Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Iran crisis, whenever it ends, will materially change how the LNG market operates.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

A potential short-term oversupply in global gas markets as we head into the low-demand season of summer,[1] combined with a heightened risk of Russia further weaponizing gas supplies, are reminders of the importance of gas flexibility sources in managing market dynamics and price volatility while ensuring the security of supply. This article unpacks three key sources of flexibility underpinning global gas trade that are critical to meeting unexpected demand and/or supply gaps: traditional natural gas storage systems, spare production and supply infrastructure capacity, and liquified natural gas (LNG) contract flexibility. It argues that with its vast storage capacity and flexible LNG supplies, North America will increasingly take on the role of a residual balancer in the global gas market.

Gas supply is affected by geopolitical and technical factors as well as those influencing demand, especially temperature and economic activity. This makes natural gas storage an indispensable part of the global gas trade value chain. In “normal” market conditions, gas storage places unused gas in locations to be used at a future date, in most cases avoiding more costly gas production swings and providing a risk buffer against peak demand periods. This peak typically occurs in the fourth and first quarters of the year. And at times of low demand, storage acts as a “demand sink,” which is especially valuable if all other tools for soaking up supplies are exhausted. For example, during the first Covid-19 lockdowns in Europe and other regional gas markets, gas storage helped minimize production shut-ins and avoid potential near-zero or negative wholesale gas prices.[2] In “exceptional” market conditions, gas storage also backs up any disruptions along the supply chain, like a sudden loss of production facilities due to extreme weather conditions or a disruption in the gas supply chain (pipelines and LNG shipping) due to geopolitical reasons.

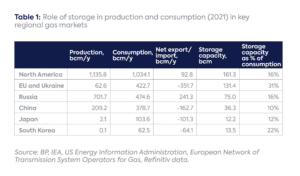

Existing storage facilities play a significant role in supporting fluctuations in demand and interregional gas trade. Of the 444 billion cubic meters (bcm) of global storage capacity, as much as 396 bcm is accounted for by underground storage facilities (in gaseous form); the remaining 48 bcm is in the form of overground LNG storage tanks located at LNG import terminals. This total storage capacity represented roughly 88 percent of global interregional pipeline trade and 86 percent of global LNG trade in 2021. This is equivalent to more than 90 percent of consumption in China and Japan, the entire gas consumption of Russia, or half of the United States’ gas consumption.

Storage capacity—influenced by geological endowment—and LNG trade bind regionally diverse markets. Thirty-six percent of global storage capacity is located in North America (Table 1) and 30 percent in the European Union (EU) and Ukraine. Storage capacity in Japan, Korea, Taiwan, China, and India, the world’s largest LNG importers, accounts for only 15 percent of the global total. These countries must rely primarily on LNG storage tanks at import terminals, and increasingly on “just in time” supply from LNG, to manage potential imbalances.

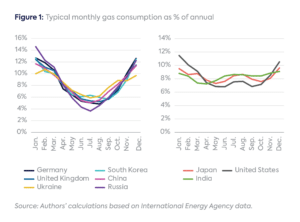

With LNG use increasing this decade, the role of storage will become more significant as most of the growth in demand will come from Asia, where relatively little seasonal storage capacity exists despite strong seasonal swings in gas use (Figure 1). Europe needs to import less LNG in the winter, which allows Asian markets to buy more in lieu of a lack of storage capacity in the region. In this regard, Eurasian and North American storage systems with huge LNG import and export capacities add trading liquidity to LNG regional markets.

Many countries have a clear summer-winter difference due to changes in temperature and household requirements for gas for heating purposes (Figure 1, left panel); in markets like Japan and the US, we see similar patterns but also summer peaks due to high energy consumption for cooling purposes. There are also countries with little variation in demand—India is in this category (Figure 1, right panel).

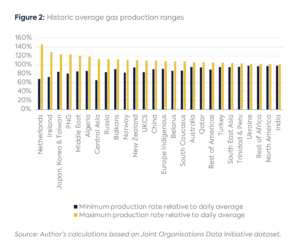

These could act as a supply solution to increase flexibility and security, and deliver the “just in time” supply. The United Kingdom, for example, has almost zero storage capacity and has historically relied on the flexibility of its North Sea production, its connectivity with Europe via massive pipelines, and LNG imports.[3] The country has been relying on interconnections and domestic UK Continental Shelf (UKCS) swing producers to meet seasonal variations in demand (Figure 2). Another example of a swing producer in Europe is the Netherlands, but with the closure of Groningen, the largest gas field in the EU, its production flexibility will soon cease—exacerbating market volatility and leading to sharper price spikes.[4]

While infrastructure capacity—production and pipelines—can provide flexibility, ensuring gas is delivered when most needed, LNG contract flexibility and LNG portfolio supply are emerging as a new form of “storage” in the context of energy security for LNG importers.[5] This new “just in time” solution could provide extra security for countries with insufficient storage capacity, such as Japan. For example, many US LNG projects are free-on-board (FOB) based contracts[6] that are flexible for buyers to divert to the market of their choice for a price linked to Henry Hub. This provides access to the US, the most liquid gas market in the world.

There is limited production flexibility from leading LNG exporters—North America, Qatar, and Australia (Figure 2). Russia has storage capacity and upstream production flexibility, but due to the ongoing war in Ukraine, its role as a flexibility provider to the global gas market will likely be limited. With Europe decoupling from the Russian gas pipeline supply and mandatory storage refill obligation, its role in providing flexibility and balance to the global gas market may also become limited. The disappearance of seasonal flexibility in Europe[7] may imply greater gas price volatilities, a critical issue for European and Asian importers, especially those relying on spot LNG purchases.

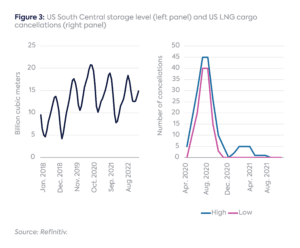

Amid the Covid-19 pandemic, 175[8] LNG cargoes from the US were canceled (Figure 3, right panel) because of low global energy demand. Some of the natural gas supply from the US ended up in the US South Central storage system[9] (Figure 3, left panel), and when Europe needed natural gas to replace the missing volumes from Russia following the war in Ukraine, US LNG met most of the incremental LNG demand.[10]

With its armada of LNG export capacity—of the more than 190 bcm expected to be added globally by 2027, at least 87 bcm will come from the US[11]—and its huge storage capacity, the US will take center stage in offering flexibility and security of supply to the global gas market at prices linked to the most liquid wholesale gas market in the world.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/

[2] For example, at the peak of the 2020 gas glut, about 10 bcm of gas was stored in Ukraine by foreign traders. See https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/.

[3] https://www.theguardian.com/business/2021/sep/24/how-uk-energy-policies-have-left-britain-exposed-to-winter-gas-price-hikes

[4] https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/en/specialreports/naturalgas/groningen-european-gas-report.pdf

[5] https://www.energypolicy.columbia.edu/publications/beyond-spot-vs-long-term-europes-lng-contracting-options-for-an-uncertain-future/; https://www.iea.org/news/market-flexibility-is-improving-thanks-to-lng-and-markets-currently-well-supplied-but-gas-security-remains-a-concern

[6] FOB is used to denote deliveries where the buyer is responsible for arranging the shipping and there is a title exchange at the loading port.

[7] Unless Europe makes use of Ukraine’s underutilized storage capacity, as suggested by Losz and Joseph: https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/

[8] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/013122-us-approaches-a-year-without-any-lng-cargo-cancellations-amid-strong-demand

[9] The region where most of the US LNG export facilities are located.

[10] https://www.eia.gov/todayinenergy/detail.php?id=55920#

[11] Based on the Refinitiv LNG infrastructure database (only projects that took final investment decision and are under constructions were considered).

The Iran crisis, whenever it ends, will materially change how the LNG market operates.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

The US-Israeli war against Iran highlights the Gulf’s dual role as the backbone of global energy supply and a major source of systemic risk.

Almost 90 percent of the LNG that transited the Strait of Hormuz in 2025 was destined for Asian countries.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia