“Everything up in the air”: LNG, the Strait of Hormuz, and Central & Eastern Europe’s energy future

"LNG shipments to Central & Eastern Europe are reliable as long as those gas markets are not overly dependent upon one supplier."

Get the latest as our experts share their insights on global energy policy.

On February 28, the US and Israel launched new attacks on Iran targeting primarily the country's leadership, security forces, and missile program.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

It’s been a head-spinning day in the Iran war. Earlier today, following a temporary truce between Lebanon and Israel, Iran announced that the Strait of Hormuz would be...

Find out more about our upcoming and past events.

The Columbia Global Energy Summit 2026 is an annual event dedicated to thought-provoking discussions around the critical energy and climate challenges facing the global community.

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

The US Federal Reserve (Fed) commenced its monetary easing cycle on Wednesday with an aggressive 50 basis points policy rate cut. The United States is not alone in this respect. Among the majors, central banks of the Eurozone, England, Canada, Switzerland, and Sweden have already embarked on their rate-cutting cycles, with some looking to increase the pace.[1]

With inflation broadly falling back into the central banks’ target ranges, it is safe to say that the inflationary environment that followed the 2020 COVID-19 pandemic is now behind. Indeed, with the risk of economic slowdown increasing, global interest rates are expected to continue falling going into next year.

The sharp increase in interest rates over the past couple of years to tame inflationary pressures led to higher costs of capital which impacted many industries. Stocks of renewable energy companies, in particular, suffered heavily. It is therefore fair to ask whether the reversal in the interest rate cycle will spur a recovery in the renewable energy sector. This blog addresses this question and concludes that while the interest rate environment is decisively turning supportive, other factors may continue to weigh on the sector preventing a turnaround at least in the near term.

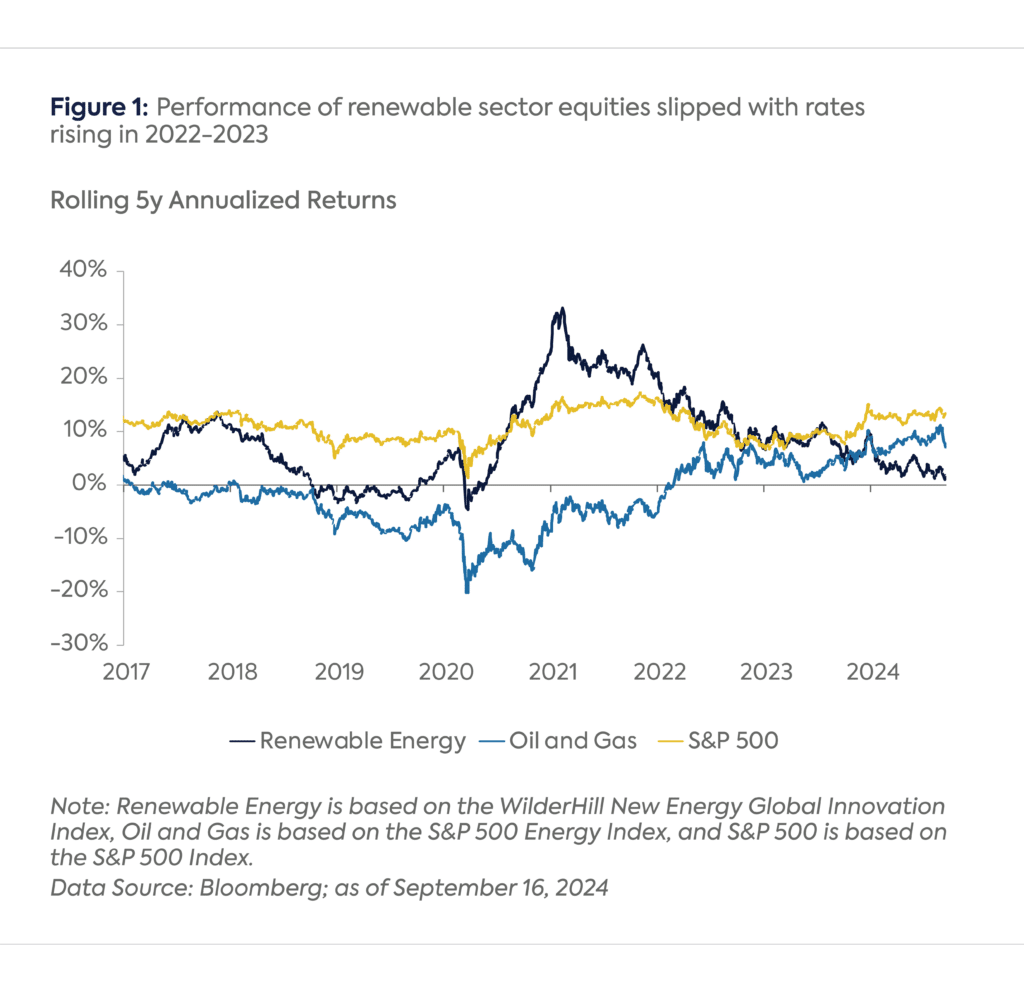

Equities in the renewable energy sector got a big boost in 2020, with the returns from the sector continuing to be high in 2021 and early 2022 relative to the pre-pandemic period (see Figure 1). Several factors were behind this performance:

The performance of the renewable energy sector started reversing in 2022, which coincided with the aggressive rate-hiking cycle by the Fed and other central banks around the world. In the United States, the policy rate was raised from close to 0% to over 5% in less than 18 months. The increase in interest rate impacted stock valuations across the board, but it was particularly penalizing for renewable energy companies.

Companies in the sector require high upfront capital investment with cash flows expected in future years. The sharp rise in interest rates implied a much lower present value of these cash flows and, therefore, stock valuations. Even the significant policy support provided in the United States―in the form of the passage of the Bipartisan Infrastructure Bill in November 2021 and the Inflation Reduction Act (IRA) in August 2022―could not reverse the sector’s underperformance, partly because it was clear that it would take a few years to deploy the funds provided by these programs.

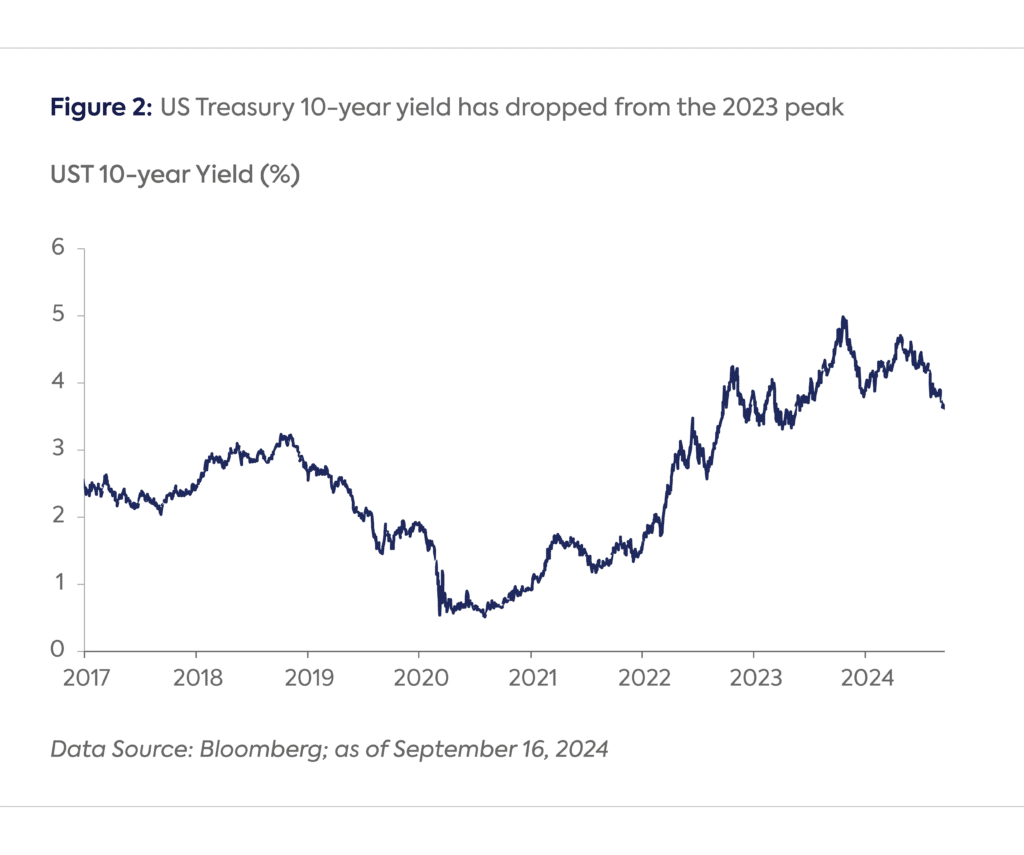

The interest rate cycle is now turning with the market expecting the Fed to lower rates by another 2 percentage points or so in a year, bringing the policy rate below 3 percent, according to Bloomberg. The yield curve is already reflecting much of this, with the 10-year late around 1.5 percentage points below its peak (Figure 2). The drop in long-end rates is important because of its relevance in discounting future cash flows as well as being the benchmark for the borrowing rate of a company, which is typically priced at a spread over the US Treasury yield of the bond’s tenor.

Although the low interest rate environment should be supportive of the renewable energy sector, several headwinds remain in the near term:

Notwithstanding the factors weighing on the performance of renewable energy stocks―particularly the high cost of capital―over the last couple of years, global investments in clean energy have continued apace as publicly traded stocks represent only about a quarter of the financing sources for renewable energy.[14]

The International Energy Agency estimates that clean energy investments should cross $2 trillion in 2024.[15] Nevertheless, the 6.4% year-on-year increase in investments in 2024 pales in comparison with the annual increases of 14.7% in 2021 and 19.0% in 2022. Moreover, without a considerable increase in the pace of deployment, the target of tripling renewables by 2030―as pledged at COP28―would be out of reach.[16]

As interest rates drop, the resulting lower cost of capital should help accelerate these investments in 2025, assuming that some of the headwinds dissipate and the election outcome in the United States is climate-friendly.

The author is immensely grateful to Dr. Noah Kaufman for his valuable feedback on an earlier draft of the blog.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] Naomi Rovnick and Alun John, “Major Central Banks’ Rate Cuts Gather Pace” Reuters, August 1, 2024, https://www.reuters.com/markets/rates-bonds/major-central-banks-rate-cuts-gather-pace-2024-08-01/ and Erik Hertzberg and Jay Zhao-Murray, “Bank of Canada to Start Jumbo Rate Cuts by December, CIBC Says,” Bloomberg, September 12, 2024, https://www.bloomberg.com/news/articles/2024-09-12/bank-of-canada-to-start-jumbo-rate-cuts-by-december-cibc-says.

[2] Lazard, “Lazard’s Levelized Cost of Energy Analysis―Version 14.0,” October 2020, https://www.lazard.com/media/kwrjairh/lazards-levelized-cost-of-energy-version-140.pdf.

[3] International Energy Agency, “Renewable Energy Market Update: Outlook for 2021 and 2022,” May 2021, https://www.iea.org/reports/renewable-energy-market-update-2021/renewable-electricity.

[4] Laura Rodríguez, “The Rise of Solar Stocks: Up in 2021 Too,” Rated Power, April 14, 2021, https://ratedpower.com/blog/solar-stocks/.

[5] Oxford Economics, “After the Presidential Debate, the US Election Remains a Toss-Up,” September 12, 2024, https://www.oxfordeconomics.com/resource/after-the-presidential-debate-the-us-election-remains-a-toss-up/.

[6] Kristi E. Swartz, “Red States Gain Major Benefits from the Climate Law. Some Still Hate It.” Earth Island Journal, August 15, 2024, https://earthisland.org/journal/index.php/articles/entry/gop-gets-85-of-the-benefit-of-climate-law.-some-still-hate-it.

[7] Senate Committee on Energy and Natural Resources, “Manchin, Barrasso Release Bipartisan Energy Permitting Reform Legislation,” July 22, 2024, https://www.energy.senate.gov/2024/7/manchin-barrasso-release-bipartisan-energy-permitting-reform-legislation.

[8] JP Morgan, “The Probability of a Recession Now Stands at 35%,” August 15, 2024, https://www.jpmorgan.com/insights/global-research/economy/recession-probability.

[9] Abraham Silverman, Gautam Jain, Dafni Papapolyzou, Kavyaa Rizal, Devan Samant, and Josh Williard, “FERC’s Interconnection Reform: Why It Matters for the Clean Energy Transition,” Center on Global Energy Policy, Columbia University, August 7, 2023, https://www.energypolicy.columbia.edu/fercs-interconnection-reform-why-it-matters-for-the-clean-energy-transition/.

[10] Adam Wilson and Tony Lenoir, “Interconnection Queues Show Swelling Volume but FERC Reforms Slowly Taking Hold,” S&P Global, May 15, 2024, https://www.spglobal.com/marketintelligence/en/news-insights/research/interconnection-queues-show-swelling-volume-but-ferc-reforms-slowly-taking-hold.

[11] International Trade Administration, “Commerce Initiates Antidumping and Countervailing Duty Investigations of Crystalline Silicon Photovoltaic Cells from Cambodia, Malaysia, Thailand, and the Socialist Republic of Vietnam,” US Department of Commerce, May 15, 2024, https://www.trade.gov/commerce-initiates-antidumping-and-countervailing-duty-investigations-crystalline-silicon.

[12] Lilly Yejin Lee and Noah Kaufman, “Q&A | Solar Tariffs and the US Energy Transition,” Center on Global Energy Policy, Columbia University, November 13, 2023, https://www.energypolicy.columbia.edu/qa-solar-tariffs-and-the-us-energy-transition/ and The White House, “Fact Sheet: President Biden Takes Action to Protect American Workers and Businesses from China’s Unfair Trade Practices,” Briefing Room, Statement and Releases, May 14, 2024, https://www.whitehouse.gov/briefing-room/statements-releases/2024/05/14/fact-sheet-president-biden-takes-action-to-protect-american-workers-and-businesses-from-chinas-unfair-trade-practices/.

[13] Rhodium Group and MIT CEEPR, “Clean Investment Monitor: Q1 2024 Update,” May 30, 2024, https://cdn.prod.website-files.com/64e31ae6c5fd44b10ff405a7/6657a11d401a6ff7a3a67466_Clean%20Investment%20Monitor%20-%20Q1%202024%20Update.pdf.

[14] Climate Policy Initiative, “Global Landscape of Climate Finance 2023,” November 2023, https://www.climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2023/.

[15] International Energy Agency,” World Energy Investment 2024,” June 2024, https://www.iea.org/reports/world-energy-investment-2024.

[16] IRENA, “Tripling Renewables by 2030 Requires a Minimum of 16.4% Annual Growth Rate,” Press Release, July 11, 2024, https://www.irena.org/News/pressreleases/2024/Jul/Tripling-Renewables-by-2030-Requires-a-Minimum-of-16-point-4-pc-Annual-Growth-Rate.

The US-Israeli war against Iran highlights the Gulf’s dual role as the backbone of global energy supply and a major source of systemic risk.

The war in Iran has significantly enhanced Latin America's geopolitical advantage as a reliable source of hydrocarbon resources.

Media reports suggest the Trump Administration is considering restrictions on US oil exports.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Within days of the initial U.S. and Israeli attack on Iran on February 28, 2026, the world was plunged into an energy crisis.

Anne-Sophie Corbeau and leading experts explore how Europe's gas sector is being reshaped by geopolitical shocks.