Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

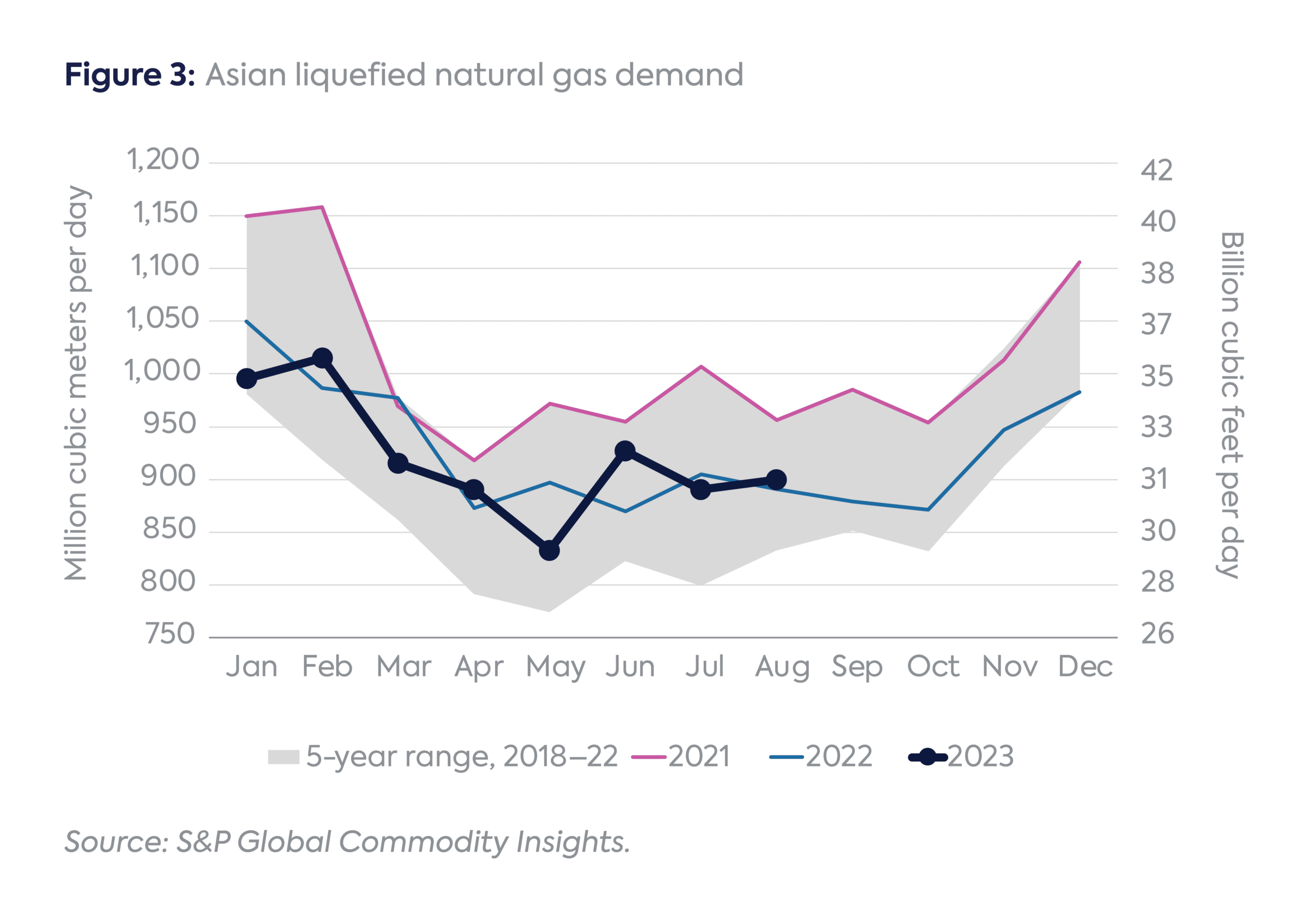

An immense amount of capital is flowing into creating the next generation of liquefied natural gas (LNG) supply; much less is going toward what happens to the LNG once it leaves the liquefaction facility.[1] One acute area of need is additional storage, particularly in Asia, where the primary markets for demand growth do not require the same level of supply all 12 months of the year. When global gas demand drops significantly in the second and third quarters—if production is not cut—the LNG needs to be stored somewhere on an interim or seasonal basis. For now, Europe is fulfilling this role,[2] as most of its Russian gas pipeline exports have disappeared. But with Asian LNG demand growing rapidly, lack of storage capacity on the continent is becoming a commercial weakness for sellers—and a strategic security risk for buyers that promises to worsen, given that demand growth for LNG in Asia will occur in places with the least amount of storage.[3]

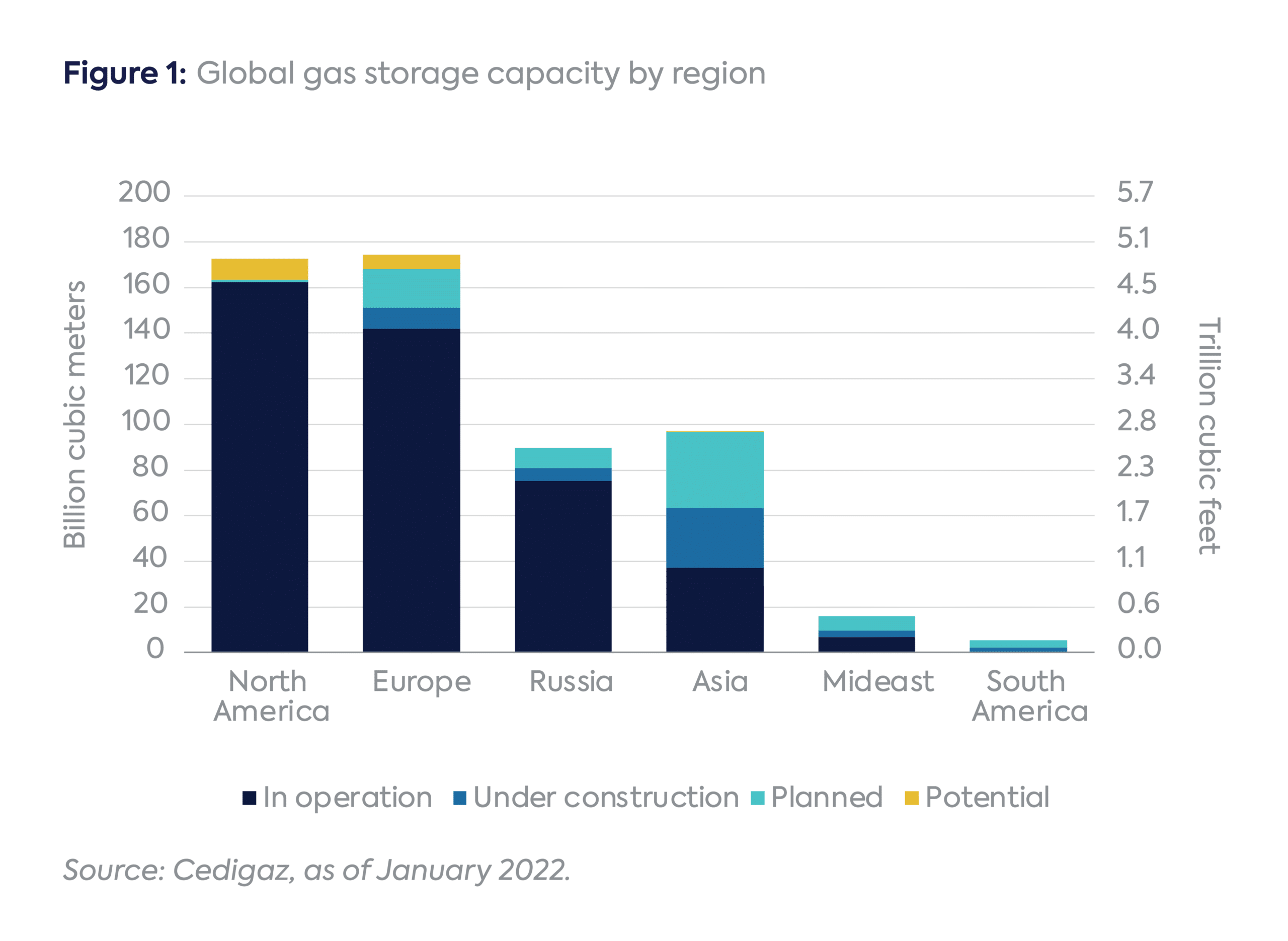

Asia, the largest growth market for natural gas over the next decade, possesses the least amount of gas storage capacity among the major consuming regions (Figure 1).[4] Lack of Asian storage is partly a choice and partly a reflection of geologic reality. Unlike North America or Europe, Asia is not blessed with significant salt cavern storage potential, which provides the most amount of seasonal storage flexibility compared to other storage options, such as a depleted storage field or an aquifer. Overall, Asian gas demand is about the same as North American; however, due to geographical differences, little of the continent is connected by pipeline, so each country must develop a unique and often costly strategy for seasonal gas storage.[5]

China, which accounts for one-third of Asian gas demand, has the most robust and fastest-growing pipeline and storage network in the region.[6] Most of the planned new Asian storage capacity pictured in Figure 1 is in China.

Other than China, most Asian countries have chosen to focus on building import infrastructure to meet peak demand rather than investing in seasonal gas storage and less import capacity. LNG import infrastructure typically comes with operational storage rather than seasonal storage, which means volumes capable of storing only two to four cargoes, or 160 million to 320 million cubic meters (mcm), but multiple times this level is needed for seasonal storage.

Asia’s need for storage is not new, but its increasing reliance on LNG to meet this gas demand now requires more seasonal flexibility in terms of when it is delivered.[7] The amount of additional storage needed to satisfy growth in overall supply and seasonal demand is not a straightforward equation. Growth among power generation, industrial, and residential/commercial (R/C) use can vary depending on location and climate. For example, Europe’s high proportion of R/C demand[8] makes storage more critical there than in a country like India, where baseload gas use varies more by economic use case and price rather than season.

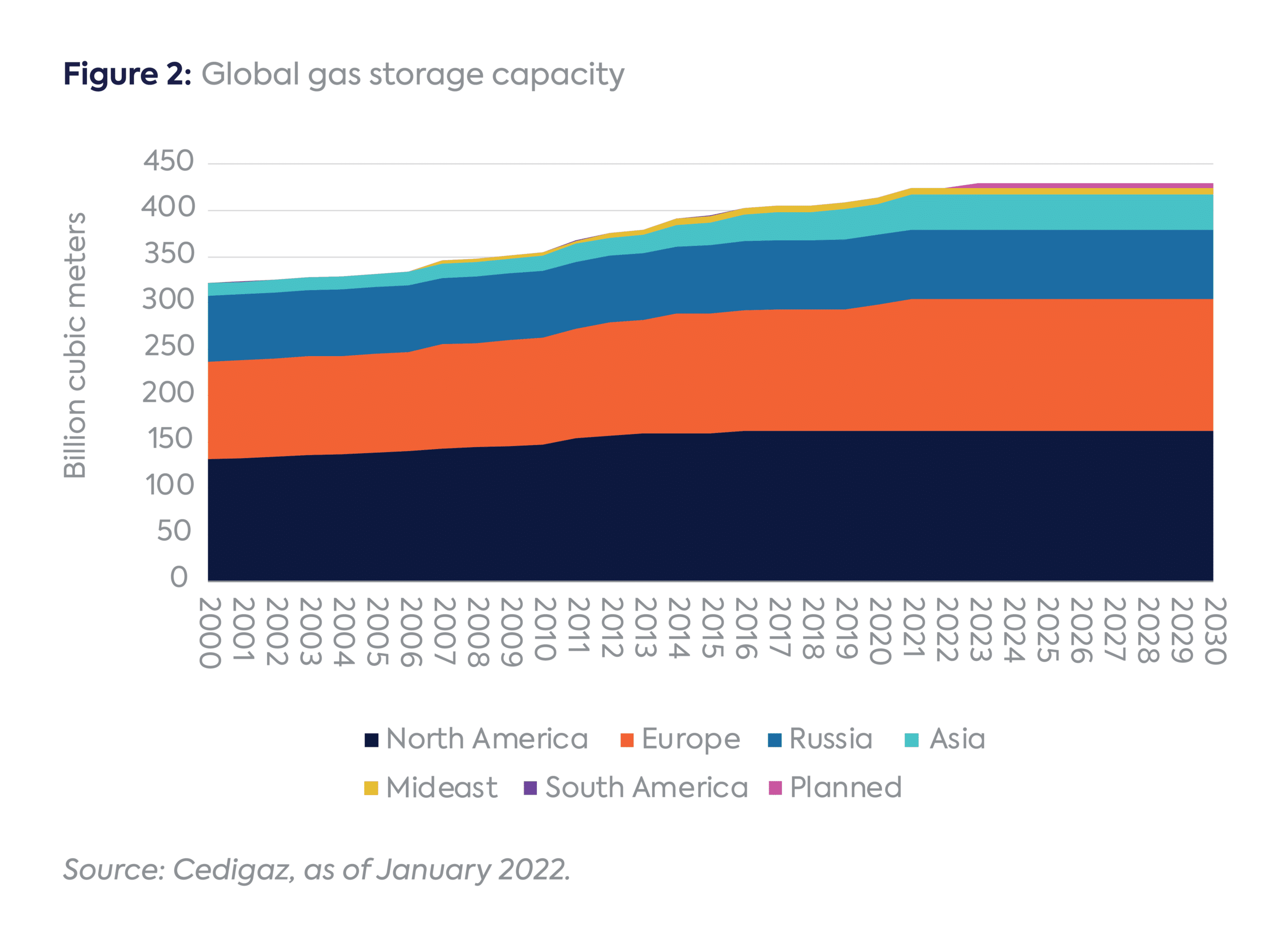

Asian gas demand will grow even if a corresponding increase in Asian storage does not (Figure 3). Even if all 43 million metric tons per annum (MTPA) of storage under construction or planned is built—and that’s mostly in China—it will be dwarfed by the expected 100 to 125 MTPA of additional LNG capacity by 2030.[9] Therefore, Asia will need to rely increasingly on gas storage in Europe and possibly North America or Russia. Europe is by far the most important, as its ample storage capacity will allow for the shutting in of LNG production to be minimized. In the US and Russia, LNG cargo cancellations and higher domestic flows into storage are more likely. Other solutions may be LNG storage on the water, although this option does not provide a seasonal solution due to operating costs of LNG boil-off[10] and daily freight issues.

Looking ahead, the more gas that Europe stores in the summer, the less it will need to import in the winter—which will incentivize more LNG to be redirected in the winter months to the Asian market, where import infrastructure is designed precisely for peak demand periods. From a pricing perspective, higher storage in Europe and higher demand growth in Asia should lead to wider price spreads between the summer and the winter. LNG will push into European markets in the summer and be pulled away in the winter.

Prior to the Ukrainian invasion, Russia provided swing gas supply for the global market by shutting in 300 to 500 mcm/d for up to six months per year in the second and third quarters. That, along with seasonal swing production designed in the Netherlands and the UK, helped Europe limit the need to build up its own storage capacity to current levels by the early 2000s. At that point, in 2005–06, Russia cut off Ukrainian gas flows for the first time, which triggered investments in both new storage capacity and the first major renewables buildout—to limit future exposure to this type of leverage during peak demand season.[11]

As LNG supply grows, Asia’s potential lack of storage will increase the risk of oversupply in Europe, particularly in the third quarter and October, as capacity begins to dry up. Such a risk is already emerging in 2023 even prior to the onslaught of vast amounts of LNG expected to enter the market in the second half of the decade. A return of additional Russian gas, even in small volumes, would enhance the weakness in summer spot prices relative to the winter by pushing European storage to fill up even sooner.

Asia and LNG suppliers can dodge this issue of seasonal storage by pushing the consumption of more LNG to South Asia in the second and third quarters to offset higher seasonal use in Northeast Asia in the fourth and first quarters. Price would be the easiest and perhaps the least expensive way to do so, offering discounts to spur greater usage in power generation. Sharing long-term contracts between seasonal buyers would be another solution, as would be securing additional storage in Europe during the summer months. If Asia wanted to store the gas regionally to enhance security of supply, an additional 35 to 50 bcm of capacity would need to be built.[12] China is putting itself in a position to meet its needs, but the rest of the region remains more vulnerable and cannot assume access to this gas.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] https://www.iea.org/data-and-statistics/charts/change-in-global-investment-in-natural-gas-supply-2019-2023

[2] https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/

[3] https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/

[4] https://www.gie.eu/transparency/databases/storage-database/

[5] https://www.energyinst.org/statistical-review

[6] https://www.gie.eu/transparency/databases/storage-database/

[7] https://www.energypolicy.columbia.edu/sources-of-flexibility-in-global-gas-markets/

[8] https://www.acer.europa.eu/gas-factsheet

[9] https://www.shell.com/energy-and-innovation/natural-gas/liquefied-natural-gas-lng/lng-outlook-2023.html#iframe=L3dlYmFwcHMvTE5HX291dGxvb2tfMjAyMy8

[10] LNG that evaporates during the process of LNG unloading and storage is called boil-off gas.

[11] https://www.reuters.com/article/us-russia-ukraine-gas-timeline-sb/timeline-gas-crises-between-russia-and-ukraine-idUSTRE50A1A720090111

[12] Author’s estimates based on historical storage usage relative to seasonal gas demand patterns in North America and Europe, as it relates to future seasonal gas demand growth in Asia. Also builds in minimum storage levels mandated by the assumed need for security of supply.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

Almost 90 percent of the LNG that transited the Strait of Hormuz in 2025 was destined for Asian countries.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Iran appears to be a natural gas giant, due to its large proved gas reserves and significant gas production and consumption.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia