This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The Center on Global Energy Policy (CGEP) at Columbia University SIPA today announced new personnel additions who bring extensive experience from government and the private sector to the...

Announcement• July 3, 2025

Energy Explained

Get the latest as our experts share their insights on global energy policy.

The European Commission (EC) published a proposed regulation on June 17 to end Russian gas imports by the end of 2027; this followed the initial roadmap to do...

The global energy landscape is shifting right now. Geopolitical tensions in the Middle East, debates about peak oil demand, and waning support for climate action in some parts...

This year, the Third Annual Energy Opportunity Lab (EOL) Forum will take place July 7th and 8th in Washington, DC, offering a chance for the Washington policymaking community...

Event

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

The politically charged debate about investing based on environmental, social, and governance (ESG) principles has led to a fog of confusion about its merits and drawbacks.[1] Claims and counterclaims about ESG—often without supporting evidence—are obfuscating the reality. Two such claims are that ESG has impeded oil and gas firms’ access to capital and increased their cost of issuing debt.[2] At present, evidence of restricted access to financing for oil and gas companies due to financial institutions’ ESG considerations appears scant at best.[3] This post addresses the second claim regarding the cost of issuing debt for these companies: While ESG investing appears not to have hindered access to capital for oil and gas companies, could it have resulted in a higher borrowing cost for these firms? So far, evidence shows that the answer is no.

Everything Is Relative

The economic recovery that followed the 2020 contraction combined with supply chain disruptions led to a sharp increase in inflation globally, which was worsened by jumps in fuel and food prices following Russia’s invasion of Ukraine last year. As a result, central banks around the world have been on a path of raising rates to address inflation, leading to globally higher costs of borrowing (i.e., higher bond yields) for all entities—sovereigns and corporations alike. Therefore, comparing the current yields of oil and gas companies with those in the past would not be meaningful, as it would show rising costs for all.

On the other hand, analyzing the bond yields of the oil and gas sector relative to a broad fixed-income market index would provide more useful information. If there was a widely followed index of oil and gas bonds, the ideal tactic would be to see if the spread (i.e., yield difference) of this index over a broad bond market index—for example, the Bloomberg Global Aggregate Index (Bloomberg Agg),[4] which is one of the most popular benchmarks for fixed-income investors—reflects any trends that can be attributed to the rise of investors’ ESG considerations. As it turns out, there are not too many oil and gas bond indexes—at least not used widely as benchmarks by investors—which somewhat complicates the analysis.

Filling the Hole

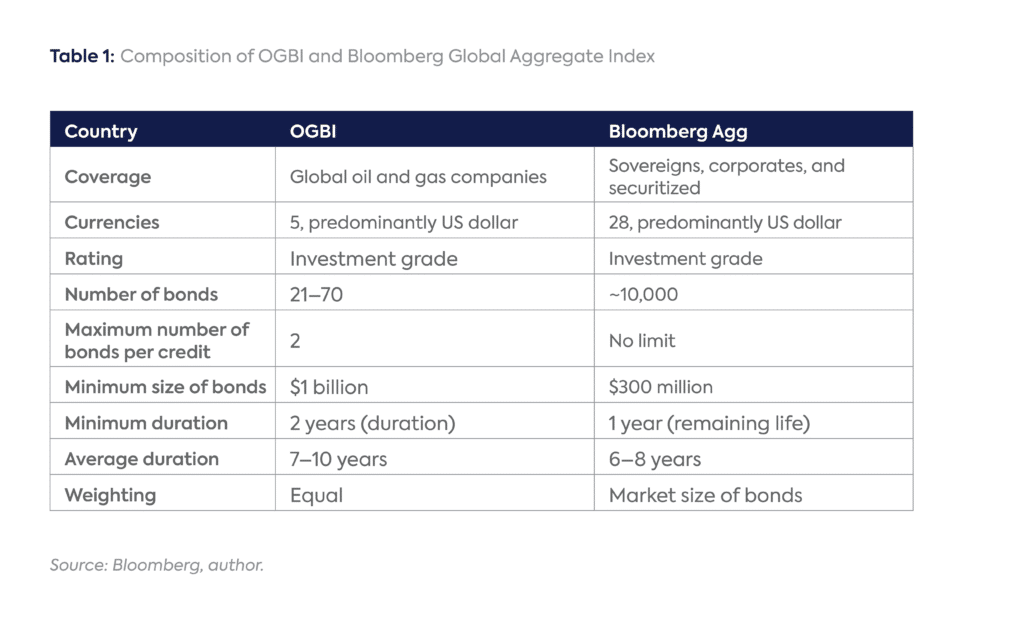

With no obvious index to use, the next best option is to construct an oil and gas companies’ bond index (OGBI) to analyze its spread. Creating an index is no trivial exercise as it involves following rules for inclusion and exclusion along with periodic rebalancing. With the purpose of drawing broad conclusions from the index while keeping the exercise as simple as possible, the metrics used to construct it were ratings, liquidity, duration, and diversification (see Table 1).

Because the duration of OGBI differs from that of Bloomberg Agg and the durations of both vary with time, the spread cannot be computed as a simple difference between the yields of the two. To correct for the slope of the yield curve attributable to the duration difference between the two indexes, the easiest approach is to first compute the spread of each index over a duration-matched US Treasury yield.[5] The difference between the spreads over the US yield curve of the two indexes (i.e., OGBI over Bloomberg Agg) is then a measure of the excess yield commanded by the oil and gas sector.

Driving Spread or Along for the Ride

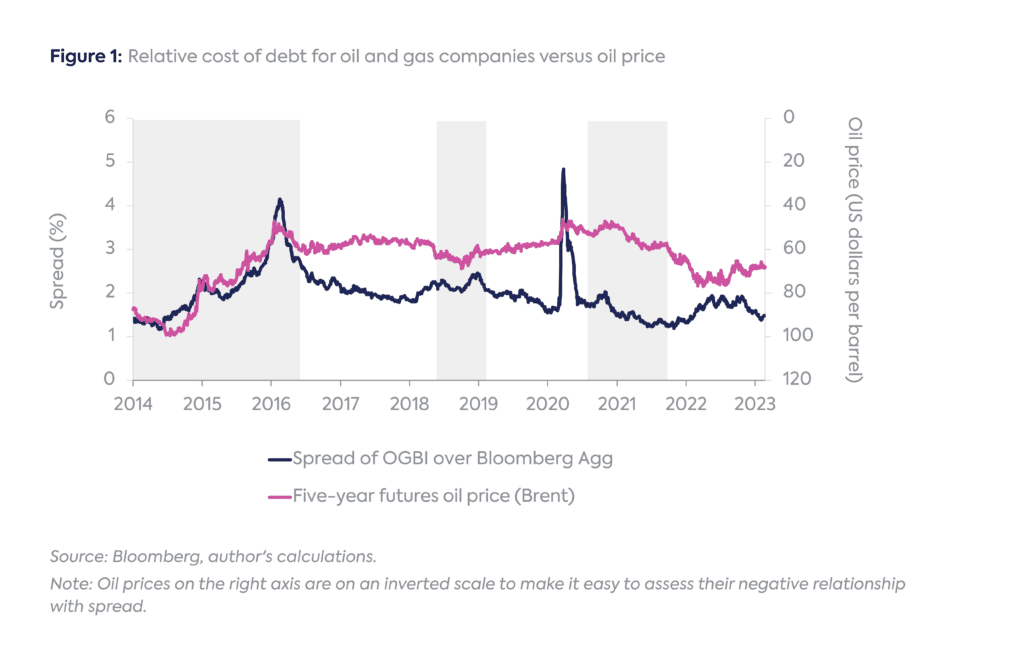

The spread of OGBI over Bloomberg Agg isolates risks related to the oil and gas sector, which should be related to oil prices. In general, one would expect a higher oil price to lead to a tighter spread—that is, better relative performance—of OGBI: all else equal, higher oil prices should increase the profitability of these companies, leading to improved creditworthiness in the eyes of investors. The spread should thus be expected to have a negative relationship with oil prices.

Plotting the spread against the five-year forward oil prices—as institutional investors tend to focus on the long-term outlook for oil rather than on its near-term gyrations—shows that oil prices and the spread, as expected, exhibited a negative relationship from 2014 to mid-2016, mid-2018 to early 2019, and from mid-2020 to late 2021 (shaded areas in Figure 1). At other times, though, the relationship between the two is either indeterminate or sometimes even reversed. Almost certainly, other drivers are at play as well.

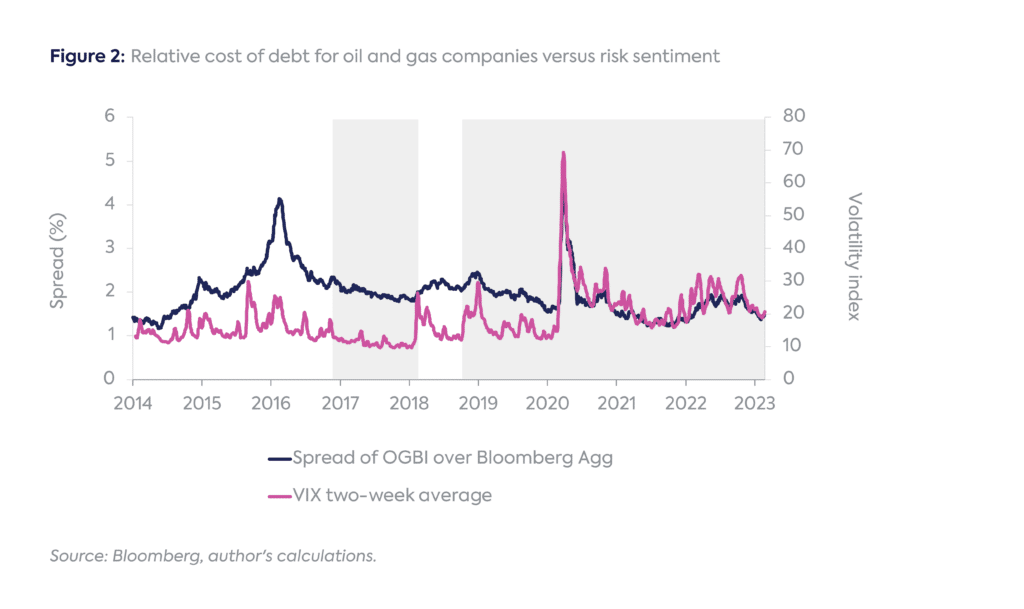

One such driver is the overall market risk sentiment. Since OGBI is a risk asset (i.e., it trades at a yield higher than risk-free rates), one would expect its demand to have a positive relationship with risk appetite. Using a broad market volatility index (VIX) as a proxy for risk sentiment (more accurately, its two-week average to reduce the noise in daily data; the lower the risk appetite, the higher the market volatility, typically) shows that the OGBI spread moved more or less in line with changes in risk tolerance between mid-2016 and 2017 and has since late 2018 (shaded areas in Figure 2).

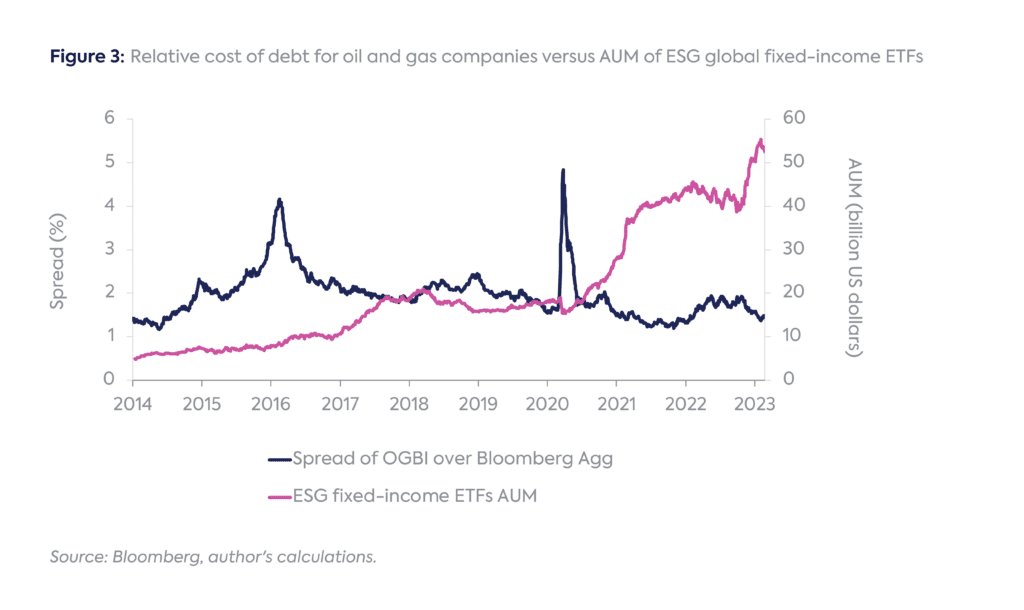

If investing based on ESG criteria had a damaging impact on the cost of issuing debt for oil and gas companies, one would expect to see their spread increase with time as the share of ESG-integrated funds has been growing rapidly within the total assets under management (AUM). However, the spread of investment-grade oil and gas companies over the Bloomberg Agg has remained in a relatively narrow range of 1.2–2.5 percent since 2017, with no specific trend (barring a brief spike during the second quarter of 2020, when economic uncertainty due to the pandemic was at its worst). Moreover, the current spread of 1.5 percent is close to the low end of the range.

Almost all of the spread movements of OGBI appear to be a function of oil price and/or risk sentiment. In particular, since mid-2020, trends in the spread have closely mirrored shifts in risk sentiment. This period is critical since it overlaps with the spectacular growth of funds incorporating ESG criteria, with assets under management in the US reaching $8.4 trillion in 2022.[6] If there were an impact from ESG, it would have been felt during this period.

Instead, changes in the assets of ESG fixed-income exchange-traded funds (ETFs)—which should be representative of the full universe of such funds since they are a microcosm of it—have had an inverse relationship with the OGBI spread at least since 2018 (Figure 3). For example, the sharp increase in ESG fixed-income ETF assets in early 2021 and late 2022 coincided with the OGBI spread tightening!

Considering trends in risk sentiment and ESG AUM, it appears that both ESG assets and the OGBI spread have been reacting to shifts in risk sentiment since late 2018. This implies that ESG is playing no discernible role in influencing the debt cost of oil and gas companies.

Can this relationship change in the future as funds integrating ESG criteria continue to grow? It’s possible, but investors are well aware of the expected growth of ESG funds and their potential impact on investments in oil and gas companies. If increasing ESG funds were a concern for the market, it would already have been priced in long-term yields. With the average remaining life of OGBI of over 10 years, its yields would already be reflecting this concern, but there is no evidence of it.

Clearing the Fog

The only way to cut through the noise in hot-button debates—like the one on ESG—is by supporting or debunking claims with analysis. This post offers one such investigation and finds that current evidence indicates that the growth of assets under management of funds with ESG mandates is not raising the cost of debt for investment-grade oil and gas companies. ESG factors could be playing a greater role in high-yield companies, which by definition are weaker credits and are therefore vulnerable to added risks. Exploring the debt costs of these companies could help gain a fuller picture of the impact of ESG. Regardless, based on the estimate that roughly 70 percent of the outstanding debt of oil and gas companies is investment grade, the evidence so far shows that ESG is not materially impacting the cost of issuing debt for these firms.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

The European Commission (EC) published a proposed regulation on June 17 to end Russian gas imports by the end of 2027; this followed the initial roadmap to do...

Saudi Arabia’s recent moves into the liquefied natural gas (LNG) market may be a sign the giant oil exporter is looking to expand into a rapidly growing and politically influential market it had long ignored.

The Trump administration may release a blueprint for a US sovereign wealth fund (SWF) in early May after the president signed an executive order in February giving the Secretary of the Treasury and the Secretary of Commerce 90 days to develop a plan.

Over the past few decades, liquified natural gas (LNG) trade has evolved from the initial point-to-point business model of the 1960s to become more flexible.

The Climate Finance (CliF) Vulnerability Index is designed to provide a comprehensive understanding of climate vulnerability for nation states in order to improve the targeting and provision of climate change adaptation financing.