In the waters off Malaysia, Iranian oil sales continue despite blockade

A large anchorage area off the coast of Malaysia is a major marketplace for sanctioned oil.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the demand for power surges across the US, the debate over how to build energy infrastructure has reached a fever pitch. And while both sides of the...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available here. Rare cases of sponsored projects are clearly indicated.

Europe is entering the 2026 gas injection season (seven months of stocking up supplies for winter) with its lowest level of gas in storage since 2018, at 31 billion cubic meters (bcm). Back then, the number dropped to 19 bcm, which then led to the largest seven months of gas injections on record, at 74 bcm. Though Europe has 110 bcm of storage capacity,[1] the loss of most Russian pipeline gas imports since 2022 and all Qatari liquefied natural gas (LNG) imports indefinitely makes it essentially impossible to import and inject enough gas to eclipse the 2018 mark.

European storage injection season typically moves into high gear starting in May, when seasonal gas demand shrinks because the weather is more moderate than in winter or summer. The gas injected starts to tail off in September and October.

The European Union requires EU storage operators to reach 90% utilization capacity by Nov. 1. This threshold was not achieved in 2025. A meeting of the EU Gas Coordination Group held last month considered reducing filling targets to 80% as early as possible in the filling season to provide certainty and reassurance to market participants.

The use of policy to manage either the rate of injection or the total amount of gas to be in storage by the end of October will affect the current price for future deliveries (reflected in a “forward curve”), and therefore the ability of the EU to achieve its storage goal. If sellers know buyers have to buy gas for a certain period of time—whether monthly, quarterly, or annually—sellers, supported by the trading community, will take a position on the forward curve to maximize their gain.

Achieving 80% utilization this year, or 88 bcm of gas in working gas storage (storage that can be used commercially, as opposed to cushion gas storage, which exists to create needed pressure), will require 57 bcm of gas injections. Filling storage to this level would cover the largest winter draw recorded: 76 bcm in 2017–18. But given current losses from Russia and Qatar, filling storage closer to 75% would be a more realistic assumption.

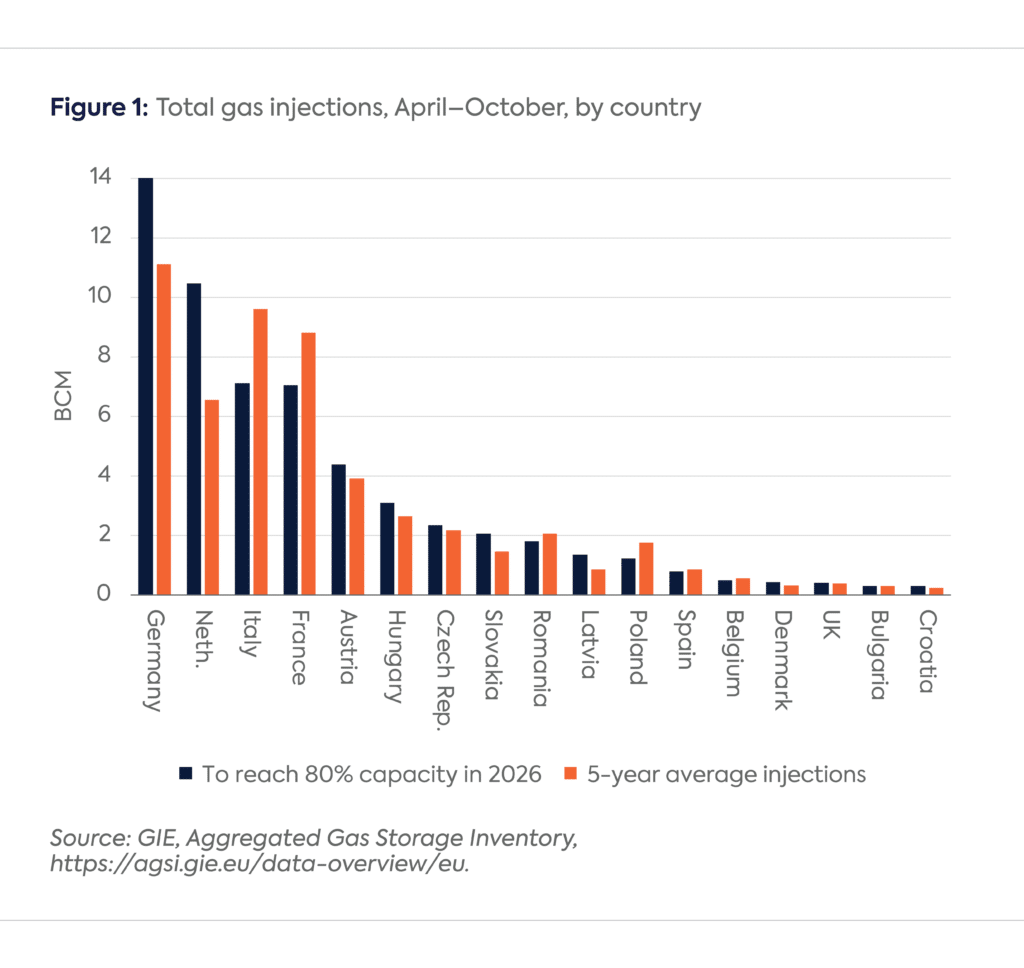

Not all countries are facing a severe storage crisis. Germany and the Netherlands stand out in Figure 1 as the major risk areas for future shortages. While the German market will require the most volume of storage injections, 14 bcm, to reach 80% of their capacity, the Dutch market will require the largest increase versus normal, at 3.91 bcm of additional injections. The Dutch ended March with only 0.69 bcm of gas in storage, which tested the limit of their working gas capacity. Note that German demand, at 82 bcm in 2025 is roughly 2.5 times the size of the Dutch market, and its demand is more seasonal, which means a greater weighting toward peak winter use.

Italy and France have more successfully managed working gas storage levels due to stricter policy measures that go beyond EU mandates. Each country will need to inject far less than its 5-year average to reach the 80% threshold. The key to their relative success was achieving higher storage targets heading into the prior winter. In addition, both countries imported more LNG during the winter versus withdrawing additional gas from storage.

Italian storage operator Snam launched a premium-based system in which the state effectively guarantees the profit margins for storage. If the price of gas during the winter withdrawal period was lower than the price paid during the summer injection period, the state compensates the difference to market operators. Italy’s energy regulator ARERA published specific “premiums” ahead of each auction to ensure that even if market conditions were unfavorable, traders had a financial reason to inject gas. Italy also maintains a separate “strategic reserve” (roughly 4.6 bcm) that is legally isolated from commercial use, acting as a hard buffer that cannot be traded away regardless of price spikes.

France maintains a stricter system than the EU through the use of its “public service obligation.” This law requires suppliers to hold enough gas in storage to cover at least 50% of their historical winter consumption for residential and small-business customers. France’s gas transport and storage operator Teréga, which primarily operates in the southwestern part of the country, introduced specialized withdrawal products such as FAST and OPSTOCK, that allow for rapid depletion during extreme 10-day cold snaps. This ensures that storage is not just full but also provides enough flexibility to meet sudden demand spikes, such as the ones that emerged in January 2026.

Most LNG importing countries only have enough storage capacity to manage imports on an operating basis rather than for seasonal swings in demand. When countries need to buy less LNG, they typically divert the volumes to the European market in the second and third quarter, or to summer peaking gas markets such as Egypt, India, or Taiwan. The more LNG diverted into European storage in the April–October injection period, the less Europe will need to pull from the LNG market in the winter, allowing LNG to flow to other markets with little storage capacity that need to import more supply on a prompt basis.

With countries outside the EU relying on European storage more than ever, potential shortages heading into next winter will be amplified around the world. Colder than normal weather next winter could lead to a bidding war for incremental spot cargoes in a market that is likely to be without Qatari and Russian volumes. Even a rapid return of Qatari volumes makes it unlikely the country will be producing LNG at 100% capacity by the time peak winter demand begins in early 2027. Europe will be cautious in drawing down its stocks, which makes the fourth quarter particularly vulnerable to price spikes. The current forward curve does not necessarily reflect this scenario.

[1] Ukraine’s 30 bcm of storage capacity is not included in this calculation, given the unknown state of its usability. For the purposes of this blog, storage capacity in the EU plus the UK is included.

The Iran crisis, whenever it ends, will materially change how the LNG market operates.

Almost 90 percent of the LNG that transited the Strait of Hormuz in 2025 was destined for Asian countries.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Iran appears to be a natural gas giant, due to its large proved gas reserves and significant gas production and consumption.

CHRONIQUE. Les Etats-Unis vont bientôt contrôler environ un tiers des capacités mondiales de GNL, bien plus que le Qatar. Sous l’administration Trump, le GNL est devenu un outil de politique étrangère, écrit Anne-Sophie Corbeau, chercheuse au Center on Global Energy Policy de l’Université Columbia

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia