This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

Over the past five months, the Strait of Hormuz has been closed for extended stretches of time, disrupting roughly 10 to 15 million barrels of oil supply each...

Join industry leaders, innovators, employers, and emerging talent for an evening exploring the technologies, trends, and career opportunities shaping the future of climate tech.

Event

• 31 W 52nd St, New York, NY 10019

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

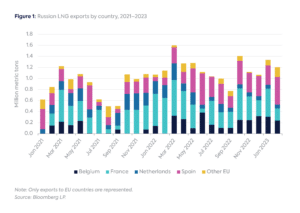

Entering spring 2023, European Union (EU) countries are looking at a more reassuring gas picture. The winter is almost over, significant flows of liquefied natural gas (LNG) are still coming to Europe, and most importantly, gas prices have dropped considerably from the highs of up to $100 per million British thermal units (mmBtu) in 2022 to around $13–15/mmBtu as of early April 2023.

While higher LNG imports helped EU countries compensate for lower Russian pipeline gas supplies in 2022, ironically, some of this LNG is Russian (Figure 1). EU countries—particularly Belgium, France, the Netherlands, and Spain—increased Russian LNG imports by around a third in 2022, to 19 billion cubic meters (bcm).[1]

With this as the backdrop, European politicians have started talking about restricting Russian LNG, proposing that EU governments should be able to temporarily limit upfront bidding for capacity for Russian LNG deliveries.[2] This move was preferred to sanctions, which require unanimity among EU countries. The United Kingdom and Lithuania stopped importing Russian LNG in 2022. Germany firmly declared that no Russian LNG would be regasified in its terminals.[3]

The EU seems on track to end its Russian gas dependency by 2027. Based on current flows, combined Russian pipeline gas and LNG in 2023 would be around 40 bcm per year (bcm/y), equivalent to around 25 percent of the levels in 2021 or 11 percent of estimated EU gas demand.[4]

The question is whether this trend of reducing dependence on Russian gas can be accelerated without hurting Europe. Fatih Birol, executive director of the International Energy Agency (IEA), recently noted that “we are not out of the woods yet” with gas markets still looking considerably tight in 2023. He warned that a combination of factors could tip the balance again toward high gas spot prices.[5]

Stopping Russian LNG imports could result in various outcomes for global gas markets, from relatively benign to potentially disruptive. These include:

Perfect swaps. The EU stops importing around 20 bcm/y of Russian LNG, which flows mostly to Asia. Quantities lost are systematically matched by other LNG suppliers. As Yamal LNG is closer to Europe than to Asia, this tightens the global shipping market during the winter season due to longer shipping routes to Asia when the northern route is unavailable. It also affects the transshipment of Russian LNG from nuclear icebreakers, which typically takes place in Belgium and France. The impact on gas prices is limited.

A not so perfect match. In this scenario, there is no perfect swap of LNG supplies. Additionally, China’s LNG appetite grows and Chinese companies compete with spot LNG going to Europe. Faced with lower LNG supplies, Europe is forced to weigh on demand while gas prices increase.

Russia retaliates. In 2022, Russian president Vladimir Putin did not hesitate to cut gas supplies. Retaliation in various forms could be in the cards again. A first obvious move could be to cut Russian pipeline gas volumes flowing through Ukraine[6] and then through TurkStream, removing around 20 bcm/y of pipeline gas. Whether or not Europe achieves the perfect swap (mentioned above) in terms of LNG supplies further impacts Europe’s gas balance. Any cut by Russia to its LNG supplies is a far more worrying move. Yamal volumes contracted by European companies (but not by China National Petroleum Corporation and Russia’s Novatek) could be cut by Russia shutting down one train (roughly 8.8 bcm/y). Russian LNG (45 bcm in 2022) is needed for the global gas balance, to avoid a return of sky-rocketing spot LNG prices.

Caution and Preparedness

Russia may very well decide to make a further cut in gas supplies to Europe, regardless of whether EU countries initiate any measures. The dilemma for European leaders is whether to preempt these potential cuts by restricting Russian gas flows. Preparedness is essential. This was certainly on European leaders’ minds as they decided to extend the 15 percent demand reduction (60 bcm) against a five-year average[7] for the period April 2023 to March 2024.[8] Faster deployment of renewables and heat pumps, along with continuous energy saving and efficiency measures, will play a role, but some parameters (weather, hydro levels, French nuclear generation) are beyond governments’ influence. Turning to supply, a critical consideration would be the success of the AggregateEU platform in securing additional gas supplies.[9]

Restricting Russian LNG imports would be an important political move. However, it could potentially result in higher gas spot prices that would particularly hurt Europe, where some member states are overly dependent on the spot LNG market, and other LNG importers relying on spot LNG cargoes. In contrast, the impact of proposed new restrictions on Russian revenues would be limited. Crucially, Yamal LNG’s exports are exempt from export duty and mineral extraction tax, unlike pipeline exports (however, LNG exporters pay a 34 percent profit tax).[10] Russia’s overall revenues from gas exports to Europe are expected to drop considerably in 2023, largely due to a combination of lower pipeline volumes and prices. Proceeding with caution will help EU countries ensure that the situation, in terms of gas demand restriction and supply diversification, is well in hand before moving to the next stage of independence from Russian gas.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[2] Kate Abnett, “EU Energy Chief Tells Companies Not to Sign New Russian LNG Deals,” Reuters, March 9, 2023, https://www.reuters.com/business/energy/eu-energy-chief-tells-companies-not-sign-new-russian-lng-deals-2023-03-09/; Siobhan Hall, “EU Ministers Back Option to Limit Russian Gas, LNG Bookings,” Montel, March 29, 2023, https://www.montelnews.com/news/1471353/eu-ministers-back-option-to-limit-russian-gas-lng-bookings. This measure would also target Russian pipeline gas.

[4] Based on Russian LNG imports in 2022 and pipeline flows for the period of January 1 to February 28, 2023; ENTSOG, Transparency Platform, accessed December 15, 2022.

[6] Naftogaz initiated an arbitration against Gazprom in September 2022, arguing that Gazprom did not pay for the gas transportation through Ukraine. Meanwhile Gazprom accused Naftogaz of rejecting transit via the Sokhranovka point with no appropriate reasons. See Reuters, “Russia’s Gazprom Rejects Ukraine’s Naftogaz Claims in Arbitration,” September 27, 2022, https://www.reuters.com/business/energy/russias-gazprom-rejects-ukraines-naftogaz-claims-arbitration-2022-09-27/.

[7] The five-year average is based on a reference period from April 1, 2017, to March 31, 2022.

[8] European Commission, “Proposal for a Council Regulation, Amending Regulation (EU) 2022/1369 as Regards Prolonging the Demand Reduction Period for Reduction Measures for Gas and Reinforcing the Reporting and Monitoring of their Implementation,” March 20, 2023, https://energy.ec.europa.eu/system/files/2023-03/COM_2023_174_1_EN_ACT_part1_v5.pdf.

[10] Russian pipeline gas is controlled by Gazprom. Gazprom pays a 30 percent export duty, mineral extraction tax, income tax, and dividends to the Russian state. LNG supplies reaching Europe come mostly from the Yamal LNG project, which is owned by Novatek, CNPC, TotalEnergies, and the Silk Road Fund. CNPC, Naturgy, Novatek, and TotalEnergies have long-term LNG contracts. Yamal LNG exports are exempt from export duty and Mineral Extraction Tax for 9 years, but LNG exporters pay a 34 percent profit tax. See Novatek, “Intergovernmental Agreement Regarding Cooperation on the Yamal LNG Project Enacted,” March 9, 2014, https://www.novatek.ru/en/business/yamal-lng/yamal_press_release/?id_4=860; International Group of Liquified National Gas Importers (GIIGNL), “Annual Report,” May 2022, https://giignl.org/wp-content/uploads/2022/05/GIIGNL2022_Annual_Report_May24.pdf; Vladimir Afanasiev, “Russian Tax Overhaul Seeks to Offset Drop in Revenues from Oil Companies,” Upstream Online, February 24, 2023, https://www.upstreamonline.com/focus/russian-tax-overhaul-seeks-to-offset-drop-in-revenue-from-oil-companies/2-1-1402417.

The Trump administration and Saudi leadership have reportedly agreed to a nuclear agreement that could enable US nuclear technology transfers to Saudi Arabia.

El Consejo Mexicano de Asuntos Internacionales (COMEXI) y la Unidad de Estudio y Reflexión sobre Energía y Sustentabilidad, presentan el análisis: “Posición en materia de energía y sustentabilidad en la revisión del T-MEC" El documento analiza cómo México puede aprovechar este proceso para fortalecer la integración energética de América del