Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Russia’s invasion of Ukraine has had widespread consequences for global liquefied natural gas (LNG) markets. There is an identified need in Europe for more LNG in the coming years in order to replace missing Russian pipeline gas. But is the current high demand for LNG in Europe just a blip in history or is it here to stay and result in a boom in new LNG supply post 2025?

The need to replace dwindling volumes of Russian pipeline gas has left European Union (EU) countries scrambling to get access to the only large alternative source of gas – LNG. These countries have successfully attracted an estimated 53 billion cubic meters (bcm) of incremental LNG supplies in 2022, representing over four times the LNG demand shock experienced by Japan after Fukushima.[1] Europe diverted a lot of LNG from Asia; in particular, the EU has been helped by President Xi Jinping’s zero COVID policy leading to China’s LNG imports dropping by 22 bcm.[2]

The European Commission has for long been advocating for a liquid, flexible, and transparent LNG market as the best tool to ensure energy security.[3] Spot LNG would be available to fill gaps – at a higher price. For sure, spot LNG has been available, but with average spot prices six times higher than historical norms.[4] In France, gas net import costs have increased from €9.4 billion (bn) during January-October 2021 to €36.6 bn over the same period in 2022.[5]

So far the market has worked, but it may not in the future given that capping wholesale gas prices is a bit like playing the sorcerer’s apprentice.[6] Ironically, there has been no need for Brussels to trigger the mechanism so far as this new measure has coincided with the start of a four-week long episode of warm weather. It remains to be seen how such price caps would impact Europe’s capacity to attract LNG.

The question that everybody with a proposed LNG project keeps asking me is: will European buyers start to massively contract LNG so that our LNG projects can move forward? The answer depends on how much LNG Europe really needs over the next two decades, and how much European companies want to contract.

Assessing Europe’s future LNG needs is not straightforward. It depends on the evolution of gas demand, domestic supply (including biomethane), alternative sources of supply and global gas prices. The REPowerEU’s objectives imply that European gas demand would be more than halved by 2030.[7] But the targets to put the EU on that path are so ambitious and likely aspirational, for example on wind and hydrogen,[8] that it’s important to ask: by how much would Europe miss them? And what would the gas demand trajectory be beyond 2030? Moreover, the EU is also looking at other alternative suppliers, for example doubling Azeri gas imports to the EU to 20 bcm.[9] Finally, while this may sound politically unfeasible at this time, one needs to consider the future evolution of imports from Russia. Will they diminish to zero or is there a future that includes peace with Russia, including the return of some Russian gas imports?[10]

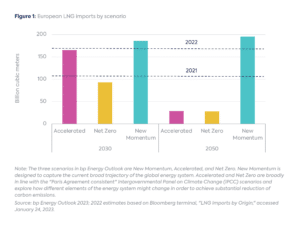

The bp Energy Outlook 2023 illustrates this uncertainty with Europe’s LNG imports varying between 93 and 186 bcm by 2030 and between around 30 to 200 bcm by 2050 (Figure 1).[11]

These uncertainties and decarbonization goals of European economies by 2050 mean that companies (and countries) are hesitant to make long term commitments to large volumes of LNG. Additionally, the EU Methane Strategy is leading to a greater scrutiny on the carbon intensity of those LNG supplies. Ideally, Europe would like to contract clean LNG for 10 years to avoid being stuck with LNG volumes in the late 2040s. If some forecasters are correct about global LNG trade peaking in the mid-2030s, there will be little appetite for those cargoes elsewhere. When German economy minister Habeck recently discussed LNG supply with Qatar for the first time, he was looking for an eight-10-year contract, a far cry from the 20 years desired by many LNG suppliers.[12] Since then, a few 20-year contracts have been signed to supply Europe, but they amount to a timid dipping of a toe into the waters of LNG contracting. 2022 has nevertheless been a record year for LNG contracting, with aggregators and traders signing half of those contracts.[13]

This contrasts with the approach of Asian customers, both in terms of contracted levels and pricing mechanisms. A large share of LNG contracts in Asia still have oil indexation, which has protected those buyers from the sharp increase in spot prices, while an increasing number also have a Henry Hub price indexation. Countries like China have signed unprecedented number of long-term contracts over the past two years, a departure from a heavy reliance on spot supplies. Indian companies have recently indicated their intention to sign several long-term contracts.[14] It remains to be seen whether other Asian countries, which had been partially relying on spot supplies, will follow this trend. LNG exporters should not forget that Asia, not Europe, is the market with the strongest long-term growth potential.[15]

For European stakeholders, the question is how to ensure security of gas supplies while decarbonizing the energy system. Before this crisis, Europe was considered to be the balancing market with no strong growth potential,[16] while Asia was considered to be the premium and fast-growing market.[17] As Europe loses its flexibility tools and is exposed to increased volatility on global gas markets, European players may need a more secure supply strategy than just buying on the spot market with little control on prices and quantities.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] bp, “bp Statistical Review of World Energy,” June 2022, https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html. This compares Japan’s LNG imports in 2010 and 2011.

[2] Bloomberg LP, “LNG imports by origin”, accessed January 24, 2023.

[3]European Commission, “Memorandum of Cooperation Between the European Commission on Behalf of the European Union, and the Ministry of Economy, Trade and Industry of Japan on Promoting and Establishing a Liquid, Flexible and Transparent Global Liquefied Natural Gas Market in the Context of Enhancing the EU – Japan Cooperation on Secure and Sustainable Energy,”, July 2017, https://energy.ec.europa.eu/system/files/2017-07/japanmoc2017_energy_0.pdf.

[4] Bloomberg LP, “TTFGDAHD,” accessed January 24, 2023.

[5] Ministère du Développement Durable, “Données Mensuelles de l’Energie,” acccessed on January 30, 2023, https://www.statistiques.developpement-durable.gouv.fr/donnees-mensuelles-de-lenergie.

[6] Kate Abnett, “EU Countries Agree Gas Price Cap to Contain Energy Crisis,” Reuters, December 19, 2022, https://www.reuters.com/business/energy/eu-countries-make-final-push-gas-price-cap-deal-this-year-2022-12-19/.

[7] European Commission, “Questions and Answers on the REPowerEU Communication,” May 18, 2022, https://ec.europa.eu/commission/presscorner/detail/en/qanda_22_3132.

[8] For example, the EU targets to have 510 GW of installed wind capacity by 2030. That would require 36 GW to be added annually, but only 15 GW was added in 2022. The IEA expects 17 GW to be added over the period 2022-2027. See International Energy Agency, “Is the European Union on track to meet its REPowerEU goals?,” December 2022, https://www.iea.org/reports/is-the-european-union-on-track-to-meet-its-repowereu-goals. The EU also targets to produce 10 million tons of green hydrogen domestically by 2030, requiring 130 GW of electrolyser capacity. Meanwhile, both countries’ targets and announced electrolyser capacity projects are around 40 GW. See International Energy Agency, “Global Hydrogen Review 2022,” September 2022, https://www.iea.org/reports/global-hydrogen-review-2022.

[9] Colm Quinn, “The EU Turns to Baku,” Foreign Policy, July 18, 2022, https://foreignpolicy.com/2022/07/18/azerbaijan-gas-eu-von-der-leyen/.

[10] Kong Chyong, Anne-Sophie Corbeau, Ira Joseph, Tatiana Mitrova, “Future Options for Russian gas Exports,” Center on Global Energy Policy, January 19, 2023, https://www.energypolicy.columbia.edu/publications/future-options-russian-gas-exports/.

[11] bp, “bp Energy Outlook 2023,” January 2023, https://www.bp.com/en/global/corporate/energy-economics/energy-outlook/energy-outlook-downloads.html. Europe includes LNG importers such as EU countries, the United Kingdom and Turkey.

[12] Hazar Kilani, “Qatar-Germany ‘Disagree over LNG’ Supply Conditions,” Doha News, May 10, 2022, https://dohanews.co/germany-qatar-disagree-over-lng-supply-conditions/.

[13] https://www.rigzone.com/news/what_can_gas_and_lng_expect_in_2023-20-jan-2023-171811-article/.

[14] Rakesh Sharma, “India Plans Rush of Long-Term LNG Deals to Speed Shift From Coal,” BNN Bloomberg, February 7, 2023, https://www.bnnbloomberg.ca/india-plans-rush-of-long-term-lng-deals-to-speed-shift-from-coal-1.1880312.

[15] See for example bp, “bp Energy Outlook 2023”.

[16] Europe has been able to smooth shocks in global gas markets in the past, by adapting pipeline imports, coal-fired generation or using its large storage capacity. In case of tightness (e.g., Fukushima), LNG cargoes would be redirected away from Europe; in case of a loose global market (e.g., in 2020), stranded LNG cargoes would flood the European gas market, displacing pipeline gas supplies and filling storage to the maximum.

[17] With Asian spot prices being above European spot prices.

The US-Israeli war against Iran highlights the Gulf’s dual role as the backbone of global energy supply and a major source of systemic risk.

The war in Iran has significantly enhanced Latin America's geopolitical advantage as a reliable source of hydrocarbon resources.

Media reports suggest the Trump Administration is considering restrictions on US oil exports.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Within days of the initial U.S. and Israeli attack on Iran on February 28, 2026, the world was plunged into an energy crisis.