This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

Despite all the advancements we have achieved globally in recent decades, as many as 750 million people still lack access to electricity. Tackling energy poverty requires far more...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Vietnam, long considered a key liquefied natural gas (LNG) growth market in Southeast Asia due to its strong economic and population growth, received its first-ever LNG cargo from Shell at the Thi Vai terminal on July 10, becoming the latest LNG importing country in the world. This Q&A discusses Vietnam’s current and future LNG demand and its implications, such as prospects for the growth of the LNG industry and replacing coal in the power sector.

What does Vietnam’s energy mix look like today and where does natural gas fit in?

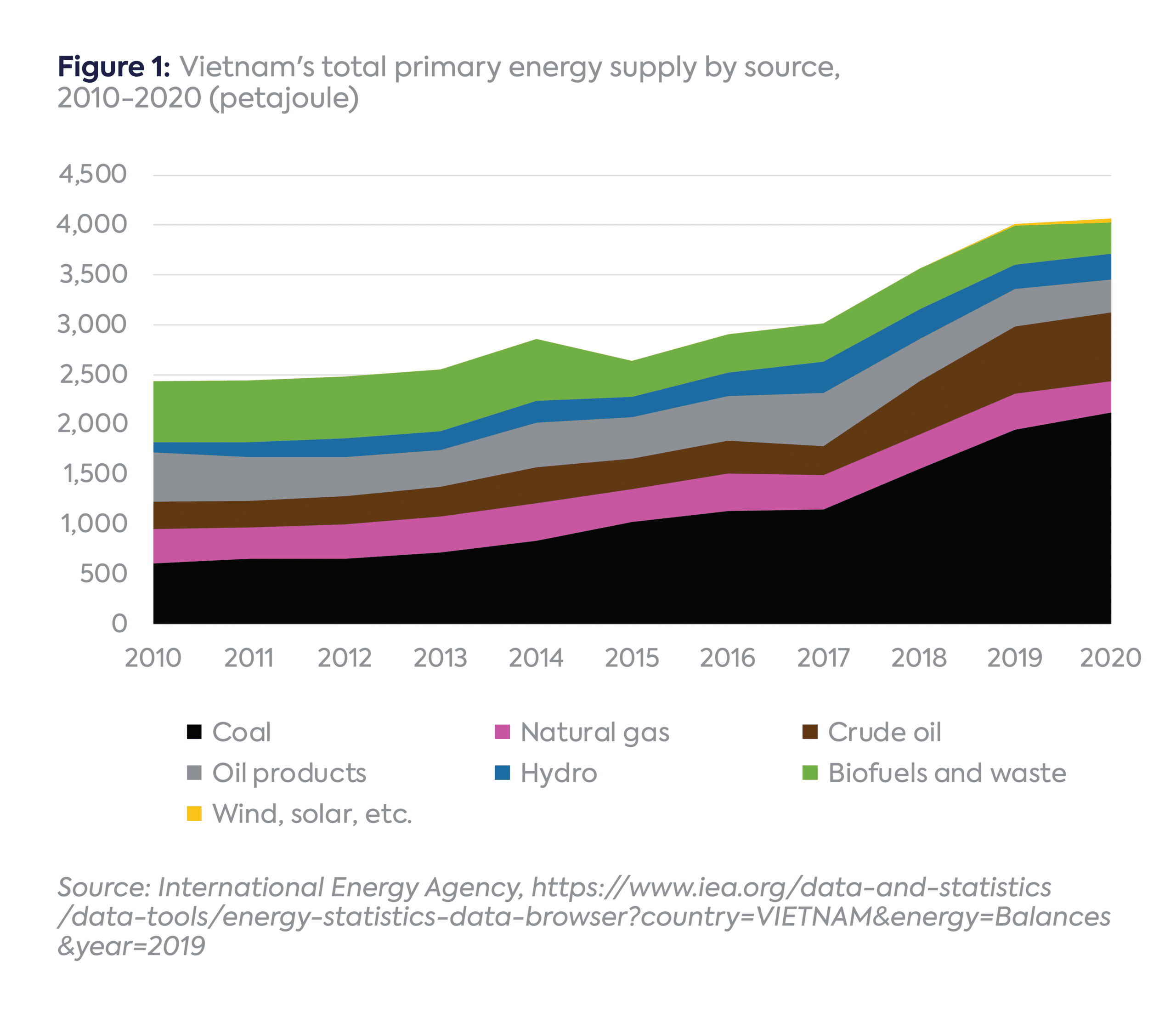

Vietnam’s total energy demand has grown steadily at 7.4 percent per year over the past decade,[1] driven by a robust average economic growth rate of 8 percent per annum and a demographic expansion of 10 percent during the same period.[2] Coal, oil, and natural gas now account for 52, 25, and 8 percent, respectively, of primary energy demand (Figure 1).[3]

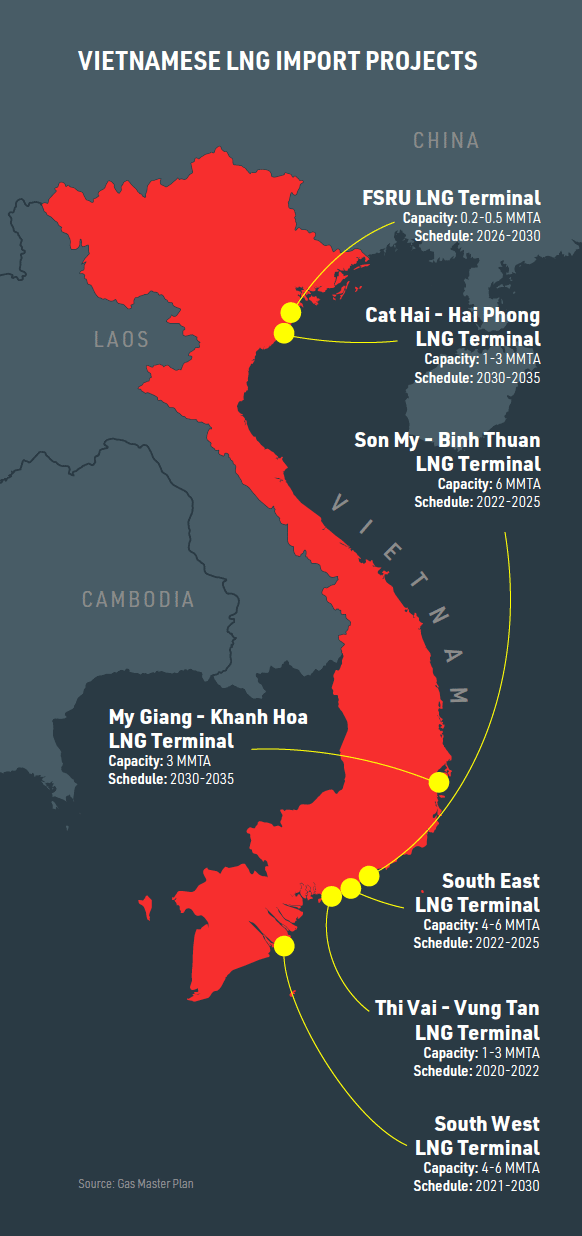

Source: Natural Gas World based on Vietnam’s Gas Master Plan.

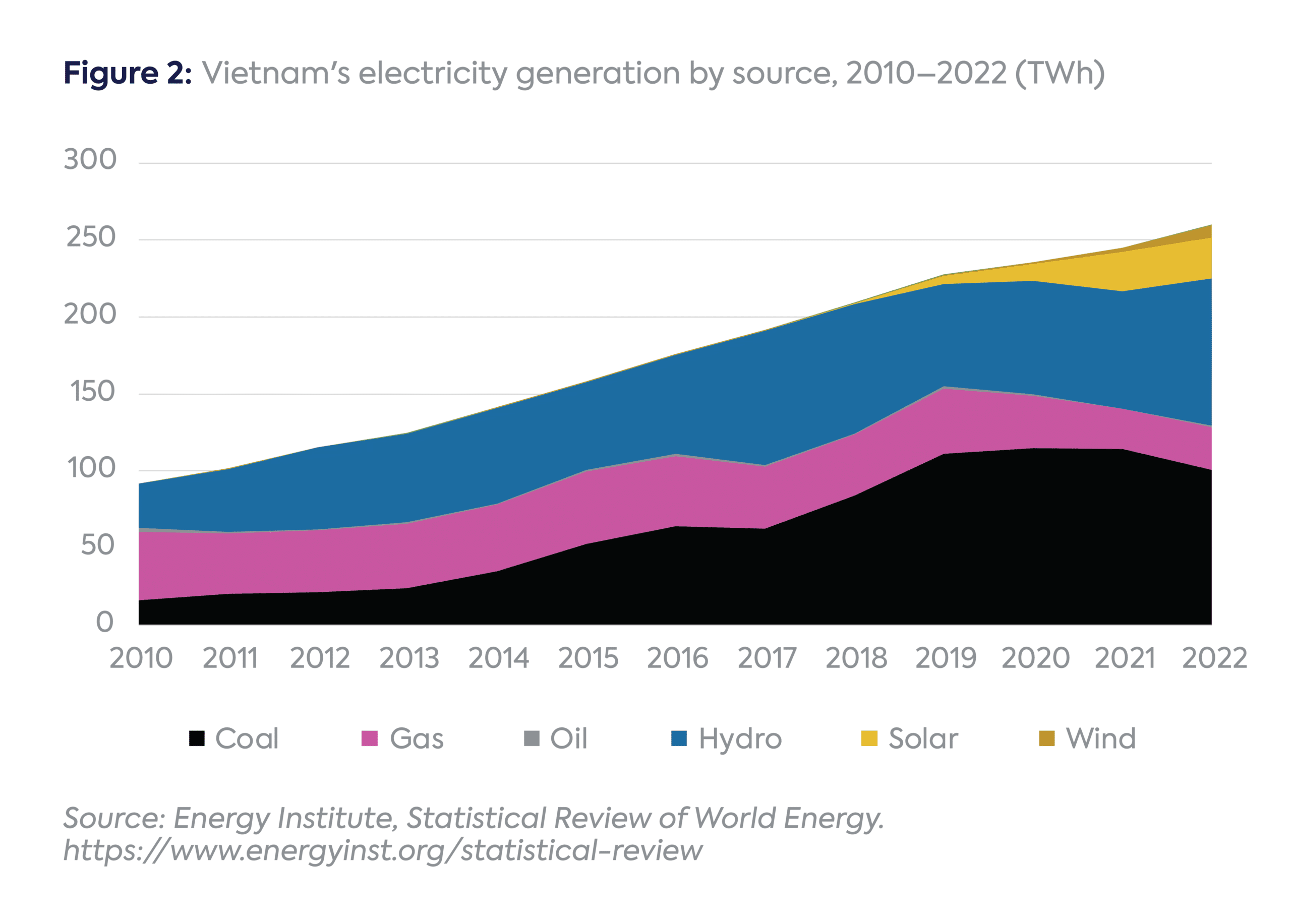

Over the past decade, Vietnam met its incremental power generation needs predominately with coal and hydro. Natural gas consumption, based solely on domestic production, peaked at 10 billion cubic meters (bcm) in 2015.[4] Constrained by declining production, the share of power generated with gas fell from 30 percent in 2015 to 11 percent in 2022.[5] LNG imports can therefore help Vietnam reduce its gas supply gap by facilitating a less carbon intensive fuel than coal for power generation and industrial uses.

The share of coal-fueled power generation grew from 33 percent in 2015 to 49 percent in 2020, before dropping to 39 percent in 2022.[6] Consequently, carbon dioxide, nitrogen oxides, sulfur oxide, and particulate matter emissions have more than doubled during the same period, with coal combustion responsible for 95 percent of this increase.[7]

Vietnam’s government has pledged to achieve net-zero carbon emissions by 2050[8] and confirmed this pledge in its National Climate Change Strategy to 2050.[9] Some key steps to reaching this target include peaking greenhouse gas emissions by 2035, ending buildouts of new coal-fired power plants after 2030, and phasing out coal-fired power plants by 2040. International financing worth $15.5 billion from the recently signed Just Energy Transition Partnership (JETP) aims to support these targets by limiting coal-based generation (among other steps), but much more investment will be needed to achieve Vietnam’s targets.[10]

The Vietnamese power sector is witnessing a solar energy boom in particular (Figure 2). Solar photovoltaic capacity additions have soared from around 100 megawatts (MW) in 2018 to 18,474 MW in 2022. In the future, low-carbon energy sources[11]—including onshore and offshore wind, battery storage, low-carbon hydrogen, and ammonia—are expected to grow.

What are Vietnam’s power sector expansion plans?

At least since 2017, the Vietnamese government has included LNG imports in its energy plans, announcing projects for five LNG importing terminals and more than 10 LNG-fueled power plants in the pipeline.[12] Nevertheless, such plans did not materialize until 2019, when PV Gas (a subsidiary of national oil company PetroVietnam) started construction of the Thi Vai LNG terminal.[13]

The terminal, originally scheduled to start operations in 2022, was first delayed by the impacts of the COVID-19 pandemic,[14] and then faced further setbacks because of extremely high Asian spot LNG prices and high crude oil prices. With a capacity of 1 million tons per annum (MTPA),[15] the Thi Vai terminal will supply the Non Trach 3 and 4 combined cycle power plants once operational.

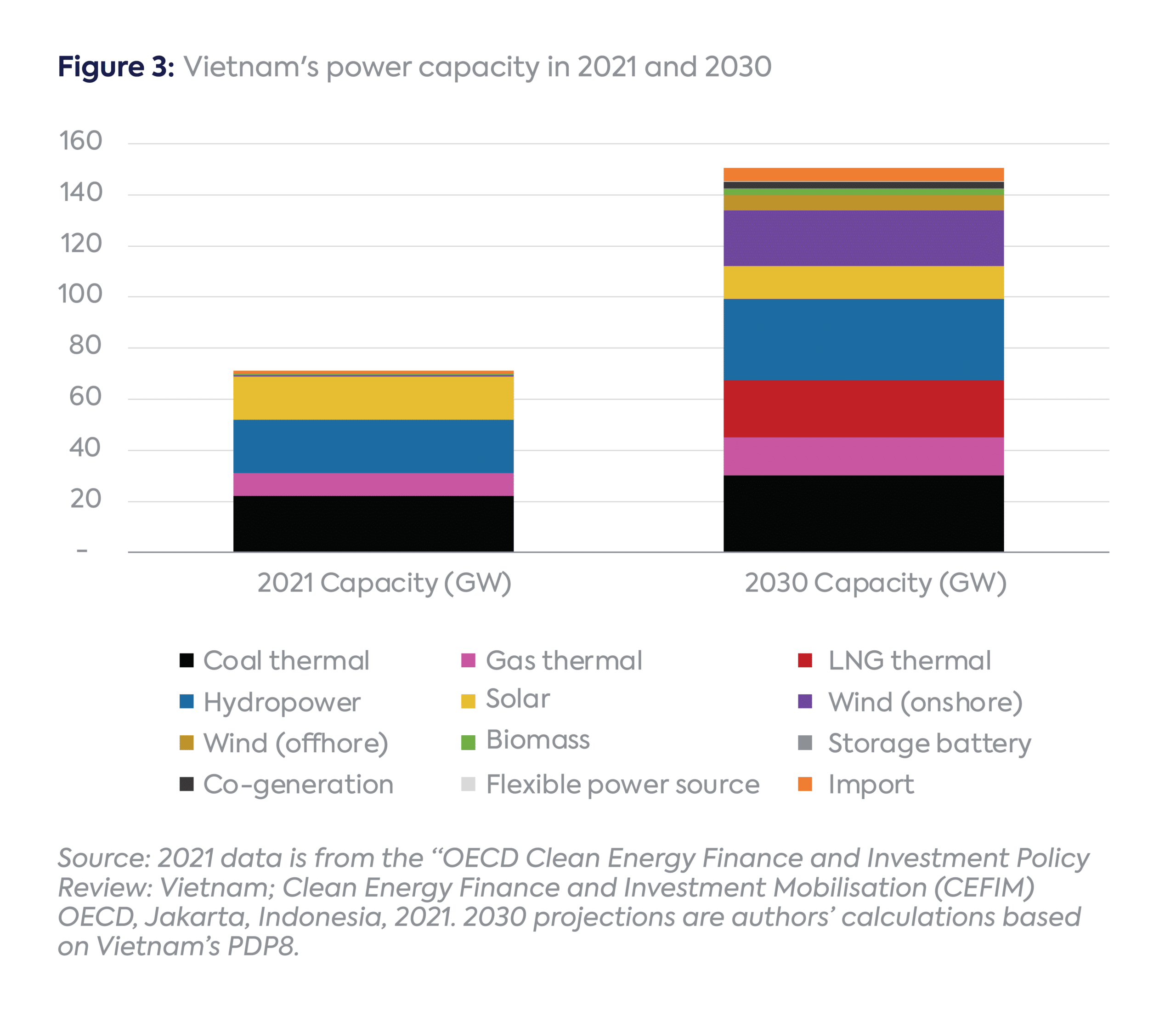

These projects are a key part of an ambitious expansion of Vietnam’s power sector, which is detailed in the Power Development Plan VIII (PDP8)[16] published in May 2023.[17] The PDP8 expects Vietnam’s power capacity to more than double, from 69 gigawatts (GW) in 2021 to 150 GW by 2030 (up from just 34 GW in 2014[18]). This includes:

6 GW of gas-fired plants using domestic gas (+66 percent)

22.4 GW of gas-fired plants using LNG (from zero)

8 GW of coal-fired plants (+36 percent)

28 GW of wind (from 0.5 GW today)

4 GW of solar (from 18 GW today)

Given Vietnam’s ambitious targets, how large can its LNG imports become?

Despite ambitious targets, the expansion faces some challenges, such as uncertainty about future domestic gas production as well as difficulties in “arranging capital” for 7.2 GW of coal-fueled power projects, which, if not “implemented” by June 2024, “must be considered for termination.”[19] Meanwhile, the PDP8 states to limit the role of LNG in the power sector “if there is an alternative to reduce dependence on imported fuels,” highlighting the government’s concern about increasing reliance on LNG imports.

Assuming these power plants operate 50 percent of the time (capacity factor), power plant capacity of 22.4 GW would demand about 13.1 MTPA of LNG. The contrast with today’s reality is stark, with only one out of three LNG terminals in the PDP8—the 1 MTPA Thi Vai LNG terminal—just commissioned. The Hai Linh terminal (3 MTPA), currently undergoing testing,[20] is expected to be commissioned later this year,[21] while the Son My LNG project (3.6 MTPA), promoted by AES and PV Gas,[22] is now expected to be operational by 2027.[23] Theoretically, these three projects, located in Southern Vietnam, would allow up to 7.6 MTPA to be imported by 2026. Not only would this leave a potential gap of 5.5 MTPA to be built before 2030, it would also result in a lack of LNG access to Northern Vietnam, where some of the power plants to be constructed will be located.[24]

Which companies are involved in helping Vietnam realize its LNG ambitions?

PV Gas is the leading player to develop Vietnam’s LNG industry along with a number of foreign companies, including some with direct US government support. Delta Offshore Energy (DOE) plans to build a 2.5–3 MTPA offshore regasification terminal in Bac Lieu Province. A consortium[25] consisting of GE, Bechtel, McDermott, Stena Power & LNG Solutions, and JP Morgan is helping DOE deliver the project. DOE is finalizing a power purchase agreement with state-owned electrical utility Electricity Vietnam (EVN).[26]

AES, another US-based company, has formed a joint venture with PV Gas to construct and operate the Son My LNG terminal in Binh Thuan.[27] Additionally, ExxonMobil and Japanese JERA are working on an integrated LNG-to-power project in Northern Vietnam.[28]

Vietnam receives its first LNG cargo in July 2023 from Shell (photo from PetroVietnam Gas website).

What types of contractual arrangements will Vietnam pursue to meet its LNG demand?

Many Southeast Asian countries rely on a mix of long-term contracts and spot LNG supplies.[29] Vietnam is likely to follow the same path, but has not signed any long-term LNG contract yet. Until 2025, Vietnam will be competing with countries relying on spot LNG supplies, notably in Europe, for either buying spot LNG cargoes or for concluding short-term LNG deals.

The first cargo bought by PV Gas was a spot LNG cargo from Shell. Although spot LNG prices have come down from their peak in 2022, the global LNG market remains tight, with spot prices currently around $12 per million British thermal units (mmBtu), against domestic gas prices above $5/mmBtu in 2021.[30] LNG supply is likely to remain costly and present affordability issues.

PV Gas is also looking at signing long-term contracts, which could provide more price stability than spot cargoes. The company has been in talks with Novatek and ExxonMobil, which have uncontracted LNG supply from their upcoming Arctic LNG 2 and Golden Pass, respectively.[31] Qatar also has significant uncontracted LNG and expects to sign many long-term contracts in 2023, for delivery starting in 2026. These could be a good fit for Vietnam. Delta Offshore Energy launched a Request for Proposal (RFP) in September 2020[32] for 25 years of LNG supply of 2.5–3 MTPA. Some of the potential LNG-to-power projects supported by international players (such as JERA and ExxonMobil) could also be supplied from these companies’ LNG portfolios.[33]

The authors would like to thank Ardhi Rasy Wardhana for their input and help with statistics.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[17] The PDP8 was approved after a delay of over two years, following changes and developments in Vietnam’s leadership and the global energy crisis that followed the Russian invasion of Ukraine. The PDP8 original proposal was submitted by the Ministry of Industry and Trade to the Prime Minister for his approval in 2022.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

When the Iran War disrupted shipping through the Strait of Hormuz and tightened global gas balances, a familiar assumption quickly resurfaced: Russia, possessing the largest proven natural gas reserves in the world, would inevitably emerge as one of the principal beneficiaries.