelters—Rio Tinto’s Garfield Smelter in Utah and Freeport-McMoran’s Miami Smelter in Arizona—both of which are over a century old and are integrated. China accounted for approximately 50 percent of copper smelter production in 2025 and has 12 of the 20 largest smelters by capacity.[13] China’s smelter expansion was originally driven by the needs of its fast-growing economy, manufacturing base, and construction boom. Of its current capacity, 75 percent has come online since 2000,[14] even as domestic demand has slowed from double digit growth in the early 2000s to 4 percent annual growth in 2024.[15] Nearly 90 percent of copper smelters in China are custom, which means they compete on the market for concentrate.[16]

China’s growing dominance in this space is the product of copper smelter economics. Leading mining companies report that building a new copper smelter in the United States could cost up to $5 billion.[17] In China, new smelters can be built up to five times cheaper.[18] This cost advantage reflects lower labor and environmental compliance as well as construction efficiency and accumulated expertise. Additionally, access to cheap capital has allowed China to build smelters with advanced by-product recovery circuits that extract and monetize sulfuric acid, gold, silver, and other materials, the revenue from which further offsets costs and keeps plants profitable. Several big Chinese players, such as Jiangxi Copper, also manufacture copper products, allowing them to accept lower or negative margins at the smelter level and recover losses through vertical integration.[19]

This cost advantage for Chinese smelters extends to operating expenses, enhancing their competitive edge. Broadly, Chinese smelters operate at less than half the cost of facilities elsewhere in the world, benefitting from cheaper power, labor, maintenance, and raw material inputs.[20] The largest operating cost for smelters is electricity and fuel, as smelting and converting copper concentrate into anode metal require high-temperature furnaces and continuous power, making smelters highly sensitive to energy prices. Chinese smelters operate under significantly lower energy costs than their US and European counterparts, with European facilities facing the most severe energy challenges. Aurubis, Europe’s largest copper producer, reports that energy costs at its facilities in Germany are roughly three times higher than those at its facilities in the United States.[21]

Beyond electricity and fuel, labor and maintenance costs are also substantial due to the complexity of smelting operations, environmental controls, and safety standards. Smelters spend heavily to manage waste and comply with environmental standards, including capturing harmful sulfur gases to protect neighboring communities and the land. China’s modern smelters were built to meet some higher environmental standards like sulfur dioxide emissions.[22] Overall, however, they face lower environmental standards than their US and European counterparts, reducing their compliance costs and contributing to the overall operating cost differential.[23] Outside of China, the high expense of required environmental upgrades has reportedly been a major factor in Glencore’s deliberations over whether to close its Canadian smelter.[24] Meanwhile, Grupo Mexico’s smelter in Arizona, initially closed because of a labor dispute, faces additional challenges to reopening because of its long history of Environmental Protection Agency enforcement actions and designation as a Superfund alternative site—liabilities that contributed to financial issues.[25]

This severe differential in operating expenses poses an immediate challenge for smelters in the United States and allied countries, especially amid overexpanded smelter capacity and a tight copper market. Smelting capacity has continued to expand globally—especially in China, which experienced 11 percent growth in 2025 from the prior year[26]—while disruptions or underperformance at major mines, such as Kamoa-Kakula[27] and Freeport’s Indonesian assets,[28] and the closure at Panama’s Cobre Panamá mine due to ongoing political and legal proceedings,[29] have led to predictions of a copper deficit in 2026.[30]

National industrial policies promoting new smelter construction have exacerbated this discrepancy. China is the main driver of these policies, but other countries such as Indonesia, where domestic-processing requirements encourage investment in new smelters, are contributing as well.[31] Global smelting capacity is rising faster than concentrate supply, increasing competition for feedstock and resulting in record-low TC/RCs, a key source of revenue for smelters. US and allied smelters are likely to bear the brunt of these trends.

Treatment charges are the fee that smelters charge miners to treat concentrate and produce a copper anode. Refining charges are the fee they charge miners to refine the anode into a high purity copper cathode. TC/RCs are estimated to account for a third of smelters’ revenue.[32] In the current overcapacity environment, smelters vie for access to copper concentrate to process. Following basic supply and demand rules, when copper concentrate supply is in a deficit relative to smelter capacity, TCs fall as smelters compete to secure supply.

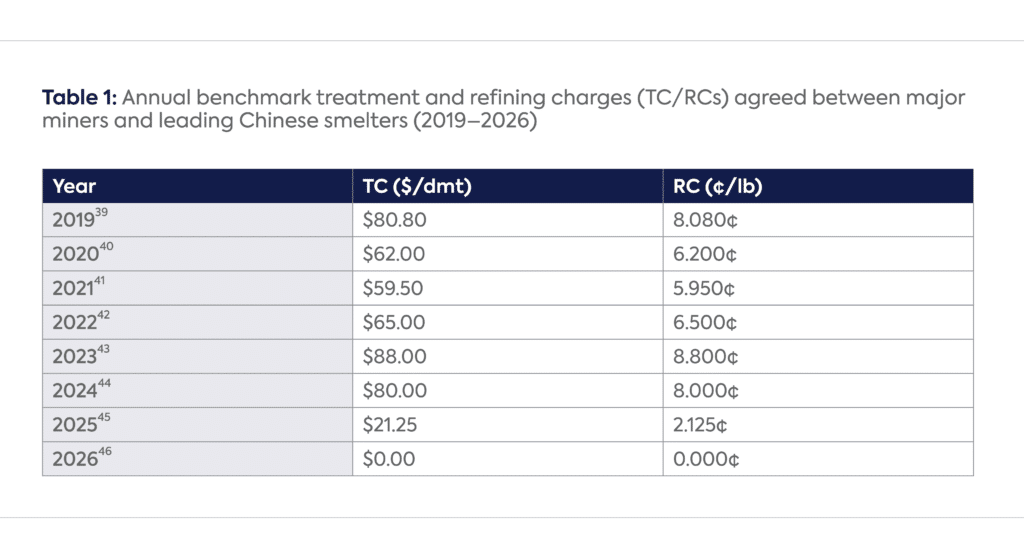

Historically, smelters and mining companies have agreed on TC/RCs through annual benchmark contracts negotiated by major players, which then served as a reference price for the wider market. This traditional benchmark system provided stability and predictability, with fees reflecting processing costs, concentrate quality, and prevailing supply-demand conditions to balance the interests of mines and smelters. In recent years, however, the bargaining power has shifted to miners. The China Smelters Purchase Team (CSPT), a consortium that coordinates procurement and negotiates benchmark TC/RCs, has strengthened China’s collective bargaining position.[33] But smelters elsewhere now face a difficult choice between three bad options: accepting low TC/RCs; shutting down, which is costly; or operating at reduced capacity, which is uneconomical.

In 2025, smelters in China, Japan, and Europe accepted TC/RCs in the $20 range.[34] But charges on the spot market went negative at several points.[35] In December, Antofagasta, the Chilean copper miner, and a Chinese copper smelter agreed to $0 TC/RCs for 2026. This represents the lowest rate ever reached in annual negotiations (see Figure 2).[36] In March 2026, spot market TCs went to negative $90 per ton.[37] Industry experts expect TC/RCs to remain low due to mine disruptions and a lack of additional feedstock.[38]

China’s own capacity restraint signals the severity of the problem. China’s top smelters have cut production by over 10 percent in 2026 specifically in response to negative processing fees.[47] Moreover, the Chinese government has halted some new smelter build-out in response to negative treatment charges.[48] The fact that even China—whose smelters operate at half the cost of Western competitors—is reacting in this way shows that the TC/RC challenge is not a temporary but a structural problem requiring immediate government intervention. While some smelters have used revenues from by-products with historically high prices, such as gold and silver, as a lifeline,[49] this is not a sustainable solution. Relying on by-product revenues exposes profitability to broader commodity market cycles. Moreover, high by-product pricing may mask the severity of the structural collapse in TC/RC rates, and when by-product markets stabilize, smelters could suddenly find themselves facing a viability crisis.

In normal market conditions, challenging economics would force uneconomical smelters offline, with the lowest-cost producers remaining in operation. But in the current environment that would mean the smelter industry being concentrated in China—an untenable outcome for the United States and allies for both economic and national security reasons. Policy intervention can help chart a different path, but it would need to be carefully tailored.

Until now, the preferred policy intervention for critical minerals projects, especially by the Trump Administration, has been equity investments or loans, but these instruments are ill-suited for keeping existing smelters operational. The companies running these smelters are global businesses with already deep balance sheets. What they lack is not funding but an incentive to continue operating unprofitable or financially weak businesses. In the current environment, it could even make financial sense for integrated smelters to shut down facilities and sell the copper concentrate on the global market.

The United States and allied economies are currently placing particular attention on building out new greenfield midstream processing facilities for critical minerals across the periodic table. While it is logical to secure medium-term resilience and essential to build a policy ecosystem to support future smelter development, new facilities take years to permit and construct, and the economics of greenfield development remain unfavorable. Some proposals suggest retrofitting older smelters to capture additional commodities, but such modernization could cost the equivalent of building a new smelter.[50]

For policy interventions to be effective at preventing market concentration, they will instead need to focus on the operating expenses of existing facilities—and to do so in a tailored way that addresses the distinct mix of feedstock, cost, regulatory, and market constraints each copper smelter faces. This is undoubtedly a challenging task. Labor costs are relatively fixed, and maintenance costs are necessary for social operating licenses. Additionally, energy cost politics are fraught across Europe and the United States—especially in the US, where rising prices reflect grid investment, disaster recovery, volatile fuel markets, and growing electricity demand from data centers. Consumers are also facing affordability issues, making energy cost support politically unviable for now. Amid these constraints, the following three policy responses on the part of US and allied economies could be particularly effective:

This policy would function as a contract-for-difference mechanism. The government and smelters would agree on a reference TC/RC based on operating breakeven levels or a historical sustainability benchmark. If market TC/RCs fall below this level, the government would compensate the smelter for the difference on open-market-purchased concentrate only. Concentrate transacted domestically would clear at globally competitive terms to ensure mines are not disadvantaged relative to export markets. This structure prevents concentrate from being exported solely due to temporary TC/RC pricing distortions while stabilizing smelter economics.

To see how these policies would play out in practice, consider the basic example of a non-Chinese copper mine that is weighing bids from competing smelters: a Chinese smelter offering a spot TC/RC of –$50 (essentially paying the mine for concentrate) and a US facility requiring a $50 TC/RC to cover labor, energy, maintenance, and environmental compliance costs. In this scenario, processing in the United States would be economically irrational. For the government to address this issue, it would need to intervene on both sides of the transaction.

These three policy measures are not mutually exclusive and would function most effectively in tandem. Even integrated smelters suffer from a structurally low TC/RC environment. The low rates influence internal transfer pricing, which directly influences how shareholders assess smelter performance, and could be the deciding factor in whether companies keep an integrated smelter alive or close it and sell concentrate for more profit externally.

Kevin Brunelli is a Non-Resident Fellow at the Center on Global Energy Policy focusing on critical minerals and the battery supply chain.

Previously, he was a member of the Critical Minerals and Energy Technologies team in the Bureau of Energy Resources at the U.S. State Department where he served as the lead for critical minerals diplomacy in East Asia and Australia. He was also the Department lead for lithium, nickel, and minerals and energy technologies facing Chinese export restrictions.

He was previously a Research Associate at the Center on Global Energy Policy, focused on critical minerals, battery supply chains, and economic statecraft. Prior to working at Columbia, Kevin was a producer at CNN. He graduated from Columbia SIPA with a Master’s in Public Administration with a concentration in Energy and Environment and received a B.A from the Catholic University of America.

Dr. Tom Moerenhout is a Professor at Columbia University’s School of International and Public Affairs and leads the Critical Materials Initiative at Columbia’s Center on Global Energy Policy. His work extends to roles as Senior Advisor at the World Bank Energy and Extractives Group, Executive Director at the Geneva Platform for Resilient Value Chains, and Senior Associate at the International Institute for Sustainable Development and Intergovernmental Forum on Mining, Minerals and Metals. He has served as Visiting Professor at NYU, Sciences Po Paris, and the Geneva Graduate Institute.

Tom specializes in the intersection of geopolitics and industrial policy, particularly as they relate to energy, critical minerals, and battery supply chains. His work focuses on integrating the interests and influence of multiple actors across complex political economies to improve supply chain security and resilience. Tom has published extensively on sustainable development and energy policy reforms, specifically on energy subsidies, critical materials, and the economic development of resource-rich countries.

He has advised and consulted for various stakeholders, including the White House, Departments of Energy and State, USTR, and policymakers in several other countries, including the EU, Canada, India, Indonesia, Nigeria, DRC, Egypt, Iraq, Chile, and Brazil. His collaborative efforts span organizations such as the OECD, IEA, World Bank, UNCTAD, UNEP, OPEC, IRENA, and several philanthropic foundations.

Tom holds two master’s degrees and obtained his PhD at the Graduate Institute of International and Development Studies in Geneva. This academic background includes fellowships at LSE and the Oxford Institute for Energy Studies. He was also a Fulbright and Albert Gallatin Fellow, and a Swiss National Science Foundation Scholar.

In his downtime, Tom enjoys reading & writing, culinary experiences, football, skiing, and chess.

[1] US Geological Survey, Mineral Commodity Summaries 2026 (Washington, DC: US Department of the Interior, January 2026), https://pubs.usgs.gov/periodicals/mcs2026/mcs2026.pdf.

[2] S&P Global, Copper in the Age of AI: Challenges of Electrification (S&P Global Energy & Market Intelligence, January 8, 2026), https://www.spglobal.com/en/research-insights/special-reports/copper-in-the-age-of-ai.

[3] Julian Luk and Thomas Biesheuvel, “Glencore Overhauls Embattled Canadian Smelters as Margins Plunge,” Bloomberg, March 14, 2025, https://www.bloomberg.com/news/articles/2025-03-14/glencore-overhauls-embattled-canadian-smelters-as-margins-plunge.

[4] Archie Hunter and Jack Farchy, “Trafigura Starts Review of Ailing Australian Smelting Assets,” Bloomberg Law, March 26, 2025, https://news.bloomberglaw.com/mergers-and-acquisitions/trafigura-starts-strategic-review-of-australian-smelting-assets.

[5] Camilla Hodgson, “Manufacturers Plead for US Tariff Clarity Before Copper Stockpiles Dwindle,” Financial Times, 2025, https://www.ft.com/content/032e9250-66df-44b3-926e-3e5e8fed8e76.

[6] Melanie Burton, “Australia Unveils $395 Million to Support Glencore Copper Smelter,” Reuters, October 8, 2025, https://www.reuters.com/business/australia-unveils-395-million-support-glencore-copper-smelter-2025-10-08/.

[7] Pratima Desai, “Exclusive: Glencore Plans to Shut Canada’s Largest Copper Metal Operation Over Costs,” Reuters, November 3, 2025, https://www.reuters.com/sustainability/boards-policy-regulation/glencore-plans-shut-canadas-largest-copper-metal-operation-over-costs-2025-11-03/.

[8] Yuka Obayashi, “Japan’s Mitsubishi Materials May Scale Back Copper Smelting Due to Worsening Margins,” Reuters, August 4, 2025, https://www.reuters.com/markets/commodities/japans-mitsubishi-materials-may-scale-back-copper-smelting-due-worsening-margins-2025-08-04/;

Yuka Obayashi and Kentaro Okasaka, “Major Japanese Copper Smelter to Cut Output Capacity as Margins Erode,” Reuters, September 5, 2025, https://www.reuters.com/world/china/major-japanese-copper-smelter-cut-output-capacity-margins-erode-2025-09-05/.

[9] Nyasha, Nyaungwa, “Sinomine Halts Namibia Copper Smelter, Citing Concentrate Shortage,” Mining.com, June 6, 2025, https://www.mining.com/web/sinomine-halts-namibia-copper-smelter-citing-concentrate-shortage/.

[10] Eric Onstad, “Aurubis Held Talks with US on Support for New Smelter, CEO Says,” Mining.com, October 14, 2025, https://www.mining.com/web/aurubis-held-talks-with-us-on-support-for-new-smelter-ceo-says/.

[11] Glencore, “Proposed Acquisition by US-Backed Orion Critical Mineral Consortium of a Strategic Stake in Glencore’s DRC Assets,” Glencore Media & Insights, February 3, 2026, https://www.glencore.com/media-and-insights/news/proposed-acquisition-by-us-backed-orion-critical-mineral-consortium-of-a-strategic-stake-in-glencores-drc-assets.

[12] Nick Pickens, Robert Griffin, Eleni Joannides, and Zhifei Liu, “Securing Copper Supply: No China, No Energy Transition,” Wood Mackenzie Horizons, August 2024, https://www.woodmac.com/horizons/securing-copper-supply-china-energy-transition/.

[13] International Energy Agency, “Copper Smelter Production by Region, 2005–2025,” chart (Paris: IEA, 2026), https://www.iea.org/data-and-statistics/charts/copper-smelter-production-by-region-2005-2025; International Copper Study Group, The World Copper Factbook 2025 (Lisbon: ICSG, October 2025), https://icsg.org/copper-factbook/.

[14] Pickens et al., “Securing Copper Supply.”

[15] International Institute for Strategic Studies, “New Constraints in the Global Copper Market,” Strategic Comments, 2026, https://www.iiss.org/publications/strategic-comments/2026/new-constraints-in-the-global-copper-market/.

[16] Pickens et al., “Securing Copper Supply.”

[17] Industry expert, personal communication with the authors, October 2025.

[18] US Department of Commerce, Bureau of Industry and Security, “Public Comment on Section 232 National Security Investigation of Imports of Copper,” Docket No. BIS-2025-0010-0076, Regulations.gov, 2025, https://www.regulations.gov/comment/BIS-2025-0010-0076.

[19] Industry expert, personal communication with the authors, October 2025.

[20] Rio Tinto, “Comment on Bureau of Industry and Security Request for Public Comments on Section 232 National Security Investigation of Imports of Copper (Docket No. BIS-2025-0010),” submitted to U.S. Department of Commerce, Bureau of Industry and Security, April 1, 2025, https://downloads.regulations.gov/BIS-2025-0010-0076/attachment_1.pdf.

[21] “Copper Smelters Not Yet at Peak Pain Despite Tight Concentrate Market, Mercuria Says.” Fastmarkets, October 15, 2025. https://www.fastmarkets.com/insights/copper-smelters-not-yet-at-peak-pain-despite-tight-concentrate-market-mercuria-says/.

[22] Pickens et al., “Securing Copper Supply.”

23 Industry expert, personal communication with the authors, October 2025.

[24] “Glencore Said to Consider Shutting Canada’s Largest Copper Plant,” Mining.com, November 3, 2025, https://www.mining.com/glencore-considers-shutting-canadas-largest-copper-plant/.

[25] James Atwood, Jacob Lorinc, and Yvonne Yue Li, “Copper Demand Rises but U.S. Industry Lacks the Refining to Supply It,” Bloomberg, June 18, 2025, https://www.bloomberg.com/news/features/2025-06-18/copper-demand-rises-but-us-industry-lacks-the-refining-to-supply-it;

US Environmental Protection Agency, “ASARCO Hayden Plant: Cleanup Activities,” Superfund Site Profile, accessed 2026, https://cumulis.epa.gov/supercpad/SiteProfiles/index.cfm?fuseaction=second.cleanup&id=0900497#Status.

[26] “In Charts: Copper’s Shifting Trade Flows,” Benchmark Mineral Intelligence, 2025, https://source.benchmarkminerals.com/article/in-charts-coppers-shifting-trade-flows.

[27] “Ivanhoe Slashes 2025 Copper Guidance by 28% Following DRC Mine Restart,” Mining.com, June 12, 2025, https://www.mining.com/ivanhoe-slashes-2025-copper-guidance-by-28-following-drc-mine-restart/.

[28] “Freeport Plans to Restore Large-Scale Production at Grasberg in Q2 2026,” Mining.com, November 18, 2025, https://www.mining.com/freeport-plans-to-restart-large-scale-production-at-grasberg-in-q2-2026/.

[29] Zijia Song and Martha Viotti Beck, “Panama Insists on Resource Ownership in Cobre Copper Mine Talks,” Bloomberg, October 20, 2025, https://www.bloomberg.com/news/articles/2025-10-20/panama-insist-on-resource-ownership-in-cobre-copper-mine-talks.

[30] J.P. Morgan Global Research, “Copper Outlook,” J.P. Morgan Insights, accessed 2025, https://www.jpmorgan.com/insights/global-research/commodities/copper-outlook.

[31] Gracelin Baskaran, “Diversifying Investment in Indonesia’s Mining Sector,” Center for Strategic and International Studies, January 31, 2025, https://www.csis.org/analysis/diversifying-investment-indonesias-mining-sector.

[32] “Key Copper Talks Begin with Offer of Negative Processing Fees,” Bloomberg, May 28, 2025, https://www.bloomberg.com/news/articles/2025-05-28/key-copper-talks-begin-with-offer-of-negative-processing-fees.

[33] CRU Group, “How CSPT Smelter Cuts Could Reshape China’s Copper Demand in 2026,” December 2025, https://www.crugroup.com/en/communities/thought-leadership/2025/How-CSPT-smelter-cuts-could-reshape-Chinas-copper-demand-in-2026/.

[34] “‘Tougher Challenges Than Ever’ Facing Global Copper Smelting Industry: 2026 Preview.” Fastmarkets, January 5, 2026. https://www.fastmarkets.com/insights/tougher-challenges-facing-global-copper-smelting-industry/

[35] Sally Zhang, “‘Tougher Challenges Than Ever’ Facing Global Copper Smelting Industry: 2026 Preview,” Fastmarkets, January 5, 2026, https://www.fastmarkets.com/insights/tougher-challenges-facing-global-copper-smelting-industry/.

[36] Tom Daly et al., “Antofagasta Agrees Zero Copper Processing Charges for 2026 with Chinese Smelter,” Mining.com (via Reuters), December 20, 2025, https://www.mining.com/web/antofagasta-agrees-zero-copper-processing-charges-for-2026-with-chinese-smelter/.

[37] Fastmarkets, “Correction to Copper Concentrates Treatment and Refinement Charges Indices on March 20 2026,” March 23, 2026, https://www.fastmarkets.com/insights/correction-to-copper-concentrates-treatment-and-refinement-charges-indices-on-march-20-2026/.

[38] Industry expert, personal communication with the authors, October 2025.

[39] “Comment: What Next for Copper TC/RC Benchmark as Antofagasta Begins Breakaway?,” Fastmarkets, July 11, 2019, https://www.fastmarkets.com/insights/comment-what-next-for-copper-tc-rc-benchmark-as-antofagasta-begins-breakaway/.

[40] “There Are Serious Differences Between Miners and Smelters on the Cost of Copper Concentrate Processing and Refining,” Shanghai Metals Market (SMM), December 1, 2020, https://news.metal.com/newscontent/101332522-there-are-serious-differences-between-miners-and-smelters-on-the-cost-of-copper-concentrate-processing-and-refining.

[41] Shivani Singh and Tom Daly, “Freeport Lower 2021 Copper Charges Signal Sixth Drop for Benchmark,” Reuters, December 16, 2020, https://www.mining.com/web/freeport-lower-2021-copper-charges-signal-sixth-drop-for-benchmark/.

[42] Erik Heimlich, “2022 Copper TC/RC Benchmark Set at $65/6.5¢,” CRU Group, December 20, 2021, https://www.crugroup.com/en/communities/thought-leadership/2021/2022-copper-tc-rc-benchmark-set-at-65-6-5/.

[43] “Freeport Settles Six-Year High Copper Charges for 2023 with Chinese Smelters,” Reuters, November 24, 2022, https://www.mining.com/web/freeport-settles-six-year-high-copper-charges-for-2023-with-chinese-smelters/.

[44] Mai Nguyen, Siyi Liu, and Julian Luk, “Copper Miners, Chinese Smelters Agree on First Drop in Fees in 3 Years,” Reuters, December 1, 2023, https://www.mining.com/web/copper-miners-chinese-smelters-agree-first-drop-in-fees-in-3-years/.

[45] Lu Han and Lucy Tang, “Antofagasta Settles Copper Concs Treatment Charge with Jiangxi Copper at $21.25/mt for 2025 Term Contracts,” S&P Global Commodity Insights, December 6, 2024, https://www.spglobal.com/energy/en/news-research/latest-news/metals/120624-antofagasta-settles-copper-concs-treatment-charge-with-jiangxi-copper-at-2125mt-for-2025-term-contracts.

[46] Tom Daly, Pratima Desai, Amy Lv, and Lewis Jackson, “Antofagasta Agrees Zero Copper Processing Charges for 2026 with Chinese Smelter,” Reuters, December 20, 2025, https://www.mining.com/web/antofagasta-agrees-zero-copper-processing-charges-for-2026-with-chinese-smelter/.

[47] Dylan Duan, Lewis Jackson, and Beijing Newsroom, “China’s Top Copper Smelters to Cut Output to Combat Negative Processing Fees,” Reuters, November 28, 2025, https://www.mining.com/web/chinas-top-copper-smelters-to-cut-output-to-combat-negative-processing-fees/.

[48] Bloomberg News, “China Firmly Opposes Zero or Negative Copper Treatment Fees,” Bloomberg, November 26, 2025, https://www.bloomberg.com/news/articles/2025-11-26/china-firmly-opposes-zero-or-negative-copper-treatment-fees.

[49] International Energy Agency, “Copper Prices Have Hit Record Highs, but Smelters Face Mounting Strategic Pressures,” IEA Commentaries, https://www.iea.org/commentaries/copper-prices-have-hit-record-highs-but-smelters-face-mounting-strategic-pressures.

[50] Industry expert, personal communication with the authors, October and November 2025.

[51] Internal Revenue Service. (2024, October 28). Advanced manufacturing production credit. Federal Register, 89(209), 85798–85846, https://www.federalregister.gov/documents/2024/10/28/2024-24840/advanced-manufacturing-production-credit.

In early 2026, CGEP held a roundtable and several hybrid closed-door meetings in Mexico City on Mexico's mining sector.

Raw material vulnerability was once again at the center of the G7 agenda at the summit in Evian, France.

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

Full report

Commentary by Kevin Brunelli & Tom Moerenhout • May 05, 2026