Could a strategic lithium reserve kickstart US supply chain development?

NEW YORK -- A strategic lithium reserve is being mooted as a solution to stabilize volatile prices that have hindered American mining projects, allowi

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

If it seems like you're hearing a lot more about geothermal energy lately, that's because this clean, firm energy source is at a technological turning point. With roots...

Find out more about our upcoming and past events.

On January 1, 2026, the European Union's highly-anticipated Carbon Border Adjustment Mechanism (CBAM) will take effect. Introduced in 2023, CBAM will require the importers of certain carbon-intensive goods...

Summaries by Marianne Kah • September 18, 2018

For more than 50 years, automobile ownership was linked to income, and there were few new innovations that threatened major upset to passenger transport. Recent years have seen that change, thanks to three technology revolutions—vehicle electrification, automation, and shared mobility. Suddenly, more than ever in the last 50 years, the future of passenger transport is indeterminate because of new uncertainties around the pace of technological innovation, how passengers may adapt to these changes, and the policy and politics that are driving change.

On July 19, 2018, the Columbia University’s Center on Global Energy Policy, in collaboration with the Institute of Transportation Studies at the University of California, Davis, held a workshop on the Columbia campus focused on the energy impacts of the three revolutions. Participants included experts from the automotive, mobility service (e.g., ride-hailing), energy, government, and financial communities as well as transportation researchers from the academic community. There was a special focus on China since vehicle ownership there is rising rapidly and that nation is the world’s leader in passenger vehicle electrification.

Workshop attendees reached no consensus on the impact of the three revolutions on energy demand, but they discussed two possible scenarios providing the bookends of how these revolutions could play out. A scenario with high electrification, efficiency improvements from automation, and ride pooling would significantly reduce energy demand from passenger transport and lower greenhouse gas emissions. However, without strong government policy intervention, there could instead be a scenario with a slower pace of electrification, automation stimulating additional travel, low vehicle occupancy, and urban sprawl. This latter scenario could significantly increase energy demand and greenhouse gas emissions. Participants indicated that even in the first scenario with strong government intervention, reducing oil consumption in vehicles is a slow process due to soaring demand for new vehicles in the developing world and slow vehicle turnover rates.

The workshop explored the drivers behind these possible scenarios. It was conducted on a non-attribution basis under the Chatham House Rule. The following summary highlights the main points that arose.

Some participants asserted that the global passenger fleet is likely to fully electrify, although the views on the pace varied. Others argued that electrification was not inevitable and would depend on continued strong government policy support. The timing and pace of electrifying passenger vehicles is primarily dependent on when battery costs make EVs competitive with the internal combustion engine–powered car, the strength of government policy support, and the pace of building out charging infrastructure.

One of the speakers indicated that EVs currently cost about $10,000 more to manufacture than comparable gasoline cars. Most projections indicate that battery pack costs would need to fall from about $200/kWh or more today to $100/kWh to be competitive with the internal combustion engine (ICE) and that this is foreseen between 2025 and 2030. However, one participating expert indicated it could happen sooner because battery makers already know how to produce batteries at close to that cost level and will be able to do so when they scale up production far above today’s levels. Thus, sales levels and scale are key factors. A view was expressed that there is greater potential for scale and innovation within the realm of lithium-nickel-manganese-cobalt chemistries, meaning that further cost improvements are possible with current battery chemistry. In addition, solid-state batteries have the potential to be safer, charge faster, and be more durable. It is also important to note that there isn’t one date when all EVs will be competitive versus ICEs. One participant indicated that smaller cars with smaller battery requirements will become competitive in advance of larger vehicles. However, purchasers of larger cars may be less price sensitive than those of smaller cars such that some larger luxury EVs could be electrified early despite the high battery price (e.g., Tesla Model S).

One concern about the pace of battery cost reduction is constraints on expanding relevant metals supply and the accompanying price increase. One presenter indicated that battery metals (lithium, cobalt, nickel, and manganese) represent one-third of the composition by weight of a battery cell, so rising metal prices could slow the timing of batteries becoming competitive with ICEs. Cobalt mining is also a very concentrated industry with pricing power. The top four producers are responsible for two-thirds of global production. The same speaker indicated that new resources and production efficiencies are important to meet the demand for battery metals. This speaker also indicated that the use of substitutes by other industries could decrease competition for metals with the EV industry. EV batteries will account for a greater share of global metal production going forward. By 2021, batteries will use 31 percent of current cobalt production and 108 percent of current lithium production. Battery makers are addressing cobalt constraints by developing battery chemistry that greatly reduces the amount of cobalt required.

There was a general consensus that electrification is being driven by strong government policy in certain regions (e.g., China, Europe, California). Most participants believed that a continuation of strong government incentives would be required to promote rapid electrification. A number of countries already announced sales bans for ICE-powered vehicles starting between 2025 to 2040 (e.g., Norway, Netherlands, United Kingdom, France), and a number of cities have announced fossil fuel–free street declarations by 2030 (e.g., Barcelona, London, Copenhagen, Paris, Mexico City). One presenter indicated that if you combined the EV sales per year for some of the major countries or states that are banning fossil-fueled vehicles, it would equate to about 8 million EVs in 2025, 20 million in 2030, and 50 million in 2035. Other policy tools to incentivize penetration of EVs include purchase subsidies (e.g., China and Norway), exemptions from sales or other taxes, registration fees, or registration limits (e.g., China). A number of other incentives were discussed in relation to China and will be described in that section of this paper. However, it is also uncertain whether current incentives will be sufficient to drive rapid electrification. One of the speakers emphasized that despite all the policy levers California has used to promote zero emissions vehicles, EVs still represent only 4.5 percent of the state’s total passenger vehicle fleet.

The question was raised about whether EV competitiveness would occur later in time due to improving fuel efficiency of the ICE-driven vehicle. One response to this query was that automakers would reduce investment in the ICE-car due to the large capital investments needed for developing electric vehicles, which are required in key geographies that have announced bans on the sale of fossil fuel–based cars. In addition, it will be easier to meet overall fuel efficiency standards in some locales with EVs in the sales mix. ICE-cars could lose their competitive edge due to underinvestment.

Some attendees who expressed the view that electrification will occur rapidly pointed to rising capital investments in EVs by the automotive industry. One speaker indicated that auto manufacturers are currently investing $170 billion in EVs globally and could be selling 15 million EVs by 2025 versus 1 million today. One participant believed that automobile manufacturers can’t afford to support both ICE and EV platforms, particularly when the industry is believed to be at the peak of the economic cycle and will experience eroding sales. Automakers will choose EVs because they have to develop them for China and other policy-driven markets. In North America, automakers may focus on electric cars while continuing to make popular models of ICEs like light duty trucks (e.g., SUVs and pickup trucks). The supply chain is also developing to support electrification. Thus far, six battery suppliers are producing over 100,000 units per year for cars, although 200,000 would be viewed as closer to full scale.

Electrification trends are thought to be interlinked with the other transportation revolutions of automation and shared-mobility services. According to participants, some automakers will invest in EVs to support mobility services because these services may have a higher margin in the future than the manufacturing of cars. The economics of EVs versus ICEs would improve in commercial fleets since the higher up-front cost of EVs can be amortized over a more highly utilized fleet. Personal vehicles are only used about 5 percent of the time compared to substantially higher utilization rates for fleets (one estimate referenced was up to 95 percent). EVs also have lower fuel and maintenance costs than ICEs, which would be a benefit for both fleets and private owners. However, the lower variable operating cost of EVs is a particular advantage for intensively utilized fleet and shared transportation service vehicles.

There was little discussion about consumer acceptance of EVs, although one of the speakers discussed the need to inform buyers about the basics of EVs and their benefits. Another speaker noted that a few leading EV brands receive some of the highest satisfaction ratings from their owners of any vehicle sold today. There seemed to be an implicit assumption that when EVs became cost competitive, consumers would embrace them. However, it is important to understand how mainstream buyers will view the value proposition of EVs versus their ICE-driven cars.

There was a divergence in views of whether plug-in hybrid electric models (versus a battery-only vehicle) would survive. Plug-in hybrids reduce battery cost and range anxiety so they would be appealing to drivers. However, they have two drivetrains, which makes them expensive, and some countries and cities that are banning fossil fuel–powered cars may not accept hybrids.

Various scenarios for EV penetration were presented, including the International Energy Agency’s reference or “New Policies” case and the agency’s more aggressive scenario of “EV30@30” (EVs having 30 percent market share by 2030). The New Policies case projects 125 million EVs on the road globally by 2030, up from 3.7 million in 2017, which is based on sales growth for EVs of 24 percent per year. The EV 30@30 scenario projects about 230 million EVs in operation by 2030, based on a sales growth rate for EVs of about 33 percent per year. A scenario was presented at the workshop with a similar EV sales growth rate as EV30@30, which indicated that more EVs would be sold than ICEs by 2032. However, even in this scenario, there would still be more than 1 billion ICEs on the road in 2035, demonstrating how long it takes to turn over the global vehicle fleet. A “revolutionary” 40 percent per year EV sales rate projection was also presented, which would have more EVs being sold than ICEs in 2029. The impact of passenger vehicle electrification on global oil demand is discussed in a later section of this report.

There was some discussion about the prospects for electrification of buses, commercial vans, and vehicles in ports and distribution centers. Participants agreed that electrifying heavy duty long-haul vehicles is extremely challenging due to the cost and weight of the batteries. Due to the weight limits on long-haul vehicles, the addition of heavy batteries could significantly reduce cargo-carrying capacity. The situation with respect to heavy duty short-haul vehicles, like buses, is substantially different. Buses provide some of the most favorable conditions for vehicle electrification (e.g., not weight sensitive, return to the same place to charge every night). The explosive growth of electric buses in China in the past few years demonstrates the electrification potential for buses.

China is the largest automobile and electric vehicle market in the world today. As a result, it received special focus at the workshop. China has ambitious policies supporting vehicle electrification and the build-out of charging infrastructure. In 2017, China had 40 percent of the global electric car stock, and new electric car sales have nearly doubled each year since 2014. China also has 98 percent of the electric bus stock in the world.

One of the speakers indicated that China’s electrification strategy is motivated by national security considerations, environmental concerns, and industrial policy. The nation is 69 percent dependent on imported oil, which hurts its balance of trade and makes it vulnerable to disrupted supply, particularly with deliveries through the Strait of Malacca. The nation has rare earth metals but insufficient volumes of oil or natural gas to meet its domestic needs. It also has abundant domestic coal resources to generate electricity. Becoming the world’s largest supplier of batteries and electric vehicles is an important industrial strategy of the country and similar to its previous policy of becoming the world’s largest producer of solar panels. China wants to leapfrog automobile manufacturers from other countries by scaling up EV production before them. China also has regional economic growth plans that benefit from local manufacturing of batteries and electric vehicles. Electrification is also important for reducing smog in megacities well as for meeting China’s commitment to international climate agreements.

China’s government has multiple policies that incentivize electrification of the passenger fleet. The central government has direct subsidies for purchase of EVs, which are gradually being phased out. Another policy is allowing car owners to avoid the lottery for obtaining a license plate and restrictions on driving into major cities if they purchase an EV. In September 2017, China adopted a zero emissions vehicle (ZEV) credit policy for passenger cars that is similar to California’s ZEV policy. The policy requires that 10 percent of new cars sold in the country have to be zero emissions vehicles by 2019, rising to 12 percent in 2020 and to 20 percent in 2025 (passenger and commercial vehicles). Aggressive targets have been discussed of reaching 50 to 60 percent of new car sales by 2035 to 2040. There have also been discussions within the Chinese government about phasing out ICE vehicles completely. Participants stressed the government would need to be convinced that it is in China’s economic interest to do so.

Some U.S. participants expressed concern that China will dominate battery and EV manufacturing if US companies don’t step up their pace and that this could result in a loss of manufacturing jobs in the United States. Most batteries are manufactured in China and elsewhere in Asia. Participants discussed the impact a trade war could have on China’s electrification strategy. A trade war could support the Chinese auto industry by concentrating even more Chinese investment in EVs and reducing foreign automakers’ investing or selling of cars in China.

Another topic of discussion was the difference between US and Chinese development of charging infrastructure. China has more unified standards and supportive policies for the build-out of public charging infrastructure than the United States. However, China faces more obstacles to charging. There is limited space in the cities and limited parking. Early EV adopters in the United States have greater access to residential charging. The United States makes greater use of charging models with the intent of attracting shoppers. Chinese charging infrastructure is growing rapidly, and there is more DC charging than in the United States. However, some of the early charging infrastructure put in place in China was deployed haphazardly (e.g., with no street access). There is also more informal and black-market charging in China (e.g., from a store or residence). A high percentage of the charging infrastructure in China is also for fleets. In addition, China’s infrastructure is being developed by domestic companies, whereas in the United States work is being done by both US and international companies. China may have an advantage over the United States in mobile EV charging because mobile pay is more universal in China than in the United States.

A question was raised whether the electrification of Chinese vehicles was likely to lower greenhouse gas emissions on a full life cycle basis, given that coal represents two-thirds of the nation’s electric power mix. Due to the higher efficiency of electric motors versus the ICE, greenhouse gas emissions for EVs in China are similar to those of ICEs. As China adds more nuclear, renewables, and natural gas capacity in its power sector, EVs offer the potential of considerable greenhouse gas emissions reductions and the possibility of deep decarbonization of the transport sector.

Many of the presenters expressed the view that the global automobile fleet would be fully automated eventually. Participants indicated that most automated vehicles that have been developed thus far are at a level 2 (on a scale of 1–5), which is commonly defined as a state where the vehicle can assist with two or more steering, braking, or acceleration functions but the driver needs to be ready to take control of the vehicle at any time. Full automation is generally considered to be levels 4 and 5, where in level 5 the vehicle does not need human intervention throughout the trip and will not have a steering wheel.

Full automation could occur for specific types of vehicles (e.g., buses, vans) in geo-fenced areas in the next five to ten years. However, it is not likely to be widespread for several decades or longer. In addition, it would take 15–20 years to get all the driven cars off the road, which will slow down the transition to automated vehicles. One factor that could speed up full automation is if the industry adopts the Google model, in which the automated vehicle (AV) can function independently from infrastructure. Automation will also likely occur first in high income countries where time is highly valued and last in high population and low income developing countries where drivers aren’t paid as much.

There are significant benefits of full automation, notably including allowing passengers to use their time on other activities while being chauffeured by the car. Groups who can’t drive due to age or physical limitations will also benefit from automated vehicles. Automobile manufacturers will also view automated vehicles as attractive because they allow them to compete in a familiar business model of making profits on high tech extras in cars. There will also be significant safety benefits and potential benefits of improved energy efficiency. The net energy implications of vehicle automation remain a significant uncertainty being evaluated, as discussed further below, and may depend on policy incentives related to vehicle configuration and utilization.

There are also significant challenges that need to be overcome to fully automate the car fleet. One is driver acceptance. People have concerns about machines being confused by unfamiliar scenarios, equipment failures, privacy or cybersecurity breaches, and safety. Some people question robots making life and death ethical decisions, even if the robot can statistically do a better job than a human. Accidents with automated vehicles are less acceptable to people, even if their occurrence is lower. There are complex social, ethical, and legal issues surrounding who is actually in charge and therefore responsible. Establishing a policy and regulatory framework for the vehicle’s driving decision process and rules of the road that is consistent across jurisdictions will be difficult. One participant stated that we may see fully automated vehicles five years after full regulatory approval. This participant was not willing to forecast the timing of full regulatory approval.

Another challenge to mass market sales of AVs is their additional cost, which by one estimate would start at $75,000 extra and fall to $12,000 at scale. A related issue is that automation presently has a significant power draw on the vehicle, reducing the range of the vehicle by 5 to 33 percent. However, one speaker indicated that developers are still in pilot mode and have not yet begun to optimize the vehicle and costs. Cost optimization and semiconductor performance are likely to improve over time.

Another significant challenge discussed in the workshop was navigating through the long transition period when there are both automated and nonautomated vehicles on the road at the same time. Participants discussed whether this would reduce the safety of AVs and whether they would get all of their potential fuel efficiency improvements. For example, you might not be able to platoon effectively and improve energy efficiency if there isn’t a dedicated lane for AVs. There is an incomplete understanding of the relationship between level of automation, extent of adoption, and fuel efficiency savings.

There was a general expectation in the group that AVs would likely be electric. The engineering is easier when there is an electric drive. In commercial (including mobility-as-a-service) fleets, AVs are more likely to be electric because EVs have lower fuel (electricity) and maintenance costs and the higher up-front cost of an EV is amortized over many more miles per vehicle for fleet vehicles. Fleet vehicles are highly utilized over time compared with private vehicles, which are utilized only about 5 percent of the time. One participant indicated that EVs are also expected to be more durable and thus better suited for very high mileage driving, apart from the batteries. However, battery life and replacement requirements for a vehicle driving more than 80,000 miles per year (0.5 million miles over six years) are also important considerations. An initial indication that EVs will be the platform of choice for AVs is that only 13 percent of the AV cars that have been permitted in California have internal combustion engines. The 87 percent of AV cars that have been permitted are either all electric or hybrid electric vehicles.

There wasn’t a consensus in the group on whether AVs are more likely to be privately or collectively owned such as in a commercial fleet of mobility service vehicles. It was suggested that particularly in a country like the United States, people may be unwilling to give up their privately owned car. The economics of automated rides on demand are still uncertain, and less compelling outside of urban areas. People in urban areas may feel that the ride on demand from an automated fleet may not come as quickly or reliably as they need it to be. Counter to that view, several participants believed that at least the initial AVs would not be privately owned because they are too much of a craft product with high tech maintenance requirements. Attendees also asserted that AVs—which have additional up-front costs relative to traditional vehicles—will likely be purchased by commercial fleets, which can amortize their costs over a much larger number of vehicle miles. Whether AVs are privately or collectively owned could have significant land use impacts. A presenter cited a preliminary study conducted in the Seattle area indicating that people want to live in areas where travel is convenient. If AVs are privately owned, the owners are more likely to live in a suburb. If AVs are made available as an urban mobility service, more people will want to live in the core area downtown.

Moving the discussion to energy demand, there is a significant debate over whether AVs reduce energy demand because they can improve the efficiency of driving or whether they increase overall energy demand due to encouraging additional vehicle miles traveled (VMT). In one efficiency-focused scenario presented, AVs would reduce energy use by 40 percent despite the increase in VMT. In a contrasting scenario, which involved increased travel as well as an increase in energy intensity from higher speeds and larger energy loads, energy use compared to a nonautomated vehicle would double. The remainder of this section addresses these scenarios.

There are a number of ways in which AVs can reduce the energy intensity of driving. Large reductions in energy intensity can be obtained through automated cruise control and platooning (vehicles traveling close together), which reduces drag. For trucks, platooning could be particularly impactful with energy savings of 20 to 50 percent. In addition, the AV would be programmed to drive in eco mode with performance deemphasized (e.g., less aggressive acceleration) in favor of fuel efficiency. If acceleration was returned to 1982 levels, there would be a 23 percent reduction in energy use. Improved crash performance would allow the vehicle to be lightweight and therefore less energy intensive. If the AV is fleet owned, it will be easier to organize the system to send you the right size vehicle for your specific trip. For example, in such a system, you wouldn’t get sent an SUV unless it is needed for the purpose of that trip. However, there are several aspects of AVs that could increase energy intensity—including potentially higher highway speeds and the additional energy load from increased features, along with increased traffic congestion from higher VMT levels.

Although highly uncertain, there was speculation that automation can increase vehicle miles traveled by as much as 60 percent due to the lower cost of driving and greater convenience, which would in turn increase energy demand, congestion, and air emissions. When you lower the cost of driving by taking the driver out of the picture, it will induce people to take additional and longer trips. It could also increase the use of ride hailing since this will become much cheaper. Some participants noted that more work needs to be done to better understand the elasticity of vehicle miles traveled as a function of price and convenience. Empirical evidence for increased travel is found in several studies cited in the workshop that show that mobility services on demand have increased vehicle miles traveled and taken market share away from mass transit. Automated heavy-duty trucks could also take away market share from more energy efficient modes of transport (e.g., rail, barge). There will also be new user groups, and in particular the elderly, who will travel more than they were able to in the absence of AVs. People may also choose to live farther from downtown when they can make productive use of their commuting time. Thus, AVs can encourage urban sprawl.

Participants also discussed some potential VMT scenarios that could appeal to consumers but terrify transportation planners, including one in which a car drives someone to work and then goes home and waits to be called at the end of the day for the return trip home. This potential scenario doubles vehicle commuting miles. Riders could also ask a car to drive around while they shop because parking is expensive or difficult to find (although mobility service vehicles and taxis may also cruise). A car could be sent to the store to pick up a single item, or a service like Amazon could deliver an item within an hour. The increase in congestion from such a scenario could be so great that it could even constrain itself. Automation should be able to lower congestion by reducing the needed space between vehicles and smoothing traffic flow by coordinating vehicle movements. These factors should increase the capacity of the road. However, that effect could be far outweighed by increased vehicle travel. The scenarios where automation can reduce vehicle travel and substantially decrease energy use/emissions involve shared mobility and ride pooling, as we discuss in the next section.

The third transportation revolution of “shared mobility” arises from the combination of the sharing economy and information technology and the ability to use cell phone–based apps to call for mobility services. Transportation network companies (TNCs) include what are more commonly referred to as ride-hailing services (like Uber and Lyft and Didi in China). At least initially, they are likely increasing vehicle miles traveled (VMT) because of their initial displacement of mass transit and human powered modes (e.g., bicylcing and walking). Ride-hailing services are attracting riders due to their greater speed of travel, convenience, and comfort than alternative higher occupancy transport modes, walking or bicycling and because of the extra miles required for vehicle repositioning between service rides. By taking out the cost of the driver and thereby reducing transportation cost, automated ride-hailing vehicles are likely to exacerbate the increase in VMT. Urban planners have expressed concern that this additional travel will increase local congestion and air emissions in addition to generating more energy demand and greenhouse gas emissions. To address this concern, the workshop discussion strongly emphasized the potential value of decoupling passenger travel (PMT) from shared-mobility vehicle travel (VMT) by encouraging higher occupancy of TNC vehicles, i.e., encouraging pooled rides.

Early evidence indicates that so far ride-hailing services are substituting for taxis, mass transit, and biking/walking more than private car trips. Several workshop participants cited research by the urban transportation expert Bruce Schaller indicating that while ride-hailing services have taken market share from taxis, annual ridership of these services and taxis together in the United States have increased more than 240 percent over the last six years after rising only 36 percent over the previous 12 years.[1] Ride-hailing services are drawing customers away from nonauto modes of transit such as public transit, walking, and biking. Bruce Schaller’s research indicated that 60 percent of ride-hailing service users in large dense cities in the United States would have taken public transit, walked, biked, or not made the trip at all if ride-hailing services were not available.[2] Similarly, research in New York City and San Francisco cited in Daniel Sperling’s recent book on the three transportation revolutions indicated that 10 to 30 percent of ride-hailing service users switched from mass transit.[3]

At the workshop, attendees discussed how mobility trends, and ride-hailing in particular, are impacting New York City. For-hire vehicle trip volumes in New York City used to be 100,000 trips per day a few years ago, and they rose to 400,000 trips per day last year. Public transit use is falling, and bicycling has plateaued. Congestion has increased. The average speed of traffic was nine miles per hour in 2010, and it fell to seven miles per hour in 2017, with an even lower five miles per hour in midtown Manhattan. As a result of increased congestion and the impact on taxi drivers, New York City’s City Council passed a bill on August 8, 2018, imposing a one-year moratorium on new licenses for hired vehicles.

Sperling’s recent book was also cited asserting that the solution to making transportation more sustainable is to merge electrification and automation with shared mobility and ride pooling.[4] The idea is to maximize passenger miles while minimizing vehicle miles. That will allow access to transportation services while constraining congestion, energy use, and emissions.

The challenge for pooling is that people have been moving away from it to low-occupancy personally driven vehicles for many years. Solo driving is the highest it has been in US history, with public transit in the United States representing only 1 percent of passenger vehicle miles traveled. Carpooling is at the lowest level in history in the United States. There was a great deal of discussion at the workshop about whether people would be willing to give up their personal vehicles and share commercially available rides with strangers, and what government policies would incentivize this behavior. One observation was that people would be less willing to pool because it adds to their trip time and increases the variability and unpredictability around their trip time. However, low income users might be incentivized more by the lower pooled fare than by the need to minimize time.

Private companies are experimenting with different models of mobility services, including TNCs and traditional automobile manufacturers. UberPool and Lyft Line have app-based pooling services to match strangers sharing rides. By 2016, 50 percent of Lyft and Uber riders in San Francisco opted for requesting pooled rides. The actual achieved rate of matched and pooled rides is not public information. Companies may also experiment with businesses that increase electrification. For example, GM Maven rents electric cars to ride-share drivers while maintaining responsibility for vehicle maintenance and providing the ride-share cars access to fast charging. That gets more EVs on the road with high mileage, which will lower oil demand.

Various government policies to incentivize shared mobility and pooled rides were discussed. Examples included congestion pricing, fees for single occupancy of vehicles, high parking fees, reduced parking and priority parking for pooled vehicles, restrictions on unpooled vehicles’ access to the city, tax credits for mobility service providers for higher occupancy, subsidies for low income users who pool, HOV lanes for pooled vehicles, etc. Many of these policies are unpopular and politically difficult to achieve, and the local jurisdiction may not even have the authority to enact them.

Some participants advocated for congestion pricing. This would not be a traditional flat fee but rather real-time pricing across different areas in the city to influence and optimize trips to avoid congestion.

Another idea several participants introduced was to redesign city streets to use dynamic pricing for parking spaces. Curbs would become places for pickups and drop-offs rather than for longer term parking. Parking spots would be designated on each block for ride-hailing services to park and wait for the next fare rather than having to cruise and add to congestion and energy use.

One participant argued for policy flexibility and the avoidance of policy lock-in before the private sector has experimented and figured out the best way to provide mobility services. This participant believed that private companies have the advantage over governments in developing new services because they can fail fast and move to a different approach. The government moves much slower and gets bogged down in myriad processes and approvals. Since cities still own the streets, the best model could be public-private partnerships.

A number of participants asserted that it would be more effective for governments to offer travelers a suite of new intermodal transportation options to encourage them to pool rather than just penalizing them if they don’t ride pool. This suite of options might coax travelers out of their private cars and get them to try options that aren’t single occupancy. A recent example of a private mobility provider integrating across modes is Lyft buying Motivate, the largest bike-sharing network in the United States. Similarly, Uber has invested in a bike-sharing network and electric scooter network.

To simplify seamless access to integrated transport options for the consumer, one participant indicated that there should be one app on cell phones that shows multimodal travel options and pricing and allows the user to schedule trips. Public-private partnerships might be helpful in accomplishing this, and there would need to be collaboration between state and city agencies. Governments could collect and manage transportation data across modes that they could make available to consumers and private mobility providers for purposes of trip optimization. Privacy issues would need to be considered as well as the protection of competitive data for private mobility service providers.

Another transportation option that the workshop discussed was microtransit, which is a technology-enabled “on demand” transit service that offers flexible routing and/or flexible scheduling of minibuses or vans. Given the decline in public transit ridership, cities have hoped that subsidized microtransit could potentially lure back riders lost to popular app-based ride-hailing services. Some early experiments with microtransit have failed to generate sufficient ridership to be a sustainable business. A question was raised by one of the participants about whether and what will be a sustainable business model for microtransit.

Returning to the question of whether Americans are willing to give up privately owned cars, there was a lack of consensus about this issue among workshop participants. Some participants believed that it was possible. They observed that millennials are currently behaving differently about car ownership than previous generations. The example given was that in 1983 90 percent of Americans who were 19 years old had a driver’s license, while today only two-thirds do. One explanation is that they may have less need for a car than their predecessors given the availability of ride-hailing services. However, other participants believed that millennials would behave more similarly to previous generations as they age, get jobs, and have families. They may only appear to be different now due to the more limited employment opportunities following the 2008 financial crisis.

Finally, participants discussed how automated vehicles will need to be redesigned to be passenger rather than driver focused. Similarly, vehicles need to be redesigned for pooling in ways that enhance privacy and security and appeal to different user groups (e.g., gender, age, etc.).

A presenter discussed how supply chain management would likely be optimized by the widespread adoption of disruptive technologies. These would include

These technologies would allow companies to reduce freight miles traveled, impacting fuel demand. Examples of how these technologies can reduce mileage today include optimizing the route and refueling points. In one to two years, companies would be able to track many of their assets in real time. In three to five years, advanced analytics would enable companies to do real-time route optimization and predict arrival times and needed fleet maintenance. In 5–10 years, companies might use automated trucks and drones for shipping.

A view was presented that it is possible for companies to use these technologies to reduce miles traveled in the shipment of freight by 25 percent in the next five years, and an additional 10–20 percent in the long term when more advanced technologies like 3-D printing and drones are widely available. There was a lack of agreement over whether these large impacts would really apply to the entire industry versus a specific set of companies.

This matters to global oil demand because road freight trucks and marine shipping are responsible for 22 percent of global oil demand. In addition, demand is a direct function of miles traveled. Oil demand for freight trucking is also expected to grow 25 percent by 2040.

The workshop included discussion about the impact of electrification on global oil demand. One speaker presented a recent forecast that there would be almost no loss of global oil demand in 2020, only about 1 million barrels per day (bpd) in 2025, about 2.5 million bdp in 2030, and about 6 million bpd in 2035. Note that these are reductions from the growth that could have occurred in the absence of EVs rather than absolute declines in demand.

Published projections generally indicate either continued growth or little impact of electrification before 2025. In 2030, projections show a loss of 1 to 4 million bpd of oil demand compared to what it would have been without electrification. In 2035 there is a loss ranging from 2 to 6 million bpd, although there is an outlier two-degree carbon scenario indicating a loss of 10 million bpd.

While electrification could significantly reduce passenger vehicle oil demand in the long run, it is possible that automation and ride hailing could increase travel demand. However, many but not all participants believed that these trends would more likely increase electricity demand than oil demand.

The passenger vehicle sector consumes about 25 million bpd of oil today. Even without electrification, oil demand was not expected to grow much in this sector due to significant vehicular fuel efficiency improvement. There are also other sectors of demand, such as aviation, long-haul freight, and petrochemicals that are expected to grow, which could offset any demand decline in the passenger vehicle sector.

A few participants discussed what would happen to oil prices if oil demand growth were to slow or decline. Theoretically, lower oil demand would allow oil prices to be set further down on the oil supply curve at a lower level. However, due to the addition of moderately lower-cost tight oil resources in the United States, the supply curve is flatter than it used to be, so the price impacts of moving down the supply curve might not be as severe as they would have been in the past. In addition, a sustained period of low oil prices could tighten the oil market. The industry would be forced to reduce investment in new supply, and lower revenue would make oil-producing countries less stable, which could lead to more oil supply disruptions. Oil price spikes would cause further substitution away from oil in the transport sector. Thus, there could be periodic oil price spikes woven through a pattern of long-term erosion of oil prices. A transition away from oil could result in even greater price volatility than we have observed in the past.

Throughout the workshop discussions, a range of topics for future research were identified.

[1] Bruce Schaller, The New Automobility: Lyft, Uber and the Future of American Cities (Brooklyn, New York: Schaller Consulting, 2018), 7.

[2] Schaller, The New Automobility, 2.

[3] Daniel Sperling, Three Revolutions: Steering Automated, Shared, and Electric Vehicles to a Better Future (Washington, D.C.: Island Press, 2018), 113.

[4] Sperling, Three Revolutions, 19.

[5] “Urban informatics” refers to the study of people creating, applying, and using information and communication technology and data in the context of cities and urban environments.

On November 6, 2025, in the lead-up to the annual UN Conference of the Parties (COP30), the Center on Global Energy Policy (CGEP) at Columbia University SIPA convened a roundtable on project-based carbon credit markets (PCCMs) in São Paulo, Brazil—a country that both hosted this year’s COP and is well-positioned to shape the next phase of global carbon markets by leveraging its experience in nature-based solutions.

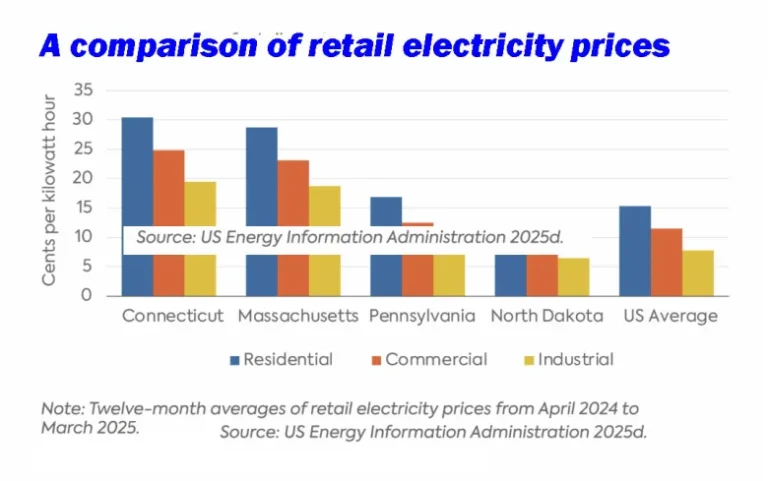

Connecticut needs an honest debate, and fresh thinking, to shape a climate strategy fit for today, not 2022.

Full report

Summaries by Marianne Kah • September 18, 2018