This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

Despite all the advancements we have achieved globally in recent decades, as many as 750 million people still lack access to electricity. Tackling energy poverty requires far more...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

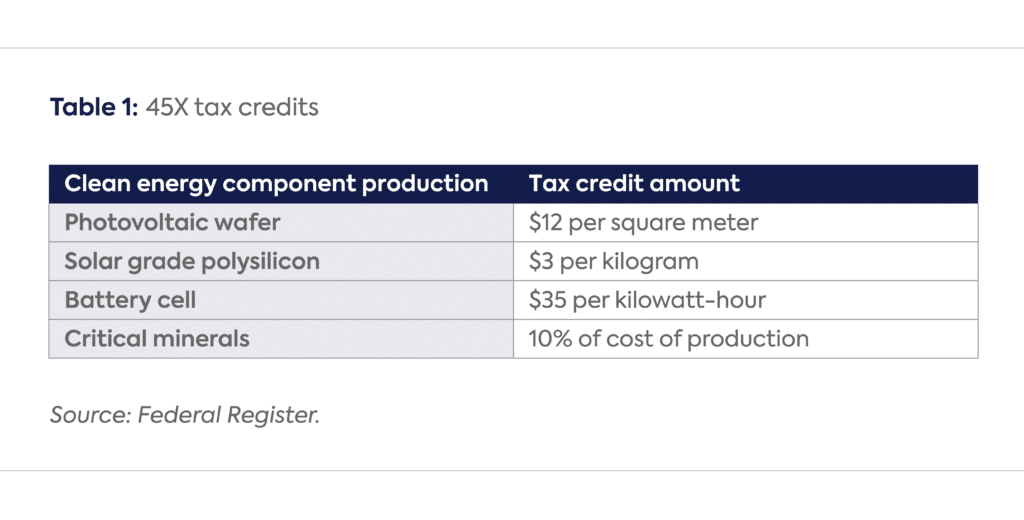

In December, the US Treasury Department released a proposed rule for the Advanced Manufacturing Production Tax Credit, part of the Inflation Reduction Act (IRA). Better known as 45X, the production tax credit is a core lever in supporting the onshoring and development of advanced manufacturing for clean energy technologies and components, including solar panels, wind turbines, batteries, and critical minerals. However, a coalition of mining companies, automakers, and Democratic senators has criticized the proposed rule, arguing against its exclusion of domestic mining. This Q&A examines the issues fueling the disagreement.

What is 45X?

The 45X tax credit is a key to unlocking the IRA’s main goals—onshoring and growing domestic manufacturing, creating new supply chains for clean energy, and combating climate change—by driving down the price of clean energy technologies. 45X is a production tax credit (PTC), meaning that a taxpayer (company) receives the credit for each unit of production.

For critical minerals, 45X provides a 10% credit on the production of 50 minerals outlined in the legislation. While for other technologies the tax credit ends on a specific date over the next decade, there is no such sunset clause for critical minerals. This can provide additional certainty for projects, especially considering that mineral-related projects can be delayed because of permitting issues. While 45X received praise from clean energy sectors like the solar industry,[1] it has come under heavy criticism by the mining industry and some legislators who believe that the proposed rule does not adequately support the domestic supply chain—when the Biden administration’s goal, along with bipartisan consensus in Congress, is to expand domestic mineral production for national and economic security in the face of China’s dominant position.

What is the issue at the heart of the debate?

The proposed rule states that “direct and indirect material costs [and] any costs related to the extraction or acquisition of raw materials would not be taken into account as production costs.” This means that the tax credit would not go to mining companies for directly extracting raw minerals (mining). Instead, the PTC could be used only by mineral processors—those that convert raw minerals into the higher-value chemicals used directly in clean energy technologies—and by battery recyclers. For example, the mining of lithium is not PTC-eligible, but its conversion into lithium carbonate or lithium hydroxide (needed for lithium-ion batteries) is. However, the current PTC guidance is challenging even for processors and recyclers, as the cost of purchasing raw materials is also not included.

The cost of acquiring raw minerals to produce critical processed minerals, as well as the cost of materials used for “conversion, purification, or recycling” of the raw material, would not count toward production costs.[2] This impacts both processing and recycling companies, as many in the industry have pointed out in comment letters to the Treasury Department. Li-Cycle, an emerging lithium-ion battery recycling company, stated that “the direct cost to acquire recyclable feedstock and the indirect cost to acquire reagents used in the processing of recyclable feedstock are the predominant materials costs associated with battery recycling.”[3] When it comes to processing, Tesla noted, “the key driver of processing costs is the cost of raw materials, which represent over three quarters of the levelized costs per ton of refining.”[4]Albemarle, a leading lithium producer, estimated that “direct and indirect materials costs currently represent upwards of 70% of sales price.”[5]

Collectively, this means that 45X does not support domestic mining and severely limits support for recycling and processing.

What is the Treasury Department’s current view on critical mineral production?

The Treasury Department has stated that the rule is written to ensure there is no double counting along the mineral supply chain and that the credit goes only to value-added activities. The rule notes that Treasury wants to “provide a credit for the costs associated with production activities that add value to the applicable critical mineral.”[6] However, the extraction of material from the ground and the process of turning it into a concentrate adds significant value.

Additionally, deputy treasury secretary Wally Adeyemo has stated that the credit is not meant to support the purchase of minerals from foreign sources.[7] This is in line with the administration’s goals as well as with other rules within the IRA. However, a “Buy America” or Free Trade Agreement (FTA) clause—as used in the IRA’s electric vehicle (EV) subsidies—could ensure that material costs are included without benefitting China or other competitors. Adopting this approach would qualify the purchase of minerals from US or FTA producers for the PTC.

What is the response to the proposed rule?

The proposed rule has elicited strong criticism from a coalition of miners, automakers, and battery recyclers, as well as some senators who voted for the IRA. Nine senators who caucus with Democrats have written to the Treasury Department requesting the rule be revised to align with “the intent of Congress.” They explicitly stated that “raw materials costs were never intended to be excluded from this calculation.”[8]

More than 40 battery supply chain stakeholders, including General Motors and Tesla, have also signed onto the letter, stating that the current proposed rule “will curtail future domestic supply, worsening an increasing minerals bottleneck.”[9] Many participants at a recent Chatham House rule event with industry stakeholders, cohosted by the Center on Global Energy Policy (CGEP), echoed this belief—with mining companies, mineral processors, and automakers agreeing that limiting 45X limits the growth of the battery supply chain in the United States.

However, environmental groups and progressive organizations are urging the Treasury Department to continue to exclude mineral extraction from the tax credit. For example, the Center for American Progress believes that the congressional intent was to expand mineral processing and that mineral processing is more important than domestic mining.[10]

What is at stake with the current rule?

The Treasury Department’s final rule proposal could have a profound impact on the United States’ ability to build a domestic mining and processing supply chain. Just as 45X is already helping to expand the solar and battery industry, the tax credit would support domestic producers that face a severe cost disadvantage compared to Chinese companies, not to mention the decades-long head start Chinese companies have over American producers.

It is important to view 45X in conjunction with another other IRA tax credit, the Clean Vehicle Tax Credit, or 30D. 30D provides a $7,500 tax credit for the purchase of a qualifying EV. Automakers must source the critical minerals needed for their vehicles’ lithium-ion batteries from the United States or an FTA country to qualify for the credit. Additionally, the minerals cannot be produced by a company controlled by a Foreign Entity of Concern (FEOC), notably China. The Treasury Department issued stringent FEOC guidance, making it difficult to source qualifying critical minerals. Elsewhere, the authors have called this a “bet” on the US and its partners quickly ramping up production of critical minerals. However, the 45X guidance makes that bet more challenging. According to Piedmont Lithium, which is considering moving its two planned lithium processing facilities abroad, “without the 45X credit, many of the critical mineral projects being planned for the U.S. will likely relocate abroad.”[11]

Permitting issues, price volatility, and increased costs of mining in the United States make domestic mining and mineral processing difficult compared to other countries, especially China. 45X could play a considerable role in making domestic production more economical and allow for more EVs to qualify for the 30D tax credit. It is also important to note that US domestic mineral production is cleaner, and hence costlier, than in many other countries. Financial support to offset the extra costs while maintaining environmental standards would ensure a more sustainable energy transition.

What is the path forward?

The proposed rule is only one stage in the policymaking process. In testimony before the Senate Committee on Energy and Natural Resources in January, Deputy Secretary Adeyemo said the administration wants input from stakeholders to create a final rule that provides the right incentives, including for mining.[12] The open comment period ended in mid-February. Now the Treasury Department will engage with stakeholders, and will provide a final rule later this year.

The Treasury Department’s final rule will provide insight into the Biden administration’s view of the battery supply chain. Adding extraction to 45X would demonstrate that the administration wants to support domestic mining, along with the other supply chain segments, just as it has financially supported mines through the Defense Production Act.[13] The current proposal supports the downstream, higher-value segments of the supply chain but eschews mining. As written, 45X suggests that US companies source raw materials from international locations with potentially lower environmental, social, and governance standards, and have the US be a home for mineral processing. Still, even this amounts to half-hearted support for the domestic industry if the rule continues to exclude material costs.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[2] The rule states that production costs that could be included include “labor, electricity used in the production of the electrode active material, storage costs, depreciation or amortization, recycling, and overhead.”

This paper proposes a de-risking framework of policy interventions to provide the risk allocation, revenue certainty and delivery confidence required by mainstream private finance.

This paper examines the trade dimensions of the policy instruments employed by the United States to secure critical minerals supply chains. Drawing on policy statements, executive orders, tariff schedules, and six bilateral critical minerals agreements announced in 2025, it assesses how US trade policy has been repurposed to advance supply-chain security objectives. The paper finds that recent US initiatives reflect bipartisan trends in reconfiguring trade policy that predate the Trump administration, even as they introduce new and consequential trade coordination mechanisms that operate outside the World Trade Organization and beyond conventional free trade agreements. Specifically, US critical minerals security strategy now relies on a differentiated set of sector-specific arrangements that combine familiar elements of US international economic engagement with more novel features that increasingly utilize trade policy instruments. What distinguishes these six minerals deals is their systematic coupling with parallel reciprocal trade negotiations, their incorporation of an explicitly ‘America First’ approach to reciprocity, the absence of a clear ideological hierarchy among partner countries, an emphasis on domestic processing and industrialization, and the growing use of exclusion mechanisms targeting third-party actors. The recurrence of these novel elements across diverse minerals deals suggests deliberate design rather than ad hoc experimentation that may have durable restructuring effects across global mineral supply chains. The paper concludes by outlining implications for US policy makers, for partner countries—particularly mineral-producing low- and middle-income economies—and for the architecture of the global trading system.