Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

In a surprise announcement a day after April Fools’ Day, the Organization of the Petroleum Exporting Countries (OPEC) and 10 additional oil exporters (together known as OPEC+) pulled a prank of its own on the oil market. Eight OPEC+ members voluntarily announced reductions in their production targets totaling 1.16 million barrels per day (mb/d) from May 2023 until the end of the year. The stated motivation for this cut was a weak demand outlook amid the banking crisis in the United States and Europe, and slower than expected demand recovery in China. According to OPEC+, the goal is to make the market more stable.[1]

Unlike previous changes in production quotas, which were distributed among all or most of the members of the coalition, this announcement was limited to just eight countries. The cuts were announced a day before a scheduled meeting of the Joint Ministerial Monitoring Committee (JMMC), the apex OPEC+ body formally charged with deliberating and enforcing production quotas among the group members.[2] Thus, it would appear that the decision by these eight countries to cut production bypassed the formal consultation process situated in the JMMC, and the official April meeting ended up merely reporting and endorsing that decision. These production cuts are in addition to the announcement by the Russian deputy prime minister in February that Russia would curtail production by 500,000 barrels per day in March 2023.[3] Russia has now extended its March production cuts until the end of the year, coinciding with the announcement by eight other OPEC+ members.[4] Thus, a potential 1.66 mb/d of OPEC+ crude accounting for about 1.5 percent of the global supply could be off from the market from May 2023. This post unpacks this announcement and discusses its significance.

OPEC+ was already producing nearly 2 mb/d less than its target production due to numerous chronic underperformers.[5] Member countries in Africa and Central and Southeast Asia, in particular, have struggled to meet their production quotas, in some cases owing to structural oil sector decline after years of underinvestment. In fact, the coalition has not met its production targets even once since January 2021, when it started to unwind production cuts instituted in April 2020 in response to the collapse in oil consumption caused by the COVID-19 pandemic.[6]

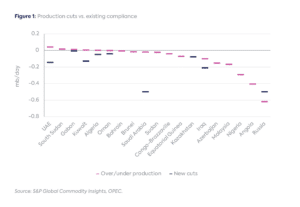

The importance of this announcement is that the production cuts it instituted apply to OPEC countries that were meeting or exceeding their targets, namely, the core Middle Eastern OPEC members of Iraq, Kuwait, Saudi Arabia, and the United Arab Emirates. These four countries alone will now account for nearly 1 mb/d of production cuts, implying a reduction in global oil supply by approximately 1 percent. (Figure 1).

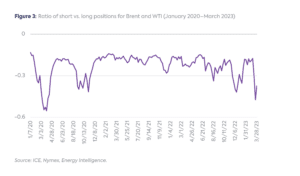

With its surprise announcement, OPEC+ proactively regained control over the oil market, establishing a firm floor for oil prices after a seasonally softer period for demand that led to limited fundamental support for prices. After markets opened on the following Monday, global oil prices jumped by 6 to 8 percent, and Brent rebased closer to $85/barrel (bbl) while WTI broke through $80/bbl. Having started the year strongly, Brent was averaging well over $80/bbl, with WTI close at $77.5/bbl. In the fortnight before the cuts, however, Brent prices had fallen into the $70s and, at the height of concerns about the banking and financial sector, threatened to fall to $70/bbl or below, while WTI was trading in the $66–$72/bbl range (Figure 2).

The authors have held the view for some time that OPEC+ would like to maintain prices in the $80/bbl range,[7] and this announcement achieved that objective. The average external breakeven price[8] for OPEC+ has been estimated at $82/bbl.[9] The International Monetary Fund estimates that the average fiscal breakeven oil price[10]for producers in the region is also in the $75/bbl range (excluding Iran, which has its own complications).[11] In addition, Russia clearly favors higher benchmark prices as it continues to face sizable discounts to sell its crude.[12] Thus, it is in the interest of all OPEC+ members that oil prices stay above $80/bbl.

Over the last few years, OPEC+ has been keenly following the trend of growing speculative positioning and options trading in the oil market. Options trading, combined with lower liquidity in oil markets, can lead to rapid downside moves in oil prices, as the market saw leading up to the surprise cuts. This type of activity has particularly irritated OPEC+ because it pushes prices below its desired levels and impacts member country revenues and budgets. Back in 2020, the Saudi Arabian energy minister, Prince Abdulaziz bin Salman, noted that traders betting on the oil market would be “ouching like hell.”[13]

The repeated narrative from the group, in particular Saudi Arabia, was that no changes to the existing production quotas were on the anvil.[14] By front-running its own JMMC, this announcement delivered on the promise to penalize any speculative activity and the rapid growth in short selling positions since early March. The ratio of speculative short to long positions had fallen to levels not seen since the market collapsed on the back of the pandemic in April 2020 (Figure 3). Given the duration of the voluntary cuts from May through potentially the end of the year (and into a potentially tight market), traders are likely to remain wary of shorting the market even in the face of macroeconomic uncertainties.

This new announcement of additional production cuts is yet another instance of the decoupling of the OPEC–US relationship. Group cohesion has been critical to the success of OPEC+ in maintaining its production quotas, and the coalition has prioritized maintaining internal consensus despite geopolitical challenges.[15] In particular, the Saudis have been arguing for a while now for the primacy of their national interests in their decision making.[16] This “Saudi First” doctrine has been central to their approach to the oil market and was evident in the strident defense of production cuts[17] announced in October 2022 despite a forceful US denunciation.[18] It also allows other OPEC members—including the Emiratis and Kuwaitis—to take the same approach, without having to be as overt as the Saudis have been.

With this new accountment, OPEC+ is effectively pulling approximately 3 mb/d of supply from the oil market when added to the existing shortfall in OPEC+ production relative to members’ allocated production quotas. Such a large withdrawal will lead to a tighter market for the rest of the year even if demand slips due to global macroeconomic and financial concerns or a slower than expected recovery in China. More importantly, speculators who were betting on oil prices falling will likely now end up supporting a rally by rushing to opt out of their short positions, affording OPEC+ a period of higher prices.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] https://www.opec.org/opec_web/en/press_room/7120.htm.

[2] https://www.opec.org/opec_web/en/press_room/4062.htm.

[4] http://government.ru/en/news/47756/.

[5] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/030923-opec-crude-oil-production-drops-in-february-despite-uptick-in-russia-platts-survey.

[6] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/110722-opec-boosts-output-by-220000-bd-as-some-members-recoup-recent-losses-platts-survey.

[7] https://www.energypolicy.columbia.edu/oil-markets-and-opec-in-2023/#_edn25.

[8] The external breakeven oil price is the oil price each country needs in order to pay for imports.

[9] https://www.energyintel.com/2022-10-11/break-even-price-outlook-october-2022-update.

[10] The fiscal breakeven oil price is the minimum price that the country needs in order to meet its expected government spending needs.

[11] https://data.imf.org/?sk=4CC54C86-F659-4B16-ABF5-FAB77D52D2E6&sId=1390030109571.

[12] https://www.reuters.com/markets/commodities/india-china-competition-opec-cuts-nudge-urals-above-price-cap-2023-04-05.

[13] https://www.reuters.com/article/us-oil-opec-saudi-price/saudi-energy-minister-promises-ouching-like-hell-for-oil-price-gamblers-idUSKBN2682V2.

[14] https://www.energyintel.com/00000186-e11b-d0fe-a7ae-e51ffa6a0000.

[15] https://www.energypolicy.columbia.edu/publications/assessing-opec-strategy-near-term/.

[16] https://www.spa.gov.sa/2334397.

[17] https://www.arabnews.com/node/2187791/business-economy.

[18] https://www.whitehouse.gov/briefing-room/statements-releases/2022/10/05/statement-from-national-security-advisor-jake-sullivan-and-nec-director-brian-deese/.

The US blockade of tankers serving Iran's oil exports is intended to cut Iranian oil exports to near-zero.

Iran has expanded its storage infrastructure over the past decade to levels that may be sufficient to handle up to two or three weeks of crude exports at pre-war levels.

The US-Israeli war against Iran highlights the Gulf’s dual role as the backbone of global energy supply and a major source of systemic risk.

The war in Iran has significantly enhanced Latin America's geopolitical advantage as a reliable source of hydrocarbon resources.

The White House declared last week that President Trump finally "broke OPEC" after the United Arab Emirates withdrew from the cartel.