Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

India issued its first pair of sovereign green bonds in January, joining a growing list of countries to issue sovereign thematic bonds.[1] India has set ambitious decarbonization goals, including increasing nonfossil electricity capacity to 500 GW[2] and producing 5 million tons of green hydrogen by 2030.[3] The bond sale was followed by the release of the 2023–24 Annual Union Budget of India, which detailed budgetary allocations for several green initiatives using green bonds to finance infrastructure to decarbonize electricity generation, carbon-intensive industries, and railways.[4] This experience of issuing bonds for large-scale green projects holds lessons for India’s future decarbonization financing strategies and other emerging market and developing economies (EMDE) considering similar measures.

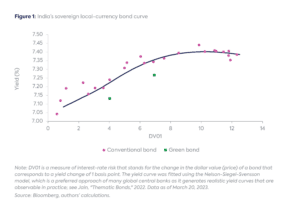

The debut green bonds were a success as they were issued with a premium and, just as importantly, in the local currency. The Ministry of Finance raised $1 billion between the two bonds, which increased to $2 billion following a second sale in February, and sold the bonds with an estimated premium of 5–6 basis points each.[5] The average premium for the two bonds in the secondary market is at 9 basis points as of March 20, 2023 (Figure 1), which is in line with the average premium observed across emerging market sovereign and quasi-sovereign green bonds.[6] The country thus managed to capture more than half of the premium in the primary market sale.

The denomination of the bonds in the Indian rupee is important because local currency issuance by EMDE makes up a minuscule of the green bond market (estimated at less than 3 percent of the global total).[7] Issuing in a local currency minimizes asset-liability currency mismatches, or countries holding liabilities in a foreign currency while generating investments and revenues in the local currency. Moreover, bonds issued in local currencies can help foster the growth of the domestic sustainability-focused fixed-income asset management industry, which can then support further issuances by the sovereign and other domestic corporations.

India’s sovereign green bond issuance was the culmination of a process that resulted in the release of a green bond framework in November 2022.[8] Establishing such a framework is key to ensuring transparency and integrity in a country’s green bond market.[9]

The framework is not legally binding, but it encourages investor confidence and reduces the risk of greenwashing. However, most countries see that creating such a framework adds time, money, and effort to issuing green bonds, leading to the temptation of simply selling conventional bonds, thereby missing out on important sources of green financing. The effort involved in creating a proper framework at the outset can be substantial, but later issuances can move more swiftly if they benefit from the properly laid groundwork. Green bond frameworks can support further issuance by assuring investors about transparent faithfulness to the International Capital Markets Association’s Green Bond Principles (GBP).[10]

India’s framework has notable features worth highlighting in each of the four core components of GBP:

To make the green bonds more easily accessible to international investors, the Reserve Bank of India made them exempt from the investment cap that applies to foreign participation.[13] Nevertheless, the buyers were predominantly domestic investors.[14]

For the green bond market to become a viable source of funding for India’s green ambitions, ESG-focused international investors will need to augment local investors. One approach for attracting external investors could be to lower or possibly eliminate withholding taxes on green bonds; in July, those tax rates for foreign investors are due to jump back to 20 percent from the current rate of 5 percent.[15] Lowering the tax rate on the coupon of green bonds has been shown to increase demand meaningfully.[16] An example in the domestic context is the tax-free bond issued by the Indian Renewable Energy Development Agency Limited in 2016, which was oversubscribed by more than five times.[17] A similar tactic could help attract foreign investors as well. The loss of tax revenue could potentially be made up indirectly by the perceived improvement in creditworthiness as a result of long-term investment in environmental sustainability.[18]

A second approach could be to address the issues that have bogged down the addition of Indian bonds into global debt indexes,[19] such as by making the bonds easy to settle and clear through international clearinghouses like Euroclear, providing clarity on taxation, and removing investment caps on foreign investors. Inclusion in bond indexes commonly used as benchmarks would likely attract international private capital.

The issuance of India’s first sovereign green bonds is the beginning of what could be an important pillar of the country’s strategy for financing its decarbonization objectives. Various estimates put the investment required for India to achieve its clean energy targets at $160-200 billion per annum.[20] The $2 billion of the inaugural sovereign green bond is a small step in addressing this need, and as it corresponds to only around 1 percent of the government’s gross borrowing for the current fiscal year, there is ample room to increase the use of this strategy.[21]

Moreover, sovereign green bonds provide a local currency benchmark for domestic companies and agencies, and India’s national framework provides a template to follow for those entities. As a next step, developing a detailed green taxonomy could further support the decarbonization effort by helping companies and investors identify projects that meet sustainability criteria.[22]

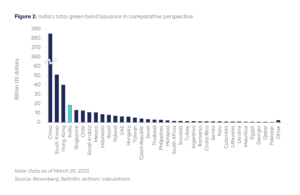

With a total of $19 billion of green bonds issued by March 20, 2023—only 13 percent of which were denominated in the rupee before the recent sovereign issuance—India currently stands fourth among EMDE and developed Asian countries (Figure 2). The sovereign issuance could help India catch up with some of its peer nations, especially if it increases the share of green bonds denominated in the local currency.

India’s detailed green bonds framework and effort toward transparency and efficiency bode well for the growth of this key source of financing for the country’s green growth strategy. With the issuance of India’s first municipal green bond last month, the national approach may already be inspiring subnational initiatives.[23] Indeed, India’s experience issuing green bonds may inform other emerging economies eager to finance climate-compliant infrastructure development.

The authors thank Mel Peh for her research assistance on this article.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffiel

[1] Reserve Bank of India, “Underwriting Auction for Sale of Government of India Sovereign Green Bonds for ₹8,000 Crore on January 25, 2023,” press release, January 24, 2023, https://www.rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=55100#.

[2] Kaushik Deb and Pranati Chestha Kohli, “Assessing India’s Ambitious Climate Commitments,” Center on Global Energy Policy, Columbia University, December 8, 2022, https://www.energypolicy.columbia.edu/publications/assessing-india-s-ambitious-climate-commitments/.

[3] Kaushik Deb, Pranati Chestha Kohli, and Dakshesh Pranav Thacker, “Unpacking India’s Green Growth Budget,” Center on Global Energy Policy, Columbia University, February 27, 2023, https://www.energypolicy.columbia.edu/unpacking-indias-green-growth-budget/.

[4] Ibid; Ministry of Environment, Forests, and Climate Change, “Notes on Demands for Grants, 2023–2024: Demand No. 28,” https://www.indiabudget.gov.in/doc/eb/sbe28.pdf; Ministry of New and Renewable Energy, “Notes on Demands for Grants, 2023–2024: Demand No. 71,” https://www.indiabudget.gov.in/doc/eb/sbe71.pdf; Ministry of Railways, “Notes on Demands for Grants, 2023–2024: Demand No. 85,” https://www.indiabudget.gov.in/doc/eb/sbe85.pdf.

[5] Dharamraj Lalit Dhutia, “India’s First Green Bond Issue Pulls Local Bidders, Foreigners Aloof—Traders,” Reuters, January 26, 2023, https://www.reuters.com/world/india/india-sells-first-green-bonds-5-6-basis-points-below-sovereign-yields-2023-01-25/.

[6] Gautam Jain, “Thematic Bonds: Financing Net-Zero Transition in Emerging Market and Developing Economies,” Center on Global Energy Policy, Columbia University, December 12, 2022, https://www.energypolicy.columbia.edu/publications/thematic-bonds-financing-net-zero-transition-emerging-market-and-developing-economies/.

[7] Ibid.

[8] Government of India, “Framework for Sovereign Green Bonds,” Department of Economic Affairs, November 9, 2022, https://dea.gov.in/sites/default/files/Framework%20for%20Sovereign%20Green%20Bonds.pdf.

[9] Jain, “Thematic Bonds: Financing Net-Zero Transition.”

[10] International Capital Market Association, “Green Bond Principles,” June 2022, https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/green-bond-principles-gbp/.

[11] Republic of Colombia, “Colombia Sovereign Green Bond Framework,” Ministry of Finance and Public Credit, August 5, 2021, https://www.irc.gov.co/webcenter/ShowProperty?nodeId=%2FConexionContent%2FWCC_CLUSTER-170719.

[12] Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, Government of India, “National Infrastructure Pipeline,” accessed March 19, 2023, https://indiainvestmentgrid.gov.in/national-infrastructure-pipeline.

[13] Neha Kumar, “Announced in Budget 2022, Debut Green Bond Performs Better Than Expected,” Observer Research Foundation, January 30, 2023, https://www.orfonline.org/expert-speak/announced-in-budget-2022/.

[14] Dhutia, “India’s First Green Bond Issue Pulls Local Bidders.”

[15] Nikunj Ohri and Shivangi Acharya, “Foreign Portfolio Investors in India to Pay Higher Tax on Debt Securities,” Reuters, February 4, 2023, https://www.reuters.com/world/india/foreign-portfolio-investors-india-pay-higher-tax-debt-securities-official-2023-02-04/.

[16] Elettra Agliardi and Rossella Agliardi, “Financing Environmentally-Sustainable Projects with Green Bonds,” Environment and Development Economics 24, no. 6 (December 2019): 608–623, https://www.cambridge.org/core/journals/environment-and-development-economics/article/abs/financing-environmentallysustainable-projects-with-green-bonds/AF17C83137370EC47C500414468EDEC6.

[17] Chittorgarh, “IREDA Ltd NCD (IREDA NCD Jan 2016) Detail,” January 2016, https://www.chittorgarh.com/bond/ireda_ltd_ncd_jan_2016/82/.

[18] Jain, “Thematic Bonds: Financing Net-Zero Transition.”

[19] Jonathan Wheatley and Hudson Lockett, “JPMorgan Declines to Add India to Widely Followed Bond Index,” Financial Times, October 4, 2022, https://www.ft.com/content/fe962737-971d-4f75-8d43-0e35d026d0af.

[20] International Energy Agency, “India Energy Outlook 2021,” February 2021, https://www.iea.org/reports/india-energy-outlook-2021; Vaibhav Pratap Singh and Gagan Sidhu, “Investment Sizing India’s 2070 Net-Zero Target,” Council on Energy, Environment and Water, November 2021, https://www.ceew.in/cef/solutions-factory/publications/CEEW-CEF-Investment-Sizing-India’s-2070-Net-Zero-Target.pdf.

[21] Radhika Pandey, “How Green Bonds Can Take India Closer to Meeting Its Climate Goals and Deepen Investor Interest,” The Print, January 27, 2023, https://theprint.in/macrosutra/how-green-bonds-can-take-india-closer-to-meeting-its-climate-goals-and-deepen-investor-interest/1336721/.

[22] Jingwei Jia, “India’s Sovereign Green Bonds May Bolster Financing Capacity,” Sustainable Fitch, February 9, 2023, https://cdn.roxhillmedia.com/production/email/attachment/1100001_1110000/486b06702a1e838e5df0175f3b6cc9c5ec2751cb.pdf.

[23] S Dinakar, “Indore’s First Municipal Green Bond a Beacon for India’s Urban Local Bodies,” Business Standard, March 5, 2023, https://www.business-standard.com/article/economy-policy/indore-s-first-municipal-green-bond-a-beacon-for-india-s-urban-local-bodies-123030500436_1.html.

The World Bank is revisiting one of its most entrenched positions, publicly questioning its long-standing emphasis on market-led approaches in economic policy.

The Trump administration is increasingly using equity investments as a tool of industrial policy to support domestic critical minerals supply chains.

CGEP scholars reflect on some of the standout issues of the day during this year's Climate Week

The Trump administration may release a blueprint for a US sovereign wealth fund (SWF) in early May after the president signed an executive order in February giving the Secretary of the Treasury and the Secretary of Commerce 90 days to develop a plan.

Project-based carbon credit markets (PCCMs) facilitate the generation, trading, and retirement of carbon credits from projects that remove, reduce, or avoid greenhouse gas emissions.