Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

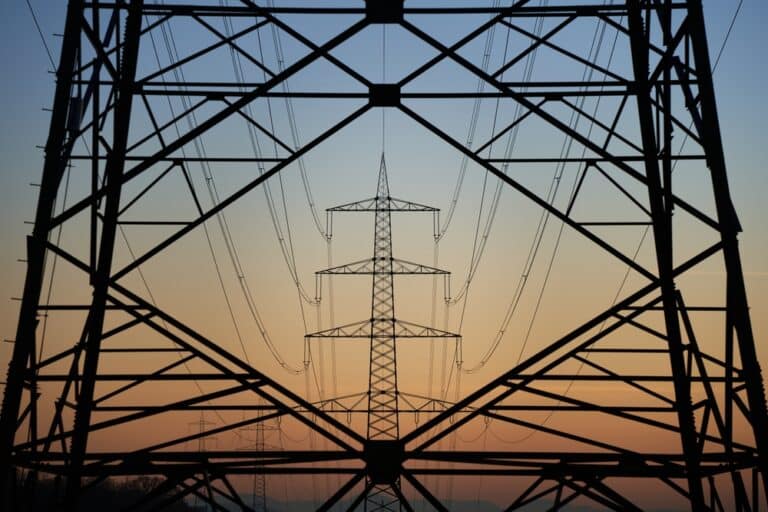

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Chief Energy Modeler, International Energy Agency

Laura Cozzi: Is AI alone a big issue? Of course. Yes it is because it is coming as a general purpose technology. We are seeing it as being the new electricity. What electricity has been in the 20th century, probably AI is going to be for the 21st century, but I think it’s important for the energy sector, the fact that this is coming in a situation that was already where we were having a lot of underinvestment, in particular in grids, and tension in parts of the supply chains.

Jason Bordoff: Artificial intelligence is transforming our world and the implications for the energy sector are profound. The International Energy Agency recently released a comprehensive report examining both AI’s projected energy demands and also how AI might reshape energy systems.

While headlines often raise alarms around electricity demand growth, the reality is more nuanced and more complex. Data centers currently account for just 1.5% of global electricity use, a number that’s expected to double by 2030, driven largely by the growth of AI. These facilities are often clustered together and connected to already congested grids. In some regions, particularly in the US, data centers could account for nearly half of all electricity demand growth in the coming years.

So how should we understand the relationship between AI and energy? What does this mean for power systems around the world? And is AI a friend or a foe to the clean energy transition?

This is Columbia Energy Exchange, a weekly podcast from the Center on Global Energy Policy at Columbia University. I’m Jason Bordoff. Today on the show, Laura Cozzi. Laura is the chief energy modeler at the International Energy Agency and its director of sustainability technology and outlooks. She oversees the IEA’s analytic work on energy, climate, and economic modeling, and she recently led the team that produced the agency’s report on artificial intelligence and energy.

Laura joined me to discuss the IEA’s findings on AI’s energy demands. We explored how renewable energy, efficiency gains in AI computing, and the potential for AI to optimize energy systems might help to accommodate load growth. We also touched on broader energy security considerations as countries navigate the energy transition. I hope you enjoy our conversation.

Laura Cozzi, thanks so much for joining us on Columbia Energy Exchange. Great to see you again and to be with you.

Laura Cozzi: Thanks to you, Jason, for having me.

Jason Bordoff: Well, thanks. There’s so much to talk to you about, but I wanted to use this opportunity to focus in particular on this new report—a very substantial 300-plus pages report coming out of the International Energy Agency on one of the questions that everyone is talking about these days, which is what AI, artificial intelligence, means for the energy sector and what energy will be needed to power AI. So sort of both of those things, but just for people who may not have read it yet, can you give our listeners a sense of what you believe the most important takeaways are? What did the IEA find in this conversation about artificial intelligence and energy?

Laura Cozzi: Thank you so much, Jason. And I know in your program you’ve already started discussing this quite a bit, and in fact, the reason why we decided here at the IEA to do this report is that over the past year or so, any energy conference has actually become an AI conference. So we felt that there was a need to actually go a bit more in-depth in understanding the real data behind it. We found that there was a lot of talk, but very little facts documenting what was really going on. So we spent over a year actually to produce this report that you mentioned—it’s going to be one of the installments on the work that we’re doing on energy and AI. And if I can summarize maybe the key findings, there are the following. After a very large review of the data, basically the share of AI in global electricity use today is only—if I may say—1.5%. However…

Jason Bordoff: And can I just pause there? When you say—help people understand when you have those estimates of electricity demand, I feel like the words AI and the words data centers get used interchangeably, but it’s not exactly the same thing.

Laura Cozzi: No, they’re very often conflated. The very reason is that you have data centers that are used for several things, including AI and increasingly used for AI. But data centers can be used for other digital applications, though increasingly they’re being used for AI. The reason why it’s very difficult to disentangle the two is that it depends very much on the use you do, but there are certain specific chips that are more and more dedicated very clearly to AI applications. So…

Jason Bordoff: And the 1.5% is data centers, to be correct.

Laura Cozzi: It’s data centers. Typically, a significant portion of it is believed to be AI. We cannot be absolutely 100% certain, but what we know is that increasingly the shipment of those chips are what are called accelerators and are increasingly really needed for AI. So the 1.5% today that we are expecting is actually going to grow significantly to around 3%. So we are expecting electricity demand related to data centers—and in particular the one related to data centers for AI—to grow much faster than the growth in global electricity demand. But at the global scale, the numbers are not very big. We are expecting other parts of the energy sector to require more electricity. In advanced economies, it’s, for example, EVs, electrification of heat, and others that are also taking an important part of the increasing electricity demand. In the emerging world, we are seeing needs for cooling and industry to be much larger.

Jason Bordoff: It’s going to grow to 3%—I think you just said a moment ago—by what year?

Laura Cozzi: Yes, to 2030. So we are expecting basically a doubling in terms of electricity use. And when you think about size, really it means that you’re adding the equivalent of one Japan in five years. In five years’ time.

Jason Bordoff: Is that a big number or a small number? One Japan in five years’ time—how should our listeners understand what that means?

Laura Cozzi: Listeners should understand that at the global level, this is a significant number but is not huge. The important thing to understand, however, is that data centers are very different from other types of electricity demand that we are currently used to integrating in electricity systems. And when I say that, the first thing that has to come to mind is that data centers are very concentrated loads. They tend to cluster together. So one data center typically in operation today at an upper scale today is around the equivalent of 100,000 households. The largest under construction is around 2 million households. The largest announced is around 5 million households. And what happens typically is that where you have one data center, then it’s very likely that you will have the next data centers in similar locations. So 50% of the load in the US today is concentrated in five places.

And if you look at the queues, it is concentrated in the same places, but it’s not only a US example—it’s very typical. Everywhere you get economies of scale, once you start building in one place, you tend to concentrate. So it’s concentrated, it’s very large. And third point, it is important and different from other large loads—it tends to be very close to cities, and this means that it’s going to be linked to grids that are most likely already congested. So this is why when we talk at the global scale, we are not really capturing the fact that in localized places, this is going to be—and is already and will be—very, very significant.

Jason Bordoff: So yeah, that’s helpful to sort of understand if this is a big deal or not. I feel like we read every day in the paper about another multi-billion dollar deal from major global infrastructure funds, major utilities acquiring natural gas assets, just scrambling for power. Where’s the power for AI going to come from? And then you read a report like this with numbers like 1.5% and you say, “What’s the big deal?” And so if I hear you correctly, just to clarify for our listeners, that might be right at a global level, but of course what matters is where the demand comes from. And so it sounds like in many parts of the world this is a small amount, maybe even a rounding error on the projections in electricity demand growth. But in certain areas, this is a very significant number, it’s a significant challenge, and it’s going to put a lot of strain on the ability to meet rising power demand. Is that the right way to think about it?

Laura Cozzi: Absolutely, Jason. I think you summarized it perfectly. We have basically surveyed all 11,000 data centers that are currently in operation in the world today. And I think the first thing to know is that basically 90% of them are concentrated first of all in the United States, second in China, and third in the European Union. And when you look even more in-depth, there are very few locations in which those data centers are actually built and operated, and this is where they need the power. So when you look at the pipeline of new projects for data centers and look at where they would like to be connected, what we find is that around one-fifth of those are in areas where either the grid is congested or the new pipeline of new power plants will not be enough to meet this demand. So it’s important that we start working very closely together—the IT sector and the energy sector—to ensure that the pipeline of projects for AI will have sufficient electricity to power those data centers.

Jason Bordoff: So let’s talk first about where that demand projection in the near term—I guess near to medium, but 2030, the next five years. You mentioned the EU, China, the US. Of course, China—there’s nothing new about rapidly rising power demand growth in a place like China. I think it has not been the case in the EU and the US for a long time in the US or the EU. Talk about how big these numbers are. How should we think about them? How big a challenge is it to meet it? Is it concentrated in certain states, certain regions much more than others? And then we can talk about what sources of power generation you think are going to ultimately meet this demand growth.

Laura Cozzi: So certainly today the United States is the leader in terms of data centers. And as you correctly said, basically we come out of a decade or so of very stagnant or modestly growing electricity demand. And what you’re expecting is actually that data centers will increase very strongly—account for over 40% of the new electricity demand in the United States in the next few years to 2030. And to give a sense of scale, the United States is one of the very few places in the world where even if you look countrywide, it does make a huge difference. So by 2030, we are expecting this electricity demand to be as large as all the industrial heavy industry needs. So in…

Jason Bordoff: In the US, you mean.

Laura Cozzi: In the US. So basically, in the next five years, what the US has built in terms of power demands for the industrial sector, for the heavy industry—for the iron and steel, cement, aluminum, etc.—we will need to produce in the next five years. So this is significant. It’s not something that is marginal. It’s changing the way electricity demand and production will be in the next few years in the US.

Jason Bordoff: And do you see that across the country or is that concentrated in certain areas?

Laura Cozzi: Data centers are very, very concentrated. So Virginia is clearly a case in point, but there are basically five clusters where we see the data centers being built. So important to say is this is significant, but at the same time, we’re seeing that speeding up building out—first and foremost—of the grid, the electricity grid. We think that all the data center demand for electricity can be delivered in the next few years. If I can just come back to the point you made because it’s very important for other advanced economies as well. While not being as significant in terms of size and in terms of percentage increase as for the US, what we’re seeing in the European Union—and in particular here I have in mind Ireland, I have in mind the Netherlands—and in Japan as well, is that we have been seeing really a decade of flat, really flat electricity demand.

And over the past two years, where the last two years where we’ve seen a big change in electricity need for data centers, is also the past two years in which for the first time after a decade of zero growth in electricity demand, we are seeing upticks in these other advanced economies. So in a way, the promise of electrification that we have been hearing for many, many years now is actually being materialized through AI and data centers. And as you said, very rightly so, no surprises at all to hear that China’s electricity demand is growing very strongly, and what’s happening in terms of AI is just a very small drop in the very big electrification which China has been undertaking over the past decade and will remain so in the next few years. So for China, it’s a very, very, very different perspective than in advanced economies.

Jason Bordoff: And you said of the growth in electricity demand in the US, AI and data centers through 2030, you expect to be around half of that growth. Is that right?

Laura Cozzi: Yeah, 45%. So yes, it is about half. Yeah.

Jason Bordoff: And I’ve seen estimates vary. I’ve seen 2% per year, 3% per year. There’s a lot of uncertainty about all of this. But just again for people listening, help them understand why that’s hard. Why is that a big number—2% to 3% per year growth? That sounds manageable, doesn’t sound like that big a number. It’s not 10% or 20% per year. Just help people understand why this is such a big thing that suddenly everyone’s talking about and everyone’s scrambling, and there’s a sense—the new president of the United States declared a national energy emergency on his first day in office, and for all the talk of “drill, baby, drill” and oil and gas, most of that executive order was about the power sector. So just help people understand what—you don’t have to call it an emergency or crisis—but what’s the challenge and why is it so significant?

Laura Cozzi: So I think we may take a step back to understand why this is so significant, and maybe we take a step back looking at the state of the electricity sector in the United States and in general. So we have been saying with a number of reports and been ringing an alarm bell vis-à-vis the state of electricity grids for some years now, even well before we have started seeing this increasing electricity demand coming from data centers and other loads. So what has been the situation on grids for the past several years is that in advanced economies in particular, the grid is quite outdated. And while we have been pushing in the grid a lot of variable renewables and new sources of generation that are very different from where they were in the past, the grid has not really been upgraded or extended to the extent that was needed.

So we are adding these important loads in many instances already in configurations where we have not been making the necessary investments to upgrade the grids. So I come back to the number that I was mentioning earlier—when we look at the queues for new data centers and we analyze—and really this is a very geographic-specific analysis—when we look at where the data centers demand is going to be coming and we look at whether the grid is congested or not or whether there is enough power or not, basically around one in five would require some kind of action. And what kind of action are we talking about here? It’s either accelerating and permitting new grid or speeding up the buildout of power plants. So I think it’s important to highlight why AI is important—it’s because not only is it large in size in itself, but it’s coming in a situation that was a bit frail already before.

So we had already—these systems were underinvested in, particularly the grids part, and in the past two years, in addition, we have seen that very essential parts of our electricity system like transformers and cables—the delivery time for those very essential elements that make the electricity grid work—are experiencing two important things. First, delays. So the delivery time of both transformers and cables have doubled over the past couple of years, and prices have gone up as a result because it’s a very, very tight market. So is AI alone a big issue? Of course, yes it is because it’s coming as probably a general purpose technology. We are seeing it as being the new electricity. What electricity has been in the 20th century, probably AI is going to be for the 21st century, but I think it’s important for the energy sector that this is coming in a situation that was already where we were having a lot of underinvestment, in particular in grids and tension in parts of the supply chains.

Jason Bordoff: This is slightly broader than AI, but just something I’m interested in—and as you know, I have written about with my friend Meghan O’Sullivan—after the energy crisis in Europe, exacerbated significantly by Russia’s weaponization of its dominant gas position and cutting off most gas supplies, there was a lot of talk about how electrification and moving away from volatile, geopolitically risky global oil and gas markets would increase energy security. And what I’m hearing you saying is a shift to electricity comes with a lot of risks of its own. You mentioned the transformers and the cables and all the equipment, and so I’m just wondering from an energy security standpoint—we obviously have decarbonization goals as well—how do you think about the energy security risks of the legacy more traditional fossil fuel system versus a more electrified system, which also can run on fossil fuels obviously, but how should we think about the reliability and security benefits or risks of much more electrification?

Laura Cozzi: Yeah, thank you, Jason. I think that this is an incredibly relevant question that here at the IEA we are spending quite a lot of time thinking about. As you very well know, the IEA was founded 51 years ago with the remit to look after energy security first and foremost, and a month ago—so it was in April—with the UK government, we hosted the Future of Energy Security Summit. It very much goes into what you’re asking now, and I think if we can summarize what were the findings and the key point of discussion there, I think there is the following. First, there are traditional energy security concerns that continue to be there. So oil security, natural gas security that you just mentioned continues to be there and will be with us even throughout the transition for many, many years to come. We need to continue to guard against those energy security risks.

However, at the same time, as we advance with energy transitions and countries decide to advance with energy transitions around the world, there are new security risks that we need to be very well aware and prepared to look for. First, the electricity part that you mentioned is becoming incredibly important. That clearly here—another bell was rung just last week with a major blackout in Spain and Portugal, with analysis that is being undertaken as we speak, but very clearly is front and center in everyone’s mind in Europe now. With that, I think that there are two other key components that are emerging. One is about critical minerals. The transition relies very strongly on certain minerals from lithium to rare earths that are incredibly concentrated—more concentrated even than oil and gas supplies. So a lot of work at the IEA and beyond in the United States, in Europe, in Japan, around the world is now really towards ensuring the critical mineral supplies.

And the third element is the technologies. So there are supply chains for clean energy technologies that also happen to be very concentrated. So a secure energy transition, a secure energy today and for the future needs an evolving—very much an evolving—definition that goes beyond the traditional parts and encompasses all. So looking at the evolving element—a key part here—but as our executive director would say, I think that there are a few watchwords that continue to be the same. Diversification being the first and foremost that is valid for everything, and we should really continue to work very strongly on the diversification element together with collaboration. That also came very, very strongly. This energy security summit where we had 60 countries coming, well beyond our normal IEA membership—we have around 30 countries—so twice as much, and really what we heard there is that the collaboration element has to be very, very critical as well.

Jason Bordoff: We should do a whole separate podcast on that because it’s really interesting. Coming back to AI and how significant this power demand growth is in countries like the US or many in the EU. And just explain to people listening why that is. You talked about the challenges in the grid that’s been there for a long time—it’s hard to build things. So we’re talking a lot about issues like permitting reform here, of course, and there’s backlogs for new gas turbines, and you kind of need power generation to be not too far from your house to deliver electricity there with some limitations, in latency and maybe a few thousand miles, it’s not that you can maybe put it anywhere, but the data centers I need for my ChatGPT search—they don’t have to be in the US. So is that correct? Talk about the locational issues and where the options are. Does this come from data privacy and security or national security concerns? Is it the preference of governments or the preference of the companies—the so-called hyperscalers? Why can’t we be putting these wherever it’s easy to build things and power—particularly low-carbon power—is really cheap?

Laura Cozzi: So I think you’re raising quite a few important things. First of all, let’s talk about the quality of power that is needed for these data centers. So those data centers require very high-quality power—what we would call really 24/7 extremely high-quality power where you don’t want to be disconnected because you would lose important output. So sometimes we hear about the possibility of having more flexible operations for those data centers, and it’s something that we find in the report—and talking to the industry—that is not being explored yet much at all. However, I think we need to keep in mind that the cost of load shedding for these data centers—we’re talking about something that is 10 times what it could be for an aluminum smelter. So it is very, very costly. So they require very high-quality power because losing this power would mean a lot of costs.

Now, the overall location issue is that up to now—and let’s not forget the AI revolution as we know it, so with the ChatGPT and the others, is relatively new—and up to now, the location has been decided really in terms of the clustering that we were mentioning before. I think it’s really very much now up for discussion that maybe the location consideration vis-à-vis where energy is high-quality, is low-carbon, and is affordable are coming more and more into the considerations of where do I build my next data center. This is shifting. We’ve been working now with the companies from the IT sector and energy sector for over a year now, and the discussion is really changing. There was first a discussion: “I want to build it there, you need to provide the power for that.” Now the discussion is shifting for a very simple reason.

If you look at how quickly you can build the data centers, you’re talking about, depending on the size, something between one to two years. If you’re talking about the grid expansion in advanced economies, you are talking about something between four to eight years, even once you have received the permitting. So there is really a big decoupling. So the two industries need to talk to each other in a much better way. You mentioned something else about what are the factors that actually determine where do I build my data center? And I think that the data privacy issue and national sovereignty issues are becoming very, very prevalent. So there is indeed in some countries in the world a very strong preference for building—to protect citizens and for broader national security considerations—to actually have the data center located where I will do my search. It’s very much reflecting the state of the world where we are in today—very fragmented—and it’s definitely a large part of the decision of where the data center is being located.

Jason Bordoff: And so many things I want to follow up on from what you just said. But you mentioned 90% of the growth for power for data centers is coming from the EU, China, the US. We just saw President Trump go to the Gulf Arab states, and part of the announcements there were significant deals for US chip companies and for data center plans that these very wealthy Gulf states have for AI and data centers. So does that come to the question I just asked? There are a lot of parts of the world with a lot of power generation capacity, there’s a lot of electricity potential in places like the Gulf, including a lot of money. Why wouldn’t we see this expand beyond the EU, China, and the US pretty quickly, especially if it’s so hard to meet that power demand in the US? Is that something that companies don’t want or is that something you think governments won’t allow?

Laura Cozzi: So absolutely. So I think that first of all, I think that one of the conclusions of the report is very, very clear—that in the race for AI, energy is going to be and will be an important factor in the decision where the next data centers will be decided. And I think the very recent deals in the Gulf with the Saudis, UAE, and beyond certainly go in that direction. I think there is also another important mismatch to be aware of today. Emerging economies are contributing around 50% of global internet traffic outside of China—I’m talking about here. But the location of data centers is just 10%. So there is already a mismatch between what is the current trend in terms of search and digital needs, but where the physical infrastructure is located. In certain cases, this is a reflection because of the fact that the grids in these places are not necessarily as reliable as data centers would need, or because there are many other competing needs that are considered more pressing for the population there. So there have been other considerations that have up to now contributed to this mismatch. But clearly, if you are in countries like in the Gulf where energy is abundant and capital is there, we are going to be seeing this being rectified. Yeah.

Jason Bordoff: And you talked about the need for high-quality power—99.99% reliability and so on. Does that mean renewables don’t really work to meet the rising power demand growth for data centers?

Laura Cozzi: This is certainly not what we find. So first of all, we have been working with all these major companies that are investing in AI today, and the large majority of them do care very much about emissions. And they do have in one way or another targets that are either for emission reductions or net-zero targets, and the PPAs—purchasing power agreements—that they have been doing and they are doing and they’re considering doing very much reflect this preference for low-carbon power. How is this being translated? In some cases, this low-carbon power is dispatchable. So we have been seeing investment, for example, in geothermal, interest in SMRs. We have seen a lot of investment in—tender investment in nuclear, conventional nuclear, but also SMRs. Having said all this, the largest part of the increase that we’re seeing from now to 2030 in terms of electricity supply is renewables—wind and solar backed by solar with batteries and complemented with the grid—being the largest, natural gas following, and then all other sources.

So we are seeing really a combination of a lot of sources, but renewables contributing the most. Now, going back to your question, “Do renewables work?” They do. We have done a lot of analysis of thousands of use cases with specific weather patterns analysis, the electricity demand profiles. And we see that in a lot of the cases where you need to supply the data centers, if you look at renewables and grids, you can get to very high levels of renewables. And here, I’m talking solar, solar-wind, batteries complemented by the grids. You can go up to 80%—very high levels—still having the system that for data centers working with the quality you need. And importantly, I think this is the interesting part: that the cost of this wouldn’t be very different from the PPAs that are being purchased now.

Jason Bordoff: But just to be clear, for that sort of high-quality, high-reliability power you’re talking about, it does require the grid for backup because while we have the ability to manage day-to-day intermittency, the few days a year—the extreme events, we all know the word “dunkelflaute” now—what happens when the wind and the sun all go away at the same time? You need the grid to handle that. Is that right?

Laura Cozzi: Absolutely, absolutely. And I think that we cannot think that data centers will be powered by on-site generation only. This is certainly not going to happen—it’s not the preference of the IT sector either. So the grid is to be certainly—they need to be going hand in hand, and the grid is going to be called upon in the X percent of cases of time in which there are certain weather conditions and load conditions. So this is not something that can happen completely off the grid. The grid is going to be—this is the first thing that we spoke about here—it’s going to be the essential piece that stitches it all together.

Jason Bordoff: And just to help people understand—this relates to the AI topic, but more broadly—when people are looking at things like levelized cost of electricity and how to understand the role renewables play in power, it does require then having grid capacity on standby, the ability to call on it when you need it. So when you look at the system cost for getting to those very high renewable penetration rates, you’re talking about as compared to—I don’t know—nuclear, geothermal, gas with CCS, other options, how does your analysis show we should think about that as a whole system?

Laura Cozzi: So currently, if you look at the solar generation per se, and if you look at LCOE—which I would argue is not necessarily the best metric that one should look at—it’s relatively cheap, but solar by itself wouldn’t be a good match for powering the 24/7 99.99% that we were mentioning earlier. So you need to start building the solar and then the batteries that go with it. But the analysis that we have done—we’re actually looking at exactly the cost you mentioned, not only looking at the LCOE but putting everything together. So you need to extend the grid, you need to make sure that the system continues to work. So there are upgrades, investments, there are modernization ones, there are extension ones, etc. And when you bring all of it together, the cheapest cost will be still for this incremental generation. The large part would still be renewables with batteries in the US—not everywhere, in the US—natural gas because it’s so cheap in the longer term, nuclear coming into the picture, some geothermal. So the simple answer to your question is the cheapest solution going forward is going to be a combination of all of the sources, expanding the grid. And in the short term, since the grid will take time to scale up, modernize, and roll out, a quick rollout of the renewables will help meet that generation gap.

Jason Bordoff: I was reading recently an op-ed from 1999, and the headline was something like “Dig More Coal, the PCs Are Coming.” And there were a lot of estimates in the late 1990s about how the internet was going to consume half of US electricity because people were just drawing exponential straight lines based on near-term trends when we needed all the power for the internet. And I’m just wondering if you could talk about that. That was true for crypto too, that crypto was going to consume as much electricity as—add up whichever countries you want to use as a benchmark. And neither of those happened. The technology gets more efficient, we become more productive, we learn how to use energy more efficiently. Energy per unit of GDP has been falling for a very long time even though total energy use obviously is going up. So I’m just wondering based on this analysis—this is all highly uncertain, of course—but do you think that’s a caution? Do you think there’s something different about AI? Do you think that maybe this is going to—we’re going to overbuild, that in fact all these estimates are going to prove exaggerated?

Laura Cozzi: Jason, I think that—so I love this 1999 article. I’d love to go and read it, but let me give you one number that for me is very much illuminating the point you just made. So when we started digging into the numbers and understanding, “Okay, this AI model, the searches, etc., how much do you need? How much energy do you need to train them? And then how much energy do you need to do the inference?” And there is this one number that really stuck with me, which is the following that is speaking to the efficiency gains of the digital sector and how incredible they are. If we had trained ChatGPT with the typical type of model that we had for AI compute and chips that we had 20 years ago, it would have taken the equivalent of the entire electricity demand of China to set up and train the model.

In reality, we estimate that that took a fraction of the demand to power the city of Paris. So we are talking about efficiency gains that are just stellar, and they are done in different parts of the system. First and foremost, it’s the chips—the chips year on year are becoming 50% more efficient. You are luminary on energy. I cannot think of another thing in the energy sector for which we can say that the technical efficiency improves year on year by 50%. It’s something that we just don’t see in the energy sector. It’s just something incredible. So just that portion in itself is something that is beyond what we normally see in the energy world. And then you have all the other parts that really—how much smarter these models and smarter, even more efficiently, smarter are these models becoming when they train themselves.

And then there are all the other parts of how do you actually do the setup of the data centers where you have the chips and how do you cool them? And this part is also becoming much more efficient. So when you come to the question “Is this uncertain?” This is hugely uncertain. So when we were talking with the chips providers, the IT sector, the digital sector, and we were telling them at the beginning of last year, “We would like to do projections for the next 5 to 10 years,” they were screaming. They were saying, “What are you talking about? We cannot project out for 5 years or 10 years. 10 years is impossible.” So what we have been doing is—I think that normally you would see projections out 2 to 3 years because this is where the shipment for chips that you can see are pretty reliable.

So it’s basically the time that you need to build those chips and then start shipping them. So what we have been doing is trying to be a bit humble as well. And we have a base scenario, but we have also explored uncertainties, and we have done quite a lot of work to understand what would be the key uncertainties. And in two words, basically there is a world in which AI thrives even more than in our base case where you see this incredible amount of trillions of dollars that we have already spoken about continue to go into the AI sector and data centers need even more energy. And so our base case is around 1,000 terawatt hours by 2030, and you would go up quite a few hundred more. But there are also cases, as you mentioned, and in fact we have two, in which you wouldn’t need around 1,000 terawatt hours, but you would need a bit less, and a bit less and “a bit less” is around 700.

So we go from 500 today in our low cases to 700 and in our base case to 1000. And maybe just two words about why do we think there could be lower demand but lower demand. You can think of difficulties for example in the energy sector that is not able to do the build out as we spoke about, but also more fragmentation in supply chains, more headwinds in terms of macroeconomic environment that would reduce the demand for the data centers. And another case is in the case in which actually efficiency and I go back to the 1990 article, go even much faster than we are anticipating today because you’re completely right. We cannot say that we have understood it all. It wouldn’t be fair.

Jason Bordoff: And look in the face of enormous uncertainty, this massive buildout probably makes sense. I would imagine for hyperscalers the risk of investing in the electricity that’s needed for leadership in AI. And there is a national security component here with competition with China, which is moving very fast. These are existential risks. The risk of overbuilding relative to the annual CapEx of these companies is probably a rounding error. So it’s a rational thing to do. And the flip side, the counter argument is maybe there is something different about AI. We’ve barely begun to scratch the surface for the use cases for this transformational technology and it’s probably going to impact every aspect of daily lives in ways we can’t even fathom yet. And so the use cases might go up exponentially in ways that we just haven’t seen in the past. But again, enormous uncertainty. Can you put all that in the context of the broader energy system? Again, we’ve been talking about a couple of countries, but I do think it’s helpful with all the talk of power for AI to just remind listeners on a global basis, this is dwarfed by things nobody ever thinks about air conditioning. Just help people understand again what the global picture looks like.

Laura Cozzi: Yeah, so I think air conditioning with the electricity demand for industries is actually the two largest drivers of global electricity demand growth over the next 5 to 10 years. And maybe a couple of numbers to give a sense of scale in the US in Japan, 9 out of 10 families own an air conditioner. But the moment you move to countries like India where most of the population growth is happening or even Africa, Nigeria, we are talking about 20 to 30% of the population that basically have access to air conditioning now wealth is growing. We have been seeing and experiencing in these parts of the world very dramatic heat waves over the past few years. So on the one hand, the ability to pay to buy the air conditioner is going up, but when we look at the data for air conditioning, sales is going even more than the increase in wealth simply because there is an expectation that the need for air conditioners is going to be even more and more.

So this for us is one of the, when we look at the numbers over the past couple of years has been one of the key reasons why their electricity demand has gone up. In fact, 20% of the global electricity demand growth last year was due to extreme weather events. And when we look at the demand across the entire energy sector was a bit larger than 20%. It was due to extreme weather events. And when we look at coal, all of the increase in coal use was related to high temperatures. So it was not necessarily the questions you raised, but I think it’s something that we sometimes of certainly for us is coming year after year is a surprise to the extent to which the very high temperatures are already impacting energy markets today and electricity for sure. So 20% alone last year was of the increasing electricity demand globally 20%, not one or 2%, 20% was extreme weather related.

Jason Bordoff: Yeah, just enormous numbers with a lot of challenges for many other parts of the world where data centers won’t be the primary driver. Look, we’ve talked a lot as many of these conversations do about energy that is needed for AI. We haven’t really talked yet about how AI can be an incredibly powerful tool to help better manage the energy sector to improve demand-side approaches, energy efficiency, potentially accelerate the deployment of clean energy in various ways. Talk about what your report shows AI can do for energy, not just what energy is needed for AI.

Laura Cozzi: Yeah, thank you very much Jason. Because I think that in the journey that we have had here at the IA over the past year of looking at this intersection of energy for AI and AI for energy, I think we spend 90% of the time on the first part and only a small fraction, 10% on the other. But this is also true for the energy sector. So when we look at the uptake of AI in the energy sector is very much what you were mentioning earlier. I think we haven’t really even started imagining all the possible use cases and how this could be transformative. So we are doing a couple of things. First of all in the report there is a collection of analysis that we have done sector by sector, but I would like to flag more importantly that we want to bring to the general public data as much as possible up to date and information that is unbiased.

So we will put in the IEA website in addition to what we have already now, all the data of AI of energy needed for AI, country by country, sector by sector, but all the use cases that hundreds of companies that we have surveyed and they were so kind to disclose as the use cases are telling us, look, today I am using AI for this reason and this is what the benefits are. Maybe I will give you two or three examples to make this a bit more concrete for our listeners as well. We spoke a lot about the grid. The grid in terms of grid being a bottleneck for electricity for AI. And actually we know of use cases of AI for the grid that could with exactly the same physical infrastructure enable this grid to actually carry more electrons. So our latest estimate is that the potential for this, which is called technically dynamic line rating, would basically enable the equivalent of what you’ve seen on average built in one year over the past five years of new grid being available at the very small fraction of the cost and much more quickly than the build infrastructure would be.

The important thing is that this dynamic line rating could be very, very localized in places where there is grid congestion. So you could deploy this dynamic line rating in areas where you have grid congestion and this would enable the same physical infrastructure to carry more electricity when it’s needed is one example.

Jason Bordoff: I’ve heard up to 30 or 40% more electricity numbers like that. I mean there are enormous numbers when you think of how difficult it is to build new transmission. Does that sound right?

Laura Cozzi: In certain areas it is up to that number. The figure that I gave you earlier, the equivalent of one year globally is the global number, but in certain cases, 30 to 40% is what some of the use cases that we will actually make available very soon are actually reporting back. So the numbers are just outstanding. It is really incredible. Now I wanted to give a completely different example, but

Jason Bordoff: Yeah, I was going to ask for one or two other specific examples because it’s interesting for people to get a sense tangibly of how AI might actually impact the way the energy system works.

Laura Cozzi: So other cases are more on the use of energy and in particular the way AI can help optimize traffic. So in the transport sector that as you know very well is one of the largest energy consumers today if you were to use this optimization through AI, especially for freight and trucks, would help produce costs for the freight companies. And our estimate would be that it would be like the equivalent in terms of energy use, we would be having to use less energy equivalent to taking away from streets a hundred million cars. So this is really a huge, huge number. So this is simply an optimization, an optimization for traffic use. Personally, the most exciting part is really related to innovation and next generation technologies. So far the energy sector has really just scratched the surface. When we look at how much venture capital, new money for innovative energy technologies have been attracting over the past couple of years, only 2% of those were mentioning AI in their scope of work.

If you look at life sciences and others, this percentage is much, much larger. So we are just at the very beginning. One example is the following. If you look at next generation solar, so perovskite, the type of materials that we have been exploring in laboratories is 0.01% of the overall possible chemistries and AI would be really the typical type of problem that AI could really help solve. Similar to what we have done with battery chemistries, et cetera. So I think the innovation space, on the innovation space, we are really just at the very, very beginning scratching the surface.

Jason Bordoff: So you talked about energy efficiency and demand side management and solar, and then earlier we were talking about this race for new natural gas supplies in the US and people have even talked about the need to keep coal online longer. So in your net assessment is AI a friend or a foe for the clean energy transition?

Laura Cozzi: So if you look at emissions, so we, even in the case where we have the highest uptake of AI, we would be talking about 500 million tons CO2 over a total that is well over 30 gigatons. So it’s one sector that is going to grow, but they growth in the overall energy sector is relatively modest. So it’s not that it’s not going to grow, it’s going to grow, but it’s relatively modest. Now, when we look at the potential of emission reduction, if there was to be a widespread uptake of existing use cases across the energy sector, we could reduce emission by several times more so as every technology is really not the technology is good or bad is the use we will make of it. That will determine in which direction this will go.

Jason Bordoff: Great. Well, as you said, this podcast focused on the general conversation, which is often how difficult this is going to be, how much power it needs, all the fossil fuels it’ll need. But I appreciate ending on an optimistic note that in fact this is a very powerful tool that can deliver a lot of benefits, including for the clean energy transition, but in other ways as well, especially at a moment when we’re focused more on energy security, affordability, reliability, and this is playing a much more dominant role in political, national security and other conversations. So it’s all early days still of course, and highly uncertain and dynamic and really grateful for all the work, Laura, you and your fantastic team at the IEA do to do analysis to help us understand all of this in a complex and dynamic and changing world. Thanks for making time to be with us to explain it this morning.

Laura Cozzi: Thank you very much to you, Jason, to you and your team. Thank you.

Jason Bordoff: Thank you again, Laura Cozzi, and thanks to all of you for listening to this week’s episode of Columbia Energy Exchange. The show is brought to you by the Center on Global Energy Policy at Columbia University. The show is hosted by me, Jason Bordoff and by Bill Loveless. The show is produced by Mary Catherine O’Connor. Additional support from Caroline Pitman, Kevin Brennan, Ashley Finan, and Kyu Lee. Gregory Vilfranc engineered the show. For more information about the podcast or the Center on Global Energy Policy, please visit us online at energypolicy.columbia.edu or follow us on social media @ColumbiaUEnergy. And please, if you feel inclined, give us a rating on Apple Podcasts. It really helps us out. Thanks again for listening. We’ll see you next week.

Artificial intelligence is transforming our world—and the energy sector. Earlier this year, the International Energy Agency (IEA) released a comprehensive report examining both AI’s projected energy demands and how it might reshape energy systems. But while headlines often raise alarms around electricity demand growth, the reality is more nuanced and complex.

While data centers currently account for just 1.5% of global electricity use, that share is expected to double by 2030, driven largely by the growth of AI. In some regions, particularly in the US, data centers could account for nearly half of all electricity demand growth in the coming years.

So how should we understand the relationship between AI and energy? What does this mean for power systems around the world? Is artificial intelligence a friend or foe to the clean energy transition?

This week, Jason Bordoff speaks with Laura Cozzi, about the IEA’s findings on AI’s energy demands.

Laura is the chief energy modeler at the International Energy Agency, and its director of sustainability, technology, and outlooks. She oversees the IEA’s analytical work on energy, climate, and economic modeling, and led the team that produced the agency’s report on artificial intelligence and energy.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Concerns about the affordability of electricity in the US have been rising along with prices. And while the headlines have pointed to AI and data centers as the...

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Yesterday, the US and Iran signed a memorandum of understanding starting the clock on a 60-day truce. The agreement intends to halt attacks, begin lifting the US naval...

Why the AI build-out was doomed from the start.

How to counter Beijing’s unauthorized "distillation."