In the waters off Malaysia, Iranian oil sales continue despite blockade

A large anchorage area off the coast of Malaysia is a major marketplace for sanctioned oil.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the demand for power surges across the US, the debate over how to build energy infrastructure has reached a fever pitch. And while both sides of the...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

White Paper by Diego Rivera Rivota, Leander Weigelt, Gaspar Simon Guevara + 2 more • June 23, 2026

This white paper is part of the Electricity Price Research Initiative and was made possible with support from Google.org. It represents the research and views of the authors. It does not necessarily represent the views of Google.org, the Center on Global Energy Policy, or Columbia University. The piece may be subject to further revision. More information is available at Our Partners.

Residential electricity prices have significantly increased across the United States beginning in 2025, diverging from their historical relationship with inflation. In 2025, the nominal average residential retail price of electricity increased by more than twice the rate of inflation.[i] By contrast, from 2019 to 2024—a period during which inflation reached its highest level in 40 years[ii] and became a major political issue—average retail electricity prices roughly tracked inflation.

These averages mask significant regional variation.[iii] In some states, including California, Maine, and Maryland, price increases have been acute, while in others, including Iowa, Nebraska, and Nevada, prices declined in real terms between 2019 and 2025.[iv] These trends have been shaped by complex, region-specific factors, including investments in replacing and hardening electricity grid infrastructure, recovery and mitigation expenses related to extreme weather events and wildfires, variability in natural gas prices, and electricity demand growth.

Synthesizing a wide range of data, academic literature, forecasts, policy documents, company press releases, news reporting, and original analysis on load forecasts, drivers of power price changes, regulatory structures, and policy responses to date, this white paper examines the specific role of rapid load growth—particularly from large loads such as data centers and increased manufacturing—in current and future US electricity price dynamics—a topic that has generated considerable expert and public debate.

The analysis proceeds as follows. The first section provides context for recent US electricity demand growth after several decades of limited growth and assesses highly divergent and uncertain data center demand growth forecasts for services such as streaming, cloud services, cryptocurrencies, and artificial intelligence (AI) applications. The second section examines how average US electricity prices largely tracked inflation between 2019 and 2024, before exceeding inflation in 2025 due to a range of region-specific factors rather than load growth alone. It also considers how both rapid load growth from data centers and electrification outpacing grid infrastructure expansion may reshape these dynamics. The third section assesses conflicting utility incentives, as well as existing policy approaches intended to prevent large-load growth from increasing residential electricity prices. The paper concludes by arguing that future pricing will depend heavily on the effective implementation of these measures and sustained coordination among regulators, grid operators, utilities, technology firms, and policymakers. Absent such coordination, the mismatch between rapid data center deployment and longer power generation and transmission build-out timelines could shift costs to end-consumers.

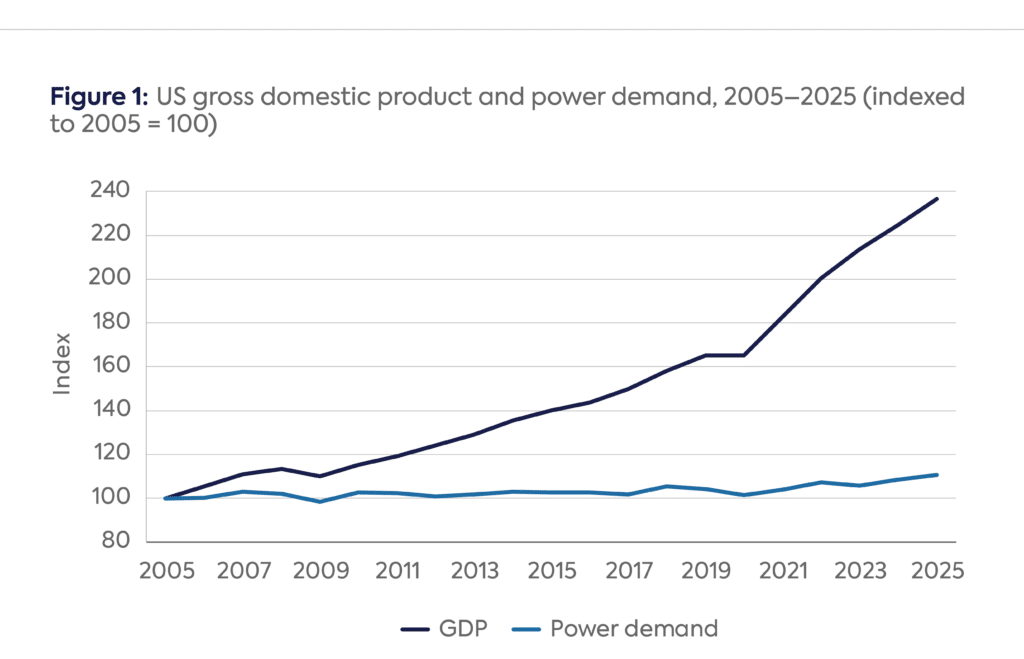

Electric load growth is becoming a particularly important driver of recent electricity price increases. Over the past two decades, US electricity demand showed little growth even as the US economy more than doubled in size. Between 2005 and 2025, the US gross domestic product (GDP) grew by 4.4 percent annually, yet total annual electricity increased by only 0.5 percent on average (Figure 1).[v] This limited growth persisted despite a rapid increase in data center energy consumption associated with the wide-scale adoption of the internet across the US economy.[vi] Data center–related power demand grew by 24 percent between 2005 and 2010, after which it stabilized at less than 2 percent of total US electricity consumption through 2015, largely due to efficiency improvements in computing and cooling.[vii] Taken together, electricity demand and economic growth became increasingly decoupled as the US economy became less electricity-intensive, reflecting gains in energy efficiency as well as structural changes in the economy, including a decline in manufacturing and a growing share of services.[viii]

Source: US Energy Information Administration, Electricity Data Browser, https://www.eia.gov/electricity/data/browser/#/topic/5?agg=0&geo=g&linechart=ELEC.SALES.US-ALL.A&columnchart=ELEC.SALES.US-ALL.A&map=ELEC.SALES.US-ALL.A&freq=A&ctype=linechart<ype=pin&rtype=s&maptype=0&rse=0&pin=; Federal Reserve Bank of St. Louis, Gross Domestic Product, https://fred.stlouisfed.org/series/GDP

However, this period of flat demand has recently given way to a new era of growth.[ix] Since 2019, US electricity demand has increased by 6 percent, from 3,813 terawatt-hours (TWh) in 2019 to 4,051 TWh in 2025.[x] Unlike the muted growth during most of the 2010s, electricity load growth reached 2.6 percent in 2024, and preliminary data suggests a similar figure for 2025.[xi] In 2024, electricity demand increased across all sectors, though commercial demand grew the most at 3 percent, reflecting in part rising electricity consumption from data centers.[xii] Industrial and residential demand followed, growing by 2.5 percent and 2 percent, respectively.[xiii]

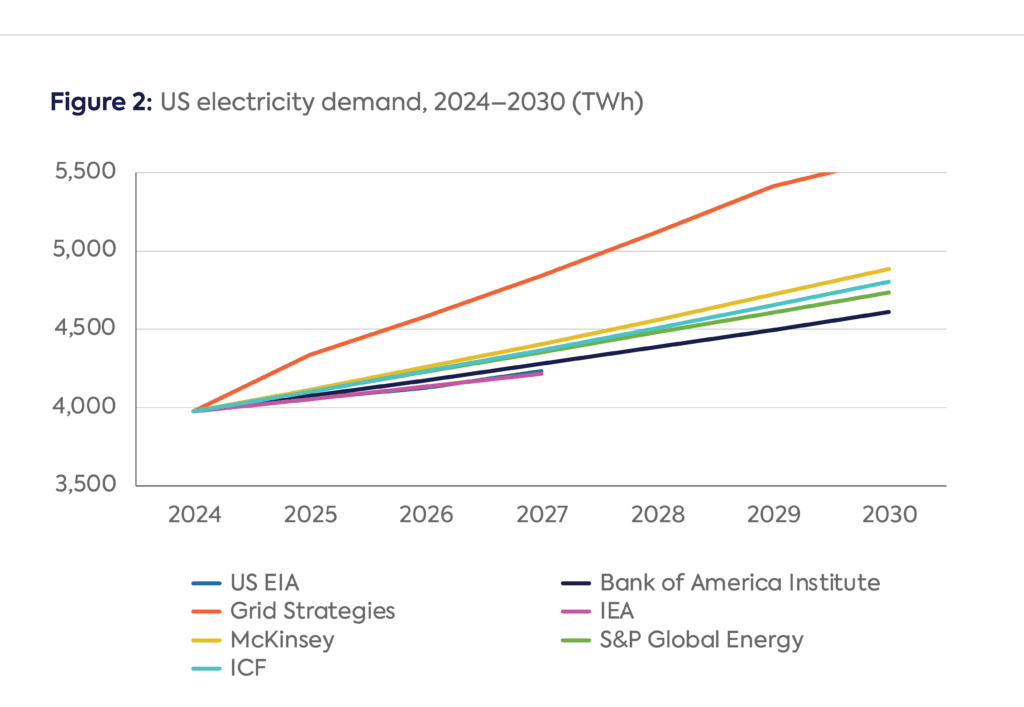

Leading analysts expect this trend to intensify in the short term. The latest short-term energy outlook from the US Energy Information Administration (EIA), for instance, forecasts total electricity retail sales to exceed 4,230 TWh in 2027, roughly 10 percent higher than in 2023.[xiv] This growth is expected to be concentrated in Texas and the mid-Atlantic, whose electricity grids are primarily managed by the Electric Reliability Council of Texas (ERCOT) and PJM Interconnection, respectively. The EIA projects that annual growth in ERCOT could grow by as much as 14 percent in 2026, while demand in PJM, which spans 13 states including Virginia, could increase by 4 percent during the same year, driven mostly by rising power demand from data centers.[xv]

Other analysts project even greater growth. One study argues that 2023 represented a structural shift, with utilities’ five-year load growth forecast filed with the Federal Energy Regulatory Commission (FERC) nearly doubling in a single year, from 2.6 percent in 2022 to 4.7 percent in 2023. Using a method that aggregates bottom-up utility filings submitted to FERC rather than top-down econometric models, the study suggests electricity usage will grow by an average of 4.7 percent annually over the next five years.[xvi]

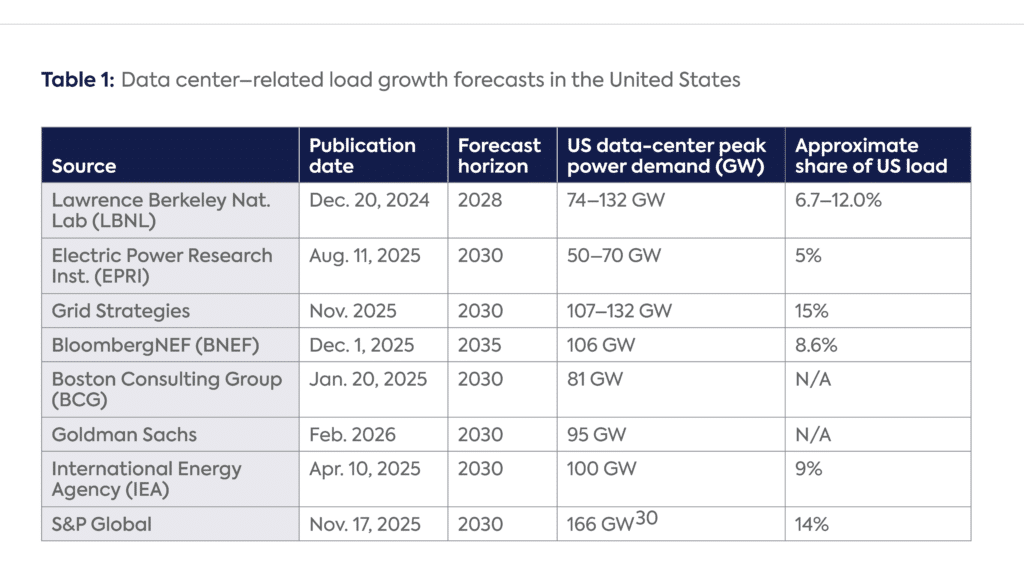

Overall load growth implies the need for more power, measured in terawatt-hours. However, the temporal profile of demand (daily, weekly, seasonal) is critical to understand because expected peak loads have direct implications for generation assets, the transmission grid, operations, reliability, and resource adequacy—all critical considerations for customers, utilities, grid operators, regulators, financiers, and other key stakeholders. Moreover, while estimates of load growth can change significantly during the period in question, the scale of projected load growth has increased dramatically over the past four years. Some analyses have revised five-year peak demand growth forecasts upward nearly seven-fold over just three years.[xvii] In 2021, utilities expected to add 24 gigawatts (GW) of installed capacity to meet new peak demand growth over the following five years; by 2024, that forecast jumped to 166 GW.[xviii]

Load growth is also attributable to multiple sources: Rising data center demand is the dominant contributor to the 2024 growth forecast, accounting for around 90 GW (55 percent of the total);[xix] approximately 30 GW (20 percent) is projected to come from industrial and manufacturing expansion driven by onshoring trends and new factory construction;[xx] residential and general commercial growth, including building electrification and electric vehicle charging, contribute roughly 30 GW (20 percent); and the electrification of heavy industry—specifically oil, gas, and mining—accounts for around 10 GW (5 percent).[xxi]

The current surge in data center demand contrasts with the previous two decades of limited electricity demand growth, when efficiency gains across the residential, commercial, and industrial sectors enabled continued productivity growth with limited additional electricity consumption. As a percentage of total US electricity demand, data center electricity use rose from 1.9 percent in 2018 to 4.4 percent in 2023.[xxii] By 2028, it is forecasted to reach between 6.7 percent and 12 percent—equivalent to 325–580 TWh, or roughly two to three times 2023 levels.[xxiii] Data center load growth is not geographically uniform. It is expected to remain highly concentrated in regions such as Northern Virginia, Texas, and Ohio.[xxiv] This concentration creates the risk of acute, localized grid constraints that are obscured by national averages.

Source: US Energy Information Administration, Short-Term Energy Outlook Supplement: Comparison of Energy Forecasts, accessed May 15, 2026, https://www.eia.gov/outlooks/steo/pdf/compare.pdf; Bank of America Institute, The Electricity Grid and the U.S. Economy (Charlotte, NC: Bank of America Institute, 2024), https://institute.bankofamerica.com/content/dam/transformation/us-electrical-grid.pdf; Grid Strategies LLC, National Load Growth Report 2025 (Washington, DC: Grid Strategies LLC, 2025), https://gridstrategiesllc.com/wp-content/uploads/Grid-Strategies-National-Load-Growth-Report-2025.pdf; International Energy Agency, “Demand,” in Electricity 2025 (Paris: International Energy Agency, 2025), accessed May 15, 2026, https://www.iea.org/reports/electricity-2025/demand; McKinsey & Company, “Powering a New Era of U.S. Energy Demand,” accessed May 15, 2026, https://www.mckinsey.com/industries/public-sector/our-insights/powering-a-new-era-of-us-energy-demand#/; American Clean Power Association, U.S. National Power Demand Study: Executive Summary (Washington, DC: American Clean Power Association, 2025), https://cleanpower.org/wp-content/uploads/gateway/2025/03/US_National_Power_Demand_Study_2025_ExecSummary_FINAL-v2.pdf; ICF, The Future of U.S. Power Demand: ICF Energy Demand Report 2025 (Reston, VA: ICF, 2025), https://www.icf.com/-/media/files/icf/reports/2025/energy-demand-report-icf-2025_report.pdf.[xxv]

While most forecasts envision strong electricity demand growth and substantial capacity additions in the United States through 2030, projected capacity additions vary widely, ranging from as little as 50 GW[xxvi] to more than 125 GW (Table 1).[xxvii] In terms of load growth, the IEA projects that data centers will account for nearly half of electricity demand growth between 2025 and 2030.[xxviii] This high variability reflects both ongoing uncertainty and methodological differences, including bottom-up versus top-down approaches, nameplate capacity versus assumed utilization rates, and reliance on utility interconnection queues versus individually tracked projects.[xxix]

Source: Arman Shehabi et al., “2024 United States Data Center Energy Usage Report,” Lawrence Berkeley National Laboratory, 2024, https://doi.org/10.71468/P1WC7Q; James You, David Owen, Daniel Porter, and Tom Wilson, “Scaling Intelligence: The Exponential Growth of AI’s Power Needs,” EPRI and Epoch AI, 2025, https://www.epri.com/research/products/000000003002033669; BloombergNEF, “AI and the Power Grid: Where the Rubber Meets the Road,” BloombergNEF, 2025, https://about.bnef.com/insights/clean-energy/ai-and-the-power-grid-where-the-rubber-meets-the-road/; Virginia Lee et al., “Breaking Barriers to Data Center Growth,” Boston Consulting Group, 2025, https://web-assets.bcg.com/pdf-src/prod-live/breaking-barriers-data-center-growth.pdf.[xxx]

Similarly, computing already accounts for 8 percent of commercial sector electricity consumption in the United States and is projected to surpass space cooling as the primary driver of commercial electricity use by 2048, potentially reaching as high as 20 percent by 2050.[xxxi] This rapid growth has been driven by the expansion of data center services into areas such as AI and cryptocurrency, which require specialized and more energy-intensive hardware. The increased deployment of graphics processing unit (GPU)–accelerated servers for AI has in and of itself contributed to a more than doubling of data center energy demand between 2017 and 2023, despite continued energy efficiency improvements.[xxxii] This combination of reindustrialization, electrification, and digital infrastructure expansion is projected to drive annual electricity demand growth of between 2 percent and 6 percent over the next five years,[xxxiii] raising important questions about the implications for retail electricity prices.

US electrical utilities fall into three main categories distinguished by their operating, financial, and regulatory characteristics: investor-owned utilities (IOUs), public power municipal utilities, and rural electric cooperatives.[xxxiv] While the latter two are public, IOUs are private, investor-owned, for-profit companies regulated by state public utility commissions (PUCs).

Utility prices have traditionally been set through cost-of-service recovery (COSR), a regulatory mechanism that allows vertically integrated utilities to recover prudent expenditures and earn a regulator-approved rate of return commensurate with the risks they face.[xxxv] PUCs conduct legal proceedings called rate cases to determine a utility’s rate base, which represents the value of physical capital assets in service minus accumulated depreciation. The total revenue a utility is allowed to collect is calculated by multiplying this rate base by a regulator-approved rate of return of the utility’s assets (power plants, transmission lines, substations, etc.) and then adding operating expenses such as fuel charges, operations and maintenance, and taxes. These total costs are then allocated to customers through rate design, which typically includes fixed connection charges and volumetric charges based on energy consumption.[xxxvi]

This ratemaking process has elicited concerns about transparency and fairness,[xxxvii] particularly in places where average electricity prices have increased significantly. Information asymmetry between utilities and PUCs, and especially between utilities and customer advocates, has been found to disproportionally impact lower-income households. States such as California and New York are attempting to counteract this asymmetry by incorporating equity considerations into their regulatory schemes.[xxxviii]

In deregulated markets, the power generation segment is unbundled from transmission and distribution, allowing independent generators to set prices competitively.[xxxix] Independent system operators (ISOs) manage wholesale markets, with generators submitting bids reflecting their marginal cost of electricity production for day-ahead or real-time delivery. Generators are dispatched in order of increasing cost, with the lowest-cost units serving demand first until it is satisfied. The bid of the final unit required to meet demand sets the market price, which is paid to all dispatched generators.

COSR and competitive markets frequently operate simultaneously within the modern US electricity system, with final prices varying by state.[xl] While many regions have restructured their electricity market to introduce competition in generation, distribution systems remain natural monopolies and are typically regulated under COSR frameworks to ensure asset owners can recover prudent expenditures and achieve a return on their investments.

Consequently, ISOs may manage competitive wholesale auctions for electricity and capacity while PUCs oversee regulated rates for the retail delivery infrastructure. This results in an overlapping set of regulatory structures in which different pricing mechanisms apply to different segments of the same supply chain in an attempt to balance economic efficiency with system reliability.

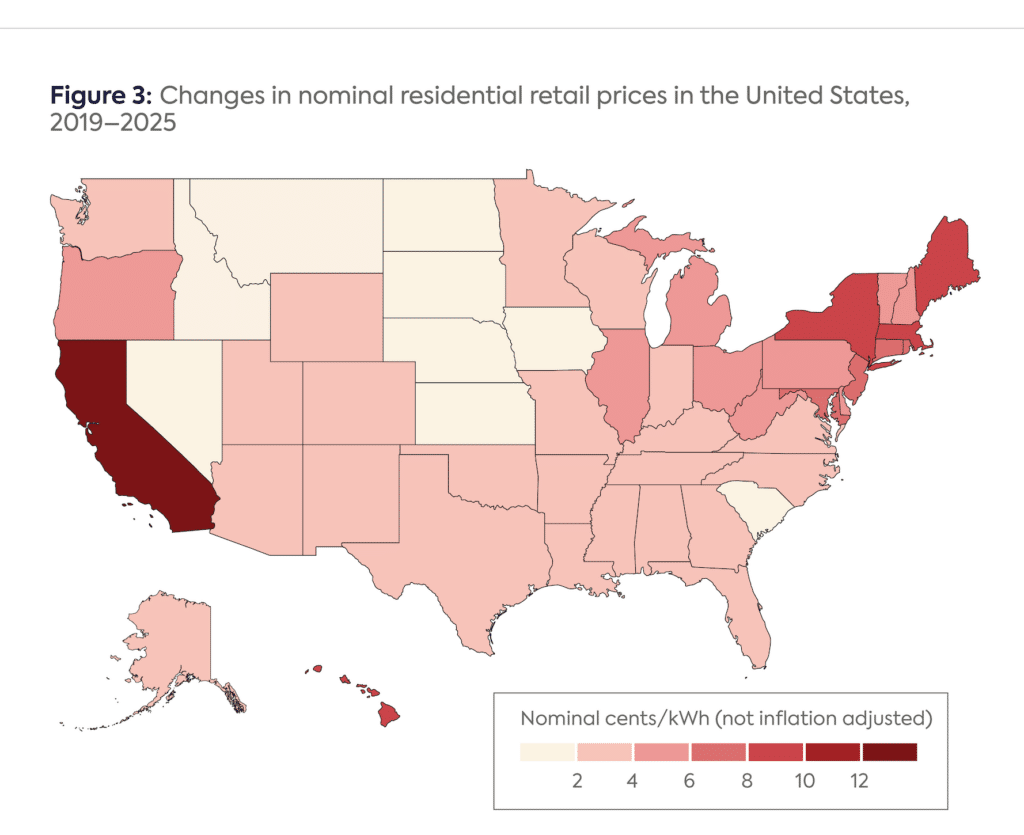

The surge in demand has complex effects on electricity prices. In 2025, average nominal retail prices ranged from under 9 cents per kilowatt-hour (kWh) in North Dakota to over 27 cents per kWh in California. Nationally averaged nominal electricity prices increased by over 29 percent between 2019 and 2025 and by 32 percent since 2010.[xli] When looking specifically at nominal residential electricity prices, all states experienced increases, with the largest occurring in California (13 cents per kWh), Maine (9 cents per kWh), and Massachusetts (8 cents per kWh) (Figure 3).

Source: Ryan H. Wiser et al., “Retail Electricity Price Trends and Drivers: Data Update—2026 Edition,” Lawrence Berkeley National Laboratory, 2026, https://emp.lbl.gov/publications/retail-electricity-price-trends-and[xlii]

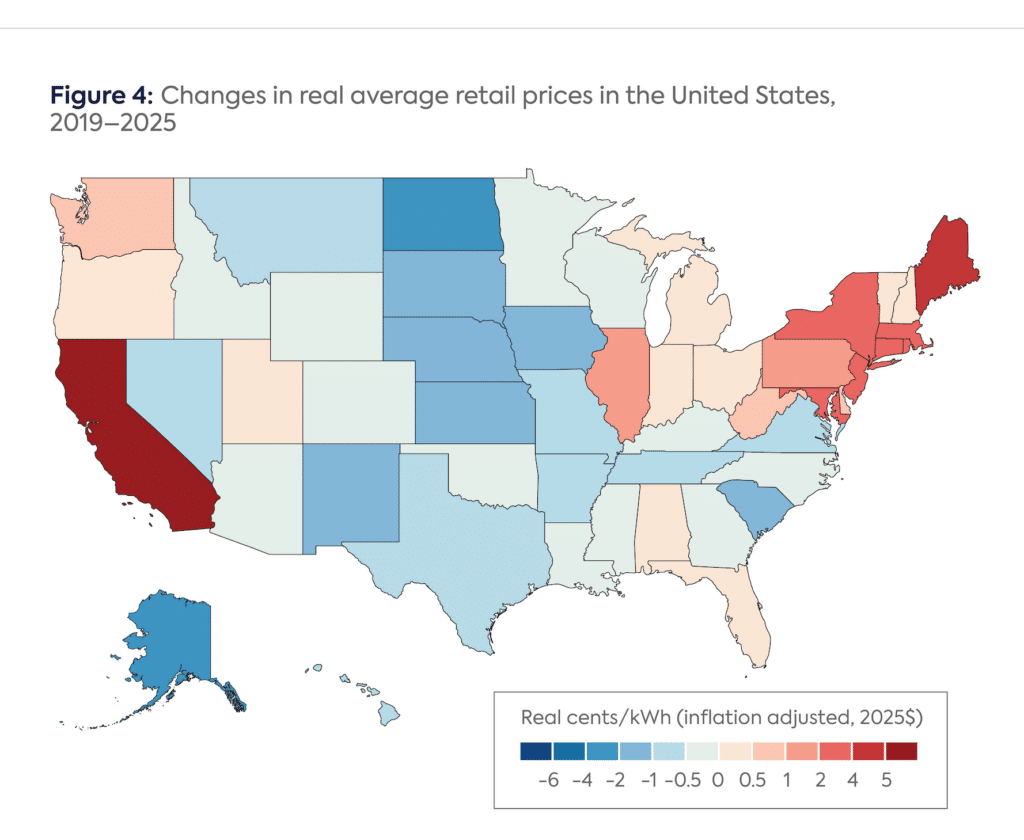

In inflation-adjusted terms, 23 states experienced real price declines between 2019 and 2025, while 27 saw real increases.[xliii] The latter were concentrated on the West Coast and in the Northeast, with California experiencing pronounced price growth (6.2 cents per kWh in real 2025 dollars). Taken together, these patterns indicate that price dynamics are highly uneven across states.[xliv]

Source: Ryan H. Wiser et al., “Retail Electricity Price Trends and Drivers: Data Update—2026 Edition,” Lawrence Berkeley National Laboratory, 2026, https://emp.lbl.gov/publications/retail-electricity-price-trends-and

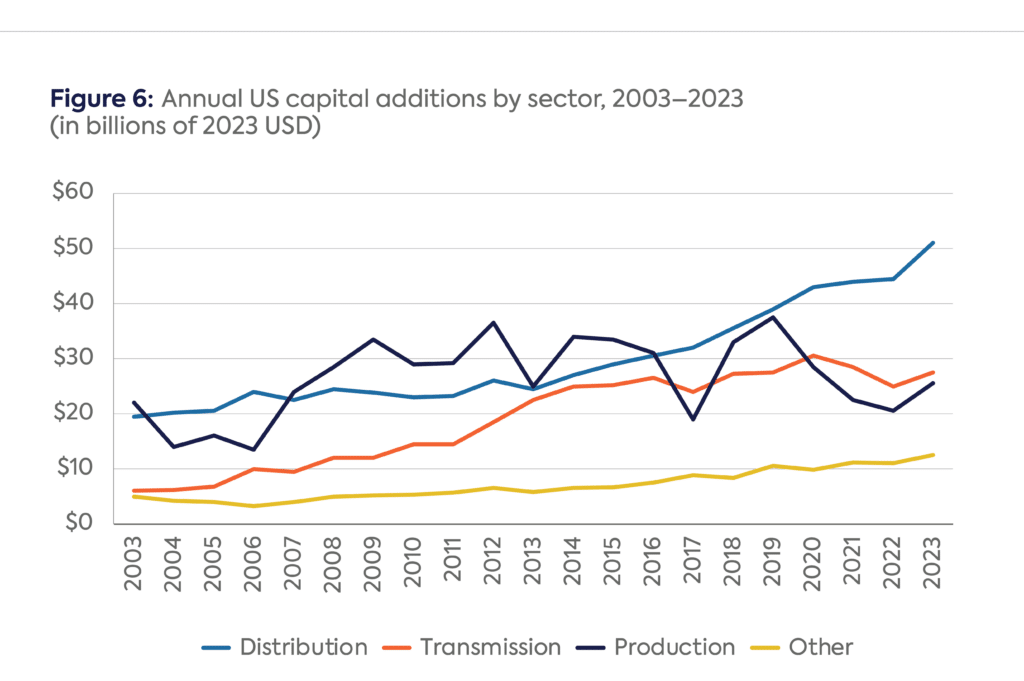

Natural disasters and extreme weather events have imposed significant short- and long-term costs on electricity consumers, particularly in vulnerable regions. Costs for repairing and rebuilding infrastructure have been substantial across the United States. In Florida, for example, residential prices rose by 1.2 cents per kWh to 3.2 cents per kWh following the 2024 hurricanes.[xlv] Proactive investments in infrastructure hardening and wildfire mitigation have become additional major price drivers in Western states. Capital investments in grids, especially distribution infrastructure but also transmission, rose by 50 percent between 2019 and 2023. In 2023, these investments represented the largest share of IOU capital expenditures, accounting for 43 percent of total spending, much of it for overhead poles, towers, and conductors.[xlvi] In California, wildfire-related expenses now account for approximately 17 percent of total utility revenue requirements, translating into an electricity price increase of roughly 4 cents per kWh.[xlvii] These localized impacts reflect the growing role of proactive infrastructure replacement and extreme weather mitigation in driving rates upward in highly affected regions.[xlviii]

Under the current system, utilities rely on ratepayers to fund maintenance, capital improvement, and expansion projects through higher electricity rates for consumers. In 2025, US IOUs requested rate base increases totaling a record $18.2 billion, compared with $8.2 billion in 2019 and just $6.8 billion in 2010.[xlix] Utilities have justified rate increase requests as necessary to fund upgrades to aging transmission and distribution (T&D) infrastructure; expanded renewable, fossil, and nuclear generation capacity to meet rising electricity demand; and preparation for extreme weather events.[l]

Figure 5: Changes in nominal residential retail prices in the United States, 2019–2025

Source: Dan Lowrey, “Record Amount of Utility Rate Requests in 2025 amid Affordability Concerns,” S&P Global, January 23, 2026, https://www.spglobal.com/market-intelligence/en/news-insights/research/2026/01/record-amount-of-utility-rate-requests-in-2025-amid-affordability-concerns.

A case in point of this dynamic is Maine, where T&D costs are rising due to a combination of aging infrastructure requiring replacement, new transmission projects, and inflationary pressures on equipment and construction that have substantially outpaced general inflation over the last decade.[li] A significant increase in the global cost of essential materials like copper—up approximately 50 percent since 2016—has compounded these pressures, alongside growing storm-related repair and grid-hardening costs. Recovery from the state’s 2024 winter storms alone is costing the average Central Maine Power residential customer about $20 per month.[lii]

Capital spending on the distribution system—the local poles and wires delivering electricity to end-users—has overtaken production and transmission as the primary driver of utility capital expenditures. Between 2003 and 2023, annual capital investment in distribution infrastructure rose by 160 percent, reaching $50.9 billion in 2023.[liii] This surge is driven not by expansion into new geographic areas but by the need to replace and harden existing systems against extreme weather and to integrate intermittent renewable resources.

The US power grid now faces increasing pressure from localized, high-density demand from AI compute clusters and industrial electrification. This comes as much of the system is aging: 70 percent of power transformers are 25 years or older, 60 percent of circuit breakers are 30 years or older, and 70 percent of transmission lines are 25 years or older.[liv] Together, these factors are propelling increased real-term capital investment in the modernization and expansion of T&D networks.

Source: US Energy Information Administration, “Grid Infrastructure Investments Drive Increase in Utility Spending over Last Two Decades,” November 18, 2024, https://www.eia.gov/todayinenergy/detail.php?id=63724.

Fuel price fluctuations, particularly natural gas prices, remain among the most volatile factors of year-to-year electricity price variation in the United States. Because natural gas accounts for 43 percent of US electricity generation, price spikes—such as those following the onset of the Russia-Ukraine war—pass through to consumers via fuel adjustment riders.[lv] When natural gas prices decrease, however, the associated electricity price reductions translate into rate reductions more slowly and less sharply due to several factors, including the role of natural gas as the marginal generator, regulatory lags, and utilities hedging in fuel purchase contracts. Evidence suggests that states with a higher reliance on natural gas for power generation consistently experience greater year-to-year variability in retail electricity prices.[lvi]

Along similar lines, analysis indicates that fuel and purchased power costs were the single largest driver of price increases in the early 2000s, accounting for approximately 95 percent of utility cost increases.[lvii] Separate analysis suggests that this dynamic has persisted over the past two decades, with natural gas–based generators often setting the marginal price of electricity in wholesale markets.[lviii] In consequence, consumers remain economically linked to gas price volatility.

Regarding the impact of renewable energy on electricity prices in the United States, it has been variable over time, depending largely on whether the deployment is market-based or policy-driven. Some evidence suggests that market-based utility-scale wind and solar deployment has reduced retail electricity prices over the past five years.[lix] However, in some states, renewable portfolio standard (RPS) programs with solar carve-outs have increased retail prices by an average of 0.25 cents per kWh, with significant variations in magnitude across states.[lx] Important knowledge gaps concerning the conditions under which higher renewable penetration rates and RPS policy design shape retail prices across regions remain.[lxi] Additionally, net energy metering (NEM) for rooftop solar can increase prices for nonadopters because utility fixed infrastructure costs are spread over a smaller base of electricity sales. In California, the impact of NEM solar on retail prices is estimated to be as high as 2.5 cents per kWh.[lxii]

Electricity load growth has traditionally been correlated with lower electricity prices because fixed grid costs can be spread over a larger volume of electricity sales. However, some analysts have suggested that recent rapid and concentrated AI data center and manufacturing demands are tightening supply markets and causing capacity prices to spike.[lxiii] Separate analysis suggests that power demand growth can lead to average price declines, but only when the incremental costs of serving new load are lower than current average costs, under appropriate cost allocation across customer classes.[lxiv]

In nearly all US jurisdictions, new load growth must be met with investments in new generation, transmission, and distribution infrastructure, the marginal costs of which have risen due to factors including elevated equipment prices and expiring tax credits. When the marginal cost of serving the new load exceeds the average cost of electricity, if costs are allocated uniformly across the rate base, adding generation and transmission to serve higher loads increases average electricity costs.[lxv] That said, some studies indicate that at least a share of incremental load growth (equivalent to around 260 GW) can be met through a range of measures that may be more cost-effective and faster than building an equivalent amount of new capacity generation.[lxvi] These measures include energy efficiency improvements, especially in buildings; virtual power plants; grid-enhancing technologies and advanced conductors; and the use of existing grid connections from decommissioned power plants to build cheaper and cleaner capacity.[lxvii]

However, evidence from 2019–2024 shows that states with faster load growth generally experienced smaller price increases or even real price declines.[lxviii] This is largely because current T&D expenditures are driven primarily by the refurbishment of existing infrastructure rather than new infrastructure build-out. Consequently, higher loads allow fixed costs to be spread over a larger customer base, reducing average electricity prices, albeit to varying degrees across customer classes depending on specific ratemaking policies and regulatory frameworks in different US jurisdictions.[lxix] Even when new generation is more expensive than older, fully depreciated plants, new large loads can benefit existing ratepayers by helping to spread the costs of generation portfolio modernization that utilities would undertake regardless of new demand.

In some wholesale electric markets, capacity markets are used to assure sufficient capacity is available to serve load and meet regulated reliability requirements. Capacity markets set a price for a supplier’s commitment to meet future electricity needs, in contrast to being paid only for the energy produced.[lxx] On paper, capacity market auctions are mechanisms that aim to have sufficient available electricity for future demand at the lowest achievable price for consumers. The goal is to signal to generators to build additional generation infrastructure. However, in the PJM Interconnection, the summer 2025 capacity auction saw clearing prices jump from $29 to $333 per megawatt (MW)-day, a historic high. This change is expected to increase retail electricity bills for ratepayers in states including Maryland, New Jersey, and Pennsylvania.[lxxi] In practice, this risks prematurely locking in elevated future capacity prices based on anticipated load growth that may never materialize, with the resulting costs borne by end-consumers. Rather than an investment signal for additional power generation infrastructure, the PJM’s latest capacity auction risks raising rates for end-consumers without increasing available power supply or enhancing related system infrastructure (e.g., transmission lines and equipment).

As discussed below, there are numerous approaches to addressing the increase in marginal generation, transmission, and distribution required to accommodate load growth, many of which ensure that large new loads pay the marginal cost of serving them, thereby avoiding cost transfers onto existing customers on the rate base. State governments and regulators are increasingly adopting proactive planning and innovative rate designs that assign incremental system costs and risks directly to large loads, limiting upward pressure on existing customer rates, including for the roughly 43 million households already struggling to pay utility bills and facing challenges in adequately heating or cooling their homes.[lxxii]

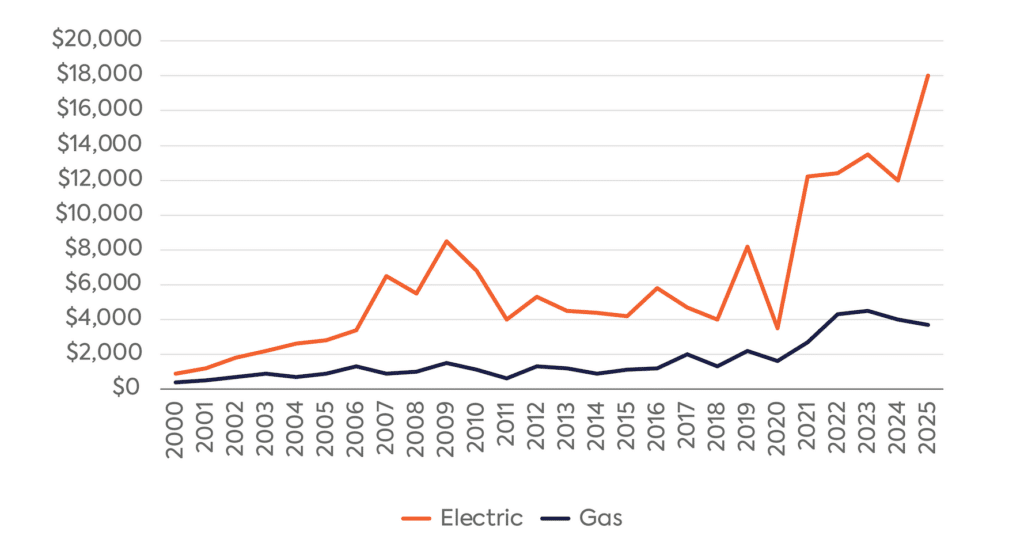

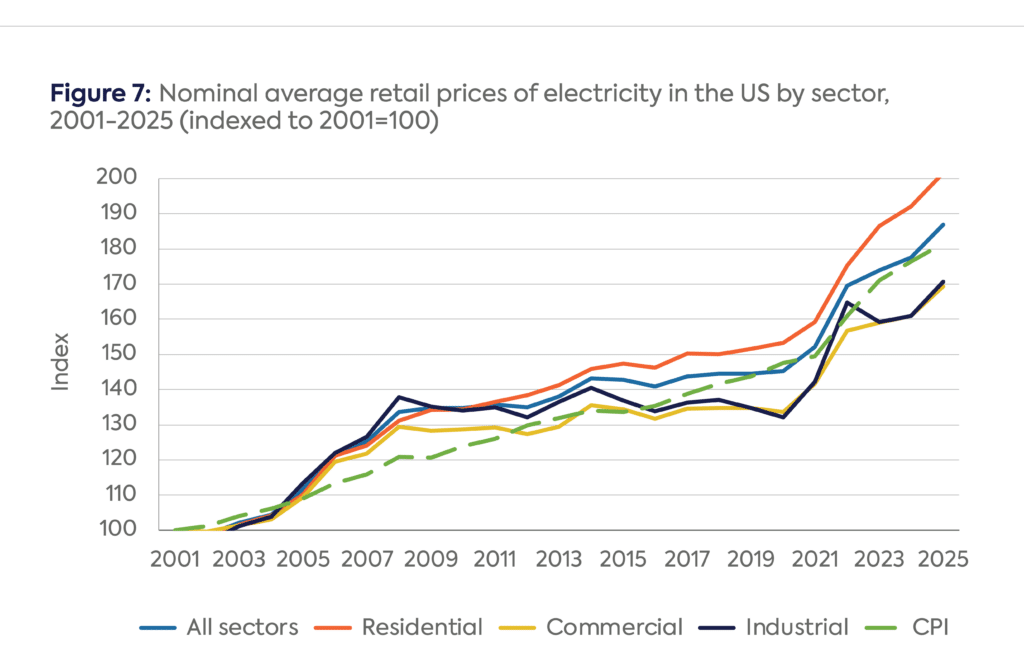

While the drivers described above explain recent trends, future load growth and its price effects in the short to medium term are evolving rapidly. Notably, residential consumers assess electricity costs by comparing their current bills with past bills, rather than with inflation-adjusted data or average national prices. Therefore, while inflation-adjusted data is useful to understand the macroeconomic context, nominal increase trends more closely reflect what end-consumers observe when paying their electricity bills (Figure 6). Consistent with this, even in inflation-adjusted terms, some states that had previously experienced declines, including Virginia and Texas, recorded increases in average retail electricity price increases in 2025 relative to 2024.[lxxiii]

This burden is particularly high for low- and middle-income households, as reflected in the fact that about 24 percent of US households were unable to pay their electricity bill in full in 2024.[lxxiv] Moreover, the share of households experiencing some form of energy insecurity, defined as the inability to adequately meet household energy needs, increased from 27 percent in 2020 to 33 percent in 2024.[lxxv] Compounding these circumstances, average electricity bills in states including New Jersey, Pennsylvania, and Maryland increased significantly in mid-2025,[lxxvi] while nominal residential electricity rates have risen significantly faster than commercial and industrial rates (27 percent versus 19 percent from 2019 to 2024).[lxxvii] Utility cost-allocation methods often shield large commercial users while requiring households to disproportionately fund grid modernization.[lxxviii] These factors help explain why electricity price increases for end-users have become an increasingly salient issue in policymaking in PUCs, state capitals, and Washington, DC.

Source: US Energy Information Administration, Electricity Data Browser, https://www.eia.gov/electricity/data/browser/#/topic/7?agg=0,1&geo=g&endsec=vg&linechart=ELEC.PRICE.US-ALL.A~ELEC.PRICE.US-RES.A~ELEC.PRICE.US-COM.A~ELEC.PRICE.US-IND.A&columnchart=ELEC.PRICE.US-ALL.A~ELEC.PRICE.US-RES.A~ELEC.PRICE.US-COM.A~ELEC.PRICE.US-IND.A&map=ELEC.PRICE.US-ALL.A&freq=A&ctype=linechart<ype=pin&rtype=s&pin=&rse=0&maptype=0; Federal Reserve Bank of St. Louis, Consumer Price Index for All Urban Consumers, https://fred.stlouisfed.org/series/CPIAUCSL.

Load growth from data centers is distinguished by its unprecedented scale, with individual facilities sometimes requiring as much electricity as a small city.[lxxix] The new data center campuses now being proposed, such as Meta’s AI clusters Prometheus (1 GW) and Hyperion (5 GW), are so large that their power requirements are comparable to the total installed generation capacity of small states, such as New Hampshire (4.5 GW).[lxxx] In California, the utility PG&E recently reported that its data center pipeline surged from 8.7 GW to 10 GW in only three months, illustrating the sheer volume of infrastructure needed to support the industry.[lxxxi]

As previously mentioned, total US data center electricity consumption has almost tripled over the last decade, reaching 180 TWh in 2024,[lxxxii] and is projected to increase further to between 320 and 600 TWh by 2028, depending on the estimate.[lxxxiii]

Analysis of data center impacts on electricity prices at a more granular spatial resolution indicates that spatial concentration is correlated with local price increases. This detail is not captured in literature that evaluates local prices rather than state prices, since the former are influenced by local marginal prices, which in turn reflect electricity delivery within local zones and include transmission congestion.[lxxxiv] Data comparing areas located near data centers with those more than 150 miles from them indicates that proximity to data centers is associated with local marginal price increases of up to 20 percent.[lxxxv] These findings suggest that transmission upgrades to accommodate greater power flow may be a significant determinant of local price impacts for grid-connected data centers.

While the continued rapid expansion of data centers appears likely, forecasts of that expansion’s scope vary widely due to factors including unpredictable build-out pace and demand for AI services, AI chip manufacturing constraints, and potential gains in AI system efficiency. This poses a significant challenge for planning, building, operations, and cost allocation. Further, whereas historical large loads had relatively predictable profiles—whether 24/7/365, structured around a five-day workweek, or seasonally variable—new load growth, particularly from data centers with high power demand and spatially concentrated consumption, increases spatial and temporal reliability and operational concerns. This is required both to meet demand and to manage loss of load, which has sometimes led to potentially impactful grid instability.[lxxxvi] System operators and regulators are increasingly examining the flexibility and configuration of these data centers, including on-site generation, backup generators, and uninterruptible power supply systems, to assess risks and vulnerabilities, marking a substantial shift in planning and operational approaches in the context of a grid originally designed for the more stable and predictable consumption patterns of traditional consumers.[lxxxvii]

Given this backdrop, the data center surge affects a wide range of factors that shape both competitive electricity markets and cost-of-service recovery outcomes. On the competitive market side, large and often inflexible data center loads directly shift aggregate demand upward, potentially increasing marginal prices as costlier and more inefficient power plants are dispatched and raising wholesale electricity prices, congestion rents, and the value of capacity and ancillary services needed to maintain reliability. The geographic concentration of data centers exacerbates transmission congestion, alters nodal price differentials, and can increase the need for new generation, storage, and transmission investments, which then feeds back into forward capacity auctions and long-run market expectations in markets that use these mechanisms.

On the COSR side, data centers contribute to substantial growth in the regulated rate base by requiring new high-voltage interconnections, substations, transmission upgrades, and grid hardening, all of which traditionally earn an authorized return through rates. The new loads also affect operating expenses through increased system planning, maintenance, and reliability obligations. Additionally, ratepayers may bear the costs of stranded assets if projected load growth fails to materialize.

Across both frameworks, data centers influence fuel procurement, reserve margins, congestion management, and system flexibility needs, while their scale and uncertainty introduce material risk into forecasts of demand growth, capital recovery, and average cost per customer, ultimately shaping cost allocation and the efficiency with which prices signal scarcity in the power system.

Recent analysis supports the argument that substantial load growth can, in some cases, reduce average retail rates by spreading high fixed costs across a larger base of electricity sales.[lxxxviii] For example, a recent study found that hyperscale data centers in California, Oregon, Virginia, and Mississippi have either a neutral impact on retail rates or the potential to generate “surplus value” though 2030, meaning they are expected to pay significantly more in utility rates than the marginal cost of serving them.[lxxxix] For a typical 100 MW data center, this surplus was approximately $3.4 million in 2025 and is projected to nearly double to $6.1 million by 2030.[xc] The study argues that because regulated utilities operate under a fixed revenue requirement, this excess revenue is distributed across users and “functions as a subsidy” for other customers.[xci] For example, in the case of PG&E, it estimates that every 1 GW of new data center load could reduce average household bills by 1 to 2 percent.[xcii] PG&E’s 10 GW data center pipeline could therefore lower household bills by over 10 percent by increasing utilization of the existing grid, which currently runs at only 45 percent capacity, and spreading maintenance costs over a larger volume of electricity consumption.[xciii]

However, realizing these benefits is far from easy; it requires regulators to implement rigorous rate design that “ring-fences” interconnection costs, ensuring that data centers pay up front for their specific grid upgrades rather than socializing those capital expenditures across residential ratepayers.

A recent report argues that utilities are incentivized to prioritize data center growth over the public interest, often shifting costs onto captive ratepayers through opaque mechanisms.[xciv] Challenging the rate-reducer hypothesis according to which higher loads can reduce electricity prices,[xcv] it identifies three primary avenues through which this cost shifting occurs:

1. Socialization of Infrastructure Costs: While data centers may pay for their direct connection to the grid (e.g., through a dedicated substation), they often do not bear the full cost of the deeper upstream system upgrades required to support their load. Utilities frequently classify major new transmission lines and power plant expansions as reliability upgrades or system benefits, rather than directly assigning them to the data center causing the need. This allows the utility to socialize these billions of dollars in capital expenditure across customer classes. The report argues that because utilities earn a guaranteed rate of return on capital investment, they have an incentive to overbuild infrastructure to serve data centers and then spread the resulting costs to residential customers, who have no choice but to pay.

2. The “Phantom Load” and Stranded Asset Risk: The study warns that utilities are building assets with 40–50-year lifespans to serve a technology sector—AI and data centers—characterized by uncertainty and future innovation over their actual energy demand in the long term. If AI demand fluctuates or efficiency gains significantly reduce power needs, as happened in the 2010s, new power plants and transmission lines risk becoming stranded assets. Unlike a traditional commercial business, whose shareholders bear investment risk, regulated utilities can pass the costs of poor investment decisions onto ratepayers over decades.

3. The “Black Box” of Special Contracts: Perhaps most critically, the report demonstrates that many data centers operate under confidential special contracts rather than public tariffs. These agreements often provide deep discounts to attract tech companies, undercutting the standard rates. Because they are shielded from public scrutiny by nondisclosure agreements, consumer advocates often cannot use them to verify whether data centers are actually covering their full share of costs. In fact, special contracts may shift costs to other ratepayers when the large-load customer pays the utility a price that is lower than the utility’s costs to serve that customer, effectively transferring that shortfall on to other ratepayers.[xcvi] According to the study, the opaque nature of the proceedings, the complexity and subjectivity involved in assessing the utility’s costs of serving a single consumer and political pressure to approve contracts pose a particular challenge to PUCs in identifying potential cost shifts.[xcvii]

Some of the cost-shifting risks identified by the study have already materialized as a financial reality. A separate analysis finds that in 2024 alone, ratepayers in 7 of the 13 PJM states, including Virginia and Ohio, were charged $4.3 billion for transmission projects required to connect data centers.[xcviii] The analysis suggests that utilities may exploit gaps between federal and state regulation to socialize the cost of new data center–related transmission and distribution infrastructure, allowing costs to creep into other consumers’ bills. This effectively forces residential households to subsidize the infrastructure of profitable tech corporations at a time when $2.5 billion in similar projects are pending for the coming year.[xcix] A recent report outlines a comprehensive suite of recommendations for utility commissions to mitigate these risks, emphasizing stricter cost-allocation frameworks, enhanced contract transparency, and proactive system-wide grid planning.[c]

As the scale of AI infrastructure grows, so does the risk that residential consumers will foot the bill for major grid upgrades.[ci] For example, PJM capacity prices surged from $29 per MW‑day for 2024 to $329 per MW‑day for 2026, before reaching a record high of $334 per MW‑day for 2027, reflecting anticipated increased capacity needs.[cii]

PJM’s 2026–2027 Base Residual Auction revealed a 6.6 GW shortfall in reliability reserves relative to the grid operator’s 20 percent installed reserve margin target, driven primarily by a 5.2 GW increase in forecasted demand attributed almost entirely to data centers.[ciii] The financial implications of this shortfall are significant: Without a temporary price cap negotiated by Pennsylvania Governor Josh Shapiro, prices would have reached nearly $530 per MW-day, with corresponding increases to residential electricity bills.[civ]

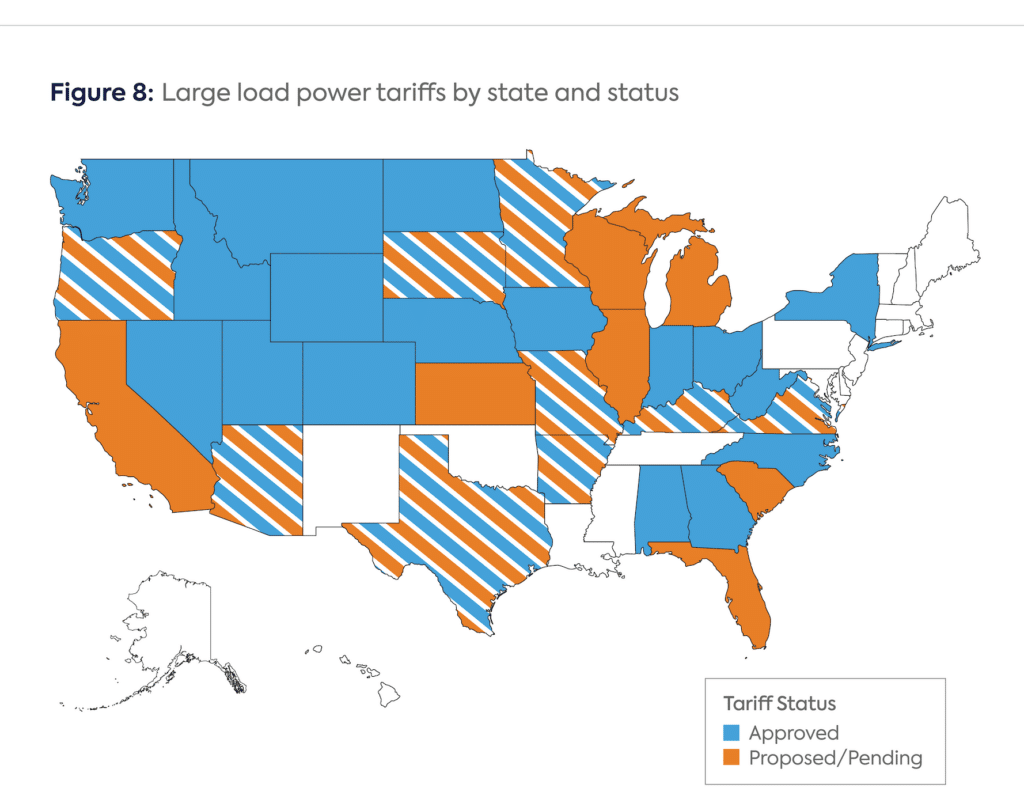

To prevent these costs from being passed through to residential bills, regulators and utilities are implementing new protective measures. For example, Delaware has paused all new interconnections over 25 MW while developing a dedicated large-load tariff intended to make data centers pay the full cost of their grid impacts,[cv] even though it may be difficult to demonstrate that specific grid upgrades or new power plants exclusively benefit a given data center;[cvi] Oregon has enacted a law requiring utilities to charge data centers a different rate from other industries;[cvii] Ohio is poised to end a moratorium on signing up new data centers as customers and to introduce a data center–specific tariff;[cviii] and at least six other states are pursuing similar actions.[cix] Even the nonprofit wholesale power supplier Tri-State Generation and Transmission Association has filed a regulatory tariff proposal with FERC based on the same logic.[cx]

Source: Source: Smart Electric Power Alliance (SEPA) and North Carolina Clean Energy Technology Center (NCCETC), Database of Emerging Large-Load Tariffs (DELTa), accessed May 11, 2026, https://sepapower.org/large-load-tariffs-database/.[cxi]

In January 2026, the Trump administration and a bipartisan group of 13 governors pressured PJM to adopt a strict “beneficiary-pays” model.[cxii] The proposal requires tech companies to bid on 15-year contracts to fund new power plants, with the aim of ensuring that these companies, rather than residential consumers, underwrite the infrastructure needed for data center construction.[cxiii]

On January 16, 2026, PJM released a decision that operationalizes the beneficiary-pays mandate through a new Expedited Interconnection Track for data centers that voluntarily finance and construct their own new generation, allowing them to bypass the backlogged interconnection queue.[cxiv] For large loads that cannot add supply, PJM introduced a “Connect and Manage” arrangement under which these facilities may be subject to curtailment amid system stress, including prioritized interruption or switching to backup generators during emergencies.[cxv] According to PJM, this structural change shields ratepayers by converting data centers from a passive drain on the grid into a flexible reliability buffer.[cxvi]

FERC has directed PJM, the nation’s largest grid operator, to establish transparent rules for colocation—the practice of siting large loads such as data centers directly at power plants to bypass transmission grid interconnections. This action followed a “show cause” proceeding in which FERC found PJM’s existing tariff to be “unjust and unreasonable” because it lacked clarity regarding the rates and conditions for these ”behind-the-meter” arrangements.[cxvii] By mandating the new rules, FERC aims to support technological advancement while mitigating price volatility for the 67 million Americans served by the PJM grid.[cxviii]

The order requires PJM to implement rules that prevent power generators from “leaving the grid” to serve a data center unless either the generator or the tech company finances the necessary transmission upgrades.[cxix] FERC’s aim is to ensure that the substantial costs of the infrastructure required to maintain reliable service for the general public are borne by the large-load customers rather than passed on to residential and small business ratepayers.[cxx]

Additionally, the ruling introduces a pathway for “interim, non-firm transmission service,” which could significantly accelerate data center deployment.[cxxi] This allows data centers to connect to a power plant and begin operations before the surrounding grid is fully strengthened, provided they accept being curtailed during periods of high grid stress or power shortages.[cxxii] While this specific order currently only applies to the PJM region, which serves 13 states and 67 million customers, it is viewed by industry observers as a critical starting point for broader federal rulemaking aimed at speeding up the integration of the AI industry into the national electricity landscape.

Interconnection queues are bottlenecks that delay the connection of new electricity resources, contributing to supply shortages and higher capacity costs. While data centers can often be constructed in just one to two years, connecting the necessary new generation to the grid currently averages five years, and major new transmission projects can take up to a decade.[cxxiii] This timing mismatch is further complicated by the extreme volatility of data center loads. For example, AI training models have been observed to reduce demand from 450 MW to 7 MW in just 36 seconds, creating unique operating challenges for grid reliability.[cxxiv]

To manage these queues more efficiently, regulators are transitioning to a “first-ready, first-served” cluster-based study process that prioritizes projects meeting strict readiness requirements.[cxxv] Key strategies include requiring an up-front entry fee tied to proactive transmission planning and providing developers with network upgrade cost certainty from the start of the process. Additionally, grid operators are encouraged to publish headroom maps, enabling well-prepared projects to claim existing capacity, gain access to capacity created by generator retirements, and proceed assuming no adverse impacts have been identified. Further efficiency gains are being pursued through optimization of the study processes. Moreover, improved construction reporting and collaboration with government agencies to address supply chain bottlenecks through cooperative procurement programs can reduce construction backlog.[cxxvi]

Bring-your-own capacity (BYOC) and flexible-grid connections can also help release interconnection queues by directly addressing the dual bottlenecks of transmission and generation constraints. It has been proposed that the simultaneous use of flexible-grid connection and BYOC can unlock faster and more affordable access to power with a ”connect now, operate flexibly” approach.[cxxvii] Flexible-grid connections bypass transmission delays by providing “conditional firm service,” which allows data centers to use grid power during normal conditions but rely on on-site resources such as batteries or load flexibility during rare periods of system stress. Simultaneously, BYOC overcomes generation shortfalls by allowing data centers to procure their own accredited capacity through clean energy power purchase agreements or on-site resources rather than waiting for multiyear utility planning or ISO queue processes.[cxxviii] Together, these solutions can enable data centers to reach full operation three to five years faster than traditional methods while maintaining grid reliability and ensuring that data centers, rather than other ratepayers, cover the incremental system costs.

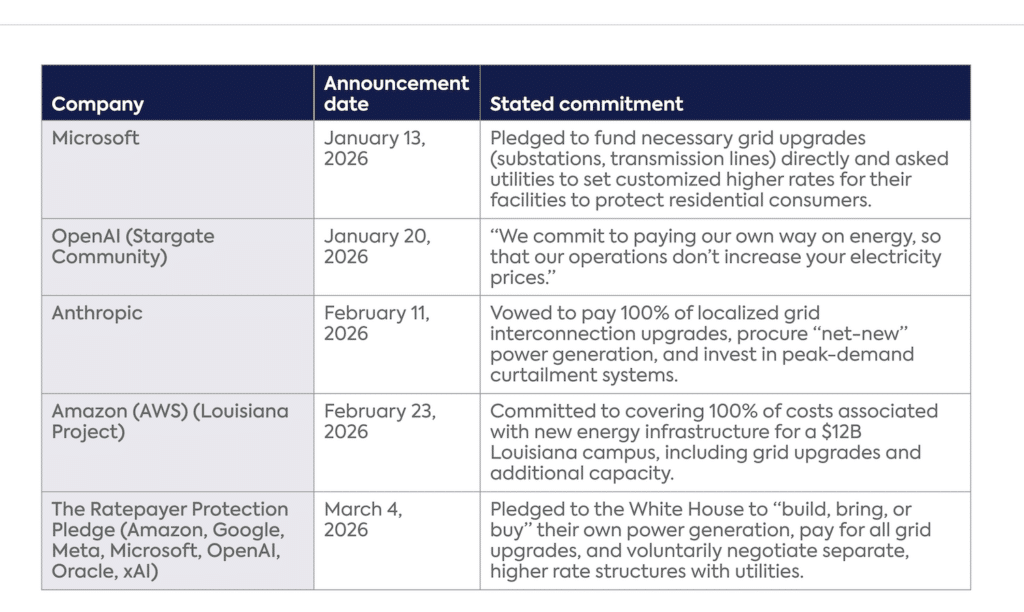

Recent data centers, particularly AI infrastructure, are increasingly being powered by significant investments in carbon-free energy sources such as solar, battery storage, and nuclear power. Some companies have also committed to fully funding necessary grid upgrades, including transmission lines and substations, in an attempt to shield local residents from shouldering these costs.[cxxix] These facilities provide positive community impacts by generating thousands of local construction and operational jobs, contributing millions in property taxes to fund essential public services such as schools, hospitals, and libraries, and providing free AI literacy and vocational training programs.[cxxx]

Brad Smith, “Building Community-First AI Infrastructure,” Microsoft On the Issues, January 13, 2026, https://blogs.microsoft.com/on-the-issues/2026/01/13/community-first-ai-infrastructure/; Anthropic, “Covering Electricity Price Increases from Our Data Centers,” February 11, 2026, https://www.anthropic.com/news/covering-electricity-price-increases; OpenAI, “Stargate Community,” January 20, 2026, https://openai.com/index/stargate-community/; Amazon, “Amazon Selects Louisiana for New Data Center Campuses, Creating Jobs and Investing in Local Infrastructure,” About Amazon, 2026, https://www.aboutamazon.com/news/company-news/amazon-data-center-louisiana-new-jobs; The White House, “Ratepayer Protection Pledge,” 2026, https://www.whitehouse.gov/releases/2026/03/ratepayer-protection-pledge/.

The Trump administration recently announced its Ratepayer Protection Pledge, which states that “the American people should not be footing the bill” for the massive energy and infrastructure needs of private data center companies.[cxxxi] Under this pledge, Amazon, Google, Meta, Microsoft, OpenAI, Oracle, and xAI are expected to build, bring, or buy all necessary new power generation resources and fully fund required infrastructure upgrades, ensuring these costs are not passed on to residential ratepayers.[cxxxii] Furthermore, the initiative requires companies to negotiate separate rate structures where they pay for power and related infrastructure regardless of whether they use the electricity, thereby shielding consumers from price hikes. Beyond direct financial protection, the White House intends to “benefit all ratepayers by leveraging these investments to increase the broader power supply and coordinate backup resources” that can help prevent blackouts and enhance grid resilience during periods of scarcity.[cxxxiii] That said, the pledge does not include specific accountability mechanisms, incentives, or penalties, relying instead on implementation via negotiations between the companies, utilities, and state regulators.

At the congressional level, a series of recently proposed bills aims to shield residential consumers from rising electricity prices and require data center developers to pay for the electricity infrastructure upgrades needed to meet rising energy demand. In January 2026, Democratic Maryland Senator Chris Van Hollen sponsored the “Power for the People Act of 2026,” intended to “promote the creation of data center load queues and data center-specific rate classes to mitigate the impact of data centers on other electricity consumers, and for other purposes.”[cxxxiv] If passed, the bill would direct FERC to create a data center load queue system, require data centers to pay for grid upgrades needed to connect them to the transmission and distribution grids, encourage new rate classes specific to data centers, and incentivize data centers to bring their own generation, among other priorities.[cxxxv]

The following month, the bipartisan “Guaranteeing Rate Insulation from Data Centers (GRID) Act” was introduced by Republican Senator of Missouri Josh Hawley and Democratic Senator of Connecticut Richard Blumenthal. The proposed act would require data centers to ensure the prioritization of residential ratepayers[cxxxvi] and would prohibit facilities larger than 20 MW from connecting to the grid unless they obtain a “Zero Rate Effect Certificate,” obligating them to demonstrate that they do not increase prices for other customers.[cxxxvii]

Beyond these two main bills, the “Power for the People Act” was introduced by Van Hollen in the Senate,[cxxxviii] and Democrat Paul Tonko introduced companion legislation in the House of Representatives. Similarly, although not a bill, Democratic Senator Elizabeth Warren and Republican Senator Josh Hawley, in a bipartisan effort, called on the EIA to implement mandatory energy-use reporting for data centers.[cxxxix]

Additional promising solutions have also emerged recently, including technology developments and efficiency gains enabled by greater flexibility in data center power demand. According to NVIDIA, the company’s efforts to increase energy efficiency center on shifting from general-purpose computing to accelerated computing platforms in order to achieve “great scale and efficiency.”[cxl] NVIDIA claims that a primary driver of this efficiency is the Blackwell platform, which is designed to run real-time generative AI at up to 25 times less energy consumption than its predecessor. Furthermore, all server designs must pass the NVIDIA-certified systems program, which includes rigorous “power consumption evaluations” to ensure that components function efficiently within the server.[cxli]

In collaboration with Schneider Electric, NVIDIA has also integrated energy efficiency into its infrastructure blueprints as a foundational design principle to support sustainability goals. These designs seek to address the limitations of traditional cooling through customized technologies. One example is the Controls Reference Design (CRD1), which provides a framework for “precise, real-time management of critical power and cooling resources.” According to NVIDIA, these efforts are intended to enhance operational efficiency and prevent power overloads.[cxlii]

Considering the forecasts for data center electricity demand, the Electric Power Research Institute’s (EPRI) Data Center Flexible Load Initiative (DCFlex) aims to create a blueprint for integrating data center with the grid and achieving grid reliability, resilience, and affordability for all electricity consumers by establishing “flexibility hubs” as living laboratories. The initiative is structured into specialized workstreams focused on developing data center design specifications informed by grid needs, testing distributed generation and storage capabilities, and creating equitable program structures to attract flexible loads.[cxliii]

While average US electricity prices were relatively stable or declined relative to inflation from 2019 to 2024, in 2025 the average residential retail price of electricity in the United States increased by more than twice the rate of inflation. Across states, power price changes during this period were driven primarily by investments in distribution and transmission networks, fuel volatility, routine maintenance, and policy mandates rather than load growth. The available data and literature show that through 2030 and beyond, electricity demand is set to keep growing, albeit with significant uncertainty regarding scope. This growth will be driven mostly by rising energy needs from AI data centers as well as the electrification of demand uses and manufacturing. This dynamic is exposing and exacerbating existing challenges related to how the electricity system’s planning, regulatory framework, infrastructure build-out, and costs are allocated.

Future price trajectories will depend on regulatory frameworks, cost-allocation mechanisms, and the extent to which new demand requires the build-out of higher-cost infrastructure relative to existing systems. Investments in additional climate hardening for distribution grids, along with transmission and generation costs associated with data centers, are likely to increase residential electricity rates and bills.

Faced with these risks, regulators and system operators will need to carefully devise policies that can meet rising power demand needs while preventing large-load growth from translating into higher residential electricity prices. To date, policy actions have focused on beneficiary-pays principles that explicitly assign infrastructure costs to the loads that create them. Certain state level actions, new PJM tariff mechanisms, and federal intervention by FERC require data centers to finance new generation and transmission upgrades and even accept curtailment risks, such as in PJM.

Yet these measures can only be effective if they are implemented through sustained coordination among regulators, grid operators, utilities, technology firms, and policymakers. The mismatch between the speed of data center deployment and the much longer timelines for generation and transmission expansion makes isolated interventions insufficient. Policy and regulatory frameworks can first aim at optimizing the existing system, including through large-load flexibility, energy efficiency measures, demand-side response, and grid-enhancing technologies. Additional reforms that can help achieve the speed and scale of the desired build-out while maintaining affordability and reliability include interconnection queue reform, expedited transmission planning and siting, market design improvement, and permitting reform. To limit higher electricity prices for ratepayers, these measures will likely need to move in tandem to prevent costs or risks from shifting across the system, especially onto residential customers.

Alexopoulos, T. A. “The Growing Importance of Natural Gas as a Predictor for Retail Electricity Prices in US.ˮ Energy (2017): https://doi.org/10.1016/j.energy.2017.07.002.

Amazon. “Amazon Selects Louisiana for New Data Center Campuses, Creating Jobs and Investing in Local Infrastructure.” About Amazon, February 23, 2026. https://www.aboutamazon.com/news/company-news/amazon-data-center-louisiana-new-jobs.

Ambrose, A. “Why Are New Jersey’s Electricity Bills Going Up, and What Does PJM Have to Do With It?ˮ 2025. New Jersey Policy Perspective. https://www.njpp.org/publications/explainer/why-are-new-jersey-electricity-bills-going-up-and-what-does-pjm-have-to-do-with-it/.

American Society of Civil Engineers. “2025 Infrastructure Report Card.ˮ 2025. https://infrastructurereportcard.org/wp-content/uploads/2025/03/Full-Report-2025-Natl-IRC-WEB.pdf.

Bank of America Institute. “Power Check: Watt’s Going on with the Grid?” 2025. https://institute.bankofamerica.com/content/dam/transformation/us-electrical-grid.pdf.

Basheda, G., M. W. Chupka, P. Fox-Penner, J. P. Pfeifenberger, et al. “Why Are Electricity Prices Increasing?ˮ Edison Foundation. 2006. https://www.brattle.com/wp-content/uploads/2017/10/6273_why_are_electricity_prices_increasing_basheda_et_al_eei_june_2006.pdf.

Batra, L, D. Harris, G. Katsigiannakis, J. Mackovyak, et al. Rising Current: America’s Growing Electricity Demand. Fairfax, VA: ICF, 2025. https://www.icf.com/-/media/files/icf/reports/2025/energy-demand-report-icf-2025_report.pdf.

Behr, P. “FERC Delivers Firm Guidance on Electricity to AI Industry.ˮ E&E News. 2025. https://www.eenews.net/articles/ferc-delivers-firm-guidance-on-electricity-to-ai-industry/.

BloombergNEF. “AI and the Power Grid: Where the Rubber Meets the Road.” BloombergNEF, December 1, 2025. https://about.bnef.com/insights/clean-energy/ai-and-the-power-grid-where-the-rubber-meets-the-road.

Bradford, T. “The Energy System: Technology, Economics, Markets, and Policy.ˮ 2018. MIT Press.

Brancucci, C., D. Cutler, E. Elgqvist, J. Jenkins, et al. “Flexible Data Centers: A Faster, More Affordable Path to Power.” Camus Energy, encoord, and Princeton University ZERO Lab, December 2025. https://www.camus.energy/flexible-data-center-report.

Carlini, S. “NVIDIA Plus Schneider Electric Reference Designs Equal Fast and Easy AI SuperPOD Deployments.ˮ Schneider Electric. 2024. https://blog.se.com/datacenter/2024/07/22/nvidia-plus-schneider-electric-reference-designs-equal-fast-and-easy-ai-superpod-deployments/.

Clark, K. “PJM Capacity Auction Hits Price Cap Again as Region Falls Short of Reliability Target.ˮ Power Engineering. 2025. https://www.power-eng.com/business/pjm-capacity-auction-hits-price-cap-again-as-region-falls-short-of-reliability-target/.

Davenport, C, B. Singer, N. Mehta, B. Lee, and J. Mackay. “Generational Growth: AI, Data Centers and the Coming US Power Demand Surge.” Goldman Sachs Research, April 28, 2024. https://www.goldmansachs.com/pdfs/insights/pages/generational-growth-ai-data-centers-and-the-coming-us-power-surge/report.pdf.

DeCourcey, M, and M. Saraswat. Retail Rate Trends in the US. Prepared for Edison Electric Institute. Boston, MA: Charles River Associates, February 2, 2026. https://media.crai.com/wp-content/uploads/2026/02/02092628/Retail-rate-trends-in-the-US.pdf.

Delaware Department of State. “Delaware PSC Opens Docket for Large Load Tariff, Pauses Interconnections.ˮ 2025. https://news.delaware.gov/2025/10/14/delaware-psc-opens-docket-for-large-load-tariff-pauses-interconnections/.

E3. “Tailored for Scale: Designing Electric Rates and Tariffs for Large Loads.ˮ 2025. https://www.ethree.com/wp-content/uploads/2025/12/RatepayerStudy.pdf.

Eberle, L., and C. Kadoch. “Building Resilient Foundations for Large Loads.” Regulatory Assistance Project, February 2026. https://www.raponline.org/wp-content/uploads/2026/02/rap-eberle-kadoch-building-resilient-foundations-large-loads.pdf.

Electric Power Research Institute. “Win-Win Watts: When Can Data Centers, Efficient Electrification, and New Loads Lower Electricity Prices.” Palo Alto, CA: EPRI, 2026. https://winwin.epri.com/en/empirical-insights.htm.

EIA. “Electricity Data Browser.ˮ 2025. https://www.eia.gov/electricity/data/browser/#/topic/7?agg=0,1&geo=g&endsec=vg&linechart=ELEC.PRICE.US-ALL.A~ELEC.PRICE.US-RES.A~ELEC.PRICE.US-COM.A~ELEC.PRICE.US-IND.A&columnchart=ELEC.PRICE.US-ALL.A~ELEC.PRICE.US-RES.A~ELEC.PRICE.US-COM.A~ELEC.PRICE.US-I.

EIA. “STEO Current/Previous Forecast Comparisons: U.S. Energy Production and Consumption Summary.ˮ 2026. https://www.eia.gov/outlooks/steo/pdf/compare.pdf.

EIA. “Use of Natural Gas—U.S. Energy Information Administration.ˮ 2024. https://www.eia.gov/energyexplained/natural-gas/use-of-natural-gas.php.

EPRI. “DCFLEX: Data Center Flexible Load Initiative.ˮ 2026. https://dcflex.epri.com/.

Federal Energy Regulatory Commission. “Electric Power Markets.ˮ n.d. https://www.ferc.gov/electric-power-markets.

Federal Energy Regulatory Commission. “Fact Sheet | FERC Directs Nation’s Largest Grid Operator to Create New Rules to Embrace Innovation and Protect Consumers.ˮ 2025. https://www.ferc.gov/news-events/news/fact-sheet-ferc-directs-nations-largest-grid-operator-create-new-rules-embrace.

Federal Energy Regulatory Commission. “RTOs and ISOs.ˮ n.d. https://www.ferc.gov/power-sales-and-markets/rtos-and-isos.

Federal Energy Regulatory Commission. “Understanding Wholesale Capacity Markets.” FERC, April 1, 2025. https://www.ferc.gov/understanding-wholesale-capacity-markets.

Finley, B., and M. Levy. “Trump and Governors Target AI Power Shortages and Price Spikes.ˮ AP News. 2026. https://apnews.com/article/trump-electricity-ai-data-centers-62e8118b069f36aa9d0844f904047933.

FRED. “Consumer Price Index for All Urban Consumers: All Items in U.S. City Average.ˮ 2026. https://fred.stlouisfed.org/series/CPIAUCSL.

FRED. “Gross Domestic Product (GDP) | FRED | St. Louis Fed.ˮ 2026. https://fred.stlouisfed.org/series/GDP.

Green, M. “Utilities: Tariffs for Data Centers?ˮ Lane Report. 2025. https://www.lanereport.com/183633/2025/09/utilities-tariffs-for-data-centers/.

Grid Strategies. “Load Growth Forecast Report 2025.ˮ 2025. https://gridstrategiesllc.com/wp-content/uploads/Grid-Strategies-National-Load-Growth-Report-2025.pdf.

Hardy, K. “With Electricity Bills Rising, Some States Consider New Data Center Laws.” Stateline, February 5, 2026. https://stateline.org/2026/02/05/with-electricity-bills-rising-some-states-consider-new-data-center-laws/.

Hernández, D. “Energy Insecurity in the United States: Trends, Disparities, and a Widening Crisis (2024 RECS Update).” Center on Global Energy Policy, Columbia University SIPA, April 29, 2026. https://www.energypolicy.columbia.edu/publications/energy-insecurity-in-the-united-states-trends-disparities-and-a-widening-crisis-2024-recs-update.

Hodge, T. “We Expect Rapid Electricity Demand Growth in Texas and the Mid-Atlantic.” Today in Energy, U.S. Energy Information Administration, 2025. https://www.eia.gov/todayinenergy/detail.php?id=65844.

Howland, E. “New Jersey Residential Customers Face 20% Bill Hikes, Driven by PJM Capacity Prices: BPU.” Utility Dive, February 13, 2025. https://www.utilitydive.com/news/new-jersey-electric-bills-pjm-bpu-pseg-auction/740053/.

Howland, E. “PJM Capacity Prices Hit Record High as Grid Operator Falls Short of Reliability Target.ˮ Utility Dive. 2025. https://www.utilitydive.com/news/pjm-interconnection-capacity-auction-data-center/808264/.

Hunton, Andrews Kurth. “FERC’S Order No. 2023 Aims at Improving and Expediting the Generator Interconnection Process.ˮ 2023. https://www.hunton.com/insights/legal/ferc-order-2023-aims-at-improving-expediting-the-generator-interconnection-process.

International Energy Agency. “Energy and AI.” Paris: International Energy Agency, 2025. https://iea.blob.core.windows.net/assets/dd7c2387-2f60-4b60-8c5f-6563b6aa1e4c/EnergyandAI.pdf.

Jacobs, M. “Connection Costs: Loophole Costs Customers Over $4 Billion to Connect Data Centers to the Power Grid.” Union of Concerned Scientists, 2025. https://www.ucs.org/sites/default/files/2025-09/PJM%20Data%20Center%20Issue%20Brief%20-%20Sep%202025.pdf.

Jacobs, M. “Data Centers Are Already Increasing Your Energy Bills. We Have the Receipts.ˮ UCS. 2025. https://blog.ucs.org/mike-jacobs/data-centers-are-already-increasing-your-energy-bills/.

Kaufman, T. “Consumers End Up Paying for the Energy Demands of Data Centers, How Can Regulators Fight Back?ˮ Georgetown Environmental Law Review. 2025. https://www.law.georgetown.edu/environmental-law-review/blog/consumers-end-up-paying-for-the-energy-demands-of-data-centers-how-can-regulators-fight-back/.

Krasniqi, Q, H. Yibrah, R. Scheu, V. Shastry, and D.Hernández. “Community Insights on Weather-Induced Energy Insecurity: A Case Study of Extreme Heat and Power Outages in North Lawndale, Chicago.” Center on Global Energy Policy, Columbia University SIPA, July 10, 2025. https://doi.org/10.7916/cexx-sv28.

Lee, V, P. Seshadri, C.O’Niell, A. Choudhary, B. Holstege, and S. A. Deutscher. “Breaking Barriers to Data Center Growth.” Boston Consulting Group, January 20, 2025. https://web-assets.bcg.com/pdf-src/prod-live/breaking-barriers-data-center-growth.pdf.

Lowrey, D. “Rate Requests by US Energy Utilities Set Record in 2023 for 3rd Straight Year.” S&P Global Market Intelligence, February 7, 2024. https://www.spglobal.com/market-intelligence/en/news-insights/research/rate-requests-by-us-energy-utilities-set-record-in-2023-for-3rd-straight-year.

Martin, E., and A. Peskoe. “Extracting Profits from the Public: How Utility Ratepayers Are Paying for Big Tech’s Power.ˮ Harvard Law School. 2025. https://eelp.law.harvard.edu/extracting-profits-from-the-public-how-utility-ratepayers-are-paying-for-big-techs-power/.

Massachusetts Institute of Technology Energy Initiative. “Data Center Power Demand.ˮ 2025. https://energy.mit.edu/strategic-priorities/data-center-power-demand/.

McDevitt, R. “As More Data Centers Connect to Pennsylvania’s Electric Grid, Some Worry Prices Will Spike.ˮ Allegheny Front. 2025. https://www.alleghenyfront.org/data-centers-pennsylvanias-electric-grid-rates/.

McKinsey & Company. “Powering a New Era of US Energy Demand.” 2025. https://www.mckinsey.com/industries/public-sector/our-insights/powering-a-new-era-of-us-energy-demand.

Meta Engineering. “Meta’s Infrastructure Evolution and the Advent of AI.” Engineering at Meta, September 29, 2025. https://engineering.fb.com/2025/09/29/data-infrastructure/metas-infrastructure-evolution-and-the-advent-of-ai/.

Mullin, R. “Tri-State Seeks FERC Approval for Data Center Load Tariff.ˮ RTO. 2025. https://www.rtoinsider.com/114132-tri-state-seeking-ferc-approval-data-center-load-tariff/.

Murphy, D, P. Vincent, and N. Rauschkolb. Factors Driving Electricity Prices in Maine. Prepared for the Maine Department of Energy Resources. The Brattle Group, February 2026. https://www.maine.gov/energy/sites/maine.gov.energy/files/2026-02/Factors%20Driving%20Electricity%20Prices%20in%20Maine%20Feb%202026%20Brattle%20for%20DOER.pdf.

NERC. “Large Loads Task Force White Paper.ˮ 2025. https://www.nerc.com/globalassets/who-we-are/standing-committees/rstc/whitepaper-characteristics-and-risks-of-emerging-large-loads.pdf.

North American Electric Reliability Corporation. Characteristics and Risks of Emerging Large Loads. Reliability and Security Technical Committee, July 2025. https://www.nerc.com/globalassets/who-we-are/standing-committees/rstc/whitepaper-characteristics-and-risks-of-emerging-large-loads.pdf.

NVIDIA. “NVIDIA Enterprise Reference Architecture Overview.ˮ 2025. https://resources.nvidia.com/c/collection-9563de54?x=sTI8RF.

Ohler, A., H. Mohammadi, and D. G. Loomis. “Electricity Restructuring and the Relationship Between Fuel Costs and Electricity Prices for Industrial and Residential Customers.ˮ Energy Policy. 2020. https://doi.org/10.1016/j.enpol.2020.111559.

Olabi, A. G. “Renewable Energy and Energy Storage Systems.” Energy 136 (2017): 1–6. https://doi.org/10.1016/j.energy.2017.07.054.

PG&E. “PG&E Data Center Demand Pipeline Swells to 10 Gigawatts with Potential to Unlock Billions in Benefits for California.ˮ 2025. https://www.pge.com/en/newsroom/press-release-details.a9a4dda5-372f-4c33-860f-df2837e9b57b.html.

PJM. “2027/2028 Base Residual Auction Report.ˮ 2025. https://www.pjm.com/-/media/DotCom/markets-ops/rpm/rpm-auction-info/2027-2028/2027-2028-bra-report.pdf.

PJM. “Board Decisional Letter on Critical Issue Fast Path—Large Load Additions.ˮ 2026. https://www.pjm.com/-/media/DotCom/about-pjm/who-we-are/public-disclosures/2026/20260116-pjm-board-letter-re-results-of-the-cifp-process-large-load-additions.pdf.

PJM. “PJM Annual Report 2024.ˮ 2025. https://services.pjm.com/annualreport2024/.

Rand, J., M. Bolinger, R. Wiser, J. Seel, et al. “Queued Up: 2024 Edition.ˮ Lawrence Berkeley National Laboratory. 2024. https://emp.lbl.gov/sites/default/files/2024-04/Queued%20Up%202024%20Edition_R2.pdf.

Rocky Mountain Institute. “Fast, Efficient Solutions to Meet Electricity Demand Growth.” RMI, February 18, 2026. https://rmi.org/fast-efficient-solutions-to-meet-electricity-demand-growth/.

Saul, J, L. Nicoletti, D. Pogkas, D. Bass, and N. Malik. “AI Data Centers Are Sending Power Bills Soaring.” Bloomberg, September 29, 2025. https://www.bloomberg.com/graphics/2025-ai-data-centers-electricity-prices/.

S&P Global. “Rate Requests by US Energy Utilities Set Record in 2023 for 3rd Straight Year.ˮ 2024. https://www.spglobal.com/market-intelligence/en/news-insights/research/rate-requests-by-us-energy-utilities-set-record-in-2023-for-3rd-straight-year.

S&P Global Commodity Insights. U.S. National Power Demand Study: Executive Summary. Study conducted for the American Clean Power Association. Washington, DC, 2025. https://cleanpower.org/wp-content/uploads/gateway/2025/03/US_National_Power_Demand_Study_2025_ExecSummary_FINAL-v2.pdf.

S&P Global Market Intelligence and 451 Research. 2026 US Data Centers and Energy Outlook Report. New York: S&P Global, 2026. https://pages.marketintelligence.spglobal.com/rs/565-BDO-100/images/US-datacenters-energy-2026-outlook-report.pdf.

Shastry, V, and D. Hernández. “How AI Growth Can Hyper-Scale Energy Equity and Affordability.” Center on Global Energy Policy, Columbia University SIPA, November 6, 2025. https://www.energypolicy.columbia.edu/how-ai-growth-can-hyper-scale-energy-equity-and-affordability/.

Shehabi, A., S. J. Smith, A. Hubbard, A. Newkirk, et al. “2024 United States Data Center Energy Usage Report.ˮ Lawrence Berkeley National Laboratory. 2024. https://escholarship.org/uc/item/32d6m0d1.

Shumway, E, D. Hernández, Q. Krasniqi, V.Shastry, A. Austin, and M. B. Gerrard. “Addressing Energy Insecurity Upstream: Electric Utility Ratemaking and Rate Design as Levers for Change.” Energy Bar Association Journal 45, no. 2 (2024): 361–397. https://www.eba-net.org/wp-content/uploads/2024/11/452_10-Shumway361-397.pdf.

Smart Electric Power Alliance. “Database of Emerging Large-Load Tariffs (DELTa).ˮ 2025. https://sepapower.org/large-load-tariffs-database/.

Smith, B. “Building Community-First AI Infrastructure.” Microsoft On the Issues, January 13, 2026. https://blogs.microsoft.com/on-the-issues/2026/01/13/community-first-ai-infrastructure/.

Srinivasan, H. “Inflation Rate by Year.” Investopedia, December 22, 2025. https://www.investopedia.com/inflation-rate-by-year-7253832.

The White House. “Ratepayer Protection Pledge.” The White House, March 4, 2026. https://www.whitehouse.gov/releases/2026/03/ratepayer-protection-pledge.

Tonko, P. D. “Tonko Introduces ‘Power for the People Act’ to Shield Consumers from Rising Energy Costs.” Office of U.S. Representative Paul D. Tonko, April 9, 2026. https://tonko.house.gov/news/documentsingle.aspx?DocumentID=4569

US Congress, Senate, “Guaranteeing Rate Insulation from ‘Data Centers Act’ (S. 3852: 119th Cong.),” 2026, https://www.congress.gov/bill/119th-congress/senate-bill/3852/text.

US Congress, Senate. “Power for the People Act of 2026 (S. 3682, 119th Cong.).” U.S. Government Publishing Office, 2026. https://www.govinfo.gov/content/pkg/BILLS-119s3682is/pdf/BILLS-119s3682is.pdf

US Energy Information Administration. “Electricity: State Energy Profiles.” EIA, 2026. https://www.eia.gov/electricity/state/.

US Energy Information Administration. “Electricity Data Browser: Average Retail Price of Electricity.” EIA, 2026. https://www.eia.gov/electricity/data/browser/#/topic/7

US Energy Information Administration. “Electric Power Monthly—EIA.ˮ 2026. https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=table_5_01.

US Energy Information Administration. “Electricity Use for Commercial Computing Could Surpass Space Cooling, Ventilation.ˮ 2025. https://www.eia.gov/todayinenergy/detail.php?id=65564.

US Energy Information Administration. “Grid Infrastructure Investments Drive Increase in Utility Spending over Last Two Decades.ˮ 2024. https://www.eia.gov/todayinenergy/detail.php?id=63724.

US Energy Information Administration. “Short-Term Energy Outlook.” Washington, DC: U.S. Department of Energy, 2026. https://www.eia.gov/outlooks/steo/pdf/compare.pdf.

Vorys. “Public Utilities Commission of Ohio Authorizes Tariff for AEP Ohio’s Data Center Customers, Requires End of Moratorium on New Services for Data Centers.ˮ 2025. https://www.vorys.com/publication-public-utilities-commission-of-ohio-authorizes-tariff-for-aep-ohios-data-center-customers-requires-end-of-moratorium-on-new-services-for-data-centers.

Warren, E. “Letter to EIA Regarding Data Center Transparency.” Office of Senator Elizabeth Warren, March 25, 2026. https://www.warren.senate.gov/imo/media/doc/letter_to_eia_re_data_center_transparency.pdf.

Wilson, J. D., and Z. Zimmerman. “The Era of Flat Power Demand Is Over.ˮ Grid Strategies. 2023. https://gridstrategiesllc.com/wp-content/uploads/2023/12/National-Load-Growth-Report-2023.pdf.

Wiser et al. “Factors Influencing Recent Trends in Retail Electricity Prices in the United States.ˮ Lawrence Berkeley National Laboratory. 2025. https://eta-publications.lbl.gov/publications/factors-influencing-recent-trends.

Wiser et al. “Retail Electricity Price Trends and Drivers: Data Update–2026 Edition. Berkeley, CA: Lawrence Berkeley National Laboratory, 2026. Retail Electricity Price Trends and Drivers: Data Update–2026 Edition (PDF).

You, J., D. Owen, D. Porter, and T. Wilson. Scaling Intelligence: The Exponential Growth of AI’s Power Needs. Electric Power Research Institute and Epoch AI, 2025. https://www.epri.com/research/products/000000003002033669.

Diego Rivera Rivota is a Senior Research Associate at the Center on Global Energy Policy (CGEP) at Columbia University’s School of International and Public Affairs (SIPA). He has over 10 years of experience working on the intersection of energy, policy and international cooperation across Asia, Europe and the Americas. Diego’s research and practical experience focuses on energy policy and geopolitics in Latin America, particularly on natural gas and LNG markets, critical minerals supply chains, and their role in the low-carbon energy transition.