This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

This event will take place in-person in Washington DC, at the Rayburn House Office Building, Room 2168 (Gold Room). Advance registration is required. Announcing New Columbia University Publications...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

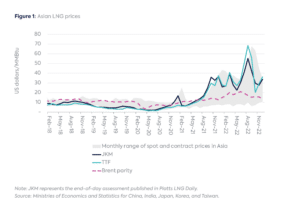

Asian liquefied natural gas (LNG) pricing is one of the hardest aspects of global gas pricing to understand. As the largest LNG growth market in the world, Asia will be central to global gas pricing, influencing global trade flows on a real-time basis. The US and European gas markets offer a wide range of spot prices based on hub locations, but Asia’s LNG market is much more fragmented due to the domination of long-term contracts. While spot price assessments like Platts Japan Korea Marker (JKM) represent the assessed value of the marginal cargo in East Asia, the core of Asia’s LNG business is long-term, oil-indexed pricing tied to contracts lasting up to 30 years.

Of the world’s 245 existing long-term (10 years or more in length) LNG contracts, 92 expire this decade, just as vast amounts of new LNG capacity is also scheduled to be commissioned, requiring long-term contracts of its own.[1] As of March 2023, roughly 146 long-term contracts, covering 195 million metric tons per annum (MTPA) of volume, exist in Asia. These totals will drop to 96 contracts and 146 MTPA by 2030, although some of these contracts will be re-signed and new deals will emerge. The conjunction of these two events creates an unprecedented moment for LNG pricing, particularly in Asia, which will be a primary destination for LNG deliveries from the three leading suppliers, including mostly oil-indexed volumes from Qatar and Australia and spot gas-indexed LNG from the US. Add in the pricing on Asian spot deals, and what emerges is a regional market still coming to grips with the broader role of gas as both a fuel and a feedstock.

Old School Asian LNG Pricing

Bilateral long-term contracts are the basis for the vast majority of LNG pricing in Asia. Buyers can be broken down into two general groups: end users that import the LNG, and portfolio players that pool supplies to optimize trading opportunities upon resale of the cargoes. These contracts come with what is commonly referred to as pricing slopes, which determine how the contract price will move over time. In Asia, these pricing slopes are largely indexed to crude oil prices such as Brent crude or the average price of Japanese crude oil imports, more commonly known as the Japanese Crude Cocktail (JCC).[2] A typical slope will range between 10 and 16 percent of Brent crude.

These contracts, combined with spot deals, can lead to a wider variety of pricing in a given month (Figure 1).

Due to the Russian invasion of Ukraine and the subsequent movement of both crude oil and gas prices relative to each other, the range of prices in Asia during a given month has widened significantly. Between 2018 and 2021, the monthly range between the highest and lowest price in Asia averaged $9/ million British thermal units (MMBtu). Since the Russian invasion of Ukraine, this range has widened to $36/MMBtu, peaking at $61/MMBtu in September 2022.

The wide price range can be tied not only to volatility in the current market, but also to when the LNG contracts covering the relevant volumes were originally signed. The state of the gas market during the time a contract is signed can have as much, if not more, influence on the pricing of the deal than the expected price during the period when the volumes are delivered. Because market conditions can change drastically over time, long-term LNG contracts come with reopener clauses that allow buyers and sellers to renegotiate the deal.[3]

The Dilemma for Future LNG Pricing

More LNG contracts will need to be priced in upcoming years than at any other time in history, and while pricing long-term gas is always difficult, today’s unprecedented market conditions are making the crystal ball even more opaque. The biggest X factor is the future of Russian gas exports: Should the return of Russian gas be priced into the market? If so, how much gas, and where will it be delivered? Adding to the complexity, Russia is the world’s low-cost gas producer, while LNG tends to be the most expensive form of gas supply. Even Qatari LNG—the cheapest on LNG supplier on a short-run marginal cost basis—cannot compete with Russian pipeline gas in Europe.

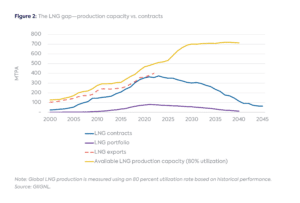

With existing contracts expiring and new capacity opening up, all this volume needs a market. Simultaneously, Europe is continuing to step up its LNG imports to replace Russian pipeline gas. Historically, Europe has committed little LNG buying to long-term contracts, although European-affiliated companies like Shell, TotalEnergies, and BP possess sizable contracted volumes in their respective global portfolios. While Europe bought 33 percent of the world’s LNG in 2022, end users in the region account for only 9 percent of long-term contracts. The gap between available LNG supply and volumes under contract is widening (Figure 2), lending tremendous significance to the next few years when new pricing terms are established for the new contracts that will be signed.

Pricing will be affected not only by how much LNG is signed under contract, but also by the pricing preferences of the sellers and buyers. Among the biggest exporters, Qatari and Australian sellers seem committed to oil indexation as the underlying basis for LNG prices. US LNG exporters are more inclined to use hub price indexation. On the buyer side, the underlying assumption in the market is that European importers will need to sign up more LNG under long-term contract. If this happens, most of this LNG will be priced based on some combination of hub price indices, such as Henry Hub and TTF. Most US LNG export volumes, including those flowing to Asia, are priced off Henry Hub.

Conclusion

No single pricing methodology will dominate LNG trade in the future, especially in Asia, where both oil-indexed and gas-indexed prices will feed into the market. In addition, spot trade, which accounts for 20 to 30 percent of the total LNG market, is typically awarded based on a tender at bid prices without any indexation. Sometimes an index such as TTF or JKM—i.e., TTF minus $0.10 or JKM plus $0.05 per MMBtu—is used to establish a base price.[4]

Two key pillars shed light on where Asian LNG pricing is heading. The first pillar is Qatar’s expansion of its production capacity by 50 MTPA by 2027, of which only 4 MTPA has thus far been signed under long-term contract. Qatar will also be marketing another 16 MTPA from its Golden Pass LNG affiliate in the US. These unsold volumes alone account for 10 percent of global LNG production capacity in 2027. An additional 12 MTPA of Qatar’s existing contracts will be expired by then. The second pillar is US LNG exports. Thirteen different US sellers have already signed a total of 53 long-term contracts covering 90 MTPA. Most of these contracts are indexed to spot gas prices.

While LNG has been the cornerstone in the globalization of gas markets, the pricing of this gas will remain bifurcated at best in Asia, with US LNG exports providing the most transparent window. The rest of the gas pricing in the region, aside from spot cargoes, will remain hidden behind a cloak of bilateral relationships.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

The World Bank is revisiting one of its most entrenched positions, publicly questioning its long-standing emphasis on market-led approaches in economic policy.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia

When the Iran War disrupted shipping through the Strait of Hormuz and tightened global gas balances, a familiar assumption quickly resurfaced: Russia, possessing the largest proven natural gas reserves in the world, would inevitably emerge as one of the principal beneficiaries.