Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Qatar is one of the world’s three largest liquefied natural gas (LNG) exporters, along with the United States and Australia.[1] Qatari and US exports are the yin and yang of the global LNG market, although some observers might argue that Qatar straddles both sides of the cosmological divide. While Qatar will compete with US LNG, its 70 percent ownership of the US-based Golden Pass LNG export project enables the powerhouse producer to market supply from dual locations and enhance its returns. One of the key questions facing the market is what Qatar will do with all the unsold LNG production capacity it is building—whether Qatar will lead or lag the balance of the field on pricing and what region, if any, it will target. Prior to the Russian invasion of Ukraine, the answer to the target market was easy: Asia. Now the lines have blurred, given Europe’s potentially greater need for LNG than previously anticipated.

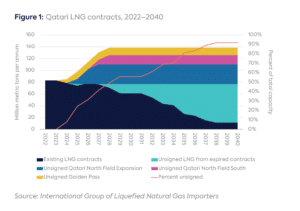

LNG export capacity controlled by Qatar will increase from 77 million metric tons per annum (MTPA) in 2023 to 138.6 MTPA by 2028 through a series of new trains to be built in Qatar and in the US at Golden Pass.[2] Meanwhile, uncontracted volumes from Qatar are expected to increase from none in 2023 to 68 MTPA by 2028 due to a combination of expiring LNG contracts from existing capacity and unsigned LNG capacity emanating from new capacity (Figure 1). This unsigned volume accounts for 49 percent of Qatari LNG production capacity in Qatar and the US.

This volume of unsigned capacity will make Qatar the single most influential force on price in the years ahead. Since Qatar does not require financeable long-term contracts to move ahead with building new liquefaction capacity, it will be sitting on the largest amount of unsold LNG in the market over the next decade.[3]

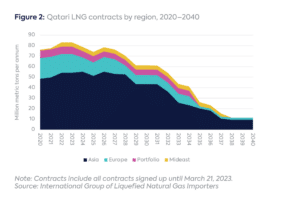

In the late 1990s, Qatar targeted Asian markets almost exclusively through LNG producers Qatargas and RasGas. Now it has consolidated all its contracts under one marketing roof: QatarEnergy. These volumes include the LNG produced at Ras Laffan in Qatar and 70 percent of the Golden Pass volumes.[4] QatarEnergy is the only company marketing all unsigned LNG volumes. Its portfolio reflects the current state of play in global LNG markets: a large part of LNG is contracted by Asian companies, which represent the bulk of global LNG trade, with the rest sold to European buyers and portfolio players (Figure 2).[5]

All LNG exporters, including Australia and the US, face a decline in contracts coverage, but the timing and pace of the decline will differ. There is no risk that Qatar, which has a single seller, will run out of gas supply, unlike some other projects. Qatari contracts tend to be twice as large as other sellers’ contracts and are often pegged to oil prices. Over the past decade, Qatar has moved from being the largest spot LNG seller, representing one-quarter of spot LNG trade in 2012 to around 6 percent in 2021, as it has opted for large contracts and oil indexation. The intention to move away from the commercial uncertainty of exposure to spot LNG markets was made clear in 2021 by the CEO of Qatar Petroleum: spot volumes would represent about 5–10 percent of volumes sold.[6] This marketing philosophy contrasts with the current US norm, where smaller contracts and spot-indexed LNG prices are prevalent.

To fill the gap left between its LNG export capacity and contracted volumes, QatarEnergy may first seek to extend volumes of expiring contracts with the same buyers. Around 10 MTPA of contracts expiring by 2030 are in the hands of buyers from developing Asia that may be keen to extend. Buyers from Japan and Korea also may want to accommodate declining demand, extending these contracts at partial volumes. About 12 MTPA are with European utilities, which may be interested in a 10-year extension to face the current deficit, due to their decarbonization strategy and uncertain LNG demand.

Re-signing with existing buyers would prevent the decline into the 2030s, but still leave around 50 MTPA to be contracted by other buyers. These buyers could include the aggregators partnering with QatarEnergy in the development of its Qatari expansion, while many also have existing (and expiring) contracts. Developing Asia is another obvious target, especially China, which has signed a record number of contracts recently and is expected to sign more—including with direct stakes in the Qatari projects[7]— although is also keen to keep a diversified portfolio.[8] The gas price spike has created new concerns about South Asia’s future appetite for LNG, after Pakistan opted for coal instead. Meanwhile, Europe’s appetite for long-term LNG contracts remains elusive,[9] and the recent Qatargate scandal might make companies wary of geopolitical risks.[10]

For contracts starting after 2025, QatarEnergy will face competition from (US) LNG projects also trying to take final investment decision (FID) and targeting a starting date in the late 2020s. Buyers are using new US contracts to extract better terms from the Qataris, while the Qataris are waiting out the signing of more US contracts to gauge how they will price their LNG and where will it go.

Every move Qatar makes over the next year should be watched closely. It will likely be signing up large volumes of LNG under long-term contract in record time, playing a central role in establishing the parameters on price for decades. The task will not be easy. Qatar’s wide range of prices historically suggests that new deals will depend on the bearable price for the buyer, with a coastal buyer in China feeding the residential/commercial market at the high end and a power generator in Bangladesh or the Philippines at the lower end of the range. Either way, bilateral deals remain at the core of Qatar’s LNG marketing strategy. But the complexity of marketing such significant volumes, after its massive capacity expansion, could result in Qatar becoming a key spot seller once again—as it was in the early 2010s— despite its current preference for long-term, oil-indexed contracts.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] Stephen Stapczynski, “US Surges to Top of LNG Exporter Ranks on Breakneck Growth,” Bloomberg, January 3, 2023, https://www.bloomberg.com/news/articles/2023-01-03/us-surges-to-top-of-lng-exporter-ranks-on-breakneck-growth.

[2] This includes the North Field Expansion, which will increase Qatar’s LNG export capacity first from 77 MTPA to 110 MTPA, followed by a further expansion with the North Field South project to 126 MTPA, as well as 70 percent of the 18 MTPA US Golden Pass project.

[3] QatarEnergy, “QatarEnergy to Take Over All Marketing and Related Activities Managed by Qatargas,” February 20, 2023, https://www.qatarenergy.qa/en/MediaCenter/Pages/newsdetails.aspx?ItemId=3746.

[4] LNG Prime, “QatarEnergy’s Trading Unit to Offtake 70 Percent of Golden Pass LNG Volumes,” October 26, 2022, https://lngprime.com/americas/qatarenergys-trading-unit-to-offtake-70-percent-of-golden-pass-lng-volumes/64887/.

[5] Ira Joseph, “Asia’s Fragmented Future on LNG Pricing,” Energy Explained, Center on Global Energy Policy, March 21, 2023, https://www.energypolicy.columbia.edu/asias-fragmented-future-on-lng-pricing/.

[6] Dmitry Zhdannikov and Rania El Gamal, “Qatar Petroleum Expands Trading as Rivals ‘Punch Above Weight,’” Reuters, February 10, 2021, https://www.reuters.com/article/qatar-petroleum-strategy-int-idUSKBN2AA1RN.

[7] Walid Ahmed and Stephen Stapczynski, “China’s Sinopec Invests in Qatari Liquefied Natural Gas Project,” Bloomberg, April 12, 2023, https://www.bnnbloomberg.ca/china-s-sinopec-invests-in-qatari-liquefied-natural-gas-project-1.1906665.

[8] Anne-Sophie Corbeau and Sheng Yan, “Implications of China’s Unprecedented LNG-Contracting Activity,” Center on Global Energy Policy, October 7, 2022, https://www.energypolicy.columbia.edu/publications/implications-of-chinas-unprecedented-lng-contracting-activity/.

[9] Anne-Sophie Corbeau, “Could Europe’s Supply Gap Herald a Golden Age of LNG?,” Energy Explained, Center on Global Energy Policy, February 14, 2023, https://www.energypolicy.columbia.edu/could-europes-supply-gap-herald-a-golden-age-of-lng/.

[10] Eleni Varvitsioti, Andy Bounds, Alice Hancock, and Silvia Sciorilli Borrelli, “Inside the ‘Qatargate’ Graft Scandal Rocking the EU,” Financial Times, January 29, 2023, https://www.ft.com/content/4663bc9e-eaa5-485f-baaf-2a85dc0eac07.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

Almost 90 percent of the LNG that transited the Strait of Hormuz in 2025 was destined for Asian countries.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Iran appears to be a natural gas giant, due to its large proved gas reserves and significant gas production and consumption.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia