Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Campus open to active affiliate Columbia University ID (CUID) holders and approved guests only.

Columbia students, faculty, and staff can use the guest registration portal to register up to two same-day guests. Alumni can use the portal to register for campus same-day access as well. Learn more below.

This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The Center on Global Energy Policy (CGEP) at Columbia University SIPA today announced new personnel additions who bring extensive experience from government and the private sector to the...

Announcement• July 3, 2025

Energy Explained

Get the latest as our experts share their insights on global energy policy.

The US Department of Defense has announced a multibillion-dollar public-private partnership with MP Materials, representing one of the most consequential federal efforts to build a secure, end-to-end domestic...

Artificial intelligence is transforming our world—and the energy sector. Earlier this year, the International Energy Agency (IEA) released a comprehensive report examining both AI’s projected energy demands and...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

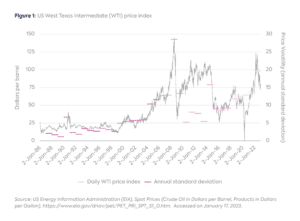

Oil markets faced near-unprecedented volatility in 2022. Although the year ended with crude prices roughly where they were at the beginning of the year, it also witnessed the US West Texas Intermediate (WTI) price benchmark rise to nearly $124 per barrel (b) and Brent crude to $133/b in March after the Russian invasion of Ukraine, before falling to $71/b of WTI and $76/b of Brent by December.[1] The largest-ever release[2] from the US Strategic Petroleum Reserve (SPR) as well as fears of slower recovery in oil demand from the lows of the pandemic and a deep and broad-based slowdown in global economic activity,[3] complicated the global oil market picture. Price volatility in 2022, as measured by annual standard deviation (Figure 1), was the second-highest on record after 2008, the year of the financial crisis.

As 2023 begins, it is an open question how all this volatility will shape oil markets over the next year, and how the Organization of the Petroleum Exporting Countries (OPEC) and 10 additional oil exporters (together known as OPEC+) will navigate the new market conditions, though recent developments may provide some important clues.

Supply Risks From Sanctions and Embargoes

The key variable that the market will be focused on in 2023 is the cadence for Russian supply of both oil and products. For the former, industry tracking pointed to a drop in exports from Russia after the price cap came into effect on December 5. But defying forecasts of a decline,[4] volumes have risen since the start of 2023. A general selloff in global crude prices, combined with persistently large discounts for Russian crude, has allowed sufficient volume to remain on the market, including some cargoes[5] that continue to use Western services remaining in compliance with the price cap. It is worth noting that Russian output consistently outperformed expectations last year since the conflict started despite occasional drops, and the reported decline in production remains just over 1 million b/d[6] as key buyers led by India, China, and Turkey[7] continue to support output and alternative markets for Russia such as Pakistan[8] continue to emerge.

Some increases in exports from Venezuela[9] with the temporary easing of sanctions[10] as well as from Iran[11], likely due to weaker implementation of sanctions, have also helped ease the market. That said, the prospects of higher production from these countries remain low. Although output elsewhere such as in North and Latin America as well as Norway[12] is gradually improving, the oil market will not enjoy the new US SPR releases that were critical to prices cooling off in 2022. Smaller mandated sales of 26 million barrels are still in the cards for 2023, but these, too, are currently under review along with potential buybacks to refill the SPR, further exacerbating uncertainty in the market.[13]

The lasting impact of all these moving parts on the supply side of the oil market is still not clear. The last month of 2022 alone saw the enactment of the EU embargo and the G7 price cap on Russian crude oil as well as the conclusion of the largest-ever US SPR allocation. Moreover, on February 5, the embargo and price cap on Russian refined products will start playing out. These recent developments only further complicate the reordering of trade flows.[14]

A Murky Outlook for Oil Demand

As 2023 gets underway, there remains considerable uncertainty around growth in oil consumption due to the still strong probability of a recession, especially in developed countries and China.[15] With forecasts suggesting that in 2023 these economies will grow by the slowest rate[16] since the financial crisis and the pandemic year of 2020, oil demand growth in developed countries represented by the Organisation for Economic Co-operation and Development (OECD) is far from certain. On the other hand, despite the conflict being centered in Europe and a sharp slowdown in GDP growth in Europe and the US, crude oil demand in the OECD has recovered strongly after the pandemic and remained robust throughout 2022.[17] Another macroeconomic indicator, inflation, is expected to ease in 2023 after hitting its highest level since 1999,[18] potentially providing additional upward support to demand in developed countries.

Globally, the largest source of weakness in oil demand has been China due to its zero-COVID strategy and a number of macroeconomic challenges. Now that the country has completely reversed its COVID restrictions,[19] it could see a recovery in demand. On the other hand, the Energy Intelligence Agency downgraded its demand forecasts for China by nearly 600,000 b/d in its Short-Term Oil Outlooks between January 2022 and January 2023. Growth in the rest of the non-OECD is also forecasted to be weaker by nearly 1 million b/d, signaling the uncertainty in this critical component of global demand growth.[20]

A key policy variable here is whether the Chinese government will continue to increase import quotas for its independent refineries, which have been the largest consumers of the growing volume of discounted Russian crude flowing to China. These companies are allocated fixed quotas of how much crude they can import, and China’s Ministry of Commerce has successively reduced these volumes for the last three years, causing a decline in their imports from 3.5 million b/d in 2020 to 3.3 million b/d in 2021.[21] In a reversal of this policy, the government has increased the quotas for 2023 by 1.3 percent even though the independents have yet to exhaust their 2022 allocations.[22] This move increases China’s ability to import higher volumes of discounted Russian crude in 2023.

OPEC+ in Wait and See Mode

Amid all the uncertainty of 2022, OPEC+ sought to dominate the oil market by attempting to control production among its members. By announcing an increase in its target production in both July and August 2022, then cutting back the increase in September,[23] and finally cutting the production target itself beginning in November 2022,[24] the coalition has attempted to signal that dominance. However, given that OPEC+ has been unable to meet its targets or in the case of most members their quotas, the impact of the group’s monthly announcements has been muted. At each of its monthly meetings, OPEC+ itself has cited macroeconomic uncertainty and the potential downside to demand forecasts as a factor influencing its strategy. More significantly, countries in the coalition benefit substantially from maintaining prices in the $80/b range and would work to maintain it.[25]

More broadly, the oil market remains in a wait and see mode in anticipation of supply shifts over the coming months, seasonal demand improvement, and a ramp up in Chinese and other sources of pent-up demand. A run in prices similar to last year is unlikely, but tightening balances could well be a feature, barring a major global economic shock. In the meantime, we expect OPEC+ to maintain its cuts at least until it has better clarity on supply variables, as signaled by the cancellation of the joint technical committee meeting ahead of the February OPEC+ meeting.[26]

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

China’s dependence on the energy supplies that move through the Strait of Hormuz makes it especially vulnerable to any possible closure of the waterway by Iran in retaliation for attacks by Israel and the United States.

The conflict between Iran, Israel, and now the United States has yet to disrupt energy supplies to global markets. However, the US decision to attack Iran's nuclear program...

Calls to "Drill, baby drill" are back with Donald Trump's return to the White House, and for US natural gas production, the catchphrase might also be a necessity over the next three years if demand for the fuel grows as steeply as expected.

Earlier this month, China convened its “two sessions”—the annual concurrent meetings of the National People’s Congress (NPC), China’s legislature, and the Chinese People’s Political Consultative Congress, a political advisor body.

CGEP recently hosted a private roundtable conducted on a not-for-attribution basis that focused on key geopolitical issues and oil markets in various hotspots, including the Middle East, Russia/Ukraine, China, and the Americas.