In the waters off Malaysia, Iranian oil sales continue despite blockade

A large anchorage area off the coast of Malaysia is a major marketplace for sanctioned oil.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the demand for power surges across the US, the debate over how to build energy infrastructure has reached a fever pitch. And while both sides of the...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

On December 31, 2019, Gazprom, Gas Transmission System Operator of Ukraine (GTSOU), and Naftogaz signed agreements to continue Russian gas transit through Ukraine for a five-year period ending in 2024.[1] The agreement was reached at the last minute and narrowly averted a repetition of the 2009 gas crisis.[2] It was supported by political negotiations between Russian, Ukrainian, and European leaders, putting an end to years-long arbitration cases between Russian and Ukrainian gas companies. In particular, Gazprom committed to pay $2.9 billion to Naftogaz following an arbitration decision, while all other arbitration lawsuits were dropped by Naftogaz.

Against all odds, Russian pipeline gas is still flowing through Ukraine—mainly to Austria, Slovakia, Italy, and Hungary. But for how long? While a 10-year extension beyond 2024 was included in the 2019 agreement,[3] the possibility of prolonging the transit agreement was unclear[4]—even before the Russia-Ukraine war—and now it has become more uncertain. This article discusses the potential fate of the contract and the implications for various stakeholders—the European Union (EU) countries, Russia, and Ukraine.

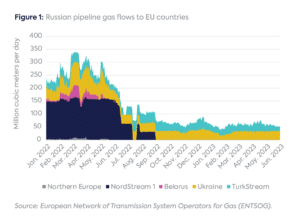

Against the total annualized Russian gas pipeline supplies to the EU of 22 billion cubic meters per year (bcm/y), current transit volumes through Ukraine are close to 12–13 bcm/y (Figure 1). The ship-or-pay transit contract foresaw a transit of 65 bcm in 2020, and then 40 bcm/y over 2021–24. Transit volumes amounted to 55.8 bcm in 2020 and 41.6 bcm in 2021, but dropped to around 19 bcm in 2022. While contracted transit volumes were initially paid by Gazprom regardless of actual transit, in September 2022 Naftogaz and GTSOU launched an arbitration against Gazprom for not paying for the full contracted volumes.[5]

In all likelihood, the contract will end on December 31, 2024, without renewal. A worsening of the current situation before that date is always possible, including physical deterioration of pipeline infrastructure. Previous contract negotiations included in-person political engagement at the highest levels from Russia, Ukraine, the European Commission (EC), Germany, and France, parties unlikely to conduct constructive negotiations now. The EC has pledged to stop Russian gas imports by 2027. EU countries are currently holding discussions on reducing Russian LNG imports.[6] Moving further toward that goal and cutting Ukrainian transit would leave only the TurkStream entry point at Strandzha, able to deliver up to 15.75 bcm/y to Europe. TurkStream volumes are currently closer to 10 bcm/y.[7] If Ukrainian transit stops, Gazprom pipeline gas deliveries to EU countries could drop to between 10 and 16 bcm/y (45 to 73 percent of current levels).[8]

Additionally, 2025 marks the start of the expected end of global gas tightness, with substantial new LNG supplies from Qatar and the United States coming on stream. European leaders may try to further reduce Russian pipeline gas supplies as soon as early 2025. For example, Italy[9] and Slovakia[10] are on a fast track toward reducing their Russian pipeline gas dependency. The timeliness of these LNG volumes and the temperatures in winter 2024–25 will affect the EU gas balance, notably in early 2025. Meanwhile, Germany has moved away from Russian gas to LNG, with three existing LNG terminals and another three expected to start within one year.

Ukraine does not import any Russian gas and hasn’t issued any official statements so far regarding plans to extend the transit agreement. Ending the transit agreement beyond 2024 means Ukraine would lose transit revenues once expected to yield $7.15 billion over 2020–24.[11] There is a discussion about preparing the gas transportation system (GTS) to work well, technically and financially, without the transit Russian gas flows,[12] but there are no signs of a political agreement to reject further contractual relationships with Gazprom.

GTSOU has already developed plans to adapt the transmission network’s operations to the loss of transit volumes.[13] They include a part of GTS commissioning, reconstruction of 10 priority compressor stations, and reorganizing the GTS flows to serve Europe and needs of domestic gas consumers. GTSOU is rather keen for Europeans to continue using Ukrainian gas transport and storage facilities to improve EU’s security;[14] in the long term, the country plans to become a supplier of biomethane and hydrogen.[15] Another important aspect of the GTS utilization under discussion is reconstruction of spare GTS compressor units into gas-fired electricity peaking power plants for daily balancing of the war-damaged power system[16] and better integration of renewables into the grid.

Meanwhile, Gazprom was not enthusiastic about contract extension even in 2019,[17] as it was counting on replacing Ukrainian transit by NordStream 2 once it had reached capacity. It is important to note, though, that following the sabotage of NordStream 1 and 2 in September 2022[18] this option no longer exists.

Transit could continue under a more flexible arrangement, with no firm take-or-pay or capacity booking, if Gazprom replicates the model being used with Yamal Europe and books transit capacity on a short-term basis (month-ahead or even day-ahead). Yet another possibility is to conclude agreements with European companies so that they receive gas at Ukraine’s eastern border and arrange for transportation services with Ukraine on a bilateral basis. Such a design was also discussed during the negotiations in 2019, but European players were not willing to take all the risks associated with this scheme. It is questionable whether there would be any takers now, in the middle of full-scale military actions.

In both cases, assuming the war situation perdures, the transit could likely be limited to the only entry point currently functioning (Sudzha), as GTSOU declared force majeure on the other entry point (Sokhranivka) in Eastern Ukraine in May 2022. Volumes transiting through Ukraine would likely remain below current levels, accounting for countries stopping Russian gas imports sooner than 2025, before progressively dwindling—mostly to supply landlocked European countries until they end their Russian gas dependency.

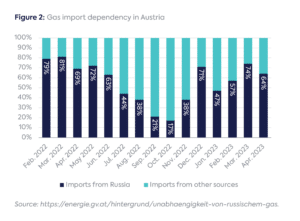

Despite previous skepticism, maintaining flows got recent support from the Russian side, with deputy foreign minister Mikhail Galuzin insisting on this proposal, perhaps hoping to prolong the EU’s dependency on Russia.[19] Maintaining some Ukrainian transit may be also supported by a few European countries, notably Austria, which lacks a clearly defined short-term plan to reduce Russian gas imports, according to the EC.[20] Russian gas accounted for 47–74 percent of Austria’s monthly imports in early 2023 (Figure 2). Another country at risk is Moldova, which extended its long-term contract with Gazprom in late 2021 for five years. While Moldova is likely to continue to reduce its dependency on Russian gas in favor of EU supplies via Romania or Western Ukraine, it is uncertain whether it can be ready by early 2025.[21]

Even if some flows continue beyond the end of 2024, it seems unlikely at this stage that the current transit agreement would be extended under similar conditions, given the lack of political support. Direct negotiations between Ukraine and Russia on the extension of the transit contract look highly implausible in the current environment. Reaching a new transit deal would require a totally different geopolitical environment.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] Naftogaz, “Naftogaz, GTSOU and Gazprom Signed a Set of Agreements to Ensure Russian Gas Transit over the Next Five Years,” December 31, 2019, https://www.naftogaz.com/en/news/naftogaz-gtsou-and-gazprom-signed-a-set-of-agreements-to-ensure-russian-gas-transit-over-the-next-five-years.

[2] Reuters, “Russia, Ukraine clinch final gas deal on gas transit to Europe,” December 30, 2019, https://www.reuters.com/article/us-ukraine-russia-gas-deal-idUSKBN1YY1FY.

[3] ICIS, “Ukraine GTSOU prepares for Gazprom transit arbitration – CEO,” September 8, 2022, https://www.icis.com/explore/resources/news/2022/09/08/10803638/ukraine-gtsou-prepares-for-gazprom-transit-arbitration-ceo/.

[4] Starting from 2015 and further on, Gazprom was skeptical regarding renewal of the transit contract as it was planning to redirect pipeline supplies via bypassing streams. Forbes, “Gazprom Refused to Extend the Contract for gas Transit through Ukraine,” June 9, 2015, https://www.forbes.ru/news/290895-gazprom-ne-prodlit-kontrakt-na-tranzit-gaza-ni-pri-kakikh-obstoyatelstvakh; A. Vozdvizhenskaya, “Gazprom ruled out the extension of the contract for transit through Ukraine,” RG.RU, April 24, 2018, https://rg-ru.translate.goog/2018/04/24/gazprom-iskliuchil-prodlenie-kontrakta-na-tranzit-cherez-ukrainu.html?_x_tr_sl=ru&_x_tr_tl=en&_x_tr_hl=en&_x_tr_pto=sc&_x_tr_hist=true.

[5] ICIS, “Ukraine GTSOU prepares for Gazprom transit arbitration – CEO,” September 8, 2022, https://www.icis.com/explore/resources/news/2022/09/08/10803638/ukraine-gtsou-prepares-for-gazprom-transit-arbitration-ceo/.

[6] High North News, “EU Begins Consultations to Curb Inflow of Russian LNG,” June 5, 2023, https://www.highnorthnews.com/en/eu-begins-consultations-curb-inflow-russian-lng.

[7] Based on ENTSOG’s flow data over January–May 2023.

[8] Based on TurkStream’s current levels in 2023 and TurkStream’s maximum capacity towards EU countries.

[9] Euractiv, “Italy Free from Russian Gas by Year’s End Says Minister,” March 21, 2023, https://www.euractiv.com/section/politics/news/italy-free-from-russian-gas-by-years-end-says-minister/.

[10] Euractiv, “Slovakia Will Survive Winter Even without Russian Gas, Says Economy Minister,” April 5, 2023, https://www.euractiv.com/section/politics/news/slovakia-will-survive-winter-even-without-russian-gas-says-economy-minister/.

[11] Naftogaz, “Annual Report 2021,” 2022, https://www.naftogaz.com/short/0ac0b2d1.

[12] S. Kroka, “End of Transit. How Ukraine’s Gas Transportation System Will Work Without Russian Gas,” January 17, 2023, https://delo.ua/ru/energetics/konec-tranzita-kak-budet-rabotat-gazotransportnaya-sistema-ukrainy-bez-rossiiskogo-gaza-409662/.

[13] “The Gas Transmission System of Ukraine Will Operate in Reverse Mode if Gas Transit from Russia Stops,” Ukrainian Business News, September 1, 2022, https://ubn.news/the-gas-transmission-system-of-ukraine-will-operate-in-reverse-mode-if-gas-transit-from-russia-stops/.

[14] Akos Losz and Ira Joseph, “Ukraine’s Underused Gas Storage Capacity,” Center on Global Energy Policy, May 30, 2023, https://www.energypolicy.columbia.edu/ukraines-underused-gas-storage-capacity/.

[15] GTSOU, “New Gas Transport Opportunities Are Among GTSOU Priorities, – Dmytro Lyppa,” May 9, 2023, https://tsoua.com/en/news/new-gas-transport-opportunities-are-among-gtsou-priorities-dmytro-lyppa/.

[16] “Russian Missile Attacks Could Lead To Three Blackout scenarios in Ukraine,” ZN.UA, November 24, 2022, https://zn.ua/UKRAINE/rossijskie-raketnye-ataki-mohut-privesti-k-trem-stsenarijam-blekauta-v-ukraine-forbes.html.

[17] Forbes, “Gazprom Refused to Extend the Contract for gas Transit through Ukraine,” June 9, 2015, https://www.forbes.ru/news/290895-gazprom-ne-prodlit-kontrakt-na-tranzit-gaza-ni-pri-kakikh-obstoyatelstvakh.

[18] Technically, one string of Nord Stream is assumed to be operational, but operating it would be politically challenging.

[19] https://tass.com/politics/1626837, https://www.euractiv.com/section/politics/news/austria-has-yet-to-make-a-clear-plan-to-decouple-from-russian-gas-commission-says/.

[20] Energie.gv.at, “Unabhängigkeit von russischem Gas,“ accessed on June 5, 2023, https://energie.gv.at/hintergrund/unabhaengigkeit-von-russischem-gas.

[21] Tatiana Mitrova, “Q&A: Can a Pro-European Moldova Reduce Its Energy Dependence on Russia?,” Center on Global Energy Policy, May 4, 2023, https://www.energypolicy.columbia.edu/qa-can-a-pro-european-moldova-reduce-its-energy-dependence-on-russia/.

The Iran crisis, whenever it ends, will materially change how the LNG market operates.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

Almost 90 percent of the LNG that transited the Strait of Hormuz in 2025 was destined for Asian countries.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

CHRONIQUE. Les Etats-Unis vont bientôt contrôler environ un tiers des capacités mondiales de GNL, bien plus que le Qatar. Sous l’administration Trump, le GNL est devenu un outil de politique étrangère, écrit Anne-Sophie Corbeau, chercheuse au Center on Global Energy Policy de l’Université Columbia

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia