Everyone Wants in on Brazil’s Rare Earths

But is Brasília ready to meet the moment?

Get the latest as our experts share their insights on global energy policy.

The Center on Global Energy Policy is providing live updates on key developments related to the Iran crisis. Check back here for the latest.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Grid operators sit at the center of many of the biggest forces reshaping the global energy system. They’re navigating rising electricity demand, a lack of transmission infrastructure, shifting...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

On June 2, Mexican citizens will head to the polls to elect the successor to President Andrés Manuel López Obrador. Among the most confrontational points of contention between the candidates has been how to handle Petróleos Mexicanos (Pemex), which is so overwhelmed by debt and lower-than-projected crude oil production that posting a net profit is attainable only through government support via tax incentives and capital injections. The candidate from the governing coalition pledges[1] to double down on the policy of the current government to increase production of petroleum products and grant Pemex (and state utility CFE) a prime market role. Meanwhile, the opposition candidates argue for greater involvement of private firms in the energy sector and downsizing Pemex refining capacity.[2] Regardless of which candidate or policy approach prevails, the task of turning Pemex into a profitable organization that can stand on its own cannot be left unaddressed. Since the opportunity cost of keeping Pemex on the current path is too high for Mexico (and the next government), it is important to shed light on the company’s challenges, which this blog discusses through six charts covering financial performance, the growing liabilities and debt, fluctuating capital expenditure levels, and the struggles around crude oil and refining production.

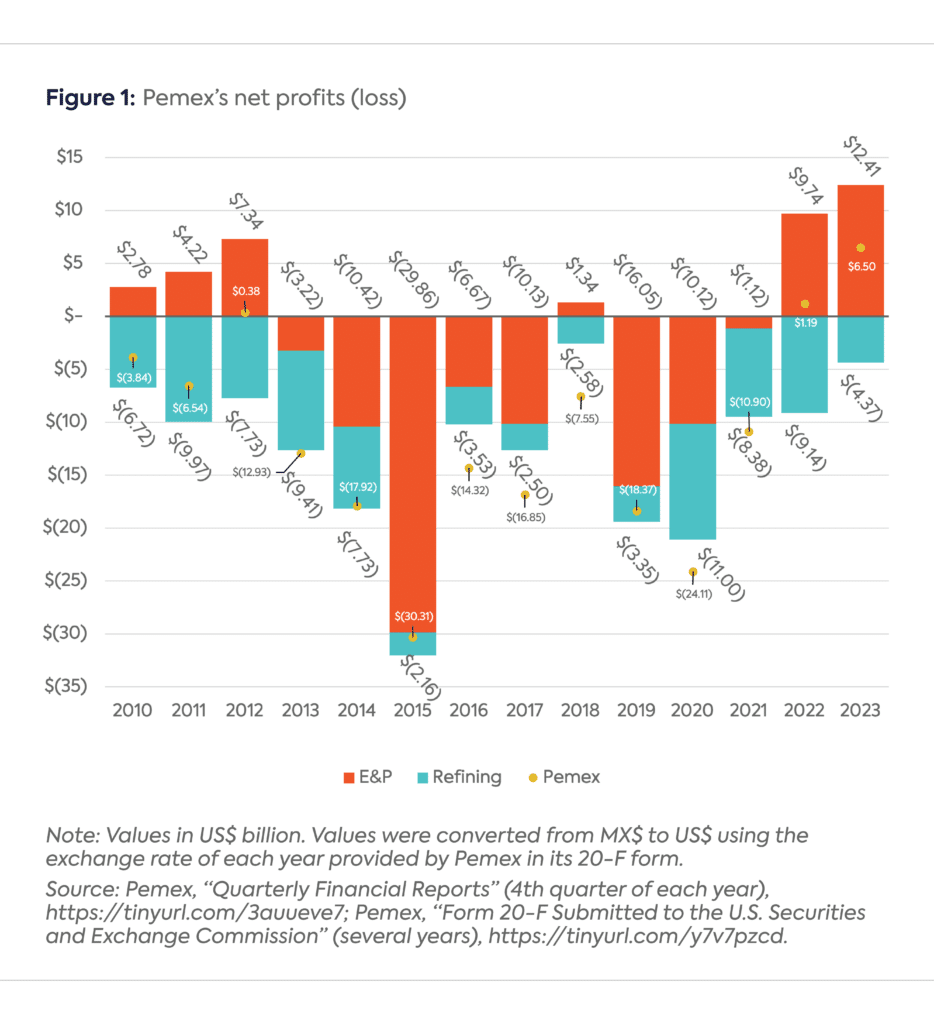

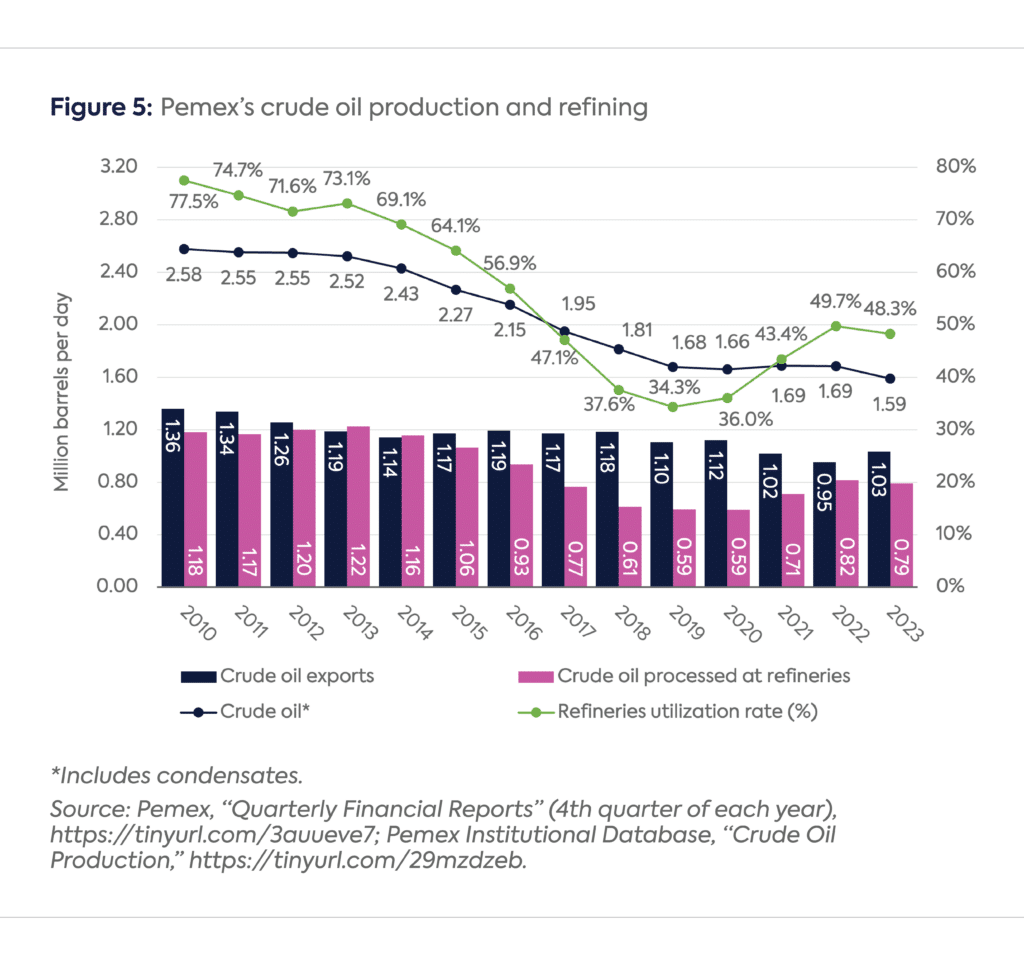

Pemex has registered net profits in only three of the past 14 years—2012, 2022, and 2023. The company’s lack of positive results can largely be attributed to high levels of debt, declining crude oil production, and fluctuating international crude oil prices. Moreover, the refining division of Pemex posted consecutive losses between 2010 and 2023 despite high utilization rates (Figure 5) between 2010 and 2014 (73.2%) and a favorable policy environment in more recent years. This has dragged down the company’s overall financial results. Policymakers have yet to formulate a solution to optimize Pemex’s existing refineries. In fact, operative inefficiencies in every corner of the company have been left unchecked for so long that the company is simply not positioned to capitalize on opportunities such as high oil prices when they arise.

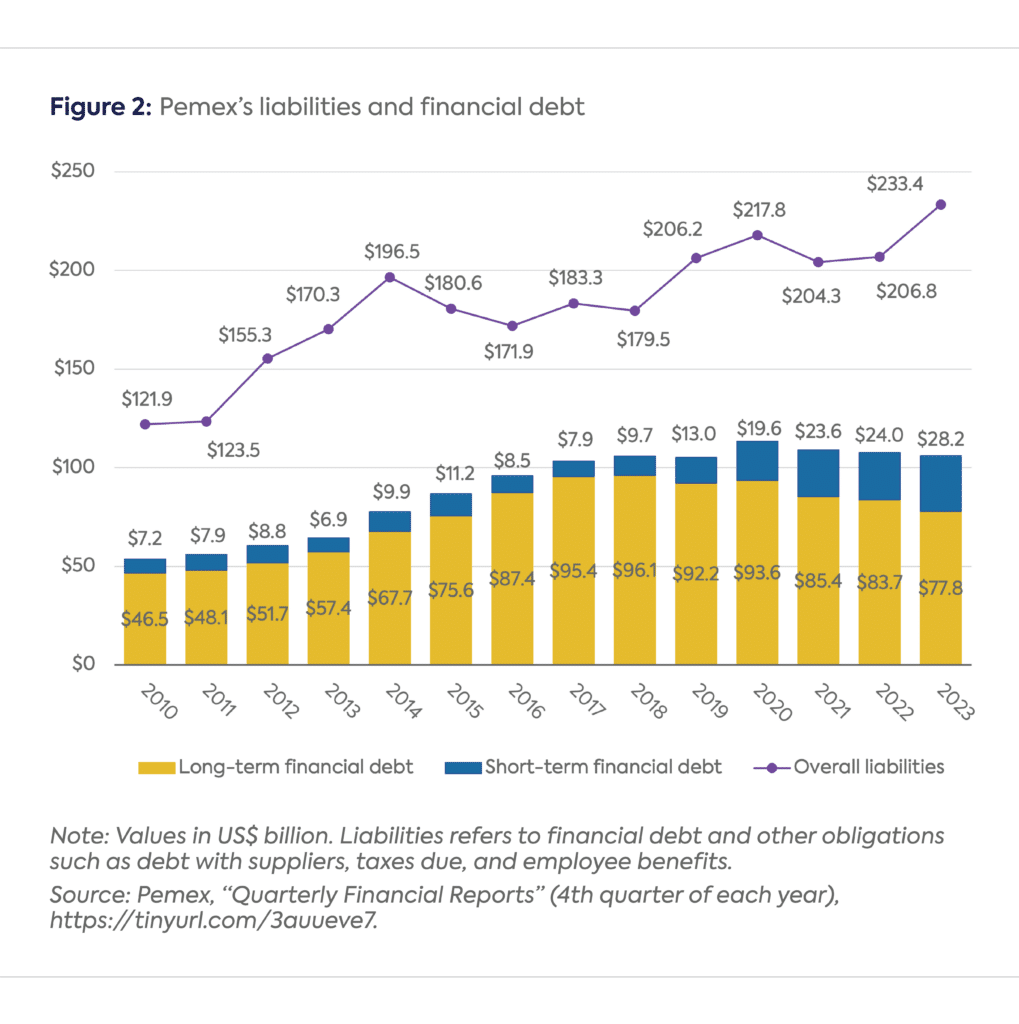

The extent to which Pemex’s financial condition has worsened over the years is evidenced by the substantial increase in the value of its overall liabilities from $121.9 billion in 2010 to $233.4 in 2023. To put this latter figure in context, if Pemex were a country, its liabilities would stand as the seventh largest economy in Latin America.[3]

Often relied upon to finance public spending, Pemex has also amassed staggering financial debt, earning it the reputation of the world’s most indebted oil company.[4] Between 2010 and 2018, the company’s total financial debt surged from $53.7 billion to $105 billion, where it has more or less remained since. Perhaps more pressing, its short-term financial debt almost tripled from $9.7 billion in 2018 to $28.2 billion in 2023.

Despite frequently renegotiating its debt[5] and receiving capital injections from the government[6] to prop up its finances, Pemex’s balance sheet remains troubled. This year is poised to be particularly complex, with Pemex anticipated to pay $28.16 billion to creditors, which corresponds to 26.54% of its total financial debt. The lingering question is whether Pemex will be able to cover its expenses, especially given López Obrador’s stated need to allocate additional resources to completing his major infrastructure projects (the Olmeca refinery and the Maya Train) before leaving office.[7] This context suggests that Pemex will continue to require government support—whether tax relief or capital injections.

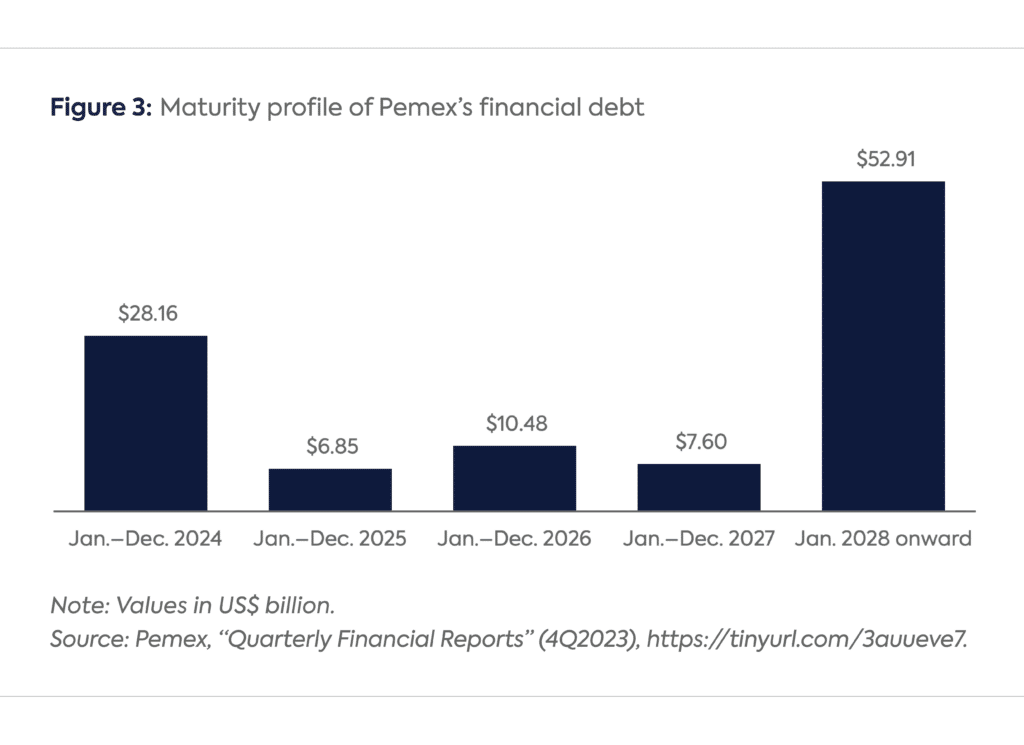

Looking beyond 2024, Pemex’s financial outlook continues to be challenging. Pemex financial debt maturing between 2024 and 2027 amounts to $53.09 billion, around half of its 2023 financial debt. Given the Mexican government’s tight finances[8] and global challenges that tend to affect the hydrocarbon sector—often unexpectedly—it remains to be seen whether Pemex can generate enough cash flow to fulfill its commitments.

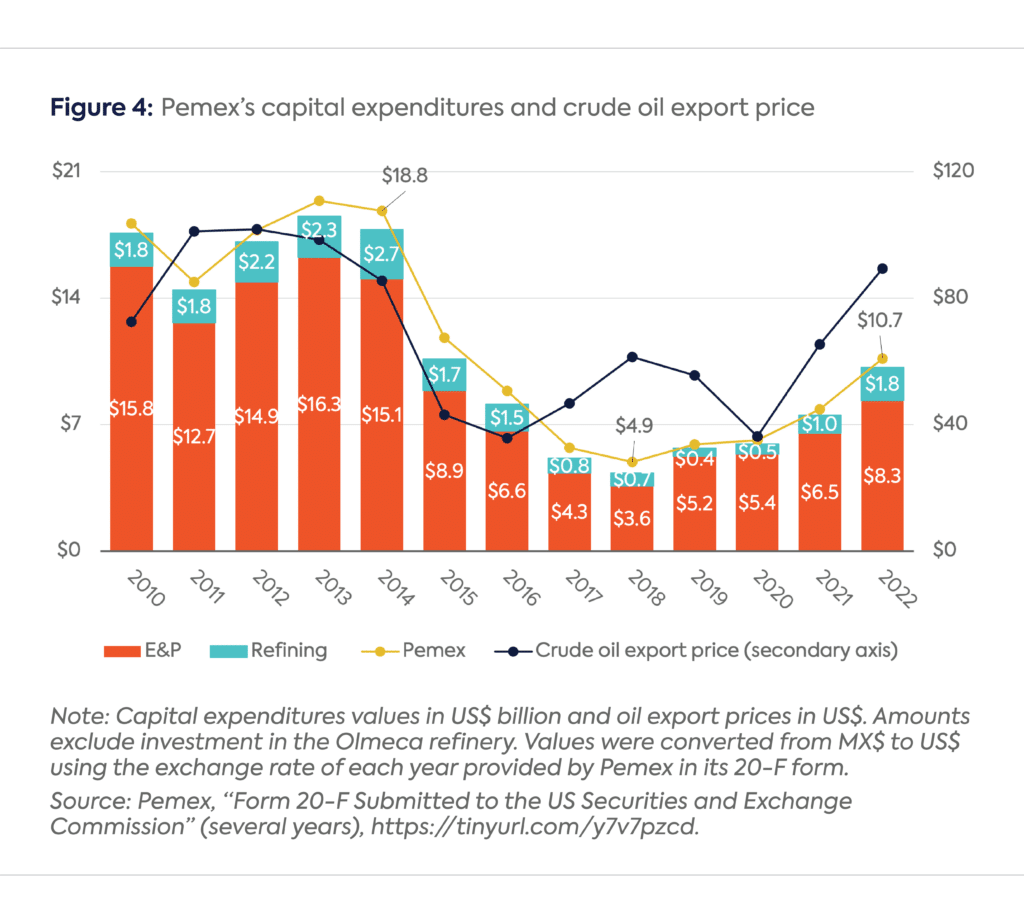

Between 2010 and 2014, Pemex benefited from high oil prices and robust crude oil domestic production, allowing for relatively high levels of capital expenditures. But the subsequent fall in international oil prices forced significant investment cuts across all operational activities from 2014–16. Oil prices recovered in 2017 and 2018, but the company’s capital expenditures remained low. Although investment has surged since then, it remains below values reported in the early 2010s. In 2018–22, Pemex yearly capital expenditures averaged $7.1 billion, down from a yearly average of $17.8 billion in 2010–14.

Refining has been at the center of López Obrador’s energy policy. But there are lingering doubts about the level of investment directed toward increasing production and the outcomes of that investment. While refinery production has surged since 2019, capital expenditures at operating refineries during the present administration are less than half of those during the previous administration, shrinking from an average of $2.045 billion per year in 2013–16 to $0.97 billion in 2019–22. This decline helps explain why as of 2023 production and capacity utilization rates at refineries remain below official expectations.

Refining operations stand out as Pemex’s most critical shortcoming. Utilization rates below 50% and persistent net losses highlight the company’s struggle to optimize operational efficiency across its six domestic refineries. Despite the Mexican government’s attempts to intervene over the last five years by, for example, sending larger volumes of crude oil to refineries, production increases have fallen short of expectations, raising doubts about the efficacy of the strategy implemented through 2023. Notably, energy self-sufficiency, a key goal of Mexico’s government, remains elusive.

Crude oil production is another area of concern. While the current administration can be credited with slowing down the pace of decline registered in previous years, production increases (excluding condensates) have not been achieved. Between 2018 and 2023, crude oil production shrank by 0.22 million barrels per day (MMbd), or 12%.

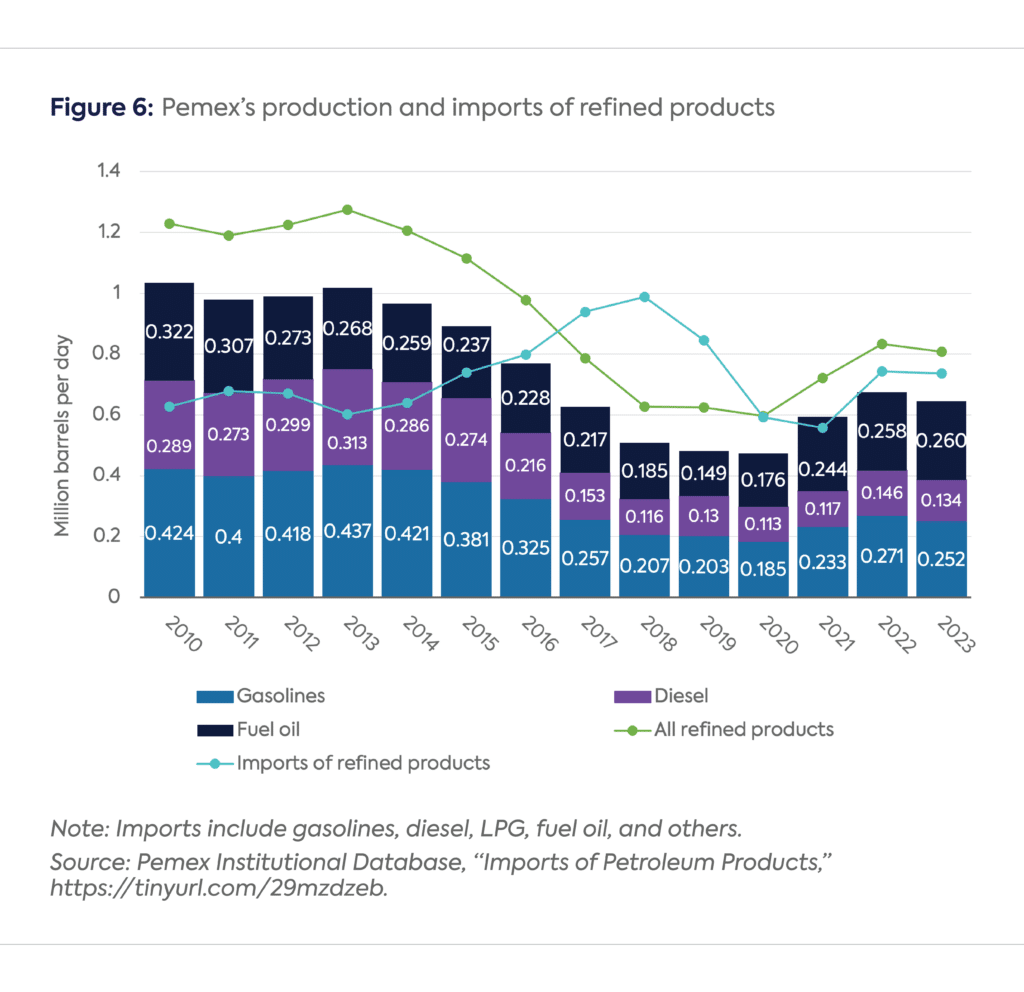

After years, if not decades, of policies that have prioritized upstream activities over transformation processes (refining and petrochemicals), Mexico gradually became a net importer of petroleum products, which means that, contrary to conventional wisdom, it now resembles a consumer market and no longer a producer (and exporter) of energy commodities. While Pemex production of petroleum products such as gasolines and diesel has increased since 2018, it is not to an extent that can meaningfully ease the country’s reliance on imports, which, as noted in Figure 6, dropped from 0.988 MMbd in 2018 to 0.736 MMbd in 2023. Mexico’s growing trade deficit in petroleum products since 2015[9] and its current status as the largest export market[10] for the US refining (and natural gas) industry are reflective of this disadvantageous market position.

Mexico’s presidential campaign has certainly cast light on the pressing need to address Pemex woes. As citizens go to the polls on June 2 to elect a new leader, it is important to look at Pemex with a forward-thinking strategy that prioritizes objectives concerning profitability and sustainability. Collaboration with the private sector, a renewed focus on crude oil exploration and production, and implementation of robust governance practices are among the measures that could help the next government pave the way for Pemex’s emergence as a more dynamic force in the country’s energy and economic landscape. In sum, the policies instrumented by the incoming president could not only shape the production and financial prospects of Pemex but also play a pivotal role in steering Mexico toward a more resilient and sustainable energy future.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] Claudia Sheinbaum [@Claudiashein], Les comparto las líneas generales de una República soberana y con energía sustentable, tweet,March 18, 2024,https://tinyurl.com/bdf85hex.

[2] Kathrine Schmidt, “Mexico Election’s Energy Transition Focus,” Energy Intelligence, March 26, 2024, https://tinyurl.com/6e9mu52s; Yared de la Rosa, “Gálvez y Máynez coinciden en el cierre de refinerías; AMLO responde,” Expansión, March 10, 2024, https://tinyurl.com/4nwf6f8y.

[3] Only Brazil, Mexico, Argentina, Colombia, Chile, and Perú boast a GDP (in current prices expressed in US$) larger than the value of Pemex liabilities in 2023. International Monetary Fund, GDP per country (current prices), https://tinyurl.com/jhuz3vut.

[4] “Pemex Is the World’s Most Indebted Oil Company,” Economist, October 12, 2023, https://tinyurl.com/4rbx4z58.

[5] Ana Isabel Martínez, “Mexico’s Pemex Places $2 Billion Bond to Refinance Debt,” Reuters, January 31, 2023, https://tinyurl.com/5n85m3f6.

[6] Eric Martin and Amy Stillman, “Pemex Get $5 Billion from Government to Boost Debt Profile,” Bloomberg, September 11, 2019, https://tinyurl.com/yc8x84ce; Tsevetana Paraskova, “Mexico Back State Oil Giant with $4 b Capital Injection,” OilPrice, July 28, 2023, https://tinyurl.com/4wbj632c.

[7] Alex Vasquez, “AMLO’s Flagship Projects Drive Big Boost in Mexico’s 2024 Budget,” Bloomberg, September 9, 2023, https://tinyurl.com/58vmxmff; Maya Averbuch, “AMLO Spends like Never Before to Set Up Successor’s Victory in Mexico,” Bloomberg, April 4, 2024, https://tinyurl.com/23ysxp7t.

[8] In 2024, Mexico’s government projects a budget deficit of 4.9% of GDP, its highest since 1988. Dave Graham and Diego Oré, “Mexico’s Election Year Deficit Plan Fuels Fear over Finances,” Reuters, September 11, 2023, https://tinyurl.com/4957ehej; Secretaría de Hacienda y Crédito Público, “Estimaciones de gasto público para 2024,” https://tinyurl.com/peeruejs.

[9] It refers to exports and imports of crude oil, natural gas, crude oil derivatives (gasoline, diesel, fuel oil, jet fuel, liquefied petroleum gas, etc.), and petrochemicals. Mexico’s Central Bank (Banxico), “Economic Information System, Historical series of petroleum products trade balance,” https://tinyurl.com/9z2v5x3z.

[10] US Energy Information Administration, “US Exports of Petroleum Products and Other Liquids,” https://tinyurl.com/mv2ex5du; US Energy Information Administration, “US Natural Gas Exports by Country,” https://tinyurl.com/3rp8fruc.

Critical minerals were once again near the top of the agenda for G7 leaders as they met in Évian, France, this week, a year after the G7 launched the Critical Minerals Action Plan.

In March 2026, the Office of the US Trade Representative (USTR) announced it was investigating "structural excess capacity and production in manufacturing sectors" in 16 economies.

The US Export-Import Bank is preparing to close the first funding tranche of Project Vault, a public-private partnership establishing the US Strategic Critical Minerals Reserve.

Two economic planning documents released at the March meeting of China's National People’s Congress include the term "energy powerhouse" for the first time.

In March 2012, Israeli Prime Minister Benjamin Netanyahu arrived in Washington to press a US president on slowing Iran’s nuclear ambitions. Inside the White House, the dilemma was stark.

Within days of the initial U.S. and Israeli attack on Iran on February 28, 2026, the world was plunged into an energy crisis.