This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

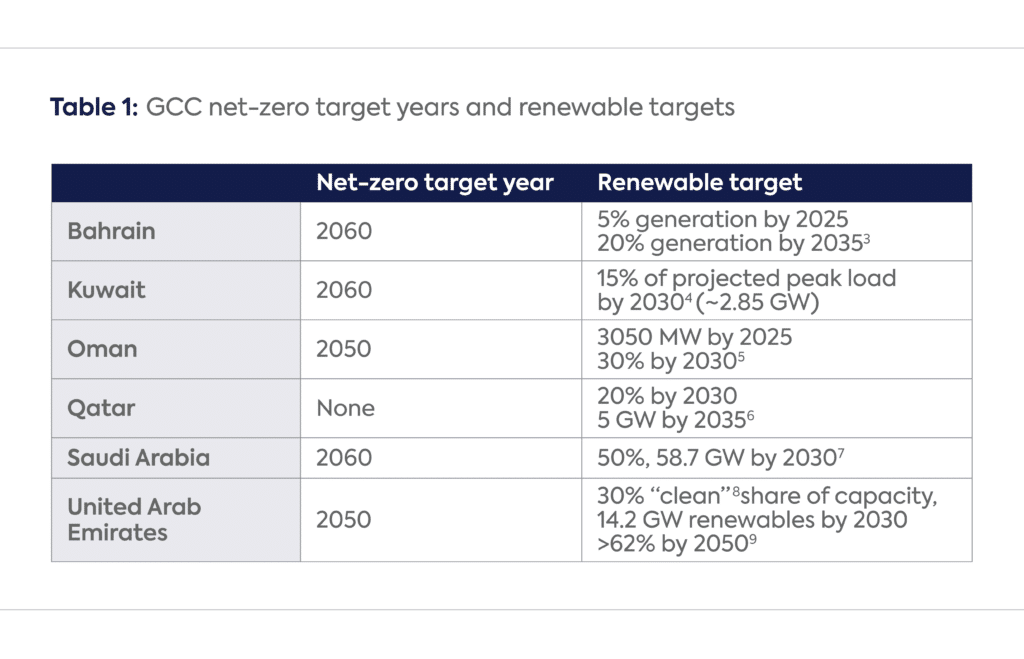

The six Gulf Cooperation Council (GCC) countries hold 2.5% of global electricity generation,[1] are some of the sunniest in the world, have set a string of records for low solar power costs, and yet they have only 0.7% of worldwide solar generation capacity.[2] With five of the six having set net-zero carbon dates, their deployment of renewable energy is a key test of their ambitions and the technology’s attractiveness in areas with abundant, low-cost oil and gas.

Installed renewable capacity in 2022 was about 5.7 gigawatts (GW), primarily solar photovoltaic (PV), out of 165 GW of total generating capacity, mostly gas-fired with some oil-fired capacity in Saudi Arabia and Kuwait. Yet all the GCC countries have ambitious targets to raise this share (Table 1).

Pricing—Not yet Rock Bottom

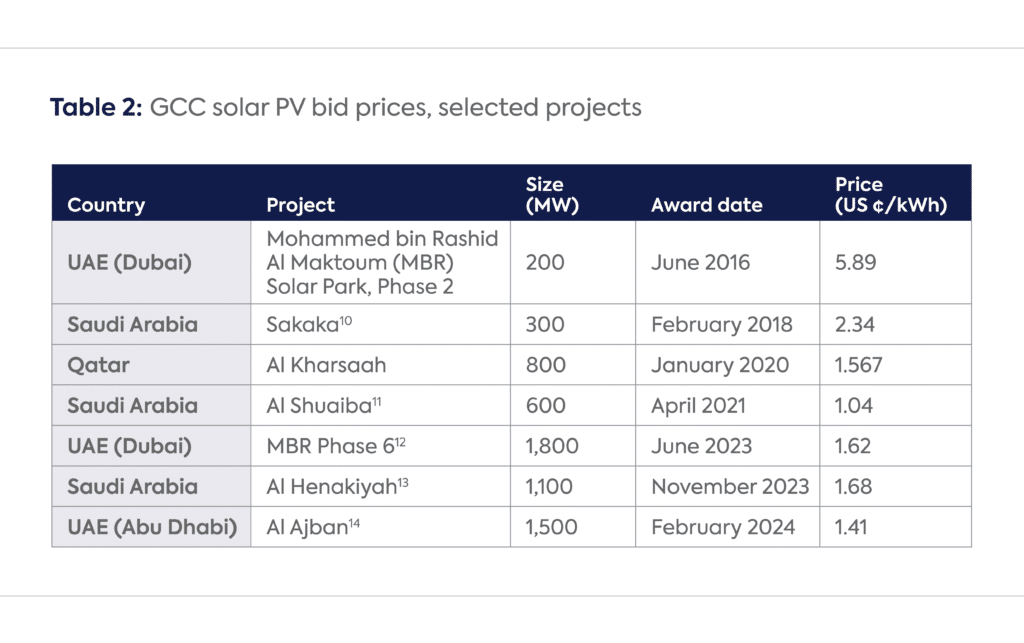

GCC countries have achieved in competitive bids among the lowest prices for solar power anywhere in the world (Table 2).

While these prices are well below the cost of alternative generation from gas or oil, they have been criticized as non-transparent and as not reflecting true costs, or incorporating elements of strategic underbidding. However, analysis suggests the very low costs achieved are mostly explained by the high-quality solar resource, very large scale of the projects, comfort with their low technical and commercial risk levels, a low cost of capital, and ease of permitting and therefore swift and predictable execution.[15] Technology improvements, such as the use of bifacial panels, have contributed secondarily.

This suggests that other countries, especially in North Africa and Latin America, could follow the GCC path to ultra-low utility solar PV costs.

Is a Boom on the Way?

GCC electricity demand is dominated by building use, primarily for summer air-conditioning. The demand on Emirates Water and Electricity Company (EWEC), Abu Dhabi’s main utility, for example, ranged in 2022 from a minimum of 7.4 GW in January to a maximum of 16.4 GW in July.[16] Although solar PV performance falls off somewhat at high ambient temperatures, this is compensated for by longer days.

Overall, matching solar supply with demand should be more tractable than in northern Europe or northern North America. The level of solar PV penetration is still low, existing fleets of mostly gas-fired plants provide flexible generation, and regional utilities are now investing in storage via batteries and engineered pumped hydroelectric plants. A relatively modest amount of battery storage, plus nuclear power in the UAE, should suffice to meet demand through the nighttime. End-user demand response and flexible use of water desalination and hydrogen electrolysis are further options.

More can be done. Distributed (“rooftop”) solar PV is a relative rarity in the region, partly because of low consumer electricity prices. But it is becoming more common, especially in Dubai, where net metering had encouraged the installation of 500 MW by 2022,[17] mostly on industrial and commercial establishments.

Wind power has been less heralded, but parts of Saudi Arabia and Oman also have good resources and projects are under development there as well as in the less windy UAE.

The prevailing model of GCC renewable development is that the local electricity ministry, utility, or state power procurement company solicits competitive bids for utility-scale projects in predefined areas. This results in large increments in capacity, but it means the pace of development is reliant on a steady stream of bids and awards.

The UAE, Saudi Arabia, and Oman now seem to have entered that steady state. Dubai is close to having awarded the entire planned 5 GW capacity of the MBR Solar Park. With EWEC planning 7.3 GW by 2030 and some smaller projects, the national target of 14.2 GW looks achievable. By 2050, the country might need about 100 GW of solar PV for electricity and another 100 GW for green hydrogen production to meet its net-zero and hydrogen export goals. This would still represent only about 2% of its land surface.

Oman should achieve about 3.7 GW of solar and wind by the end of 2027, surpassing its 2025 target but a couple of years late, but it will need additional projects to meet the goal of 30% of generation by 2030.

Qatar has 800 MW of solar PV in the Al Kharsaah plant, and is working on another 800 MW between two projects, so its 5 GW target by 2035 should be feasible. These plants are intended to help lower the carbon footprint of liquefied natural gas export facilities, making them more competitive.

In Kuwait, by contrast, the 1.5 GW Dibdibah component of the Shagaya solar project was canceled in 2020 amid the Covid-19 pandemic, leaving the country with just 114 MW of capacity. But the new minister of electricity, Salem Al Hajraf, is an advocate of renewables, and a tender has been launched for a 1.1 GW solar farm at Shagaya.[18] This would approach halfway to the 2030 goal.

Bahrain is limited by its small land area. It had 57 MW of solar installed in 2023 and is planning its first utility-scale project, the 72 MW Sakhir PV. Even if this is completed, renewable generation in 2025 will be around 0.5% of the total, and so far short of the 5% target, not to mention the 20% target by 2035. Boosting the share of renewables further would likely require some combination of much more distributed “rooftop” PV, floating solar, offshore wind, and possibly investment in plants in neighboring Saudi Arabia dedicated to supply Bahrain.

Saudi Arabia is the big question, given the huge scale of its ambition. The King Abdullah Center for Atomic and Renewable Energy in 2013 proposed 54 GW of renewables by 2032, including 41 GW of solar. But the institution did not have the heft to take this forward, while it was not until the award of MBR Phase 2 in 2016 that the potential for very competitive solar power in the region was fully demonstrated. The King Salman Renewable Energy Initiative, part of Vision 2030, was launched in 2016 with a target of 9.5 GW by 2023, upgraded in 2018 to 27.3 GW. But by the end of 2023 total capacity was only at 2.8 GW.

The National Renewable Energy Program was announced in February 2019, targeting 40 GW of solar PV, 16 GW of wind, and 2.7 GW of CSP by 2030.[19] The intention is to award 30% of planned capacity through tenders and to establish competitive price benchmarks. The influential Public Investment Fund (PIF) would carry out the remaining 70%, likely drawing heavily on its partnership with Saudi developer Acwa Power, which is listed on the Kingdom’s Tadawul exchange but in which PIF holds 44%.

The program is finally gathering momentum, following the beginning of operations at the 300 MW Sakaka solar farm in November 2019, the 400 MW Dumat Al Jandal wind farm in August 2021, the 300 MW Rabigh PV in April 2023, and the 750 MW first phase of Sudair PV in September 2023. The 2.8 GW at the end of last year will probably rise to 3.8 GW by the end of 2024, but the real acceleration will come in 2025–26. A further 12.6 GW has been awarded, and Saudi energy minister Prince Abdulaziz bin Salman announced that 20 GW will be tendered this year[20] and that a total of 130–150 GW by 2030 was doable.

Therefore the 27.3 GW target might be reached around 2027, four years late, leaving another 30 GW to be delivered in three years to reach the 2030 aim. This does not include renewable energy devoted to hydrogen production, notably the 1.37 GW of wind and 2.93 GW of solar being built at Neom in the country’s far northwest. But this pace of additions should be achievable if the 20 GW pace of planned awards can be sustained and completed on time. The solar PV projects are moving more quickly than wind, although Round 4 of the NREP included 1.8 GW of wind. CSP, a much smaller component, does not appear to have advanced recently.

Will This Put the GCC on Track for Global Targets?

Tripling installed global renewable energy capacity by 2030, as committed at COP28 last year,[21] from 3,400 GW last year to 10,500–11,000 GW by 2030, means an annual addition of about 1,500 GW by 2030. There are various ways to assess how much of that “should” be in the GCC, but using the 2.5% share of world electricity generation as a simple benchmark, it would equate to about 37.5 GW. This requires a considerable step-up of the current pace, but it would appear achievable if Saudi Arabia can sustain more than 20 GW in annual awards and completions, particularly when including additional renewables dedicated to hydrogen. In fact, GCC capacity is likely to increase more than 10 times over 2022 levels by 2030.

However, as noted, this is very patchily distributed between the six countries. With the partial exception of Bahrain, it would be technically and economically feasible for all of them to boost renewable capacity substantially beyond current targets by around 2030. This depends on intensified government focus along with opening the sector to wider participation. Allowing more flexible procurement of renewables, including by industries for their own use with “wheeling” through the grid, and reforming end-user electricity pricing to reward distributed generation appropriately, would complement state utilities and power procurement bodies.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

Two trade agreements recently negotiated by the Trump administration contain novel and coercive provisions with little precedent in US trade policy or the global trade system.

Gulf Cooperation Council (GCC) countries have not only the world's lowest costs for oil and gas production but also the lowest costs for electricity generated from renewable energy sources.