This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This transcript has been automatically generatedSubscribe to âShift Keyâ and find this episode on Apple Podcasts, Spotify, Amazon, or wherever you get your podcasts.You can also add the showâs RSS feed to your podcast app to follow us directly.Robinson Meyer:Hello, it is Monday, July 6, and a year h...

Concerns about the affordability of electricity in the US have been rising along with prices. And while the headlines have pointed to AI and data centers as the...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Three CGEP scholars weigh in on the consequences of the Biden administration’s decision to pause pending approvals of liquefied natural gas (LNG) exports from the US to non-free trade agreement countries.[1]Anne-Sophie Corbeau looks at the pause in the context of the broader LNG market. Ira Joseph takes on its significance for the projects themselves and their relation to the US gas market, and Akos Losz looks at the longer term implications for the global gas market and US climate policy.

Anne-Sophie Corbeau

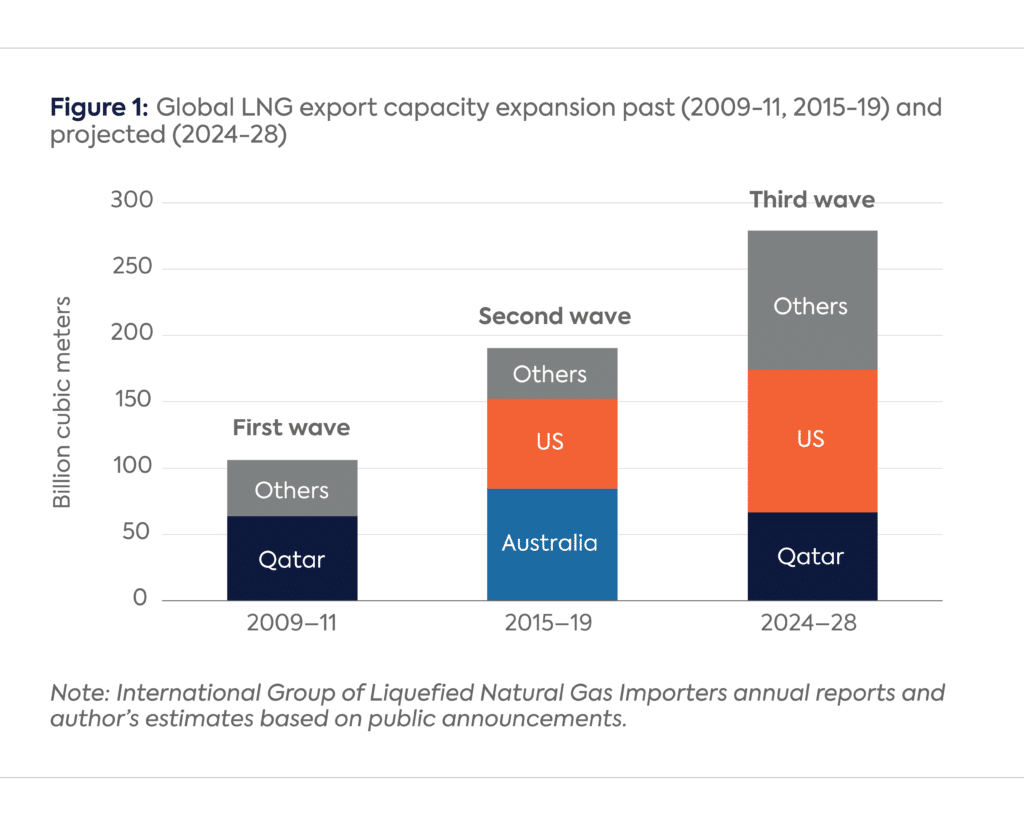

First, this decision will not affect US LNG projects currently under construction. By 2028, the US will hold 232 billion cubic meters per year (bcm/y) of LNG export capacity, up from 126 today, far ahead of Qatar (171 bcm/y). Additionally, the world is currently engaged in the largest LNG capacity expansion to date, with 280 bcm/y under construction. The medium-term impact of this decision will be minimal.

In the long term, the question is whether the world needs additional LNG beyond that capacity, be it from the US or not. Answers vary among institutions, but bullish views on future LNG demand tend to be more in line with business-as-usual scenarios than with those calling for significant reductions in GHG emissions.[2] Meanwhile, net-zero scenarios tend to show a higher reduction (against business-as-usual scenarios) in US LNG exports than in those from the Middle East.[3] That US capacity could be eventually stranded.

A lot of attention has been given to the EU market, but its LNG appetite will eventually decline as its gas consumption drops. The future of LNG remains in Asia, with China using LNG as the balancing item in its supply/demand equation while LNG has to fight to displace coal in other developing Asian economies.

This pause will be important in assessing one key parameter of LNG besides the economic and market factors: its environmental footprint, especially the assertion that US LNG could be worse than coal.[4] LNG plants impacted by the pause could come online in the late 2020s at best; it is, therefore, of utmost importance that they are prepared to be “environmentally” competitive given recent developments on methane regulations in the EU. Given the increased attention to reducing these emissions, regulatory measures will likely become stricter and broader rather than more lenient, eventually including other key LNG importers. For these LNG projects, this means having access to very low methane emissions upstream gas and reducing methane emissions—as well as using either clean electricity to liquefy natural gas or carbon capture, utilization, and storage—at the liquefaction plant, potentially forcing other US LNG plants (existing and under construction) to do the same. In a world where LNG supplies compete, other exporters with simpler value chains will make the investment to reduce their LNG’s carbon footprint.

Meanwhile, a new outlet could soon present itself for US gas: exporting hydrogen or its derivatives based on gas. But it will also have to be low-emissions.

Ira Joseph

Pausing US Department of Energy (DOE) regulatory approval for emerging LNG projects puts a brighter spotlight on the relationship between LNG production and meeting environmental standards. While 17 LNG projects are theoretically affected by this pause, only four—Venture Global’s Calcasieu Pass 2 (CP2), Delfin LNG, Lake Charles LNG, and Commonwealth LNG—are of note given how far they have progressed commercially.[5] Among these four projects are 21 million tons per year (mtpa) (29 bcm/y) of sales and purchase agreements signed in the past two years. This total constitutes 37 percent of their designed capacity.[6] These projects have yet to receive a final investment decision, as none of the four have contracts totalling more than 50 percent of the project’s capacity. It is safe to assume that this capacity is unlikely to see the light of day before 2028 based on the typical time it takes to build a greenfield unit, with the possible exception of CP2 given its modular design and track record of faster delivery.

Studying the environmental impact of LNG projects was a necessary step to take given the changing nature of the US gas market. Stricter oversight and controls on methane emissions in the upstream sector, which historically accounted for 60 percent of emissions along the US gas value chain, were already in place, so it was logical for the fastest growing downstream market for US gas, the LNG sector, to receive a similar and more comprehensive treatment. Feed gas for LNG use has gone from essentially nothing in 2016 to constituting 15 percent of US gas demand. By 2030, this number will climb to over 20 percent and, if all these projects in pause mode move ahead, 30 percent of demand is a distinct possibility.[7]

The pause by the DOE does not pause the development of the projects. Nothing is stopping these LNG projects from continuing to sign LNG contracts with buyers, which is essential for their success. A typical LNG project will seek at least 80 percent of its capacity under long-term contract before declaring final investment decision (FID) and locking down the non-recourse financing required to fund construction and initial operations.[8]

The effect of the pause on the broader LNG market is minimal at this point. Vast amounts of LNG capacity under construction in the US and Qatar do not have volume under long-term contracts. Even among the LNG that is in contract from emerging projects, at least 40 percent is sold to portfolio players that will need to resell the LNG to end users or into a spot market like Europe. If buyers are concerned that the DOE pause is a risk to their security of supply, plenty of LNG is on offer to assuage these concerns.

Akos Losz

Two assumptions appear to have informed the decision to temporarily halt pending approvals of LNG exports to non-free trade agreement (non-FTA) countries: that the impact on global gas markets—and the supply security of allies—will be minimal,[9] and that limiting export approvals to non-FTAs countries could be an effective tool in limiting the lifecycle GHG emissions of US gas.[10] Both assumptions may turn out to be wrong, depending on what happens after the pause.

When it comes to gas market impacts, the crucial question is how much LNG the world will need in the 2030–2050 period. Forecasts vary enormously, but most business-as-usual—and even some net-zero-compliant—pathways show the current plus under-construction LNG capacity falling short of projected demand, at least during some parts of this period.[11] One might take comfort in the fact that the US alone has another 90 mtpa of pre-FID capacity already fully permitted by both the Federal Energy Regulatory Commission (FERC) and the DOE.[12] However, only one of these projects (Delfin LNG) has secured binding LNG contracts to date (for 3 mtpa),[13] while the others have struggled to make progress or stalled altogether.

One might also take comfort in the fact that there is roughly 200 mtpa of pre-FID capacity outside the US that can plausibly fill a supply gap.[14] However, 40 percent of this capacity is located in Russia (hit by Western sanctions), 15 percent in East Africa (plagued by above-ground issues), and another 15 percent in Mexico (subject to DOE jurisdiction as projects take feedgas from the US). If global LNG demand goes into freefall in a decade (as some net-zero scenarios suggest),[15] then the fate of US projects matters little. But if demand is closer to current industry projections (or the more LNG-intensive net-zero pathways)[16], then any restrictions on future US LNG supply may well have a tangible impact on global balances 5 to 10 years from now, especially if the current suspension of permitting is maintained or extended in the future. In reality, US LNG does not have many easy alternatives, unless Qatar decides to undertake further expansion rounds. Meanwhile, the politicization of LNG exports is already prompting European[17] and Asian[18] policymakers to re-evaluate the risk profile of US LNG—and it will likely slow the pace of contracting until the regulatory uncertainty clears up.

Concerns about the lifecycle emissions of US LNG, especially methane emissions in the US shale patch, are very real and justified.[19] Since most methane emissions are concentrated upstream from the liquefaction plants,[20] it is more effective to target these emissions directly at the source—as the EPA’s methane rules already do,[21] and could potentially do even better—rather than indirectly and selectively through the DOE’s non-FTA authorizations for LNG exports. Imposing a separate GHG performance standard on US liquefaction plants based on industry best practices would be a sensible policy for any administration that takes climate change seriously. Knowing the actual emissions is a vital first step. However, picking a handful of projects with pending DOE applications to further study their climate impact while giving all operating, under-construction, and fully approved pre-FID projects a free pass is arguably not the most effective way to rein in LNG export related GHG emissions.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[13] The DOE non-FTA permit of Delfin LNG requires the project to commence LNG exports by June 2024. According to the DOE’s earlier policy statement in April 2023, an extension beyond this date will not be granted, unless the project has physically commenced construction AND it can prove that its inability to comply with the existing export commencement deadline is the result of extenuating circumstances outside of its control. See: https://www.energy.gov/fecm/articles/policy-statement-export-commencement-deadlines-natural-gas-export-authorizations

[14] Volume estimated by author based on S&P Global Commodity Insight, Liquefaction projects and contracts data, January 2024.

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

In March 2026, the Office of the US Trade Representative (USTR) announced it was investigating "structural excess capacity and production in manufacturing sectors" in 16 economies.

The US Export-Import Bank is preparing to close the first funding tranche of Project Vault, a public-private partnership establishing the US Strategic Critical Minerals Reserve.

CHRONIQUE. Nouvelles usines de liquéfaction et augmentation des exportations expliquent, entre autres, pourquoi les prix du gaz ne connaissent pas le pic observé en 2022, lors de l’invasion de l’Ukraine. Mais cette stabilité des prix ne traversera pas l’été, écrit Anne-Sophie Corbeau, spécialiste de l’énergie au Center on Global Energy Policy de l’Université Columbia