Trump says ongoing talks are Iran’s ‘last chance’

Karen Young, senior research scholar at the Centre on Global Energy Policy at Columbia University, joins BNN Bloomberg to discuss the energy sector.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Over the past five months, the Strait of Hormuz has been closed for extended stretches of time, disrupting roughly 10 to 15 million barrels of oil supply each...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Commentary by Erica Downs, Akos Losz & Tatiana Mitrova • May 15, 2024

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

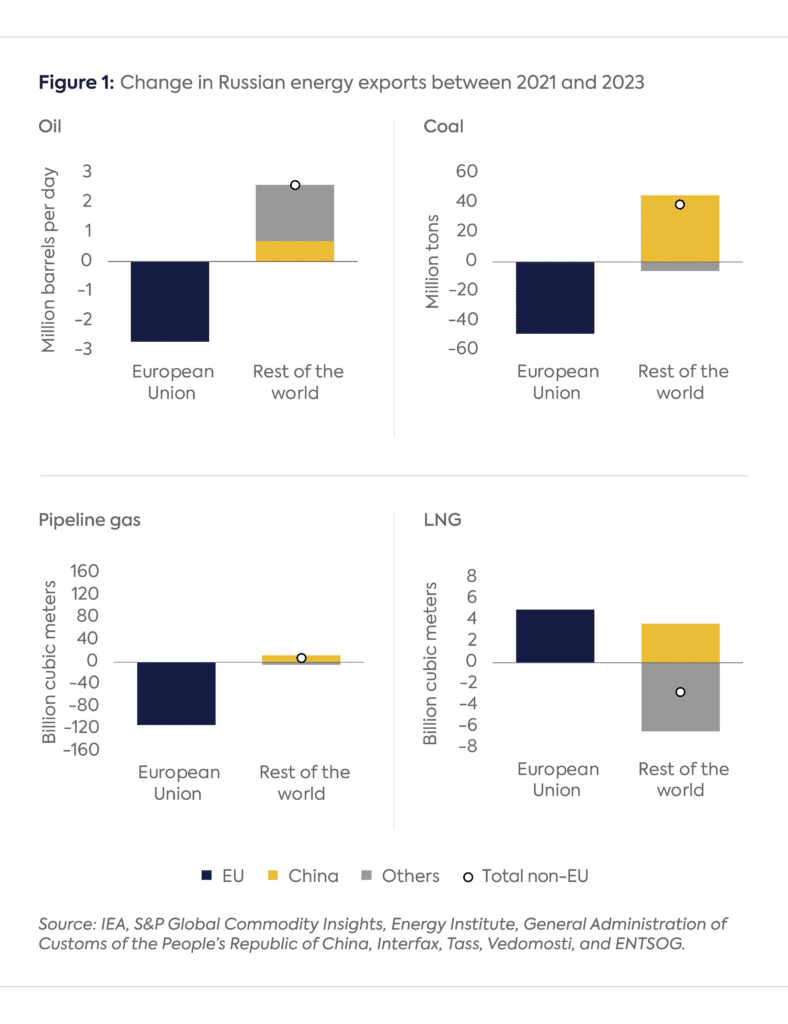

As Russian President Vladimir Putin prepares to visit China on May 16-17, 2024, the proposed Power of Siberia 2 (PS-2) natural gas pipeline is likely high on his agenda. After all, Russian energy exports to Europe have fallen precipitously since the invasion of Ukraine in February 2022, with pipeline gas and oil flows to Europe declining by more than 80 percent and coal exports by nearly 100 percent. Although Russia has been able to redirect most of its oil and coal exports to other markets, it has been unable to do so with natural gas due to a lack of infrastructure linking its western production basins to consumers in Asia (Figure 1).[i]

PS-2, with its 50 billion cubic meters per year (bcm/y) design capacity, could offset nearly half of the decline in Russian pipeline gas export to the EU between 2021 and 2023. While the Kremlin has made no secret of its eagerness to expedite the project,[ii] its fate remains uncertain, largely because China has refrained from committing to it.

This commentary explores the future of PS-2 through an analysis of the broader China-Russia energy relationship and the Russian and Chinese positions on the project. It also examines implications of the pipeline’s potential completion for global gas markets. The piece contends that despite Russia’s intentions, PS-2 has made limited progress because China currently stands to benefit from keeping the project in a holding pattern. But if China can secure an attractive price for PS-2 gas, and if China’s relations with the United States continue to deteriorate, Beijing could be motivated to reverse course. The completion of PS-2, if it happens, would likely therefore be on China’s terms, and could reshape global gas markets in important ways.

The China-Russia energy trade relationship was sizeable before Russia’s invasion of Ukraine and has grown even larger since. In 2021–23, Russian crude oil exports to China increased by one-third, while coal and LNG exports nearly doubled (Figure 2). In 2023, Russia was China’s largest supplier of crude oil, second-largest supplier of coal, and third-largest supplier of LNG. Russia is also a growing exporter of pipeline gas to China. It increased deliveries through the Power of Siberia 1 (PS-1) pipeline from 10.4 bcm in 2021 to 22.7 bcm in 2023, accounting for 34 percent of China’s pipeline gas imports.[iii] Russia expects PS-1 to reach its full 38 bcm/y capacity by 2025.[iv] Additionally, China and Russia signed an agreement in early February 2022 for another pipeline, the Far Eastern Route, to deliver 10 bcm/y by 2027.[v]

Russia regards the loss of the European market as irreversible.[vi] While the Kremlin understands that expanded bilateral gas trade with China will never fully compensate for the loss of gas export revenues from Europe, [vii] and will naturally increase Russia’s dependence on China,[viii] it continues to prioritize PS-2 for several reasons.

When it comes to natural gas exports, geopolitics is the foremost consideration for Russia. Moscow regards gas as a potent tool in its dealings with counterparties across Eurasia. Until the 2010s, gas was widely used as “geopolitical currency” in the post-Soviet space: Russia offered gas at below-market rates in exchange for geopolitical alignment or control over critical energy infrastructure.[ix]

A similar calculation is likely at play with PS-2. By selling large volumes of cheap gas to China, Russia can potentially tie Beijing into a closer geopolitical alliance. Russia’s bargaining power with China is much weaker than it was with its former satellite states in previous decades, however. Convincing China to commit to such a large project during the war would be a geopolitical coup for Moscow, demonstrating to the West and the Global South that it is able to deepen its energy relationship with China despite the war.

PS-2 would most likely be less profitable than PS-1, due to its higher construction cost and the lower expected sales price of gas to China.[x] However, the pipeline is expected to generate a positive free cash flow, especially if it receives tax breaks as PS-1 did.[xi] The project would also generate orders for Russia’s steel producers and subcontractors and accelerate the economic development of eastern Russia,[xii] a top priority for Moscow.[xiii]

Russia is preparing for a long period of international isolation and transitioning to a wartime economy,[xiv] which supports large-scale, state-funded infrastructure projects. PS-2 could be one such flagship project, simultaneously marking Russia’s decisive breakup with the West and its pivot to the East. Russia’s indication in December 2023 that it was prepared to start building PS-2 without a supply contract underscores that the economic benefits associated with the project go far beyond the sale of gas molecules.[xv]

Gazprom, Russia’s state-owned pipeline monopoly, has its own reasons for championing PS-2 that dovetail with those of the Kremlin. In 2023, Gazprom suffered a collapse in gas revenues, leading to a staggering $6.8 billion net loss—the company’s first annual loss since 1999.[xvi] On top of its recent financial woes, the company has no large-scale infrastructure projects planned aside from PS-2 and the stalled Baltic LNG terminal.[xvii] The PS-2 project therefore poses an existential challenge to Gazprom: completing it can reaffirm its role as Russia’s natural gas champion; failing to do so could jeopardize the company’s very existence, with its assets potentially being divided among various elite groups inside Russia.

Gazprom’s main domestic rival, Rosneft, has been seeking to challenge Gazprom’s monopoly over gas export in Russia. In 2014, Rosneft tried to connect to PS-1, but Gazprom was able to retain full control over the pipeline’s capacity, despite Rosneft’s political heft. In 2023, Rosneft’s CEO repeated arguments from a decade before for allowing the company to use PS-2: the ability to monetize 8 bcm/y of associated gas in Eastern Siberia, the prospect of unlocking additional oil production in the region, and the possibility of reducing gas flaring and reinjection volumes.[xviii] Rosneft is still seeking to secure access, though it faces long odds. Nonetheless, the company is closely monitoring Gazprom for any mistakes that can sway Russian decision-makers to change course.

China has the luxury of time when it comes to PS-2 because it does not need the gas right away. Moreover, China is spoiled for choice in its supply options. As Beijing assesses whether and how PS-2 fits into its future import portfolio, its considerations almost certainly will include the following factors.

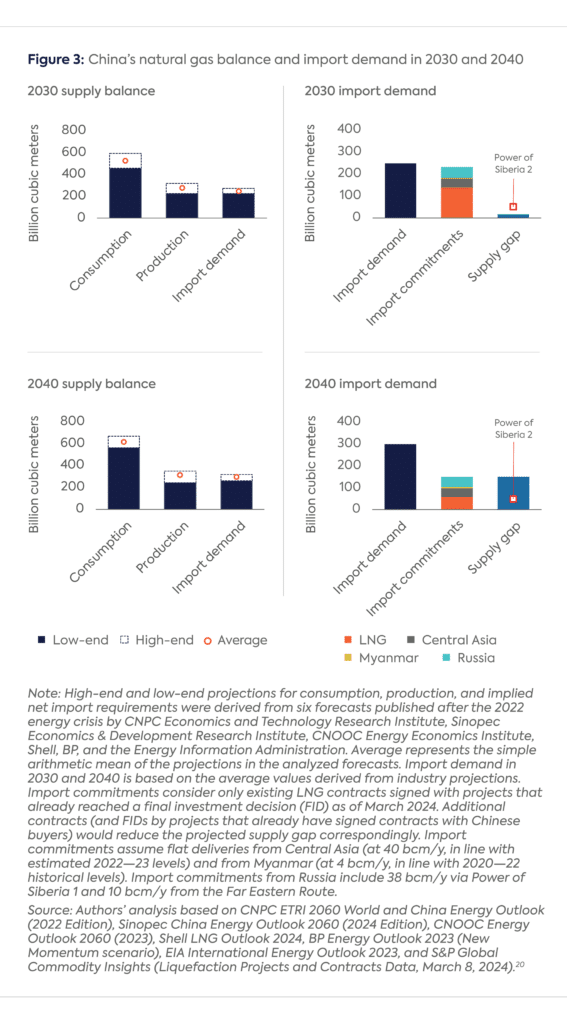

One reason China is in no hurry to finalize an agreement for PS-2 is that the country is unlikely to need the gas before the mid-2030s. Projections of China’s natural gas balance indicate that imports will reach around 250 bcm by 2030 (from less than 170 bcm in 2023),[xix] which largely (or entirely) can be met by already contracted supplies (Figure 3). Reference case projections also show, however, that there will most likely be room for PS-2 in China’s import portfolio by 2040. In that year, China’s gas imports could approach (or exceed) 300 bcm, with only 150 bcm covered by existing contracts.

Source: Authors’ analysis based on CNPC ETRI 2060 World and China Energy Outlook (2022 Edition), Sinopec China Energy Outlook 2060 (2024 Edition), CNOOC Energy Outlook 2060 (2023), Shell LNG Outlook 2024, BP Energy Outlook 2023 (New Momentum scenario), EIA International Energy Outlook 2023, and S&P Global Commodity Insights (Liquefaction Projects and Contracts Data, March 8, 2024).[xx]

PS-2 faces competition nonetheless. China’s LNG import capacity is set to increase from 144 to 250 bcm/y between 2022 and 2027.[xxi] This will allow China to absorb the 85 bcm/y of new LNG supply contracted in 2021–23—and to ink new agreements.[xxii] China could also increase pipeline imports from Central Asia via the stalled Line D project, which could deliver an additional 30 bcm/y from Turkmenistan if completed.

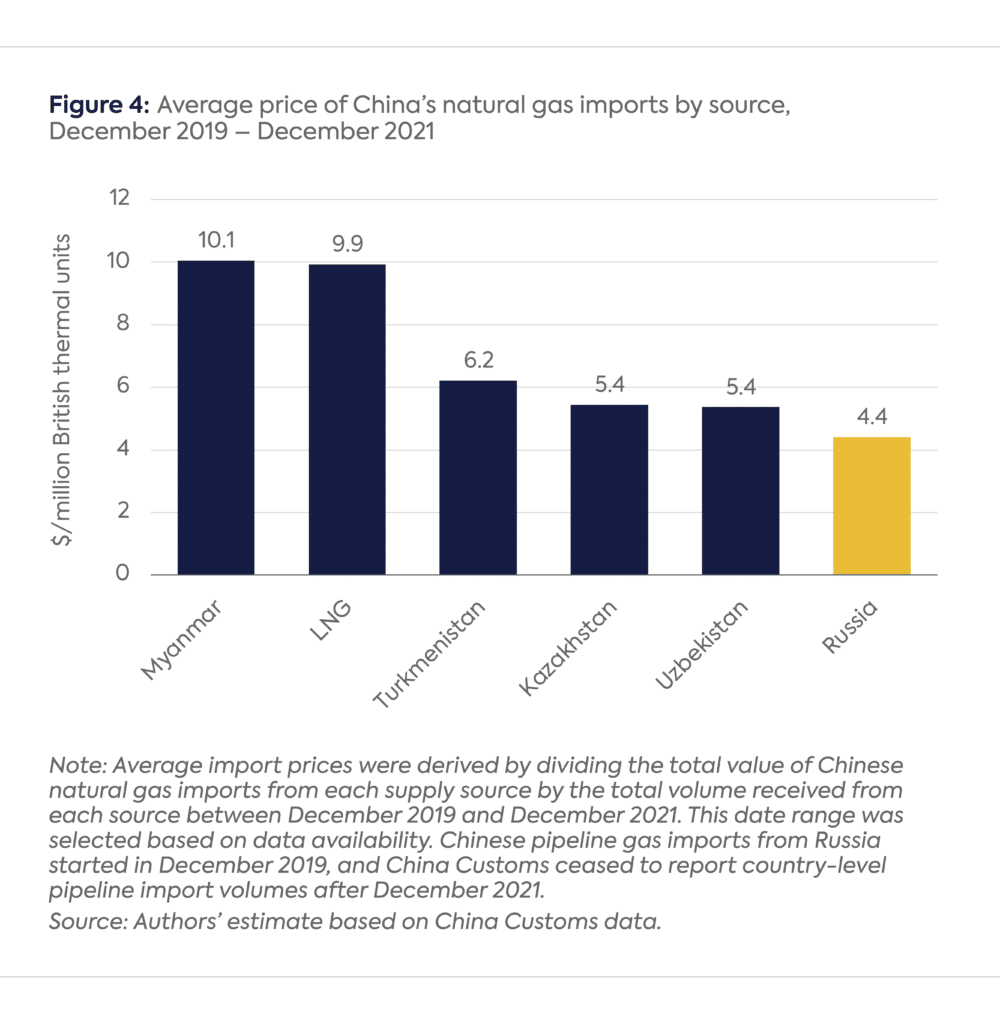

If China moves forward with PS-2, it will look to secure a lower price for PS-2 gas than it secured for PS-1 gas, since it is in an even stronger negotiating position with Russia than it was in 2014 when the supply contract for PS-1 was signed. China customs data from December 2019 through December 2021 show that PS-1 gas was cheaper than China’s other pipeline gas and LNG imports (Figure 4).[xxiii]

LNG prices will probably also factor into China’s PS-2 calculus. Sinopec noted in its long-term energy outlook that a likely increase in future LNG prices may necessitate the development of new import pipelines.[xxiv]

Slow-walking PS-2 also gives China’s importers leverage in contract negotiations with Russia and other suppliers; the discussions themselves put pressure on suppliers to sign contracts or risk losing a share of China’s natural gas imports. Indeed, as those discussions have unfolded, Chinese companies have signed new LNG supply contracts, including three 27-year deals with Qatar.[xxv] Moreover, in May 2023, China’s leader Xi Jinping told Central Asian leaders that construction of Line D should be expedited.[xxvi] These moves are reminders to Russia that China is pursuing other options to meet its import requirements.

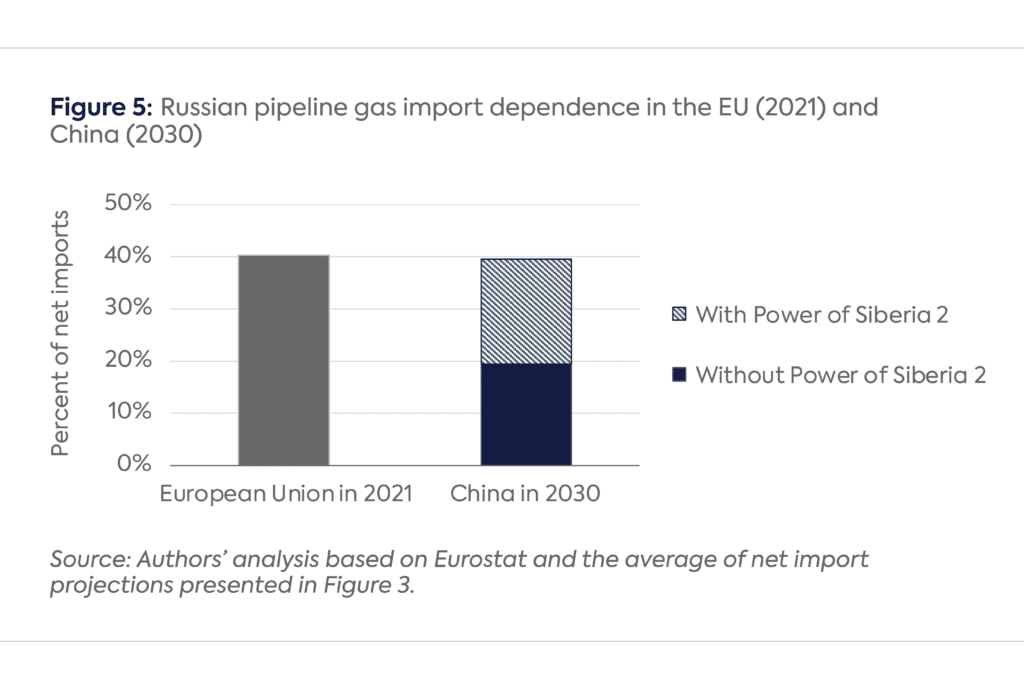

The fate of PS-2 will partly depend on Beijing’s assessment of the relative risks of greater dependence on Russian pipeline gas versus greater dependence on LNG imports. PS-2 would increase Russia’s pipeline capacity to China to 98 bcm/y. If this capacity is built and fully utilized by 2030, China’s net import dependence on Russian pipeline gas could reach 40 percent by 2030, on par with the EU’s dependence before Russia invaded Ukraine (Figure 5).

On the other hand, China’s reliance on LNG would almost certainly increase without PS-2. Chinese analysts have identified overreliance on US and Australian LNG as a vulnerability for China, which can be mitigated by growing gas imports from Russia.[xxvii] Indeed, as mentioned previously, it seems likely that a prolonged deterioration in the US-China relationship would prompt Beijing to look more favorably upon PS-2.[xxviii]

PS-2 would have profound implications for global gas trade. The project would bring up to 50 bcm/y of stranded Russian gas to the global market by displacing LNG in China’s import portfolio. For comparison, this volume is greater than Russia’s total LNG exports (43 bcm) and slightly less than Africa’s total LNG production (56 bcm) in 2023.[xxix]

If PS-2 starts deliveries by 2030, as Gazprom’s current plans suggest,[xxx] the extra gas from Russia would likely arrive in a market still coping with excess supply from the latest wave of LNG investment. Between 2024 and 2030, close to 300 bcm/y of new LNG export capacity could start operations.[xxxi] Most analysts maintain that this unprecedented supply wave will push the market into oversupply from 2025–26 until the late 2020s or early 2030s. China is expected to absorb much of the surplus.[xxxii] PS-2 could exacerbate this glut by weakening China’s LNG appetite.

There is a tension between PS-2 and Russia’s plans to more than triple LNG exports by 2030 (to 100 million tons per annum or 136 bcm).[xxxiii] Facing Western sanctions and possibly EU LNG import bans, Russia is increasingly reliant on Chinese equipment, financing, shipbuilding, and LNG offtake. China would likely have to reduce its LNG imports to make room for PS-2 gas, removing an obvious destination for incremental Russian LNG supply. Without a concerted effort to create additional demand for Russian LNG in emerging economies (potentially by offering affordable LNG to the Global South at a modest profit in exchange for geopolitical influence),[xxxiv] PS-2 would call into question the viability of Russia’s planned LNG projects.

PS-2 could also turbo-charge the emergence of Chinese LNG importers as global traders.[xxxv] Adding 50 bcm/y of pipeline gas to China’s import portfolio would force Chinese companies to be even more agile in their optimization of import flows, especially contracted LNG. This could entail greater reloading capabilities within China, joint LNG optimization schemes with other importers, and reserving LNG regasification capacity in overseas terminals. A long position in LNG following the ramp-up of PS-2 and a more prominent role in global LNG trading could reinforce China’s role as a global LNG market balancer in the 2030s, with far-reaching consequences for LNG trade flows, market liquidity, and energy geopolitics.

China has been content to keep PS-2 on the drawing board for now, affording it time to assess its post-2030 import needs, including the balance between pipeline and LNG imports. But certain geopolitical considerations for both China and Russia could propel the project toward completion, even if China has no immediate need for additional pipeline gas. Russia’s push for the project has been driven by noncommercial factors all along. For China, the price of gas and overreliance on a single supplier have been the primary concerns until now, but worsening relations with the US could lend additional support for PS-2. If and when the project is built, it likely will be on China’s terms—and it may well reshape the global gas market.

[i] LNG is an outlier as Russia was able to increase deliveries to both the EU and China (at the expense of other markets) between 2021 and 2023.

[ii] “Putin: Russia and China Have Agreed on Nearly All Parameters of Agreement on Power of Siberia 2 Gas Pipeline,” Interfax, March 21, 2023, https://interfax.com/newsroom/top-stories/88903/. See also President of Russia, “Russian-Chinese Talks,” March 21, 2023, http://en.kremlin.ru/events/president/news/70748.

[iii] “Russia’s Gas Supplies to China via Power of Siberia Hit 15.5 Bcm in 2022, says Novak,” Tass, January 16, 2023, https://tass.com/economy/1562675; Vladimir Soldatkin, “Russian Pipeline Gas Exports to China to Exceed 22.5 Bcm in 2023 – Gazprom,” Reuters, December 28, 2023, https://www.reuters.com/markets/commodities/russian-pipeline-gas-exports-china-exceed-225-bcm-2023-gazprom-2023-12-28/; Anastasia Dmitrieva et al., “Russia Starts Gas Deliveries to China via Power of Siberia,” S&P Global Commodity Insights, December 2, 2019, https://www.spglobal.com/commodityinsights/es/market-insights/latest-news/natural-gas/120219-russia-starts-gas-deliveries-to-china-via-power-of-siberia; National Bureau of Statistics of China, “Energy Production in December 2023,” January 18, 2024, https://www.stats.gov.cn/english/PressRelease/202402/t20240201_1947122.html.

[iv] Stuart Elliott, “Russian Pipeline Gas Exports to China Hit New Daily Record: Gazprom,” S&P Global, February 2024, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/natural-gas/020124-russian-pipeline-gas-exports-to-china-hit-new-daily-record-gazprom#:~:text=In%20a%20statement%2C%20Gazprom%20said,the%20supply%20record%20on%20Jan.

[v] “Russia to Begin Gas Supplies to China via Far Eastern Route by 2027 – Gazprom CEO,” Tass, October 22, 2023, https://tass.com/economy/1695103.

[vi] Sergey Vakulenko, “Can China Compensate Russia’s Losses on the European Gas Market?,” Carnegie Endowment for International Peace, June 1, 2023, https://carnegieendowment.org/politika/89862.

[vii] Alexey Belogoriev, “Blue Dream: Can China Save Russian Gas Exports,” Institute for Energy and Finance Foundation, June 23, 2023, https://fief.ru/media/news/golubaya-mechta-smozhet-li-kitay-spasti-rossiyskiy-gazovyy-eksport/.

[viii] Vladimir Soldatkin, “Russia’s Weaker Hand Undermines Case for Power of Siberia 2 Gas Link to China,” Reuters, October 30, 2023, https://www.reuters.com/business/energy/russias-weaker-hand-undermines-case-power-siberia-2-gas-link-china-2023-10-30/.

[ix] Belfer Center for Science and International Affairs, Harvard University and Baker Institute Center for Energy Studies, Rice University, “The Geopolitics of Natural Gas: The Geopolitics of Russian Natural Gas,” February 2014, https://www.belfercenter.org/sites/default/files/legacy/files/CES-pub-GeoGasRussia-022114.pdf.

[x] Recent projections by Russia’s Economy Ministry indicate that the export price of gas to China is expected to progressively drop from $287 per thousand cubic meters in 2023 to $228 per thousand cubic meters by 2027, and remain at a nearly 30 percent discount relative to Gazprom’s European sales throughout the 2023-27 period. “Russia Forecasts Lower Price for Its Gas to China Versus Europe,” Bloomberg News, April 23, 2024, https://www.bloomberg.com/news/articles/2024-04-23/russia-forecasts-lower-price-for-its-gas-to-china-versus-europe.

[xi] Sergey Vakulenko, “Can China Compensate Russia’s Losses on the European Gas Market?,” Carnegie Endowment for International Peace, June 1, 2023, https://carnegieendowment.org/politika/89862.

[xii] The Power of Siberia 1 pipeline, which has a shorter length and lower capacity than PS-2, required approximately 2.7 million tons of large diameter steel pipe, according to one preliminary estimate by a supplier. See TMK Group, “Investor Presentation 1Q 2015,” June 2015, p. 12, https://www.tmk-group.com/media_en/files/292/64/1Q_2015_IR_Presentation_June1.pdf.

[xiii] The Russian Government, “Establishment of Five Areas of Priority Socio-Economic Development in the Far Eastern Federal District,” August 22, 2015, http://government.ru/en/docs/19369/.

[xiv] “How Putin is Reshaping Russia to Keep His War-Machine Running,” Economist, November 30, 2023, https://www.economist.com/briefing/2023/11/30/how-putin-is-reshaping-russia-to-keep-his-war-machine-running.

[xv] “Gas Pipeline Construction in Mongolia May Begin as Early as 2024,” Oil and Capital, October 24, 2023, https://oilcapital.ru/news/2023-10-24/gazoprovod-v-mongolii-mogut-nachat-stroit-uzhe-v-2024-godu-3079188.

[xvi] “Russia’s Gazprom Group Reports First Net Loss in 24 Years,” Bloomberg News, May 2, 2024, https://www.bloomberg.com/news/articles/2024-05-02/russia-s-gazprom-group-reports-first-net-loss-in-23-years.

[xvii] Vladimir Afanasiev, “Baltic LNG Delayed for at Least Two Years,” Upstream, August 3, 2023, https://www.upstreamonline.com/lng/baltic-lng-delayed-for-at-least-two-years/2-1-1495193.

[xviii] Rosneft’s oil production is constrained by the lack of monetization options for associated gas in eastern Siberia. Licensing requirements prohibit the flaring or reinjection of associated gas in this producing region, effectively obligating subsurface users either to produce the associated gas or to curtail liquids production. See Tatyana Dyatel and Dmitriy Kozlov, “Rosneft Looks for Spot in Power of Siberia-2,” Kommersant, January 9, 2023, https://www.kommersant.ru/doc/5758825.

[xix] National Bureau of Statistics of China, “Statistical Communique of the People’s Republic of China on the 2023 National Economic and Social Development,” February 29, 2024, https://www.stats.gov.cn/english/PressRelease/202402/t20240228_1947918.html.

[xx] CNPC Economics and Technology Research Institute (ETRI), “World and China Energy Outlook 2022,” presentation delivered in January 2023; Shell, “LNG Outlook 2024,” February 2024, https://www.shell.com/what-we-do/oil-and-natural-gas/liquefied-natural-gas-lng/lng-outlook-2024.html; BP, “Energy Outlook 2023,” January 30, 2023, https://www.bp.com/en/global/corporate/energy-economics/energy-outlook/energy-outlook-downloads.html; US Energy Information Administration, “International Energy Outlook 2023,” October 11, 2023, https://www.eia.gov/outlooks/ieo/data.php; Sinopec Economics and Technology Research Institute and Sinopec Consulting, eds., China Energy Outlook 2060 (2024 Edition) (中国能源展望2060 (2024年版)), pp. 42 and 46, https://www.cpnn.com.cn/news/baogao2023/202401/W020240105322424121296.pdf; “There Are Still 20 Years to Go! China’s Offshore Oil and Natural Gas Production Will Peak” (还有20年!我国海洋油气产量将达峰), International Petroleum Online (国际石油网), November 18, 2023, https://oil.in-en.com/html/oil-2961324.shtml.

[xxi] Existing capacity at the end of 2022 based on GIIGNL, “Annual Report 2023,” July 2023, https://giignl.org/wp-content/uploads/2023/07/GIIGNL-2023-Annual-Report-July20.pdf; new capacity under construction based on Refinitiv.

[xxii] Contracted LNG volume with Chinese destination in 2021-23 calculated based on S&P Global Commodity Insights, Liquefaction Projects and Contracts Data (March 8, 2024); total volume includes contracts with pre-final investment decision projects and heads of agreement.

[xxiii] PS-1 commenced operations in December 2019; December 2021 is the last month for which Chinese Customs published country-level volumes of pipeline gas imports.

[xxiv] Sinopec Economics and Technology Research Institute and Sinopec Consulting, China Energy Outlook 2060 (2024 Edition).

[xxv] Andrew Mills and Maha El Dahan, “QatarEnergy, China’s National Petroleum Corp to Sign 27-Year LNG Deal,” Reuters, June 20, 2023, https://www.reuters.com/business/energy/qatarenergy-chinas-national-petroleum-corp-sign-27-year-lng-deal-sources-2023-06-20/; Jason Xue, Dominique Patton, and Maha El Dahan, “Sinopec Signs New 27-Year LNG Supply Deal with QatarEnergy,” Reuters, November 5, 2023, https://www.reuters.com/business/energy/sinopec-says-signs-new-27-year-lng-supply-deal-with-qatarenergy-2023-11-04/; Andrew Mills and Maha El Dahan, “Qatar Seals 27-Year LNG Deal with China as Competition Heats Up,” Reuters, November 21, 2022, https://www.reuters.com/business/energy/qatarenergy-signs-27-year-lng-deal-with-chinas-sinopec-2022-11-21/.

[xxvi] Ministry of Foreign Affairs of the People’s Republic of China, “President Xi Jinping Chairs the Inaugural China-Central Asia Summit and Delivers a Keynote Speech,” May 19, 2023, https://www.mfa.gov.cn/eng/zxxx_662805/202305/t20230519_11080116.html.

[xxvii] “Major Russian Natural Gas Producer Set to Expand Business in China,” Global Times, February 7, 2024, https://www.globaltimes.cn/page/202402/1306886.shtml; “GT Voice: US Hegemony in LNG Calls for Higher Chinese Vigilance,” Global Times, January 3, 2024, https://www.globaltimes.cn/page/202401/1304747.shtml; Qi Zhiye and Fan Lijun, “Analysis of the Interest Considerations and Prospects of China-Mongolia-Russia Natural Gas Pipeline Cooperation in the Context of the Ukrainian Crisis” (乌克兰危机背景下中蒙俄天然气管道合作的利益考量及前景分析), Russia, Eastern European, and Central Asian Studies (俄罗斯东欧中亚研究), No. 1 (2023), https://www.essra.org.cn/view-1000-5040.aspx.

[xxviii] For the argument that a deterioration of China’s relationship with the West would mean China has less to lose and more to gain from closer energy ties to Russia, see Henrik Wachtmeister, “Russia-China Energy Relations since 24 February: Consequences and Options for Europe,” Swedish National China Centre and Stockholm Centre for Eastern European Studies, June 1, 2023, pp. 35-37, https://www.ui.se/globalassets/ui.se-eng/publications/sceeus/russia-china-energy-relations-since-24-february.pdf.

[xxix] Based on S&P Global Commodity Insights, Global LNG Balances (April 7, 2024).

[xxx] Mrinmay Dey, “Russia’s Planned Gas Pipeline to China Faces Construction Delay, Financial Times Reports,” Reuters, January 28, 2024, https://www.reuters.com/markets/commodities/russias-planned-gas-pipeline-china-faces-construction-delay-ft-2024-01-28/.

[xxxi] Authors’ estimate based on S&P Global Commodity Insights and recent company announcements.

[xxxii] See, e.g.: Shell, “LNG Outlook 2024,” February 2024, https://www.shell.com/what-we-do/oil-and-natural-gas/liquefied-natural-gas-lng/lng-outlook-2024.html.

[xxxiii] “Russia’s Share on LNG Market to Rise to 20% by 2030 from Current 8% — Novak,” Tass, November 22, 2023, https://tass.com/economy/1710029.

[xxxiv] Anne-Sophie Corbeau and Tatiana Mitrova, “Russia’s Gas Export Strategy: Adapting to the New Reality,” Center on Global Energy Policy, February 21, 2024, https://www.energypolicy.columbia.edu/publications/russias-gas-export-strategy-adapting-to-the-new-reality/.

[xxxv] Cindy Liang, Melody Li, and Eric Yep, “Chinese Energy Companies to Consolidate Gas/LNG Trading, Supply Chains in 2024,” S&P Global Commodity Insights, January 18, 2024, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/011824-chinese-energy-companies-to-consolidate-gaslng-trading-supply-chains-in-2024; Chen Aizhu, “China’s Incumbent and Upcoming LNG Traders,” Reuters, August 21, 2023, https://www.reuters.com/business/chinas-incumbent-upcoming-lng-traders-2023-08-21/.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

The Trump administration and Saudi leadership have reportedly agreed to a nuclear agreement that could enable US nuclear technology transfers to Saudi Arabia.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Full report

Commentary by Erica Downs, Akos Losz & Tatiana Mitrova • May 15, 2024