Trump says ongoing talks are Iran’s ‘last chance’

Karen Young, senior research scholar at the Centre on Global Energy Policy at Columbia University, joins BNN Bloomberg to discuss the energy sector.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Over the past five months, the Strait of Hormuz has been closed for extended stretches of time, disrupting roughly 10 to 15 million barrels of oil supply each...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision.

Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available here. Rare cases of sponsored projects are clearly indicated.

Critical minerals security is at the top of the policy agenda for governments around the world, as market concentration and price volatility have exposed the limits of purely market-led approaches. This industry is a domain where governments appear to be rapidly and unambiguously discarding free-market economics in favor of directly intervening to shape outcomes.

At the Critical Minerals Ministerial summit in Washington earlier this month, US Vice President JD Vance said the Trump administration sees an active government role as essential to addressing supply chain vulnerabilities and reindustrializing the American economy. Vance announced a preferential minerals trading zone with price controls, which marks a shift from an exclusively domestic minerals security strategy toward the internationalization of US industrial policies.

This blog post discusses recent US efforts to extend its America First critical minerals security strategy abroad through the creation of a managed trade zone. It argues that the effectiveness of this effort will hinge on Washington’s ability to align its minerals security priorities with those of the invited partners and on restoring credibility to US-led transnational initiatives.

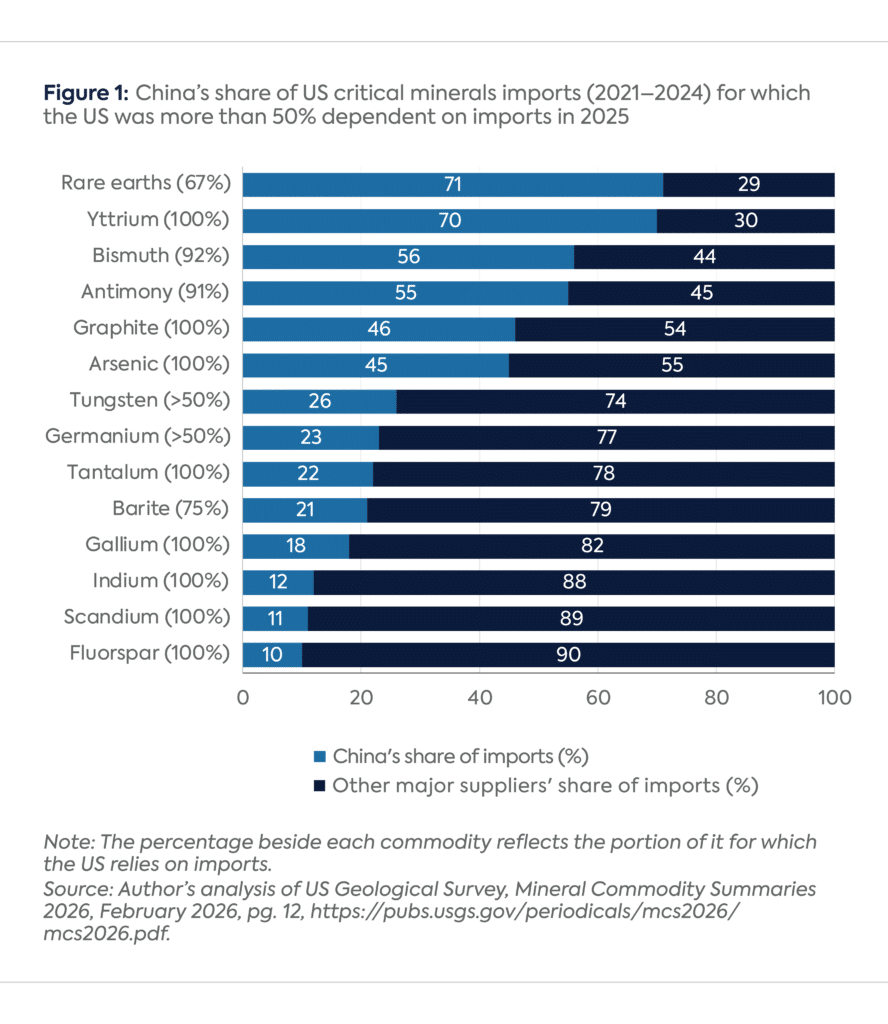

Since President Donald Trump’s return to the White House, the US government has pursued a variety of industrial policies to secure reliable supplies of critical minerals and reduce dependence on adversarial sources. The US is 50–100% reliant on imports for 32 critical minerals, and China is a supplier of 14 of these (see Figure 1). Consequently, the US government has used regulatory, financial, and trade tools to expand domestic mineral production, including permitting reform, equity stakes in select mining firms, and tariffs on copper and aluminum imports.

These industrial policy measures have proven insufficient to jump-start domestic production and refining of critical minerals, necessitating a pivot of the inward-looking America First strategy toward transnational coordination. Vance conceded that some critical minerals projects have struggled to attract investors. Sustained price weakness has stalled mining projects and constrained investment in both high-income countries and low- and middle-income countries (LMIC). According to the IEA, investment in critical minerals grew in real terms by only 2% in 2024, down from 14% in 2023, with both exploration and venture capital spending flatlining.

The main constraint to expanding investments in critical minerals projects is that global commodities markets favor Chinese producers. Western operations face higher costs, longer project timelines, and limited resilience during market downturns. In the US, it also takes an average of 29 years to bring a mine from exploration to production, according to David Copley, special assistant to the president and senior director for global supply chains. Chinese investments benefit from state financial backstops, guaranteed off-take, and the ability to weather low prices.

To reshape global commodities markets, the US government invited 54 countries attending the aforementioned summit to join a preferential trade zone for critical minerals, signaling efforts to internationalize America’s industrial policy. The trade zone aims to create a protected market through enforceable price floors, using tariffs and other measures to exclude Chinese and non-member participation. To join this bloc, a country has to enter into a critical minerals agreement with the US. According to the State Department, the US signed 10 such agreements in the preceding five months, 11 at the summit, and had completed negotiation on an additional 17.

The trade zone will include a coordination platform called the Forum on Resource Geostrategic Engagement (FORGE). FORGE is the successor to the Minerals Security Partnership, which was established to identify eligible projects, coordinate member states’ development finance institutions to mobilize private capital, and uphold high standards and governance norms. In contrast, FORGE and the associated preferential trade zone propose direct government involvement in shaping the critical minerals market through tariffs, subsidies, and guaranteed domestic demand facilitated by the recently established Project Vault stockpile. A central challenge will be coordinating tariff adjustments to sustain price floors while excluding lower-cost Chinese supply—an objective that tariffs alone are unlikely to achieve without complementary subsidies to reduce a variety of production costs, even within such a proposed managed trade zone.

The success of efforts to internationalize US industrial policy for secure, China-free critical mineral supply chains depends on gaining the willing support of participating countries through alignment and credibility.

The US will need to ensure that components of its critical minerals security objectives align with priorities of member states in the planned trade zone. The policy announcement is framed in America First language that emphasizes meeting domestic demand for critical minerals, protecting US companies, establishing a domestic stockpile, and building local refining and processing capabilities. However, many resource-rich LMICs similarly aspire to strengthen their own refining and processing industries. Countries from Indonesia to Zambia, Chile to Ghana have national strategies to this effect and are unwilling to be relegated to the peripheral role of exporting unprocessed commodities for advanced industries abroad.

The mechanisms by which LMICs might participate in the midstream segment of the mining value chain within the planned US trading zone remain unclear. While threats of tariffs and visa restrictions could coerce countries’ participation in the short term, such approaches are unlikely to offer sustainable outcomes. The notion of shipping a country’s unprocessed commodities to feed US-managed stockpiles and industries could mobilize political opposition in participating governments. Host communities are also likely to oppose such extractive mining operations, thereby undoing decades of companies’ efforts to secure the social license to operate, or a social compact with local communities.

The success of the preferential trade zone will hinge on its ability to restore the credibility of US-led transnational initiatives to deliver infrastructure projects. Partner countries will need to be assured that the trade zone will not be abruptly jettisoned once political conditions in the US change, such as with a new administration in 2028.

Although the US government possesses vast fiscal resources and a convening power through its network of alliances, repeated patterns of launching and then discontinuing major infrastructure programs have led many countries to question its reliability. For instance, the much-publicized Partnership for Global Infrastructure and Investment—introduced at the G7 summit in 2022 as a counterweight to China’s Belt and Road Initiative (BRI)—no longer maintains even a website. Similar outcomes befell the Blue Dot Network, initiated during Trump’s first term as another proposed alternative to Chinese-funded projects. Other State Department projects to unite allies around high-standard goals in climate finance and infrastructure have stalled or been discontinued after spending millions of dollars in convening international conferences and conducting feasibility studies.

These experiences have turned quiet doubts about US reliability into a genuine credibility gap, especially as alternatives like China’s BRI or the Saudi-led Africa-Asia minerals corridor take shape. When FORGE becomes operational, success will be determined by whether it can restore confidence in America’s commitment to its own international initiatives.

Raw material vulnerability was once again at the center of the G7 agenda at the summit in Evian, France.

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

One of the central objectives of the second Trump administration has been to pursue a maximalist trade policy toward China.

The US Export-Import Bank is preparing to close the first funding tranche of Project Vault, a public-private partnership establishing the US Strategic Critical Minerals Reserve.

In early 2026, CGEP held a roundtable and several hybrid closed-door meetings in Mexico City on Mexico's mining sector.

This paper proposes a de-risking framework of policy interventions to provide the risk allocation, revenue certainty and delivery confidence required by mainstream private finance.