Trump says ongoing talks are Iran’s ‘last chance’

Karen Young, senior research scholar at the Centre on Global Energy Policy at Columbia University, joins BNN Bloomberg to discuss the energy sector.

Get the latest as our experts share their insights on global energy policy.

The economic and humanitarian consequences of the June 24 twin earthquakes in Venezuela continue to emerge.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Over the past five months, the Strait of Hormuz has been closed for extended stretches of time, disrupting roughly 10 to 15 million barrels of oil supply each...

Find out more about our upcoming and past events.

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Commentary by Ira Joseph & Diego Rivera Rivota • October 24, 2023

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

Mexico is among the largest natural gas importers in the world. But within this group it stands apart for meeting most of its natural gas demand (69 percent in 2022[1]) through a single source: piped gas from the United States. Mexico’s reliance on US gas has grown steadily over the past decade. Today, some 6–7 billion cubic feet per day (Bcf/d) of gas (62–72 billion cubic meters per year) flows across the border.[2] As Mexico attempts to boost its economy and shore up its power sector, as well as build out its LNG export capacity based on US gas production growth, this reliance will likely grow stronger in the years ahead.

Two key assumptions have underlined this relationship: low prices (around $3 per million British thermal units [MMBtu]) and an abundance of volumes with elastic room for supply growth. Though tempestuous political relations between Mexico and the United States, particularly around immigration, narcotics, and trade, have so far left those assumptions unscathed, that reality is subject to change. This commentary explores how US natural gas exports to Mexico could turn into more of a focal point in bilateral relationships between the two countries as US gas supply becomes more limited and potentially more commercially expensive as early as 2030. It also analyzes how high reliance on natural gas within the power mix, elevated dependence on Texas-produced natural gas, a wave of proposed projects to re-export gas imports in the form of LNG, and limited storage capacity in Mexico could further weaken the country’s energy security and delay its clean energy transition.

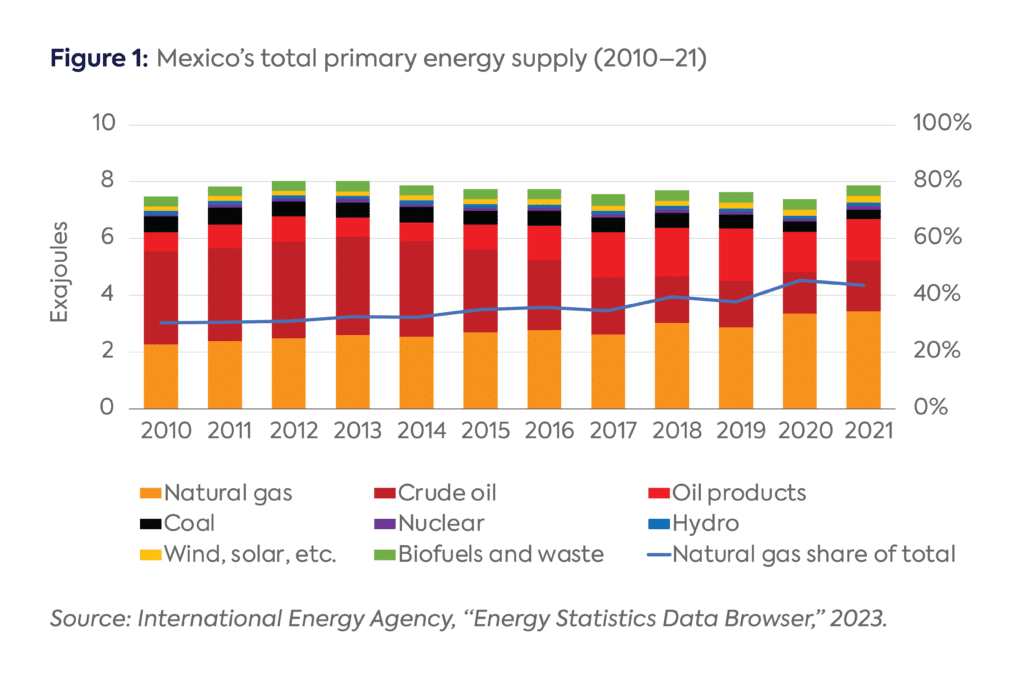

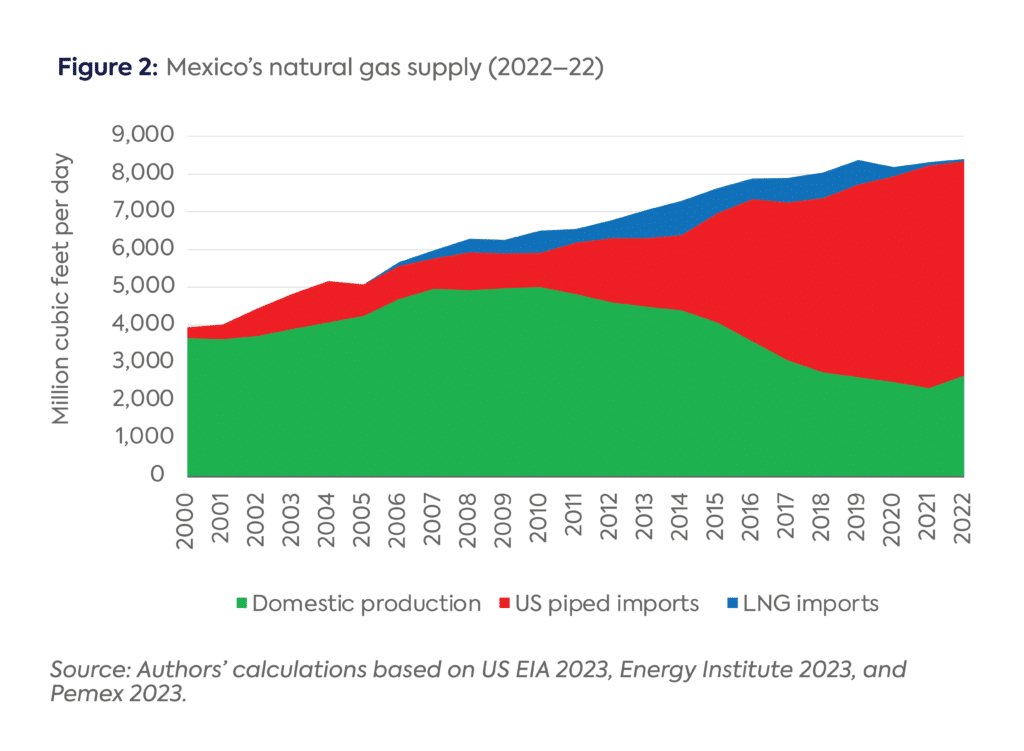

Natural gas was Mexico’s most-consumed energy source in 2022, accounting for 44 percent of total primary energy demand (Figure 1).[3] While Mexico is the world’s 11th-largest crude oil producer and 12th-largest crude oil exporter,[4] it is not among the world’s top 20 natural gas producers, and its natural gas production has declined by 47 percent since it peaked in 2010.[5] The country’s current production levels are nowhere near sufficient to meet its increasing domestic need.[6] In 2022, gas demand in Mexico reached 8,397 million cubic feet per day (MMcf/d), of which only 32 percent was met with domestic production.[7] The remainder of that demand was met with imports comprised almost exclusively (99 percent) of piped gas from the US.[8]

Mexico had been natural gas self-sufficient until the turn of the 21st century, when demand started increasing at a faster pace than what Mexico’s national oil company, Petróleos Mexicanos (Pemex), could produce. Pemex, which enjoyed a monopoly on oil and gas production until 2013,[9] reached peak dry natural gas production in 2011 at 5,004 MMcf/d.[10] From that point, Mexican domestic natural gas output entered a steady decline, falling by 47 percent to only 2,661 MMcf/d in 2022 (Figure 2).[11] Based on Mexico’s limited gas reserves of around 30 Bcf and Pemex’s challenging financial situation (among other factors), Mexico’s National Hydrocarbon Commission expects stagnant production to persist through 2028.[12] Output in that year would be able to meet the equivalent of 40 percent of today’s gas demand at best.[13]

Theoretically, domestic production is enough to cover around 30 percent of Mexico’s dry gas demand. However, Pemex itself is an enormous consumer of natural gas, which it uses for its exploration and production activities, refineries, gas processing centers, and petrochemical facilities. When consumption by Pemex’s own operations are excluded, domestic production accounts for less than 15 percent of available gas volumes in Mexico for power generation, industry, and other end-uses.[14] This figure would be higher if not for inefficient processes in Mexico’s oil and gas industry, which wastes around 10 percent of Mexico’s total natural gas production through flaring or, worse, venting into the atmosphere,[15] but it highlights just how insufficient domestic production in Mexico has become.

In contrast, Mexican gas demand has seen strong growth, nearly doubling over the past two decades and increasing from 6.5 Bcf/d to 8.4 Bcf/d between 2010 and 2022.[16] This growth has mainly been driven by the power sector, where electricity demand has almost doubled and an oil-to-gas fuel switch occurred in the power mix.[17] Although the pace of growth over the past 5 years was slower than before due to a range of factors (e.g., solar and wind capacity additions in the power sector meeting most of the incremental demand, slower declines and an uptick in domestic production in 2022, and muted demand growth in the industrial sector), and demand actually declined in 2020 due to Covid restrictions, demand levels in 2022 surpassed those just prior to the pandemic and monthly data indicates even higher demand in 2023.[18]

At first, Mexico tried to balance the supply gap by importing liquefied natural gas (LNG). Toward that end, it built three receiving terminals across both coasts starting in 2006.[19] These would not be enough, however, in light of a 47 percent decrease in domestic production between 2010 and 2022.[20] In the interim, innovations in horizontal drilling and hydraulic fracturing led to the boom in oil and gas production in the US known as the “shale revolution,” which transformed global oil and gas markets. Once it became clear that abundant volumes of natural gas at a low price were available only a few hundred kilometers north of several Mexican demand centers, Mexico bet on meeting demand growth through incremental pipeline imports from the US, and specifically Texas.

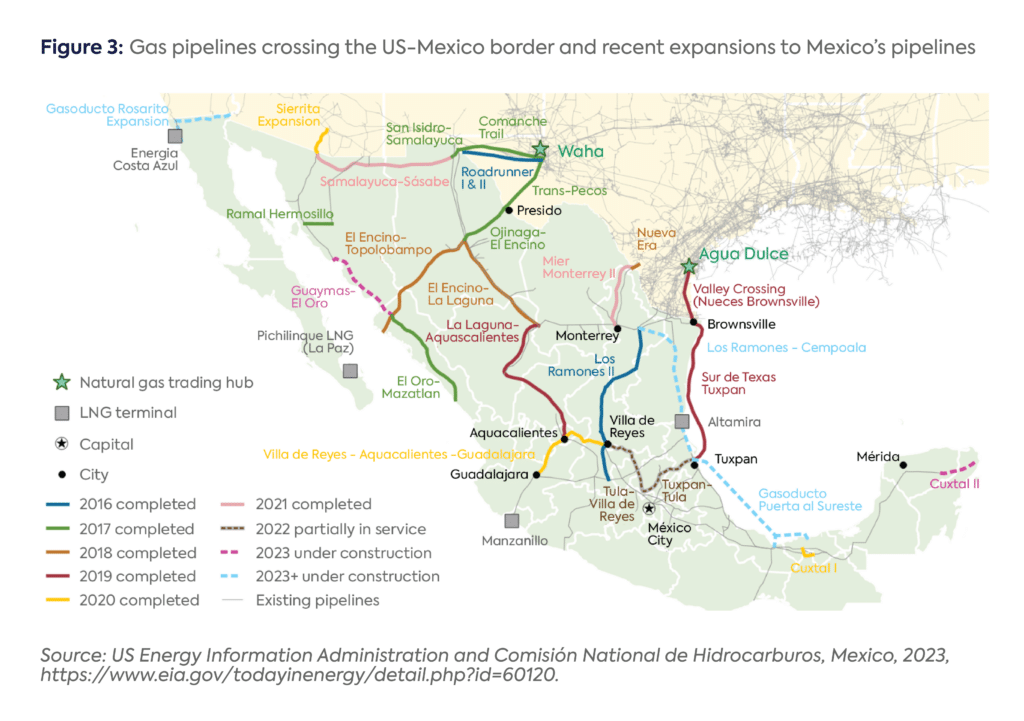

By 2010, however, it was clear that Mexico’s pipeline infrastructure was insufficient to import incremental volumes, so it launched an ambitious project to expand pipeline capacity through the two state-owned energy companies, Pemex and Comisión Federal de Electricidad (CFE). A network of over 25 gas pipelines were built through long-term transport contracts awarded by Pemex or CFE to companies such as TC Energy, Sempra, and Esentia Energy Systems (Figure 3).[21] Most of these projects were intended to move gas from Texas to newly built or refurbished combined-cycle power plants, acting as offtakers of that demand. The pipelines increased both import capacity (from 2.76 Bcf/d in 2012 to over 11 Bcf/d in 2020) and access to the gas-abundant Permian and Eagle Ford shale basins.[22] In this way, Mexico’s gas-thirsty and growing electric and industrial demand came to be met with Texan-produced natural gas. Thus far, only up to 7.4 Bcf/d of this cross-border capacity has been used due to numerous factors, including midstream constraints on the Mexican side of the border.[23] While those volumes have been plentiful and inexpensive (on average below $5/MMBtu),[24] they have also rendered Mexico’s energy system increasingly reliant on Texas’s natural gas production dynamics.[25]

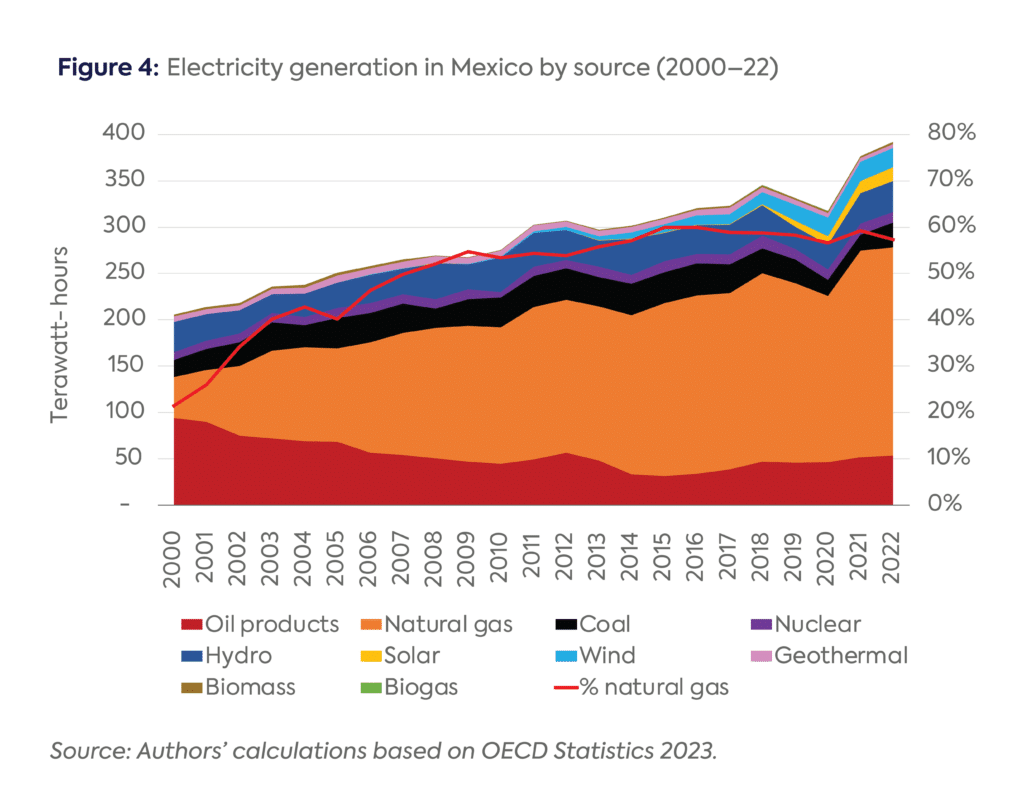

Today, US natural gas imports are critical to Mexico’s energy system. Most volumes go to combined-cycle power plants and other less modern natural-gas-fueled plants, which account for 63 percent of the electricity generated in Mexico in 2022 (Figure 4).[26]

However, natural gas is also a key fuel in the Mexican industrial sector, where it accounts for 33 percent of demand.[27] In the medium term, some industries may speed up and expand the electrification of their processes as they seek to lower their carbon emissions, but energy-intensive sectors, including cement, iron, and steel production, will be harder to decarbonize.

Given low-cost gas imports, severe congestion in Mexico’s electricity transmission network, and a lack of substantial renewable capacity in the works, natural gas demand in Mexico is set to grow over this decade, absent a major policy shift. Peaking before 2030 seems unlikely unless US gas prices were to spike. Indicatively, state-owned utility CFE reported that it is currently building 12 gas-fired plants, accounting for 6.9 gigawatts (GW), though it remains unclear when these projects will become operational and, ultimately, how much additional gas they will require.[28] In contrast, new solar and wind project construction has stalled over the past five years, adding pressure to meet growing power generation demand with natural gas.[29] Mexico’s Ministry of Energy expects only 17 percent of capacity additions through 2026 (about 1.5 GW) to come from non-fossil fuel sources.[30]

That may change in 2024, when a new presidential administration will take over in Mexico. The country’s next leader has the opportunity to prioritize the development of renewable energy projects in attempting to cover incremental electricity demand growth, especially given that Mexico’s renewable resources remain largely untapped. Mexico’s national technical potential includes 24,918 GW of solar photovoltaics, 3,669 GW of wind, 2.5 GW of geothermal, and 1.2 GW of additional hydropower capacity; by comparison, today’s renewable installed capacity of all technologies stands at only 27 GW.[31]

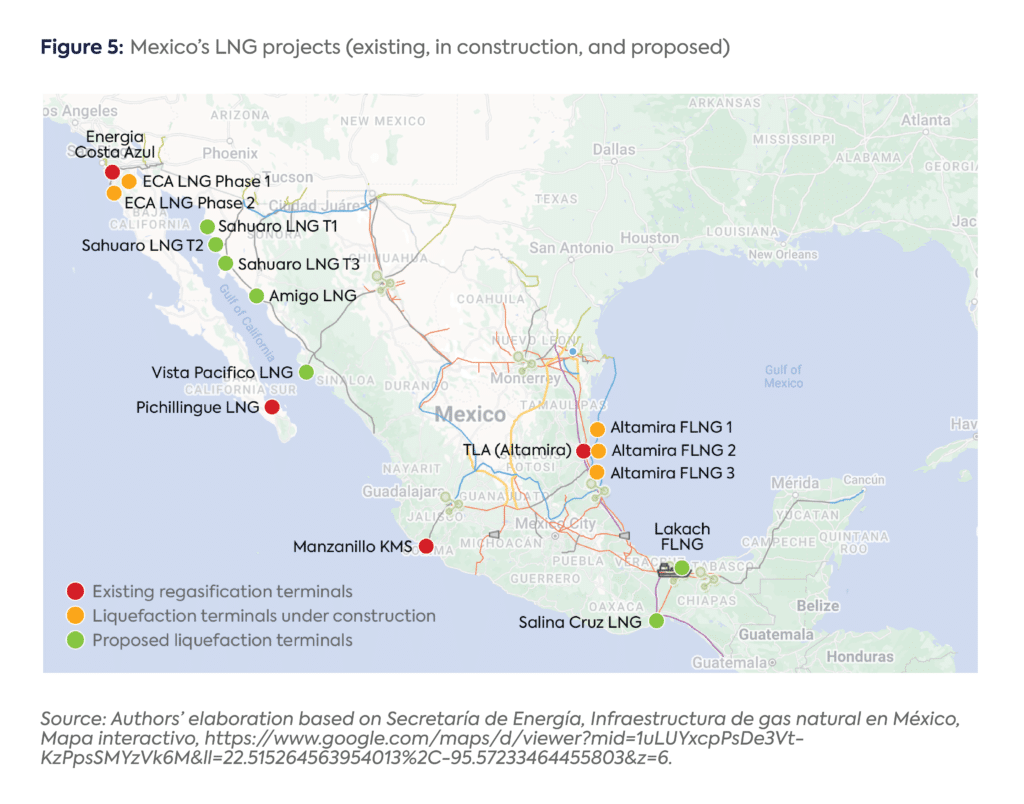

Despite a chronic shortage of gas for domestic use, 12 projects to re-export US-produced natural gas in the form of LNG from Mexico have been proposed, with a joint capacity of around 50 million tons per year (MTPA) (Figure 5). Most of these projects are unlikely to be built due to financial constraints, among other challenges—the proposals mirror the frenzy of LNG announcements that have occurred in the US over the past decade, of which only a fraction were or will be built.[32] Indeed, as of September 2023, only two projects (Sempra’s ECA LNG Phase 1 and New Fortress Energy’s Altamira FLNG 1) are under construction and none are operational.[33] A handful of projects have been announced to start construction in the coming months, including New Fortress Energy’s Altamira projects FLNG 2 and 3 as well as Mexico Pacific Limited’s Sahuaro LNG trains 1 and 2.[34] If these four projects move ahead, they will represent an installed liquefaction capacity of 17 MTPA, or about 2 Bcf/d.[35] Ultimately, though, any new projects that are completed will require incremental US gas supply for decades unless a major and unlikely turnaround occurs in Mexico’s upstream sector, further increasing demand for US piped gas imports as well as competition with domestic power generators, industrial users, and rival LNG export projects.[36]

Mexico’s increasing need for natural gas, paired with its already high dependance on a single import source, high reliance on the fuel in the power matrix, and extremely limited gas storage capacity,[37] could prove problematic for Mexico’s energy security. This point is borne out by several episodes in which US flows across the southern border were interrupted or significantly reduced: the 2000 California energy crisis[38] and Winter Storm Uri in Texas in February 2021.

Taking the latest example, Winter Storm Uri caused extreme weather conditions that led to a massive electricity generation failure in Texas, with outages of over 50 GW leaving 4.5 million homes without power and causing sizable human and material losses.[39] The power outages and low temperatures also affected natural gas production facilities and transmission infrastructure. On February 17, Texas governor Greg Abbott ordered natural gas producers “not to export product out of state until February 21st and instead sell it to providers within Texas.”[40] Natural gas flows to Mexico sharply decreased and prices rose by over $400/MMBtu.[41]

At the height of the crisis, between February 15 and 19, gas flows to Mexico dropped by around 90 percent to below 1 Bcf/d.[42] This translated to a total decline in February 2023 of 20 percent (1.2 Bcf/d) of the volumes imported the previous month.[43] The most-affected cross-border point in terms of volume was Rio Grande in South Texas, where the NET Mexico pipeline connects with the Los Ramones pipeline to feed two important Mexican industrial hubs, Monterrey and Bajío. Imports through this point, which normally make up about a quarter of Mexico’s imported gas, fell by 25 percent compared to the previous month.[44] However, flows from West Texas to Chihuahua were also severely affected: volumes through the Ojinaga-El Encino pipeline dropped by 37 percent in February compared to the previous month.[45] This reduction of natural gas flows was followed by power cuts, which initially hit the Mexican states of Sonora, Sinaloa, Chihuahua, Durango, Coahuila, and Nuevo León.[46] Eventually, power supply disruptions came to affect over 5 million users across 26 Mexican states.[47] This crisis was a tough and expensive lesson for Mexico’s government, energy companies, and household and energy consumers on the vulnerability embedded in near-exclusive dependence on Texan-produced natural gas. It also revealed how Mexico’s northern states of Chihuahua, Coahuila, Durango, and Nuevo León—and especially the power sector, which is highly dependent on gas-fired power plants—may be particularly vulnerable in the event of future supply disruptions.

Moreover, this high dependency on US gas production, which is on track to grow given Mexico’s rising domestic demand and imminent LNG exports, is rife with potential pitfalls. Countless scenarios could be created where either the US or Mexican government uses gas flows as a political weapon. Critically, the more US and Mexican gas markets lean on overseas LNG markets as a source of gas demand, the more upward pressure there will be on prices for Mexico, which must compete to attract supply.

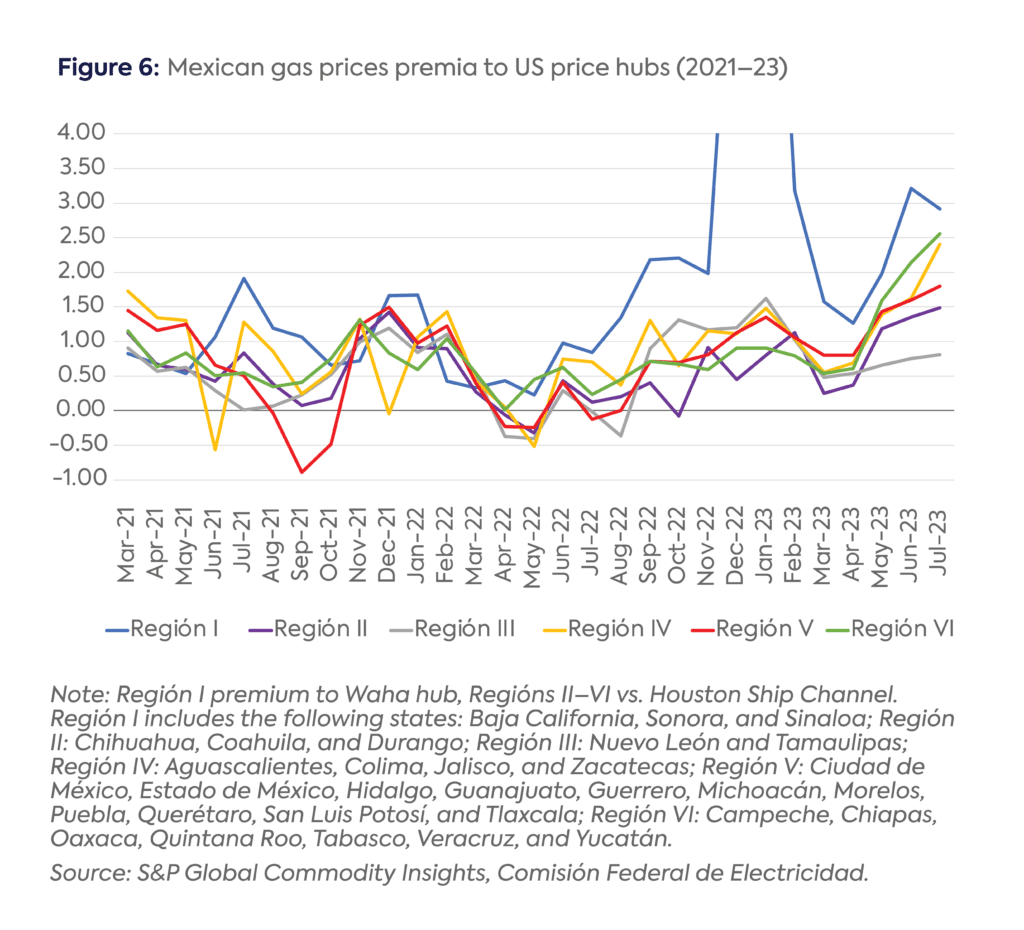

In any case, if US production growth lags and upward pressure emerges on US prices for a sustained period, both pipeline exports to Mexico and US LNG exports will be targeted. In pure commercial terms, the Mexican pipeline volumes for domestic use are likely most vulnerable to reduction, as the netbacks, or gross profit, on LNG sales from both the US and Mexico will be higher than sales to the domestic Mexican market. In other words, Mexican consumers, who typically buy gas on a spot or short-term basis, will need to be willing to pay the netback equivalent of Asian and European buyers to outbid the lifters of the LNG. Otherwise, the gas will flow to the LNG terminals ahead of other buyers in Mexico. History suggests that this figure will be higher. Netbacks on gas sales to Mexico are typically under $0.50/MMBtu, while LNG netbacks to Europe and Asia are significantly higher. Prior to the Russian invasion of Ukraine, US Gulf Coast netbacks ranged from $2–$10/MMBtu; since the invasion, they have been consistently above $5 (Figure 6).[48]

In the US, both sides of the aisle in Congress could begin to question why the US is even sending gas to Mexico. Gas trade could be rolled into countless economic or social divides ranging from immigration and sanctuary issues to free trade and the question of what best serves the economic interests of the US public, which is a key component for approving US LNG projects. Would Mexican LNG projects based on US gas meet the same criteria regarding export authorizations and the US public interest?[49] For several projects so far, the answer is “yes.” On the Mexican side, it may only be a matter of time before one or both of these same points on LNG exports are raised. In a scenario where US gas volumes are not as abundant and less affordable, how would Mexican consumers benefit from exporting LNG when they need the gas domestically? One alternative is that Mexican LNG becomes less competitive and shut in for periods of time. Would it be palatable to the Mexican government and Mexican consumers that US companies are profiting most from the export of LNG from Mexican ports? Even when the state utility CFE receives some of these profits, why would Mexican industry and consumers pay directly or indirectly for more expensive electricity and natural gas bills?

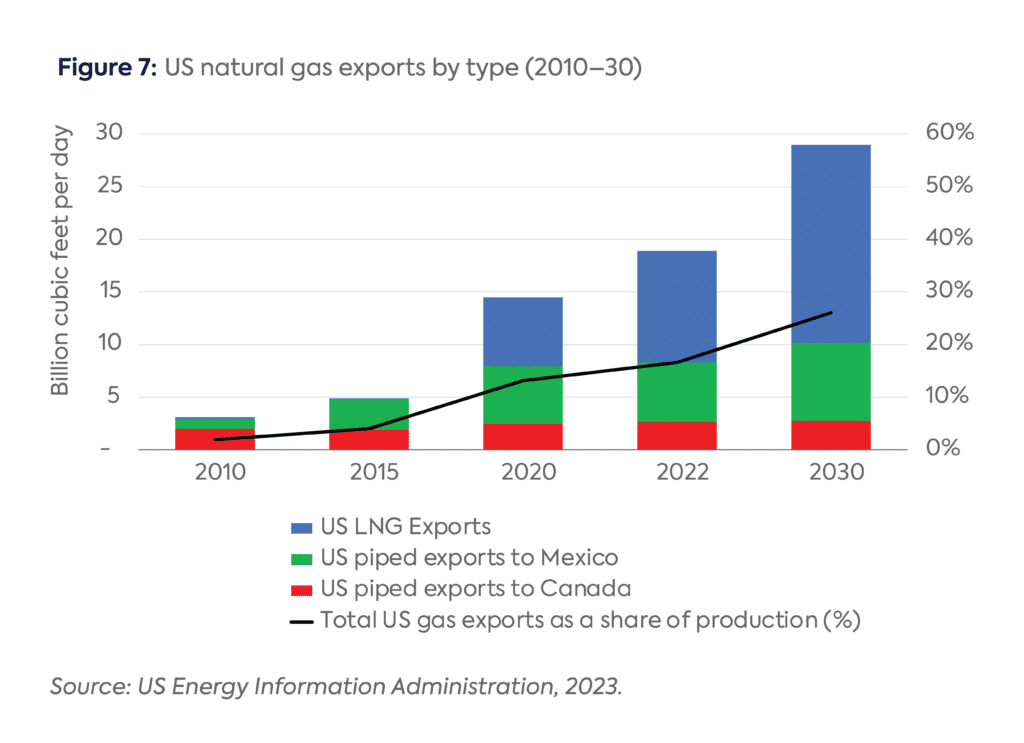

US natural gas production saw another record-high year in 2022, with LNG importers around the world, piped natural gas importers south of the Rio Grande, and consumers in the United States demanding higher volumes of natural gas in the first half of 2023. Gross US natural gas exports, including via LNG and piped exports to Mexico and Canada, accounted for almost 20 percent of the US total gas production, and that trend is projected to increase by 2030 (Figure 7).[50] In this context, US gas production will need to rise more to meet these demands; it sounds simple, but it is far from it. This could also mean higher natural gas prices for consumers on both sides of the border. If gas prices rise high enough in Mexico, alternatives—such as a more rapid uptake in renewables—will gain credibility, just as they did in Europe and China after Russia invaded Ukraine and cut its gas pipeline exports to Europe.

Policymakers on both sides of the border would benefit from assessing and planning long term on the role of natural gas in their energy transitions. This moment is a particularly timely opportunity to do so, as both countries prepare to hold presidential elections in 2024. While the world demands more LNG and Mexico more piped gas, consumers in the US may end up seeing gas prices go up if US gas production cannot keep pace. For Mexico, if the next administration will seek to mitigate this dependency, it will need to explore measures such as increasing storage and redundancy while diversifying power generation with solar- and wind-based electricity. Failing to do so will further weaken Mexico’s energy security and delay the clean energy transition, forcing end-consumers to pay, one way or the other, more money for more pollutant energy.

[1] Secretaría de Energía, “Prontuario estadístico de gas natural y petroquímicos Enero 2023,” 2023, https://datos.gob.mx/busca/dataset/prontuario-de-gas-natural-y-petroquimicos.

[2] US Energy Information Administration, “US Natural Gas Exports and Re-Exports by Country,” 2023, https://www.eia.gov/dnav/ng/ng_move_expc_s1_m.htm.

[3] International Energy Agency, “World Energy Balances 2022,” 2022, https://www.iea.org/data-and-statistics/data-product/world-energy-statistics-and-balances.

[4] Organization of the Petroleum Exporting Countries, “Annual Statistical Bulletin,” 2023, https://asb.opec.org/data/ASB_Data.php.

[5] Energy Institute, Statistical Review of World Energy, 2023, https://www.energyinst.org/statistical-review.

[6] Secretaría de Energía, “Prontuario estadístico de gas natural y petroquímicos Enero 2023,” 2023, https://datos.gob.mx/busca/dataset/prontuario-de-gas-natural-y-petroquimicos.

[7] Secretaría de Energía, Sistema de Información Energética, “Distribución de gas seco,” 2023, https://sie.energia.gob.mx/.

[8] Ibid.

[9] In 2013, the Mexican constitution was amended, followed by a series of legal reforms in 2014 that, among other measures, allowed access to private investment in the whole oil and gas value chain, as well as in the power sector. This upended Pemex’s monopoly in the oil and gas industry. In 2015, the first contracts to non-Pemex entities were awarded for oil and gas exploration areas. For more on the 2013 energy reform in Mexico, see: Secretaría de Energía, “Explicación ampliada de la Reforma Energética,” 2015, https://www.gob.mx/sener/documentos/explicacion-ampliada-de-la-reforma-energetica; and Duncan Wood, ed., Mexico’s New Energy Reform, Mexico Institute Woodrow Wilson International Center for Scholars, 2018, https://www.wilsoncenter.org/sites/default/files/media/documents/publication/mexicos_new_energy_reform.pdf.

[10] Secretaría de Energía, Sistema de Información Energética, “Distribución de gas seco,” 2023, https://sie.energia.gob.mx/.

[11] It is important to note, however, that 2022 was an exception to this, given that production actually grew by 15 percent compared to 2021, to 2,661 MMcf/d. This output is comparable to that seen in 2019. Pemex, “Base de datos Institucional, Balance de gas seco,” 2023, https://ebdi.pemex.com/bdi/bdiController.do?action=cuadro&cvecua=GBALGSE_G.

[12] Comisión Nacional de Hidrocarburos, “Prospectiva de Producción 2022–2028,” 2022, https://hidrocarburos.gob.mx/media/5452/reporte-prospectiva-3er-trim-2022.pdf.

[13] Ibid.

[14] Comisión Nacional de Hidrocarburos, “Balance de gas natural,” 2022, https://hidrocarburos.gob.mx/media/5651/balance_gas_natural_202209.pdf.

[15] World Bank, “Global Gas Flaring Reduction Partnership (GGFR),” https://www.worldbank.org/en/programs/gasflaringreduction/global-flaring-data/; and Pemex, “Quarterly Reports,” https://www.pemex.com/ri/finanzas/Paginas/resultados.aspx.

[16] Secretaría de Energía, Sistema de Información Energética, “Distribución de gas seco,” 2023, https://sie.energia.gob.mx/.

[17] Ibid; US Energy Information Administration, “US Natural Gas Exports and Re-Exports by Country,” 2023, https://www.eia.gov/dnav/ng/ng_move_expc_s1_m.htm.

[18] US Energy Information Administration, “US Natural Gas Exports and Re-Exports by Country,” 2023, https://www.eia.gov/dnav/ng/ng_move_expc_s1_m.htm.

[19] “Mexico’s LNG Terminals,” Mexico Business News, January 22, 2013, https://mexicobusiness.news/oilandgas/news/mexicos-lng-terminals.

[20] Secretaría de Energía, Sistema de Información Energética, “Producción de gas seco,” 2023, https://sie.energia.gob.mx/bdiController.do?action=cuadro&subAction=applyOptions.

[21] Secretaría de Energía, “Estatus de la infraestructura de gas natural,” 2019, https://www.gob.mx/cms/uploads/attachment/file/497827/Estatus_de_gasoductos_octubre_2019.pdf.

[22] Import capacity to Mexico has not been expanded significantly since 2020 to date. Secretaría de Energía, “Estatus de la infraestructura de gas natural,” 2019, https://www.gob.mx/cms/uploads/attachment/file/497827/Estatus_de_gasoductos_octubre_2019.pdf.

[23] S&P Global Commodity Insights, Regional Balances Reports, Cell Model History, US Totals

[24] S&P Global Commodity Insights, CFE, 2023. Region 1 and 2 premium to Waha Hub, Regions III-VI vs. Houston Ship Channel.

[25] Most imported gas from the US is priced based on a premium differential to either the Houston Ship Channel (HSC) or the Agua Dulce trading hub in the US. The assessed prices range from HSC plus X to HSC plus Y and largely reflect the tariffs on the Mexican gas grid. During non-extreme or exceptional periods like freeze-offs, Mexican prices range from a $0.90/MMBtu discount to Houston Ship Channel to a $3/MMBtu premium. Note that in CRE’s Region I and locations along the Wahalajara system, Waha hub prices tend to be the US price used for indexation, while import prices in Regions II through VI typically use Houston Ship Channel or Agua Dulce hub prices plus a premium. Region I includes the following states: Baja California, Sonora, and Sinaloa; Region II: Chihuahua, Coahuila, and Durango; Region III: Nuevo León and Tamaulipas; Region IV: Aguascalientes, Colima, Jalisco, and Zacatecas; Region V: Ciudad de México, Estado de México, Hidalgo, Guanajuato, Guerrero, Michoacán, Morelos, Puebla, Querétaro, San Luis Potosí, and Tlaxcala; Region VI: Campeche, Chiapas, Oaxaca, Quintana Roo, Tabasco, Veracruz, and Yucatán. Comisión Reguladora de Energía, “Índices de Referencia de Precios de Gas Natural al Mayoreo,” 2023, https://www.cre.gob.mx/IPGN/. The Wahalajara system refers to a set of pipelines that connect the Waha hub in West Texas with the city of Guadalajara in Mexico’s western state of Jalisco. The pipelines flow south from Texas to the Mexican states of Chihuahua, Durango, Coahuila, Zacatecas, Aguascalientes, and Jalisco.

[26] Centro Naciona de Control de Energía, “Energía Generada por Tipo de Tecnología,” 2023, https://www.cenace.gob.mx/Paginas/SIM/Reportes/EnergiaGeneradaTipoTec.aspx.

[27] Secretaría de Energía, Sistema de Información Energética, “Balance Nacional de Energía: Origen y destino de la energía,” https://sie.energia.gob.mx/bdiController.do?action=cuadro&subAction=applyOptions.

[28] Comisión Federal de Electricidad, “Informe Annual 2022,” 2023, https://www.cfe.mx/finanzas/reportes-financieros/Informe%20Anual%20Documentos/Informe%20Anual%20Portal.pdf.

[29] The government’s pipeline of 8.6 GW “strategic projects” to be commissioned between 2023 and 2026 includes only 0.7 GW of solar PV projects and none of wind power. Wind power capacity grew by only 900 MW between 2019 and 2022. Moreover, while solar PV grew by almost 3 GW in the same period, almost all of these additions were delayed projects from three long-term power auctions that took place between 2015 and 2017. The current administration canceled an announced fourth auction in 2019 and has no plans to resume them. See: Secretaría de Energía, “Programa de Desarrollo del Sistema Eléctrico Nacional (PRODESEN) 2023–2027,” 2023, https://www.gob.mx/sener/articulos/programa-de-desarrollo-del-sistema-electrico-nacional-2023-2037.

[30] Ibid.

[31] Riccardo Bracho et al., “Mexico Clean Energy Report,” National Renewable Energy Lab, US Department of Energy, April 2022, https://doi.org/10.2172/1862951; World Bank, “Solar Photovoltaic Power Potential by Country,” July 2020, https://www.worldbank.org/en/topic/energy/publication/solar-photovoltaic-power-potential-by-country; and World Bank, “Global Wind Atlas,” 2023, https://globalwindatlas.info/en.

[32] Federal Energy Regulatory Commission, “North American LNG Export Terminals—Existing, Approved not Yet Built, and Proposed,” 2023, https://cms.ferc.gov/media/north-american-lng-export-terminals-existing-approved-not-yet-built-and-proposed-8; Corey Paul, “LNG Project Tracker: Contracting Surge Accelerates Next Cycle of Export Projects,” S&P Global Market Intelligence, 2023, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/lng-project-tracker-contracting-surge-accelerates-next-cycle-of-export-projects-70992920.

[33] Sempra, “First Quarter 2023 Earning Results,” 2023, https://investor.sempra.com/static-files/9aa519fe-717c-44c2-af99-3bd59387f5ee; New Fortress Energy, “Form 10-Q, Q2 2023,” 2023, https://ir.newfortressenergy.com/static-files/c2698c66-b347-4e6f-a614-a39121497b15.

[34] New Fortress Energy, “New Fortress Energy Announces Second Quarter 2023 Results,” 2023, https://ir.newfortressenergy.com/news-releases/news-release-details/new-fortress-energy-announces-second-quarter-2023-results; Mexico Pacific Limited, “Mexico Pacific Concludes Long-Term LNG Sales and Purchase Agreements Across Three Trains with ConocoPhillips,” 2023, https://mexicopacific.com/mexico-pacific-concludes-long-term-lng-sales-and-purchase-agreements-across-three-trains-with-conocophillips/.

[35] These volumes are equivalent to about a third of total gas imports from the US in 2022. Authors’ calculations based on company websites.

[36] A testament of this is that Mexico Pacific Limited announced the construction of a greenfield gas pipeline from West Texas to their LNG terminal in Puerto Libertad, Sonora, in Mexico’s northwest. This signals a potential bottleneck on the current gas pipeline infrastructure if demand in this region increases as other rival LNG exporting projects and new combined-cycle plants are fed via the same pipeline system.

[37] Mexico does not count with any underground natural gas storage facilities, with storage limited to tanks from the four existing LNG importing terminals, of which only two are connected to the main pipeline system (SISTRANGAS) and are equivalent to only two days of average consumption.

[38] For more on the California energy crisis, see: US

Energy Information Administration, “Subsequent Events California’s Energy Crisis,” https://www.eia.gov/electricity/policies/legislation/california/subsequentevents.html; and Jose Luis Calva and Germán Alarco, “Política energética,”Volume 8 of Agenda para el desarrollo:

Conocer para decidir, UNAM, 2007, 114.

[39] Carey W. King, Josh D. Rhodes, and Jay Zarnikau, “The Timeline and Events of the February 2021 Texas Electric Grid Blackouts,” The University of Texas at Austin Energy Institute, 2021, https://energy.utexas.edu/sites/default/files/UTAustin%20%282021%29%20EventsFebruary2021TexasBlackout%2020210714.pdf.

[40] Office of the Texas Governor, “Governor Abbott Gives Update on State Response to Severe Winter Weather, Power Outages,” 2021, https://gov.texas.gov/news/post/governor-abbott-gives-update-on-state-response-to-severe-winter-weather-power-outages.

[41] Carey W. King, Josh D. Rhodes, and Jay Zarnikau, “The Timeline and Events of the February 2021 Texas Electric Grid Blackouts,” The University of Texas at Austin Energy Institute, 2021, https://energy.utexas.edu/sites/default/files/UTAustin%20%282021%29%20EventsFebruary2021TexasBlackout%2020210714.pdf.

[42] Ibid.

[43] US Energy Information Administration, “US Natural Gas Exports and Re-Exports by Point of Exit,” 2023, https://www.eia.gov/dnav/ng/ng_move_poe2_a_EPG0_ENP_Mmcf_a.htm.

[44] Ibid.

[45] Ibid.

[46] Comisión Federal de Electricidad, “Interrupción del suministro de energía eléctrica por déficit de generación,” 2021, https://app.cfe.mx/Aplicaciones/OTROS/Boletines/boletin?i=2110.

[47] Ibid.

[48] S&P Global Commodity Insights, “Gas Daily Mexico Prices,” 2023.

[49] Ben Cahill and Sophie Coste, “Subtle Shift in U.S. LNG Export Authorizations,” Center for Strategic and International Studies, 2023, https://www.csis.org/analysis/subtle-shift-us-lng-export-authorizations.

[50] US Energy Information Administration, “Short-Term Energy Outlook,” 2022 https://www.eia.gov/outlooks/aeo/data/browser/#/?id=72-AEO2023&cases=ref2023&sid=ref2023-d020623a.23-1-AEO2023~ref2021-d113020a.10-76-AEO2021~ref2022-d011222a.10-76-AEO2022&sourcekey=0 and US Energy Information Administration, “Annual Energy Outlook AEO2023,” 2023, https://www.eia.gov/outlooks/aeo/.

CHRONIQUE. Les Etats-Unis vont bientôt contrôler environ un tiers des capacités mondiales de GNL, bien plus que le Qatar. Sous l’administration Trump, le GNL est devenu un outil de politique étrangère, écrit Anne-Sophie Corbeau, chercheuse au Center on Global Energy Policy de l’Université Columbia

The Iran crisis, whenever it ends, will materially change how the LNG market operates.

Full report

Commentary by Ira Joseph & Diego Rivera Rivota • October 24, 2023