Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

The Southern Gas Corridor (SGC) aims to increase and diversify Europe’s energy supply by bringing gas resources from the Caspian Sea to European markets. Continuing her series analyzing energy issues in post-Soviet states, including in Uzbekistan, Moldova, and Kazakhstan, the author answers key questions about the economics of Caspian gas in this article.

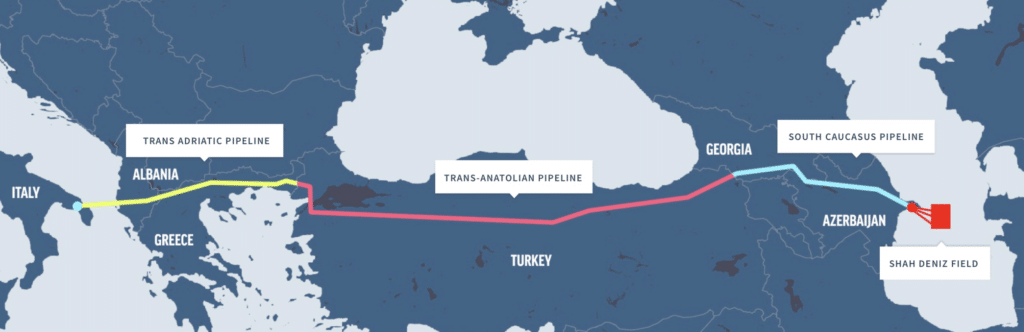

The SGC is a route from the Caspian region to Europe, proposed in 2008[1] to reduce Europe’s dependency on Russian gas.[2] It consists of the South Caucasus Pipeline (SCP) and its expansion (SCPX), the Trans-Anatolian Natural Gas Pipeline (TANAP), and the Trans-Adriatic Pipeline (TAP).

Source: https://www.sgc.az/en.

The SGC’s role as a gas supplier to the EU—though still small—is increasing. During the 2022 energy crisis, gas deliveries via the SGC to Europe increased by more than 40 percent, from around 8 billion cubic meters (bcm) in 2021 to 11.4 bcm in 2022, going above the TAP pipeline’s nominal capacity of 10 bcm.[3] The SGC’s share in total EU gas imports was 3.4 percent in 2022 up from 2.4 percent in 2021.[4]

In July 2022, the European Union (EU) and Azerbaijan signed a Memorandum of Understanding (MoU) on a strategic partnership with an ambitious commitment to double the capacity of the SGC to deliver at least 20 bcm of gas to the EU annually by 2027.

Azerbaijan, with its giant Shah Deniz field that started production in 2006, is the only source of gas for the SGC so far. For many years, the country supplied gas only to Georgia[5] via SCP and then to Turkey via TANAP. It was only when the TAP was launched, as an extension of the SGC in 2020, that Azerbaijan started supplying gas directly to the EU. The TAP starts at the Greek-Turkish border, runs through Greece, Albania, crosses the Adriatic Sea and connects to Italy’s natural gas network.

Gas deliveries to Italy and Greece began immediately after the commissioning of the TAP.[6] Deliveries to Bulgaria began in 2022[7] and in 2023, Azerbaijan started gas supplies to Romania[8] with plans to start deliveries to Hungary and Serbia by the end of the year.[9] All of these flows have been enabled by the completion of the EU-funded Interconnector Greece-Bulgaria pipeline in October 2022.

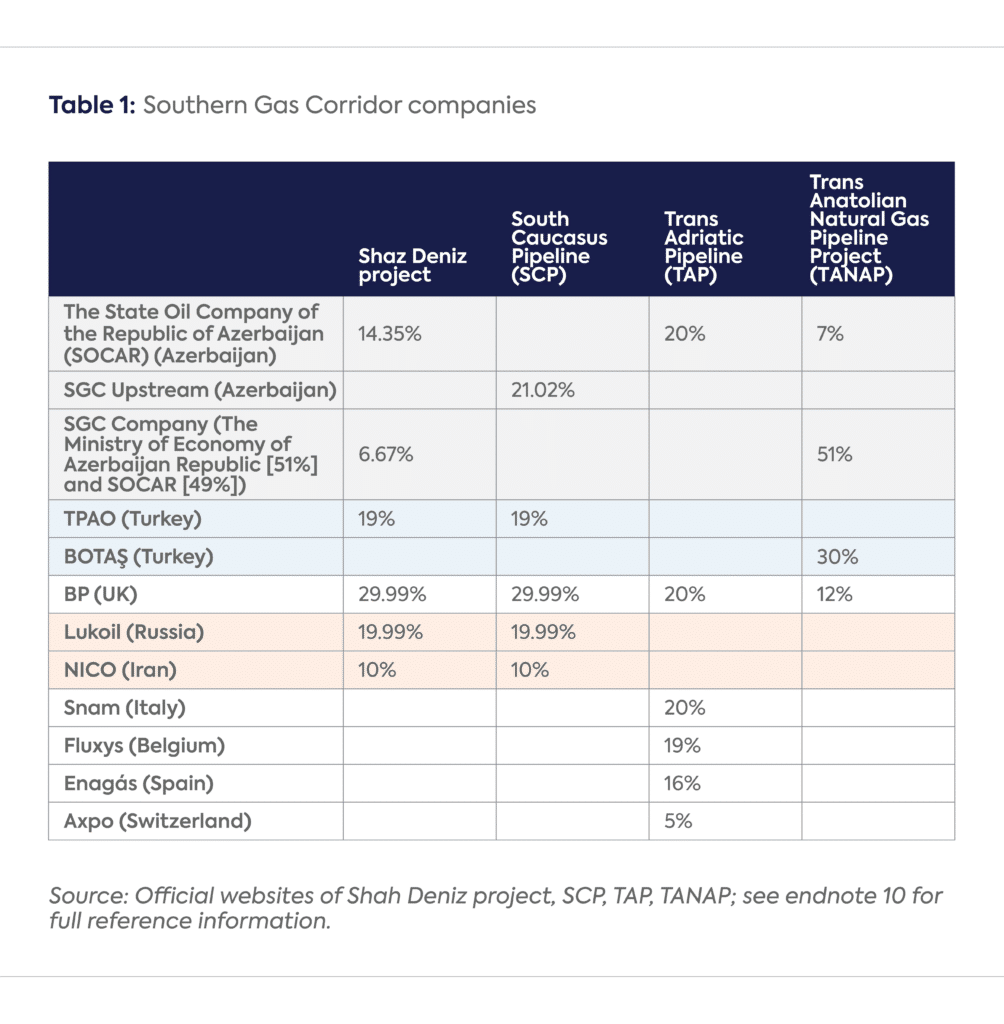

The SGC’s total investment amounts to $40 billion.[10] It is an international mega-project with many stakeholders. Azerbaijan participates in all parts of the supply chain and Turkey provides crucial transit to Europe in all parts except TAP. Several Western companies, including BP, have a stake in the project along with—surprisingly—Russian LUKOIL and Iranian NICO that together control nearly 30 percent of the upstream investments and the SCP (Table 1).

The promised doubling of gas deliveries from Azerbaijan to the EU in four years would require huge investments in the SGC’s infrastructure expansion (including in all sections of the corridor), estimated at $6.3-$9.3 billion[11] and further upstream investments in additional gas production in Azerbaijan. So far, according to the forecast approved by the government in 2021, Azerbaijan is expected to increase its output by only 3 bcm until 2026,[12] likely leading to volumes falling short of the additional10 bcm needed to fulfil the new MoU. In theory, a Shah Deniz extension together with the other projects such as ACG Deep, Absheron Phase 1 and Ümid,[13] could add about 13.5 bcm of incremental gas production for export, but these projects would require additional investments of more than $10 billion.[14]

Investment at this scale is unlikely to materialize without long-term guarantees of investment returns. Azerbaijan itself can hardly ensure the required investments, while the EU—with its ambitious decarbonization targets and plans to phase out long-term contracts[15]—is not supporting the contract structures to justify upstream and midstream capital expenditures. European commercial companies are also not keen to make long-term commitments given the uncertainty related to the future of European gas demand. There are fundamental doubts about whether Europe needs so much additional gas from Caspian, likely more expensive than other supplies (such as the LNG[16] that will become available starting 2025) and that new pipeline projects could become stranded assets by the mid-2030s.

It remains uncertain whether Azerbaijan can simultaneously boost production for export and meet its growing domestic needs. Domestic consumption of natural gas stood at about 13 bcm in 2021 and is expected to grow to 15-16 bcm by 2027.[17] So far, Azerbaijan has addressed this issue by importing gas from Russia as well as from Turkmenistan via Iran. However, the deal with Russia, signed last November to supply approximately 1 bcm of gas to Azerbaijan over five months, was not extended in 2023[18] after the EU raised concerns about increased gas exports from Russia to Azerbaijan.[19]

Meanwhile, Azerbaijan’s dependency on Turkmenistan is deepening. An initial deal for annual 1,8-2,1 bcm of gas swaps from Turkmenistan to Azerbaijan via the Iranian pipeline system was signed in December 2021,[20] with the volumes doubled in June 2022.[21][22] This August, the Iranian Ambassador in Turkmenistan emphasized the potential to increase gas swaps from 7-7,5 million cubic meters per day (mcm/day) to up to 20 mcm/day.[23]

The problem of where to find the additional roughly 10 bcm of gas for the SGC could be solved by building the Trans-Caspian pipeline from Turkmenistan to Azerbaijan. The Trans-Caspian pipeline project was initiated by Turkmenistan in November 2007, as part of its diversification plans away from Russia and as construction of a gas pipeline from Turkmenistan to China started. These discussions gradually come to naught, most likely because of Turkmenistan’s concerns about Chinese complaints about the country failing to deliver on its commitments. In 2022, when Russia cut gas supplies to Europe, the project regained the interest of the EU after years of Turkmenistan asking for Western financing for it. The initial project envisaged 30 bcm annual capacity and an estimated construction cost of $5 billion or more. Latest estimates suggest that a lighter version of the project, to be built over 24 months at a relatively modest cost of $500-800 million, could deliver 10-12 bcm of gas annually.[24] An expected announcement about it when the presidents of the three Turkic states—Turkmenistan, Turkey, and Azerbaijan—met in Turkmenistan last December[25] did not materialize,[26] but in May, Azerbaijan’s President Ilham Aliyev confirmed that his country would provide technical assistance turning the focus on Turkmenistan: “this decision must be made by the owners of these resources [Turkmenistan]. We cannot initiate this project, and we cannot finance it. We can only be a transit country.”[27]

There have long been doubts about whether Turkmenistan is really planning to join the Trans-Caspian project and provide additional gas volumes for the SGC, but in July, Turkmen authorities clarified their position[28] calling the Trans-Caspian pipeline “an absolutely realistic project, justified from an economic point of view, capable of making a tangible contribution to ensuring energy security in Eurasia.” Turkmenistan now says that it is committed to the strategy of diversifying energy flows and will cooperate with partners in the implementation of the Trans-Caspian pipeline project.

Following the statement, a Turkmen envoy met with president of the European commission, Ursula von der Leyen, expressing Turkmenistan’s readiness to “develop effective cooperation between Turkmenistan and the EU.”[29] Continuing this diplomatic shift, Turkmenistan signed a political agreement (not a binding one) to supply Turkmen gas to Hungary in August.[30] Favorable political declarations notwithstanding, the prospects of a Trans-Caspian pipeline are still quite remote. Based on existing infrastructure, Turkmenistan may only be able to supply up to 5 bcm/year from the Petronas’ owned offshore Block I fields.[31] Most of the country’s untapped production potential is far from the Caspian at the Galkynysh field in the southeast. Turkmenistan recently committed to more than double its natural gas exports to China—to 65 bcm/year—via the expansion of the Turkmenistan-Uzbekistan-Tajikistan-Kyrgyzstan-China gas pipeline, synchronized with the second stage of the Galkynysh field development.[32]

An additional concern is that Turkmenistan is responsible for the world’s largest number of methane emitting fossil fuel facilities,[33] not acceptable for the EU given its methane strategy.

Moreover, a key obstacle again, as with Azerbaijan, is the unwillingness of international commercial enterprises to provide project financing considering the uncertainty of future European gas demand.

The geopolitics of Caspian gas are just as complex, as the author will discuss in her next article.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] EU (2008) Communication from the Commission COM (2008) 781 dated 13 November 2008: Second Strategic Energy Review: An EU Energy Security and Solidarity Action Plan. Brussels: EU; http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2008:0781:FIN:EN:PDF.

[2] The current configuration emerged from several competing project proposals, including the Nabucco pipeline.

[3] https://energy.ec.europa.eu/news/commissioner-simson-azerbaijan-co-chair-9th-southern-gas-corridor-advisory-council-2023-02-03_en; https://ec.europa.eu/commission/presscorner/detail/en/ip_22_4550

[4] https://energy.ec.europa.eu/topics/energy-security/diversification-gas-supply-sources-and-routes_en

[5] https://www.bp.com/en_ge/georgia/home/who-we-are/scp.html

[6] https://www.tap-ag.com/infrastructure-operation/history-timeline#period-12977

[7] https://www.tap-ag.com/infrastructure-operation/history-timeline#period-12977

[8] https://caliber.az/post/130979/

[9] https://www.argusmedia.com/en/news/2456293-hungarys-mvm-signs-deal-for-100mn-m-of-azeri-gas

[10] https://www.bp.com/en/global/corporate/news-and-insights/reimagining-energy/southern-gas-corridor-special-feature.html; https://minenergy.gov.az/en/qaz/sahdeniz-yatagi; https://www.sgc.az/en/project/scp; https://www.tap-ag.whicom/about-tap/taps-shareholders; https://www.tanap.com/en/shareholders

[11] Gulmira Rzayeva, “Expansion of the Southern Gas Corridor pipelines and future supplies to Europe,” Oxford Institute for Energy Studies, NG-180, April 24, 2023, 9, https://books.google.co.uk/books/about/Expansion_of_the_Southern_Gas_Corridor_P.html?id=EpwT0AEACAAJ&redir_esc=y

[12] https://interfax.az/view/852215

[13] https://www.spglobal.com/commodityinsights/en/ci/research-analysis/will-azerbaijan-meet-europes-2027-gas-demand-deadline.html

[14] Gulmira Rzayeva, “Expansion of the Southern Gas Corridor pipelines and future supplies to Europe,” Oxford Institute for Energy Studies, NG-180, April 24, 2023, 9, https://books.google.co.uk/books/about/Expansion_of_the_Southern_Gas_Corridor_P.html?id=EpwT0AEACAAJ&redir_esc=y

[15] https://www.energyintel.com/0000017d-beef-d2b5-a1fd-bfefc7620001

[16] https://www.energypolicy.columbia.edu/publications/beyond-spot-vs-long-term-europes-lng-contracting-options-for-an-uncertain-future/

[17] https://www.eiu.com/n/azerbaijans-gas-exports-to-the-eu-face-challenges/

[18] https://eurasianet.org/azerbaijans-russian-gas-deal-raises-uncomfortable-questions-for-europe; https://www.eiu.com/n/azerbaijans-gas-exports-to-the-eu-face-challenges/

[19] https://www.europarl.europa.eu/doceo/document/P-9-2022-003854_EN.html#:~:text=There%20are%20reports%20that%20Gazprom,and%20March%202023%5B1%5D

[20] https://www.bbc.com/azeri/region-59413187

[21] https://www.newscentralasia.net/2023/04/16/nigc-iran-recorded-a-surge-in-gas-swap-from-turkmenistan-to-azerbaijan/

[22] https://eurasianet.org/turkmenistan-iran-azerbaijan-gas-swaps-surge

[23] https://az.sputniknews.ru/20230813/iran-narastil-svopovye-postavki-turkmenskogo-gaza-v-azerbaydzhan-457668115.html

[24] https://www.intellinews.com/pannier-how-putin-may-have-leant-on-turkmenistan-to-spike-gas-for-europe-plan-265579/

[25] https://www.intellinews.com/pannier-how-putin-may-have-leant-on-turkmenistan-to-spike-gas-for-europe-plan-265579/; https://eurasianet.org/turkmenistan-smashing-time

[26] https://www.intellinews.com/analysts-say-turkmenistan-told-us-diplomats-it-s-not-interested-in-caspian-gas-to-europe-connector-project-wants-major-pipeline-265227/

[27] https://eurasianet.org/turkmenistan-iran-azerbaijan-gas-swaps-surge

[28] https://mfa.gov.tm/en/news/3969

[29] https://mfa.gov.tm/en/news/3977

[30] According to Peter Szijjarto, Hungary’s minister of foreign affairs and foreign economic relations, “On the part of Turkmenistan, the political will and political intention is absolutely clear for Hungary to become one of the directions of potential supplies of Turkmen gas to Europe and one of the transit countries.” https://orient.tm/en/post/58762/szijjarto-said-budapest-and-ashgabat-have-concluded-political-agreement-gas-supplies.

[31] https://www.spglobal.com/commodityinsights/en/ci/research-analysis/will-azerbaijan-meet-europes-2027-gas-demand-deadline.html

[32] https://www.enerdata.net/publications/daily-energy-news/turkmenistan-plans-more-double-gas-exports-china-65-bcmyear.html#:~:text=Turkmenistan%20plans%20to%20more%20than%20double%20its%20natural%20gas%20exports,gas%20pipeline%2C%20currently%20under%20construction; https://www.reuters.com/markets/commodities/china-prioritising-turkmenistan-over-russia-next-big-pipeline-project-2023-05-24/

[33] https://www.theguardian.com/environment/2023/mar/06/revealed-1000-super-emitting-methane-leaks-risk-triggering-climate-tipping-points

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

The UNFCCC process is marred by gridlock in the COP multilateral framework, threatening joint efforts by countries to mitigate the climate crisis.

The US blockade of tankers serving Iran's oil exports is intended to cut Iranian oil exports to near-zero.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia