This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The Center on Global Energy Policy (CGEP) at Columbia University SIPA today released a new report examining Project-based Carbon Credit Markets (PCCMs) in G20 countries and Singapore. A...

Announcement• June 17, 2026

Energy Explained

Get the latest as our experts share their insights on global energy policy.

The 109-day-old Iran crisis is heading toward an off-ramp in the form of a not-yet-public Memorandum of Understanding to reopen the Strait of Hormuz. While energy markets are...

This event will take place in-person in Washington DC, at the Rayburn House Office Building, Room 2168 (Gold Room). Advance registration is required. Announcing New Columbia University Publications...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

As the world moves along the path of decarbonization, trade in energy is expected to evolve and eventually shift to new commodities and technologies, including critical minerals and hydrogen.[1] Much has been written about China’s significant role in the critical minerals value chains. But reflections regarding its role in the hydrogen space are mostly limited to analyses of China’s current and future manufacturing capacity—likely the world’s largest—of electrolyzers.[2] Much less consideration has been given to China’s future role in global hydrogen trade—whether it would take off and what its impact on investments, geopolitics, and interactions with potential trade partners might be. In this article, the authors assess China’s prospects for becoming a hydrogen importer.

China’s Current Role in the Hydrogen Market

China currently leads the world in hydrogen consumption and production, accounting for one-third of global demand.[3] However, the bulk of this hydrogen is derived from fossil fuels, mainly coal, resulting in significant carbon dioxide emissions. China’s “30·60” goal, announced in 2021, aims to peak carbon emissions by 2030 and achieve carbon neutrality by 2060. Therefore, China is accelerating its transition to a green and low-carbon economy.[4] The 14th Five-Year Plan on Hydrogen Industry Development underscores hydrogen’s pivotal role in the future energy system and prioritizes it for upcoming industrial developments.[5] With vast investments in research and development and technology deployments, China aims to become a global leader in low-carbon hydrogen. However, China’s strategy only sets a modest target of 100,000 to 200,000 tons of renewable hydrogen by 2025, with no quantified target beyond 2025.

While China will undeniably remain one of the largest, if not the largest, hydrogen markets, a key uncertainty emerges: will it also become an importer of hydrogen (or its derivatives)? China is currently a key player in all fossil fuels markets: it is the largest coal consumer, second-largest oil consumer, as well as the third-largest market for natural gas. Most importantly, it is also the largest importer of crude oil, natural gas and coal.[6] A swing in the country’s demand in any of these commodities has a direct impact on its imports and can, in turn, have significant implications for prices and global trade. Moreover, China’s policy decisions on fuel imports impact energy trade: for example, following tensions with the US, China imposed tariffs on US LNG, leading to near disappearance of its US LNG imports in 2019–20.[7] Similarly, tensions with Australia led to Chinese restrictions on Australian coal imports.[8]

Uncertainty about China’s Future Hydrogen Imports

China’s future role in global hydrogen trade is, therefore, a crucial question. But there is no consensus on the answer.

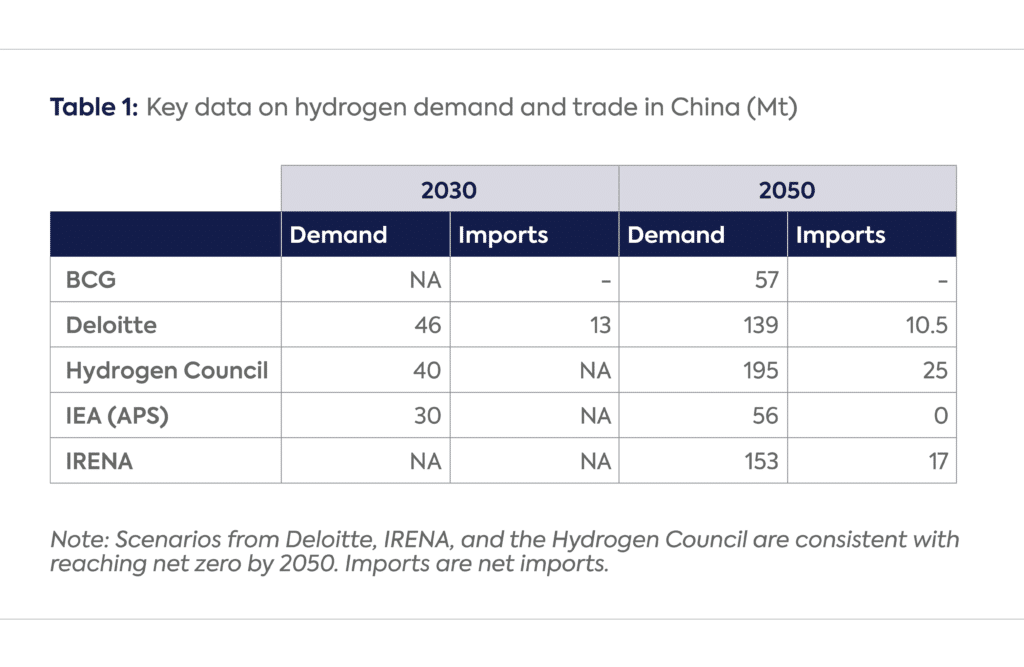

Deloitte expects China to be the world’s largest hydrogen importer with 13 million tons (Mt) by 2030—ahead of the EU’s 10 Mt—primarily sourced from the Middle East as ammonia.[9] These imports are projected to drop to 10.5 Mt by 2050, mainly in the form of sustainable aviation fuel, as China reaches near self-sufficiency.

The Hydrogen Council anticipates China’s imports to reach 25 Mt by 2050 under the form of green steel from Brazil and Canada, methanol and synthetic kerosene from the US, as well as ammonia.[10]

IRENA presents a slightly different perspective: while China may fulfill its domestic hydrogen needs and even have the capacity to export to neighboring countries, it will likely still import hydrogen in the form of low-carbon ammonia, primarily from Australia.[11]

IEA’s latest World Energy Outlook suggests that China achieves self-sufficiency by 2050 in the announced pledges scenario (APS) scenario[12].

BCG highlights a high uncertainty regarding China, including the expectation that it could become a net exporter by 2030.[13]

China could become an importer due to a rapid increase in demand for low-carbon hydrogen and its derivatives by 2030, a steadily high low-carbon hydrogen demand after that (notably in net-zero scenarios) and the lack of infrastructure linking future demand hubs, situated along the southeastern coast, to the northwest and northeast supply centers.

China faces a potential choice: either invest in extensive new infrastructure or opt for hydrogen imports. Currently, China has only a few short-distance hydrogen pipelines, which cannot transport large amounts from the northwest to the southwest. Construction of the first long-distance trans-regional hydrogen pipeline, spanning 400 km from Ulanqab in Inner Mongolia to Beijing, began last year.[14] Several proposed long-distance hydrogen pipelines have not even begun construction. Projections from the state-owned China Petroleum Pipeline Engineering Corporation indicate that, by 2050, China might require up to 6,000 km of hydrogen pipelines.[15] Building this infrastructure seems achievable in a country which built 46,000 km of gas pipelines over 2016–20,[16] and it’s a modest target compared to the European Hydrogen Backbone plans to build 27,000 km of hydrogen pipelines by 2030.[17] Still, in coastal regions distant from the hydrogen production centers, importing hydrogen or its derivatives could prove more cost-effective than domestic hydrogen transported over long distances.

Nonetheless, China’s hydrogen strategies, from both national and provincial governments, do not indicate any desire to import hydrogen from abroad.[18] This contrasts with Europe (especially with Germany), Japan, and Korea, which explicitly aim to import hydrogen. Unlike countries like Germany and Japan that have outreach strategies and have concluded several MOUs, China’s diplomatic efforts on green hydrogen development don’t indicate plans for hydrogen (or its derivatives) trade, except for one signed with Saudi Arabia that imports a small amount of blue ammonia.[19] So far, China has made hydrogen partnership announcements with over 10 countries in Southeast Asia, North Africa, the Middle East, Latin America, and Central Asia, mostly as part of the “One Belt, One Road” Initiative. Its involvement with other countries in the hydrogen space mostly remains in the area of construction of green hydrogen projects and sales of hydrogen-related equipment.

Besides, China’s large hydrogen production potential, underpinned by its abundant renewable energy resources, could improve its energy independence and security. The country’s photovoltaic resources have the capability to produce nearly 12 times the total electricity demand, including both hydrogen and ammonia production requirements.[20] Such renewable energy power generation potential positions China to drive a swift scale-up of renewable-based hydrogen production. Additionally, low capital costs imply the potential for low costs for domestic hydrogen and ammonia production. A significant factor behind this is China’s dominant share of electrolyzer manufacturing capacity, currently accounting for more than 50 percent the world.[21] As of 2023, China has spearheaded electrolyzer deployment with expected installed electrolyzer capacity reaching 1.2 GW—50 percent of the global capacity—by the end of 2023.[22]

Conclusion

China’s national low-carbon hydrogen targets are modest and, for now, there is no indication that China wants to boost low carbon hydrogen demand at the cost of becoming an importer. Besides, the country is well-positioned to be one of the largest low-carbon hydrogen producers in the world. Yet, should China fall short in meeting its domestic hydrogen needs, it could open the door to potentially sizable opportunities for exporters. Future trade patterns also depend on technological developments to transport hydrogen and its derivatives internationally, as there is still uncertainty about the future of global hydrogen trade.[23] Still, if China becomes a hydrogen importer, it will have significant ramifications not only for the global hydrogen market but also in terms of geopolitical power dynamics.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[11] IRENA, “Global Hydrogen Trade Part 1,” July 2022, https://www.irena.org/publications/2022/Jul/Global-Hydrogen-Trade-Outlook. Hydrogen consumption in Table 1 is estimated from “China is responsible for about a quarter of the global hydrogen demand” which is expected to be 614 Mt, and hydrogen trade from 1900 PJ in Figure 3.18.

China’s commitment to what it calls its “dual carbon” goals of carbon neutrality by 2060 and to ammonia’s potential role as a hydrogen derivative and carrier have fostered expectations that its renewable ammonia market will expand significantly and thus so will production.

La géopolitique de l’hydrogène s’inscrit dans un nouvel ordre énergétique mondial opposant les pétro-États, fondés sur l’exportation d’hydrocarbures, et les […]