Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Commentary by Ahmed Mehdi & Tom Moerenhout • June 08, 2023

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

In a bid to unlock incentives for clean energy technologies and transform the position of the United States on the global clean energy map, the Biden administration succeeded in getting the Inflation Reduction Act (IRA) passed into law on August 16, 2022. Among the many tax incentives the bill gives to clean energy industries, it provides massive support for the lithium-ion battery (LiB) value chain for electric vehicles (EVs) and energy storage. In less than one year since its passage, the IRA has already led to a flurry of investment activity, particularly in the US downstream cell industry,[i] and has been touted as a major game changer for US battery economics.

Just as crude oil was the key raw material for the 20th century, battery metals such as lithium, nickel, and copper will be the key materials for the 21st-century electric economy. Batteries are a core part of net-zero roadmaps, both for electric vehicle manufacturing and renewables deployment rates. Battery metals derive their status as “critical” materials from being a major input for battery cathodes—the highest-value component of a LiB—placing them at the heart of the electrification debate.[ii]

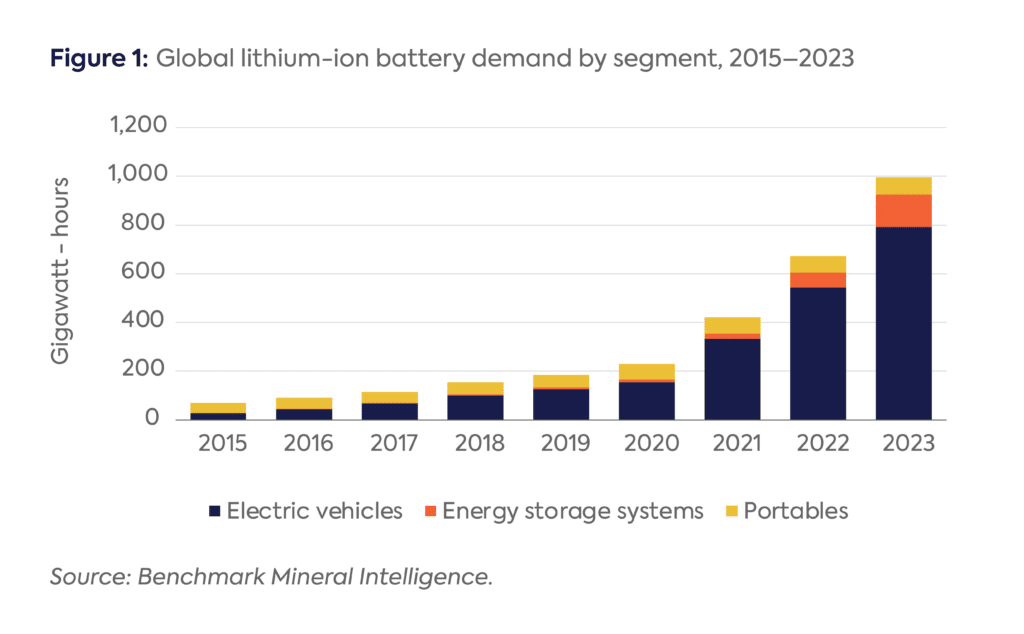

Last year saw global LiB demand reach almost 700 gigawatt-hours (GWh), a 67 percent increase year on year.[iii] As the key platform technology for electric vehicles, energy storage systems, and portables (see Figure 1), LiBs are expected to witness demand growth at an annual compound growth rate (CAGR) of 20 percent over the next decade. As evidence of this anticipated growth, there are now more than 380 gigafactories[iv] in the pipeline through 2030 (compared to just 10 five years ago), though not all of them will be built. Policy makers and original equipment manufacturers (OEMs) have been confronted by the dual challenges of scaling raw material supply to meet electrification targets and ensuring the rules of the clean energy geopolitical playbook are not solely written by China—currently the most dominant actor across the entire LiB value chain.

Against this backdrop, the passage of the IRA has reshuffled the economics and geopolitics of the LiB value chain. This commentary, the first in a two-part series, addresses the economics of the battery supply chain, who controls its key components, and, most importantly, how the IRA changes the position of the US in the global battery market. It will show that the IRA was necessary from a security-of-supply perspective, and allows the US to diversify critical supply chains, as evidenced by strong levels of investment in those supply chains both in the US and among its strategic partners since the enactment of the industrial policy.

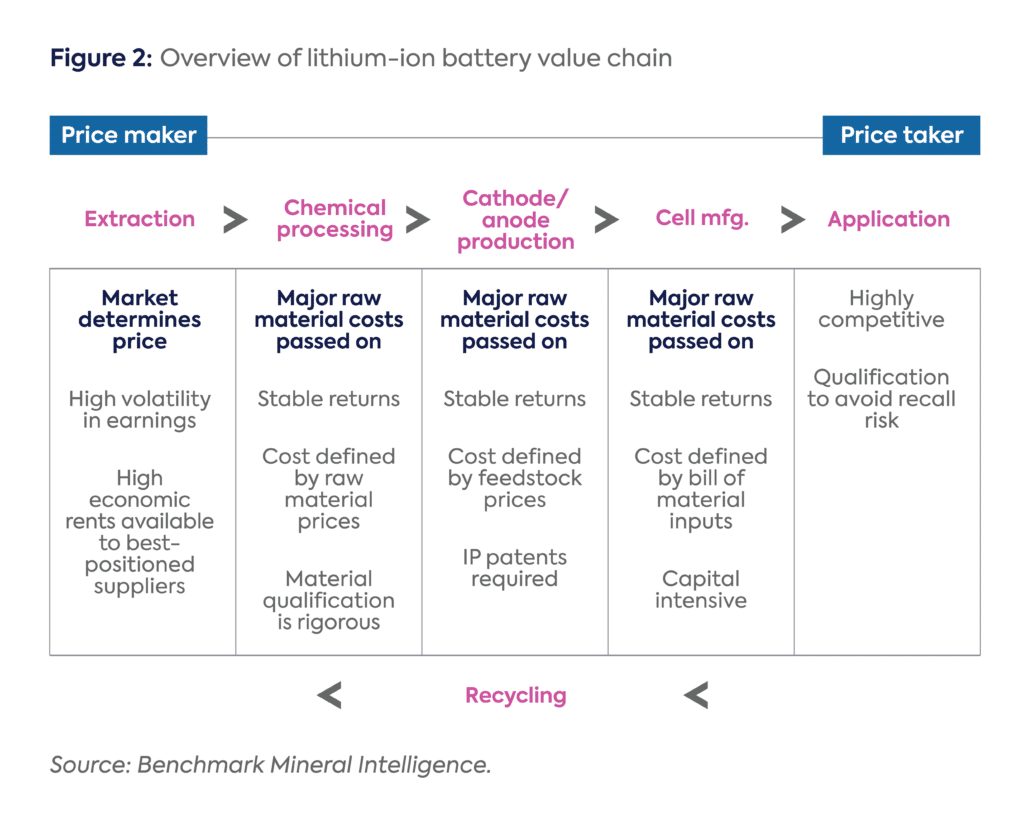

The global LiB value chain is both long and deep (see Figure 2 for an overview) and includes materials used to produce key battery components: the cathode (which is used to store ions when a battery is used); the electrolyte (which allows ions to move through the battery); the anode (which, during battery discharge, allows positively charged ions to flow to the cathode); and the separator (a barrier preventing the anode and cathode from interacting). Each of these components relies on engineering, technology, and chemical processes, and ultimately on the availability of critical minerals needed for their production.

A key characteristic of the battery is its energy density, a measure (in watt-hours per liter [Wh/L]) of energy stored per unit of volume. The higher a battery’s energy density, the more energy it can store—and, in the case of electric vehicles, the greater the range on a single charge. The cathode is critical to determining a battery’s energy density because its capacity determines the battery’s overall energy storage capacity, which in turn indicates the battery’s energy density.

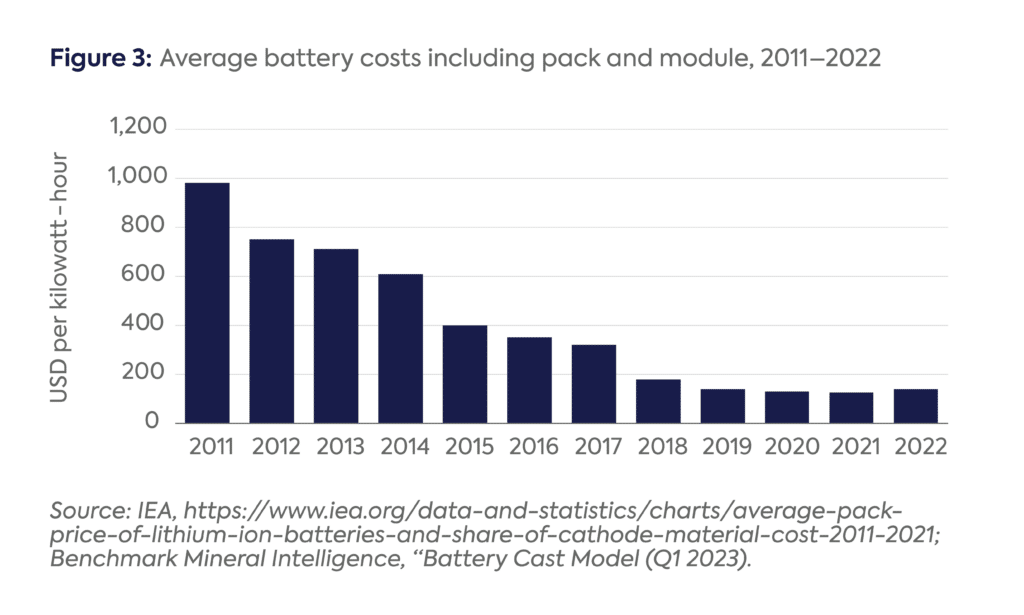

Broadly speaking, the global battery industry has made significant gains over the past decade in both battery cost reductions and technological performance, specifically energy density. With respect to battery cost reductions, the scaling of gigafactories[v] has enabled economies of scale as well as a reduction in manufacturing costs through learning-by-doing. Combined with improvements in cell manufacturing (such as process automation and enhanced electrode manufacturing), this has led to a dramatic fall in average battery pack costs since 2010 (see Figure 3).

Because the global battery industry is not commoditized, margins and costs differ across battery types. Currently, the two dominant LiB types are those with nickel, manganese, and cobalt in the cathode (NMC) and those with lithium, iron, and phosphorous in the cathode (LFP). Over the past decade, battery technologies have continuously improved. For example, cell energy density has risen from around 120 watt-hours per kilogram (Wh/kg) (264 Wh/L) a decade ago to around 270 Wh/kg (650 Wh/L) today, as the global EV industry has embraced higher nickel-cathode technologies. Even lower energy density LFP cathodes have seen significant technology improvements.[vi]

Generally speaking, energy density gains have an inverse relationship to cost. For now, though, the current generation of positive electrodes have largely reached their performance limits,[vii] at least until next-generation high-nickel cells (NCM 811) increase market share or solid-state batteries move beyond the lab stage to mass commercialization (a trend not expected to take root until the mid-2030s[viii]).

With most cost declines having been achieved at a pack and manufacturing level and most gains extracted from an energy density level, cathode raw material costs as a proportion of overall cell costs have increased. Given that raw materials make up around 90 percent of cathode costs[ix] and the cathode now accounts for around 50–60 percent of battery cell costs,[x] critical inputs such as lithium (which has similar chemical intensities across different cell types) have grown in importance. Anode materials such as graphite (and silicon dopants[xi]) also remain key to the performance of the battery, but represent only around 10–11 percent of overall cell costs.[xii] In short, cathode costs now drive overall battery costs, and by extension the cost of EVs.

So why does this matter for the electrification targets of governments and OEMs?

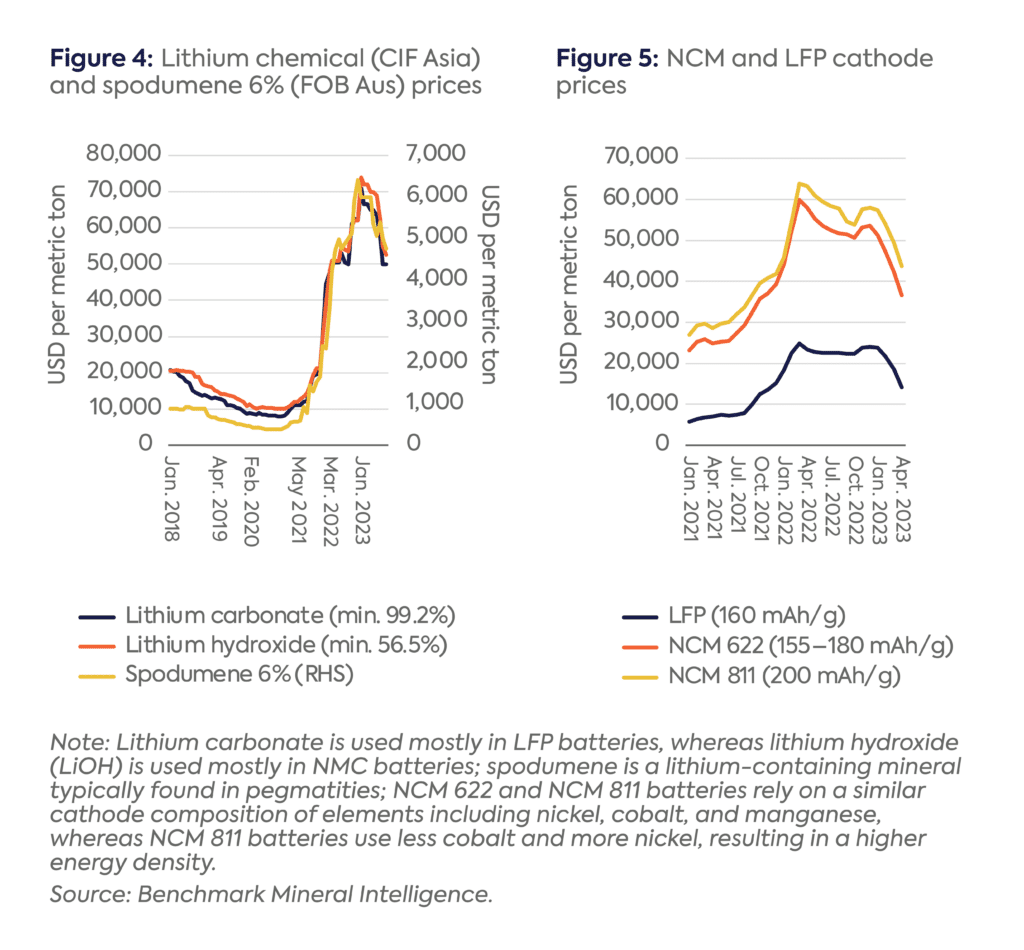

The battery industry largely operates on a cost pass-through basis, which puts the onus on OEMs to absorb the rise in raw material prices, leading to margin compression and pressure on governments to ensure that EV uptake is not compromised. As critical minerals supply is already tight and demand is increasing faster than supply for key minerals such as lithium, price volatility may ensue alongside a general increase in input prices (see Figures 4 and 5). This will continue in coming years because the lead times between exploration and production of these minerals takes, on average, more than a decade. Notwithstanding other obstacles such as the inflationary impact on long-run incentive prices[xiii] and ongoing challenges with permitting, the inelasticity of supply has been a growing concern for industry participants—as it has directly impacted cathode and EV costs, which, if passed on to the consumer, could impair EV adoption rates.[xiv]

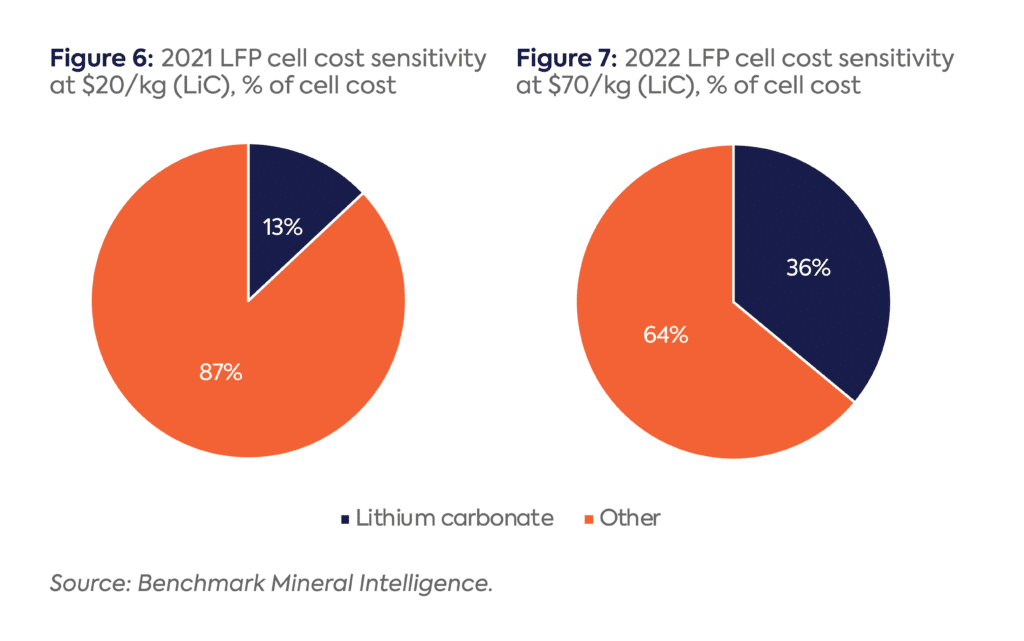

Figures 6 and 7 provide an example of cell cost sensitivity to rising lithium prices through the example of two price scenarios and their impact on LFP cell costs. Figure 6 shows that under a scenario where lithium prices are around $20,000 per ton, lithium carbonate accounts for around 13 percent of the total cell cost of around $100/kWh[xv]; meanwhile, under a $70,000 per ton spot price scenario (as witnessed in 2022), the LFP cell cost inflates up to around $140/kWh, with the lithium cost eating up around 35 percent of this share.[xvi]

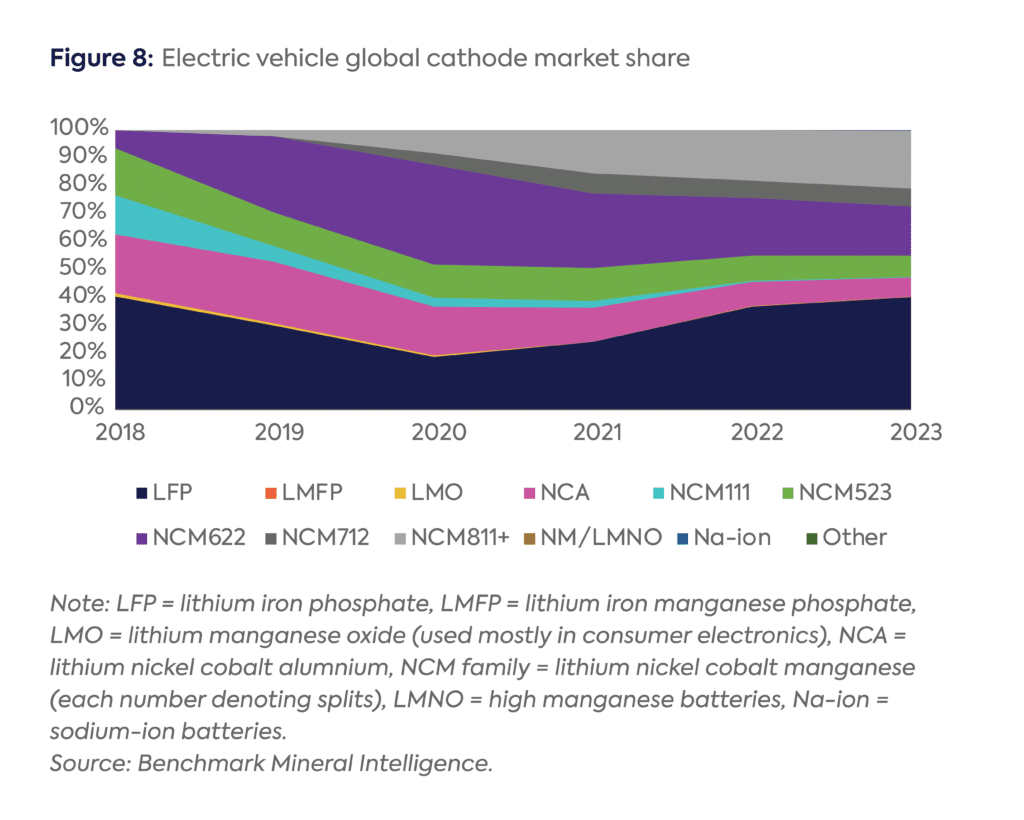

While there has been discussion[xvii] about future battery chemistry projections for the EV industry, OEM technology roadmaps have stuck with a variety of cathode formulations with common trade-offs between cost, performance, and safety. Figure 8 provides an overview of key cathode formulations used in the EV industry today. In general, the trend in EV battery chemistry is a combination of high-performance, high-cost, high-nickel batteries (NCM 811) and medium-performance, low-cost, no-nickel batteries (LFP).

Because of the sensitivity of cathode active material costs on margins, OEMs have ventured to vertically integrate to directly source critical minerals and de-risk mining operations.[xviii] Simultaneously, governments have stepped in to ensure subsidies are in place across the supply chain, from mining to EV purchases, often with the fundamental goal of localizing battery production.

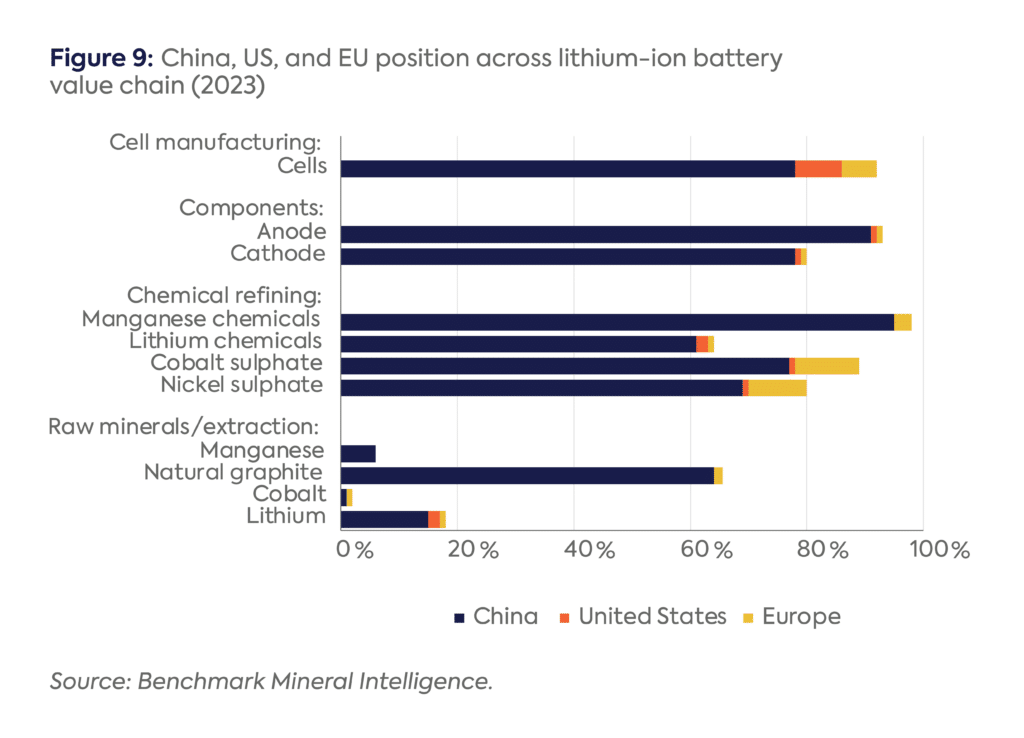

In addition to the cost pressures faced by OEMs and their wakeup call on raw material supply so late in the day, governments are waking up to the reality that the battery industry has been overtaken by geopolitical considerations. This development is not surprising given China’s outsized role across the entire supply chain coupled with the deterioration of US-China relations (see Figure 9 below). While China plays a small, albeit significant, role in upstream mining, it dominates the midstream and downstream parts of the battery supply chain: Chinese firms currently refine around 60 percent of the world’s lithium, 69 percent of the nickel, 75 percent of the cobalt, and all the world’s natural graphite.

The country’s dominant position in battery cell production is supported by its dominance of cathode and anode production, and the economies of scale of big players such as Chinese LiB manufacturing giants CATL and BYD. China accounts for more than 75 percent of global cathode and anode supply, and about 78 percent of global battery cell supply. In terms of cell type, the starkest dependency is on LFP cells, with China controlling around 99 percent of LFP cathode output.

Lithium is arguably the most geopolitically sensitive material in the battery supply chain. Both the complexities of bringing on new lithium supply (with average project delays of 2–3 years) and limited substitution risk from alternative technologies reinforce this point.[xix] In short, lithium is key to unlocking net-zero targets.

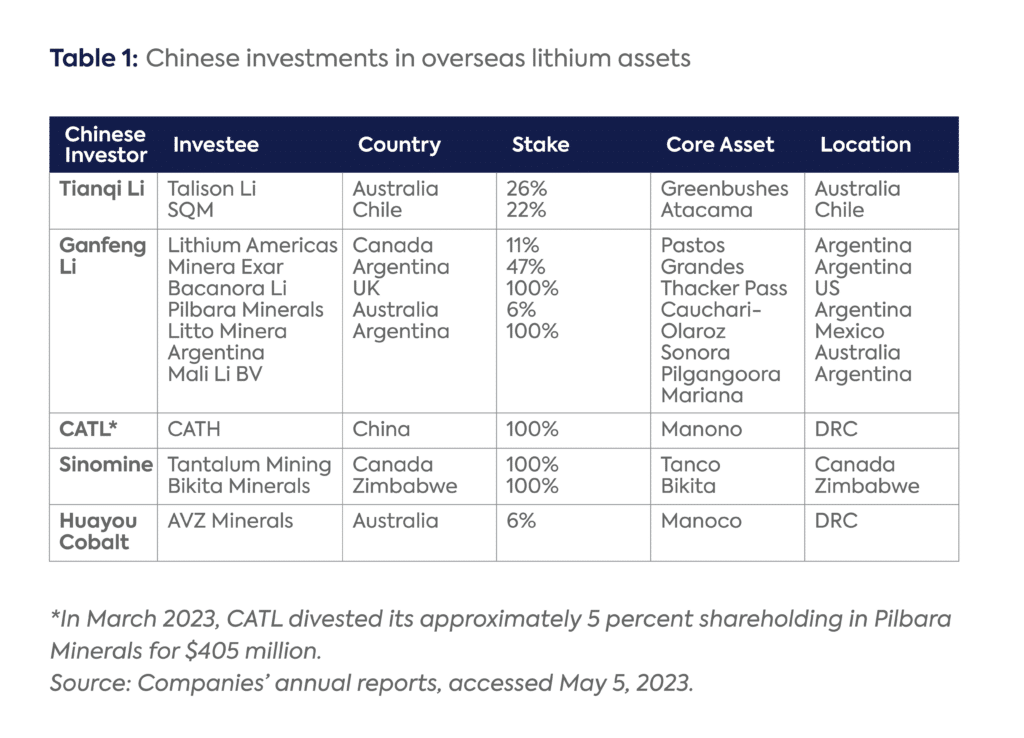

While China has an outsized role in lithium refining capacity, domestic mined lithium output (typically consisting of low-grade micas and lepidolite grades) is high-cost. Over the past decade, China has relied heavily on raw material supply from two key countries: Australia (a key supplier of hard-rock spodumene) and Chile, where brine is used to produce lithium carbonate (which can also be converted into hydroxide, at a cost). China has spent the past decade securing offtakes or equity stakes in high-class deposits around the world (see Table 1).

While it is true that some US companies (e.g., Albemarle) have strong refining positions in China, and that Australia’s dominance in hard rock production acts as a geopolitical counterweight to China’s midstream dominance, the reality remains that China enjoys a decades-long head start over the West. Amid the Ukraine conflict and anxieties over security of supply, scenarios of cell supply being cut, tariffs being imposed, or even chemical supply being curtailed have garnered attention. However, localization policies such as the IRA are as much about government support to scale raw material supply as they are a response to such potential scenarios; in an energy world where supply chains are no longer regime-agnostic, the balance between building a supply chain that deals with issues such as cost, emission intensity of transport and production, and geopolitics is becoming increasingly difficult—a point that is already apparent in how the IRA is being discussed in Washington.[xx]

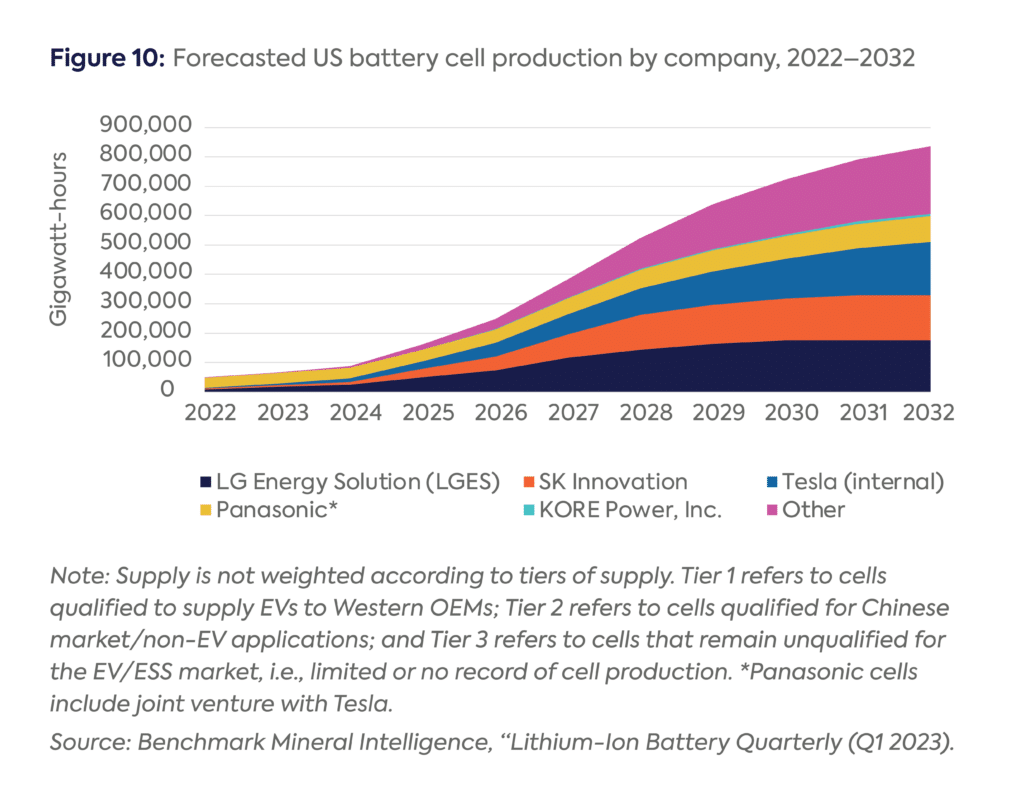

The balancing act between building supply chains that can deliver deployment and geopolitical relevance is apparent in the case of the US. President Biden has set a goal of ensuring that 50 percent of all new vehicles sold in 2030 are zero-emission vehicles.[xxi] Last year the US sold around 1 million EVs, representing a penetration rate of almost 6 percent, double that of 2021 even if overall new car registrations decreased.[xxii] Battery demand in the US is expected to rise from around 36 GWh in 2021 to just over 800 GWh by 2032.[xxiii] So far, the US has made major inroads in cell supply, led by Tesla (the front-runner) and supported by South Korean joint venture partners such as LGES, SKI, and Panasonic (Tesla’s original joint venture partner).

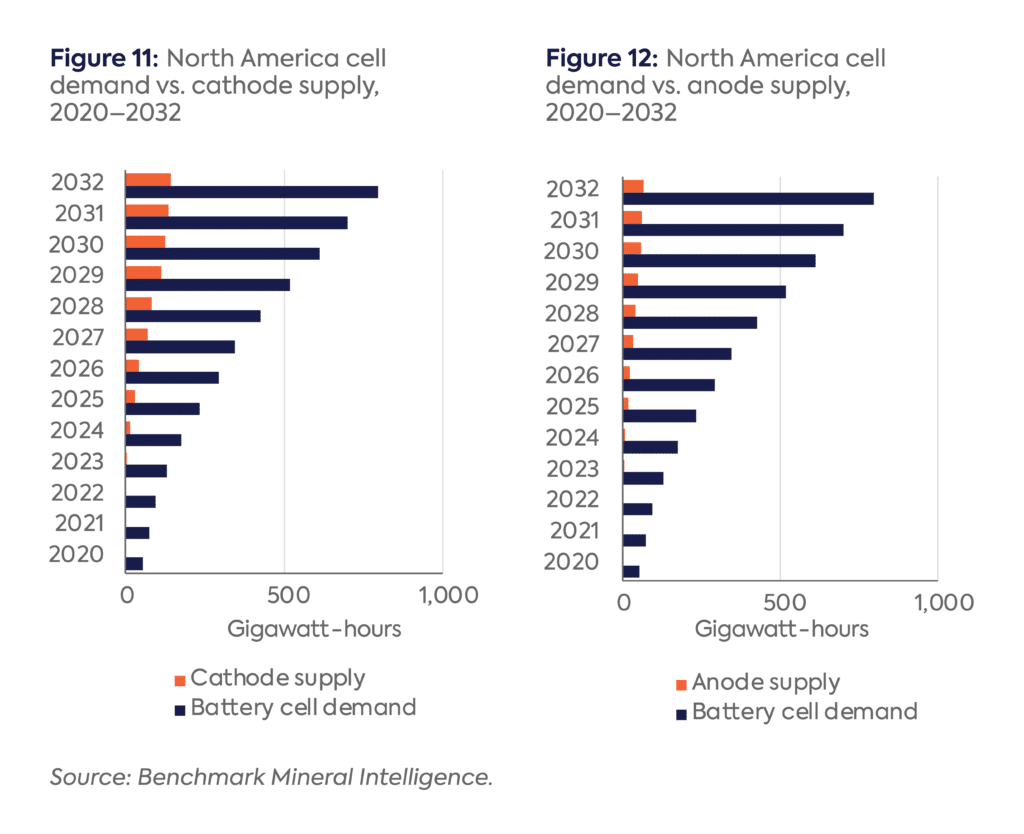

While the US has made successful inroads in downstream cell investment as well, the challenges of localization are apparent in other parts of the supply chain—a key trigger for the IRA. In the midstream, shortages of cathode and anode, currently estimated to be 82 percent and 92 precent, respectively (see Figures 11 and 12), represent a major bottleneck for regional supply security, increasing US exposure to Chinese imports. Projections through 2032 show clearly that cathode and anode supply in North America will not meet demand. This situation contrasts with that of battery cell supply. It is expected that by 2032 North America will have the gigafactories available to satisfy cell demand, but will not have the local supply of cathodes and anodes to construct those cells; in other words, it will remain dependent on imports.

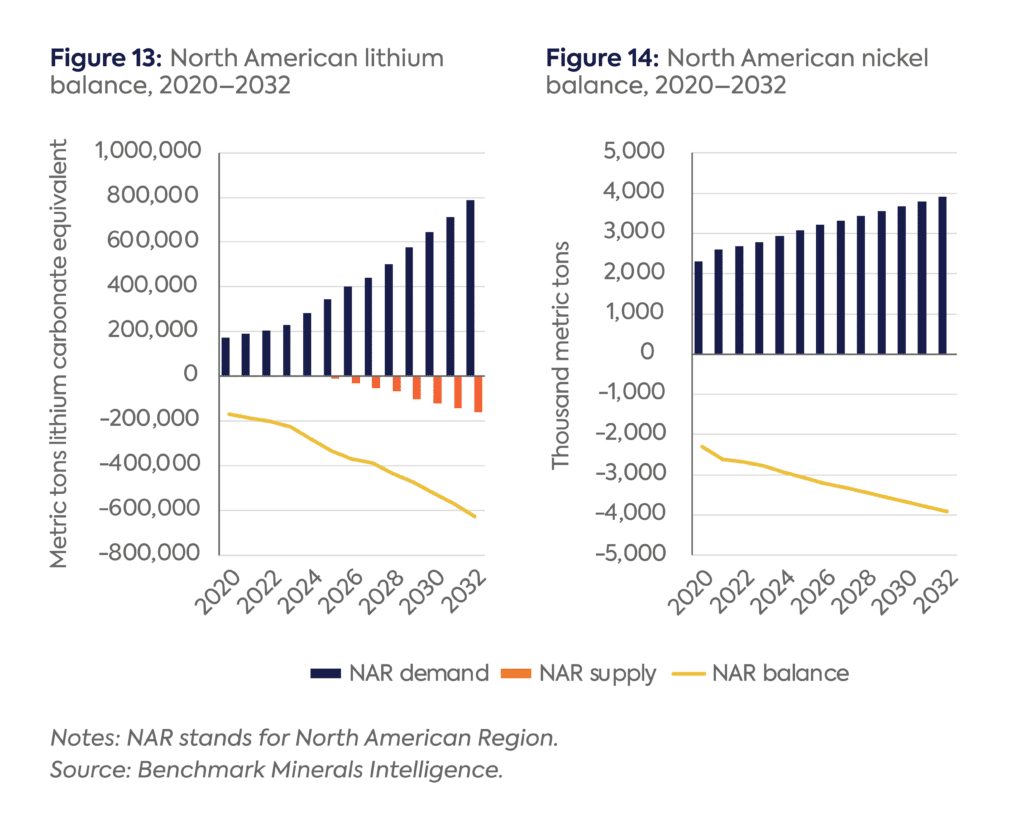

Shortages of lithium and nickel mean that the US will also remain dependent on imports of critical minerals used for cathode manufacturing. North American lithium and nickel balances show that supply-demand shortage (see Figures 13 and 14 below) will render US procurements largely dependent on players in China and Indonesia.

As this commentary has made clear, the battery industry is at an inflection point. Suppliers face numerous requirements in their supply chain, including ensuring sufficient supply to meet demand; minimizing cost increases to avoid impacting electric vehicle costs; improving environmental, social, and governance (ESG) standards in critical mineral mining; and addressing geopolitical concerns to reduce reliance on China. In addition to incentivizing EV uptake, the IRA is designed to address these challenges. It seeks to take on a difficult balancing act between using fiscal policy as an anchor to de-risk investment flows into the supply chain and ensuring that the US is not hostage to China. The ability to sustain this balancing act depends on how OEMs and the industry grapple with the new rules—a major test of whether policy design will align with the margin sensitivities of the battery value chain or geopolitics will trump economics and create additional hurdles and costs for EV deployment in the West.

[i] According to the International Energy Agency, between August 2022 and March 2023, post-IRA investments amounted to approximately $52 billion in North America—50 percent of which was for battery manufacturing and 20 percent for components and EV manufacturing. Source: International Energy Agency, Global EV Outlook 2023, April 2023, https://www.iea.org/reports/global-ev-outlook-2023/executive-summary.

[ii] Batteries account for 40 percent of the cost of an EV. See: Bernstein Research, “Global Energy Storage: Are Car Companies a Threat to Battery Makers?,” May 2022.

[iii] Benchmark Mineral Intelligence, “Li-ion Battery Quarterly Database (Q1 2023).”

[iv] Originally coined by Tesla, “gigafactory” refers to a large-scale manufacturing plant for producing batteries for EVs/energy storage systems (typically over 1 GWh capacity). Source: Benchmark Mineral Intelligence, “Benchmark Gigafactory Assessment,” April 2023.

[v] According to Bernstein, battery plant size has doubled every 5 years from 2 GWh in 2013 to 4 GWh in 2017 to more than 20 GWh in the mid-2020s.

[vi] These innovations include advanced battery architecture and cell design. For example, LFP cell-to-pack (CTP) technology eliminates the requirement for modules to house cells, reducing dead weight and improving energy density. CTP tech has been deployed by BYD with its Blade battery and CATL.

[vii] Particularly given safety considerations due to the use of liquid electrolyte.

[viii] According to Benchmark Mineral Intelligence, solid-state batteries—which replace the liquid electrolyte used in traditional lithium-ion batteries with a solid separator—remain in infancy, with just 2 GWh in current supply. See: Benchmark Source, “Emerging Solid-State Industry Has 9% Utilisation Rate as Production Ramps Up,” May 11, 2023, https://source.benchmarkminerals.com/article/emerging-solid-state-industry-has-9-utilisation-rate-as-production-ramps-up.

[ix] See: Bernstein Research, “Turn Up the Voltage…Investing Across the Battery Value Chain,” October 2022.

[x] Benchmark Mineral Intelligence, “Battery Cost Model (Q1 2023).”

[xi] Silicon oxide used to increase energy density of graphite anodes.

[xii] Benchmark Mineral Intelligence, “Battery Cost Model (Q1 2023).”

[xiii] See: Benchmark Source, “Will Oil and Gas Companies Invest in the Battery Supply Chain? Q&A with Ahmed Mehdi,” February 9, 2023, https://source.benchmarkminerals.com/article/will-oil-and-gas-companies-invest-in-the-battery-supply-chain-qa-with-ahmed-mehdi.

[xiv] Tom Moerenhout, James Glynn, and Lilly Lee, “Assessing Critical Mineral Supply Constraints for Inclusion in Energy Transition Models,” Center on Global Energy Policy, 2023 (forthcoming).

[xv] Includes cost of remainder cathode (preparation cost and cathode margin) and cell manufacturing cost (e.g., separator, electrolyte, and packaging materials), as well as processing costs (energy, labor, depreciation, etc.).

[xvi] Spot price is illustrative only as most cell producers will have offtakes linked to a formula price based on bilateral contract prices.

[xvii] See: International Energy Agency, The Role of Critical Minerals in Clean Energy Transitions–Analysis, May 2021, https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions.

[xviii] Mike Colias and Scott Patterson, “The New EV Gold-Rush: Automakers Scramble to Get into Mining,” Wall Street Journal, May 15, 2023, https://www.wsj.com/articles/the-new-ev-gold-rush-automakers-scramble-to-get-into-mining-ebda14eb.

[xix] Despite growing interest in sodium-ion batteries, energy density still remains an issue and key utilization will be more applicable for the energy storage market.

[xx] See for example: Josh Siegel, “Manchin’s ‘Playing with Fire’—and Some Democrats Are Tired of the Drama,” Politico, May 1, 2023, https://www.politico.com/news/2023/05/01/joe-manchin-joe-biden-fued-00093131.

[xxi] The White House, “Fact Sheet: President Biden Announces Steps to Drive American Leadership Forward on Clean Cars and Trucks,” August 5, 2021, https://www.whitehouse.gov/briefing-room/statements-releases/2021/08/05/fact-sheet-president-biden-announces-steps-to-drive-american-leadership-forward-on-clean-cars-and-trucks/.

[xxii] Dan Mihalascu, “EVs Made Up 5.6 Percent of US Car Market in 2022 Driven by Tesla,” Inside EVs, February 20, 2023, https://insideevs.com/news/653395/evs-made-up-5point6-percent-of-overall-us-car-market-in-2022-driven-by-tesla/.

[xxiii] Benchmark Mineral Intelligence, “Li-ion Battery Quarterly Database (Q1 2023).”

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

One of the central objectives of the second Trump administration has been to pursue a maximalist trade policy toward China.

Full report

Commentary by Ahmed Mehdi & Tom Moerenhout • June 08, 2023