Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

The decisive move toward a battery economy is intertwined with deep concerns, in the United States and elsewhere, about critical mineral shortages and energy transition supply chains that are currently dominated by China. Yet this concern is not leading to discussions in the US about electric car and battery sizes. This article discusses why that’s a problem if the US wants to meet its energy security and climate goals, and proposes policies to incentivize sales of medium-sized 100 percent battery electric vehicles (EVs) over large ones, as well as a reassessment of the potential role of plug-in hybrids (PHEVs) in the energy transition.

While EVs are becoming increasingly competitive with internal combustion engine (ICE) vehicles in up-front costs, there is a cascading threat now categorically recognized by the International Energy Agency[1]: big cars with large batteries that are mineral guzzlers are growing in popularity. This trend triggers an uncomfortable déjà-vu. For decades, as the US worried about oil importation from the Middle East, Russia, and other regions that it wasn’t politically aligned with, US car sizes kept getting bigger. Even as fuel economy improved, the benefits were partially offset by growing car sizes.[2]

When the US was slowly recovering from the traumatic oil shock recession caused by the Organization of the Petroleum Exporting Countries (OPEC) oil embargo in the mid-1970s, the share of medium-sized cars, or “sedans,” was above 75 percent; 30 years later, 75 percent of new cars were SUVs, vans, or pickups.[3] Given that around 40 percent of US petroleum demand was for passenger vehicles, the US government became preoccupied with security of supply.[4] Domestically, the government kept subsidizing oil and gas production by the billions.[5] Internationally, geopolitical endeavors, such as the Iraq War, have been linked to the oil-dependent US economy.[6]

EV batteries today require a lot of critical minerals, and while the US is strongly focusing on improving supply, both domestically and from friendly countries, these efforts may be insufficient to create security of supply.[7] While battery prices have dropped and energy densities have improved,[8] these gains are partially offset by larger and heavier cars that seek to drive longer ranges on a single charge.

Policies that don’t incentivize sales of medium-sized 100 percent battery electric cars or plug-in hybrids over large, fully battery-powered electric ones are missing a core point of the EV revolution. To decarbonize quickly and limit catastrophic global warming, what is needed is an expansion in collective EV ownership, not of driving ranges for individual consumers.

Automakers and battery producers are integrating and seeking economies of scale. The capital needed to build Gigafactories in China is much lower than anywhere else, so automakers elsewhere need to produce cells at scale to compete. Besides larger electric vehicles delivering higher margins, automakers are also simply responding to consumer preference for larger vehicles—with longer ranges—that are 100 percent battery powered. Perhaps unaware of the impact of their consumption choices, consumers are “maximizing individual utility,” in economic parlance, by choosing larger vehicles. Car companies will compete for sales on this premise.

Government signals could guide EV producers and consumers alike. This may include educating consumers about the impact of car and battery sizes on security of supply and climate. If medium-sized cars or plug-in hybrids are to be incentivized, tailoring fiscal incentives and regulatory policies will help. These include subsidies to benefit smaller batteries or plug-in hybrids, and fiscal penalties, such as taxes, to disincentivize larger vehicles that operate only on batteries.

Battery Sizes

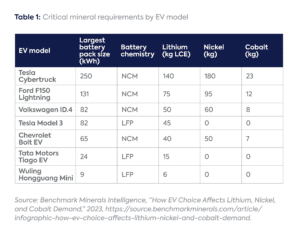

Mineral demands of large 100 percent battery EVs can easily be triple that of medium-sized vehicles. The critical minerals used in the battery of one Tesla Cybertruck, for example, could power three Chevy bolts, or three Tesla Models 3, or even nine Tata Tiagos or plug-in hybrids (Table 1).

There needs to be a greater focus on demand behavior. Take lithium, whose security of supply is a key concern for battery makers. A lithium supply deficit of 12.5 percent is expected by the end of this decade, which could put a high floor price on a mineral without many substitution possibilities in EV applications.[9] There are also serious concerns about China’s outsized role in the lithium supply chain; it processes over 60 percent of global lithium[10] and is a key player in the market for lithium hydroxide, the type of lithium used in long-range nickel manganese cobalt (NMC) batteries.

Yet instead of addressing battery sizes that can rationalize the demand for lithium, US policies are doing opposite: the Inflation Reduction Act has extended the budget threshold for receiving EV subsidies from $55,000 for midsize sedans to $80,000 for fully electric SUVs.[11]

Without a focus on battery size, the future of critical mineral supply security is grim. If annual sales remain constant and the Biden administration’s goal—50 percent share of EVs in car sales by 2030—is realized, the difference between 25 percent (1.75 million) and 75 percent (5.25 million) fully battery electric SUVs[12] in total sales would signify a difference in demand of around 123,000 metric tons of lithium carbonate equivalent (LCE), or about one-fifth of total global lithium production in 2022.[13] That’s a whole lot of lithium.

Also largely missing are discussions about the opportunity that PHEVs offer to be a bridge toward full battery EVs. PHEVs with a battery size of around 30 kilowatt-hours—backed up by an internal combustion engine that can charge the battery when it is depleted—are sufficient to meet the needs of most US passengers who travel between 30 and 40 miles per day. With regulations and safeguards that ensure PHEV passengers would mostly be driving electric, PHEVs can deliver batteries that don’t guzzle minerals[14] while addressing consumer concerns about driving range and recharging capacity.

Battery Chemistries

Battery chemistry matters too. NMC batteries, for example, increasingly contain less cobalt but more nickel. For medium-sized cars, however, NMC batteries can be replaced by lithium iron phosphate (LFP) batteries, which use about the same amount of lithium per kilowatt-hour but no nickel or cobalt at all. LFP batteries are cheaper, safer, and can run more cycles than NMC batteries. But LFP production is not surging in the US because most LFP capacity is in China, which controlled patents until the end of 2022.

With patents released, the US could move faster on LFP. Some manufacturers realize this, as shown by Ford’s plans for an LFP plant in Michigan with the Chinese battery conglomerate CATL,[15] and Tesla’s rumored plan to build LFP plants also using CATL’s LFP technology.[16] At the same time, there are political demands that technology licensed from Chinese players disqualify US companies from accessing tax subsidies, even if those companies own the manufacturing plant in the United States.[17] Behind these politics is the uncomfortable fact that the US needs to cooperate with Chinese technology providers that are simply ahead.

Can medium-sized cars make a comeback after four decades? For that to happen, US policies should focus on incentivizing smaller 100 percent battery EVs and supporting battery types that guzzle less critical minerals. Or they could begin by urgently reevaluating the role of PHEVs, which can operate with smaller battery sizes even as SUVs remain the preferred option. What’s important is a focus on the demand side, so that the costly supply-side fixation of the oil era is not replicated for critical minerals.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] International Energy Agency, “Critical Minerals Market Review 2023,” https://iea.blob.core.windows.net/assets/afc35261-41b2-47d4-86d6-d5d77fc259be/CriticalMineralsMarketReview2023.pdf.

[2] US Environmental Protection Agency, “Highlights of the Automotive Trends Report,” https://www.epa.gov/automotive-trends/highlights-automotive-trends-report#Highlight2.

[3] US Environmental Protection Agency, “2022 EPA Automotive Trends Report,” https://www.epa.gov/system/files/documents/2022-12/420r22029.pdf.

[4] Nancy W. Stauffer “US Passenger Cars,” MIT Energy Initiative, January 10, 2012, https://energy.mit.edu/news/us-passenger-cars/#:~:text=Effects%20of%20US%20driving%20habits,change%20and%20energy%20security%20reasons.

[5] USG, “United States Self-Review of Fossil Fuel Subsidies,” 2015, https://www.oecd.org/fossil-fuels/publication/United%20States%20Self%20review%20USA%20FFSR%20Self-Report%202015%20FINAL.pdf.

[6] Raymond Hinnebusch, “The US Invasion of Iraq: Explanations and Implications,” Critique: Critical Middle Eastern Studies 16:3 (October 2007): 209-228, https://www.tandfonline.com/doi/pdf/10.1080/10669920701616443.

[7] Aspen Institute, “A Critical Minerals Policy for the United States,” 2023, https://www.aspeninstitute.org/wp-content/uploads/2023/06/Critical-Minerals-Report.pdf.

[8] Ahmed Mehdi and Tom Moerenhout, “The IRA and the US Battery Supply Chain: Background and Key Drivers,” June 8, 2023, https://www.energypolicy.columbia.edu/publications/the-ira-and-the-us-battery-supply-chain-background-and-key-drivers/.

[9] Benchmark Minerals Intelligence, “Albemarle’s Turbo-Charged Demand Data Showcases Lithium’s Growing Supply Problem,” 2023, https://source.benchmarkminerals.com/article/opinion-albemarles-turbo-charged-demand-data-showcases-lithiums-growing-supply-problem.

[10] Ahmed Mehdi and Tom Moerenhout, “The IRA and the US Battery Supply Chain: Background and Key Drivers,” June 8, 2023, https://www.energypolicy.columbia.edu/publications/the-ira-and-the-us-battery-supply-chain-background-and-key-drivers/.

[11] US Department of the Treasury, “Treasury Releases Proposed Guidance on New Clean Vehicle Credit to Lower Costs for Consumers, Build U.S. Industrial Base, Strengthen Supply Chains,” March 31, 2023, https://home.treasury.gov/news/press-releases/jy1379.

[12] Twenty-five percent SUVs would represent 1.75 million SUVs and 75 percent SUVs would represent 5.25 million SUVS; calculations are assuming an average 60 kilograms (kg) of LCE per electric SUV and 25 kg of LCE per electric sedan.

[13] Benchmark Minerals Intelligence, “Global Lithium Supply Forecasts to Hit 1 Million Tonnes for First Time,” 2023, https://source.benchmarkminerals.com/article/global-lithium-supply-forecast-to-hit-1-million-tonnes-for-first-time.

[14] Jeremy Neubauer and Eric Wood, “The Impact of Range Anxiety and Home, Workplace, and Public Charging Infrastructure on Simulated Battery Electric Vehicle Lifetime Utility,” Journal of Power Sources 257 (July 1, 2014), https://doi.org/10.1016/j.jpowsour.2014.01.075.

[15] Ford, “Ford Taps Michigan for New LFP Battery Plant,” press release, February 13 2023, https://media.ford.com/content/fordmedia/fna/us/en/news/2023/02/13/ford-taps-michigan-for-new-lfp-battery-plant–new-battery-chemis.html.

[16] Dan Mihalascu, “Tesla Said to Plan US Battery Cell Factory Using CATL’s LFP Tech,” Inside EVs, March 31, 2023, https://insideevs.com/news/660046/tesla-said-plan-us-battery-cell-plant-using-catl-lfp-tech/.

[17] “Rubio Introduces Bill to Block Subsidies to Chinese Battery Companies,” press release, March 9, 2023, https://www.rubio.senate.gov/public/index.cfm/2023/3/rubio-introduces-bill-to-block-subsidies-to-chinese-battery-companies.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

One of the central objectives of the second Trump administration has been to pursue a maximalist trade policy toward China.

The US Export-Import Bank is preparing to close the first funding tranche of Project Vault, a public-private partnership establishing the US Strategic Critical Minerals Reserve.

As the US and Europe navigate a difficult and uneven shift toward full battery electric vehicles (BEVs), the US and EU auto markets are under heavy pressure.

High political walls are hurting an industry vital to the character of the country.