Could a strategic lithium reserve kickstart US supply chain development?

NEW YORK -- A strategic lithium reserve is being mooted as a solution to stabilize volatile prices that have hindered American mining projects, allowi

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Over the past week, President Trump has intensified pressure on Venezuelan president Nicolás Maduro by targeting the regime’s economic lifeline—oil. The United States has seized two oil tankers...

Find out more about our upcoming and past events.

On January 1, 2026, the European Union's highly-anticipated Carbon Border Adjustment Mechanism (CBAM) will take effect. Introduced in 2023, CBAM will require the importers of certain carbon-intensive goods...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision.

Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available here. Rare cases of sponsored projects are clearly indicated.

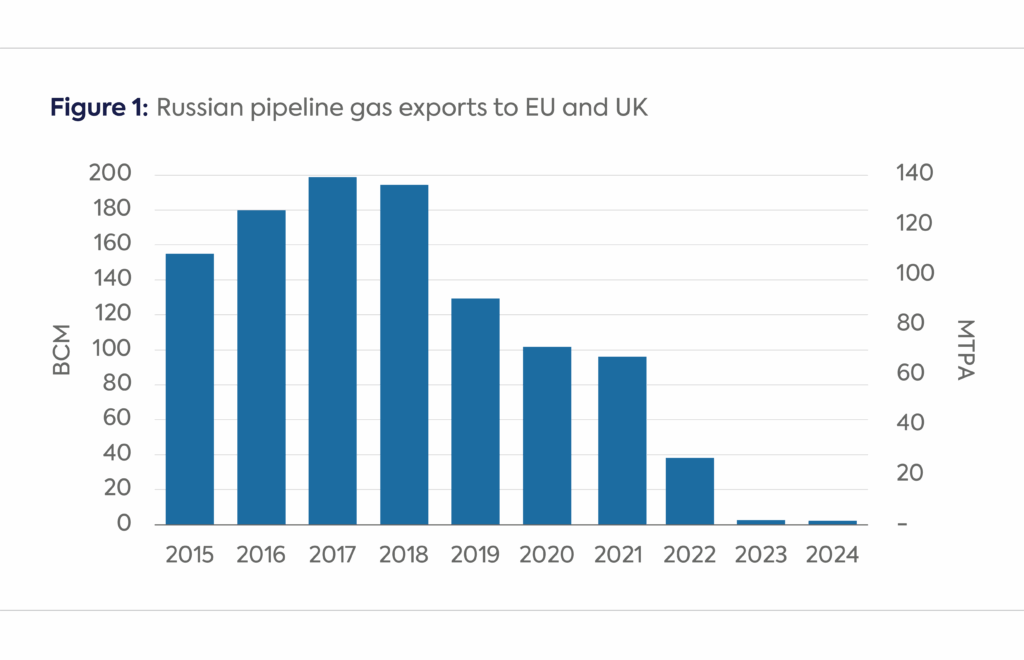

Despite producing little natural gas,[1] the European Union could become the most powerful entity in global gas markets in the decades to come. As the European Commission currently debates cutting off Russian pipeline gas completely later this decade, new LNG capacity continues to reach final investment decision status around the world. Drawing such a definitive line on the use of Russian pipeline gas seems premature at this point, given how much leverage could be gained by not drawing one. The EU’s growing influence stems from a unique position: it could cause an immense supply swing of 100–125 billion cubic meters per year (bcm/yr) of Russian pipeline imports (see Figure 1).[2] By deciding how much, if any, of this gas to allow back into its market, the EU can function like a 1970s-era OPEC, with the power to significantly raise or lower global gas prices. While the EU is taking a hard line on Nord Stream (a series of offshore gas pipelines flowing directly from Russia to Germany) ever reopening, other options remain that can provide the EU with the kind of supply flexibility any buyer would crave.

Source: Energy Institute, Statistical Review of World Energy 2025, https://www.energyinst.org/statistical-review/resources-and-data-downloads; International Energy Agency, Gas Trade Flows, accessed July 2025, https://www.iea.org/data-and-statistics/data-product/gas-trade-flows.

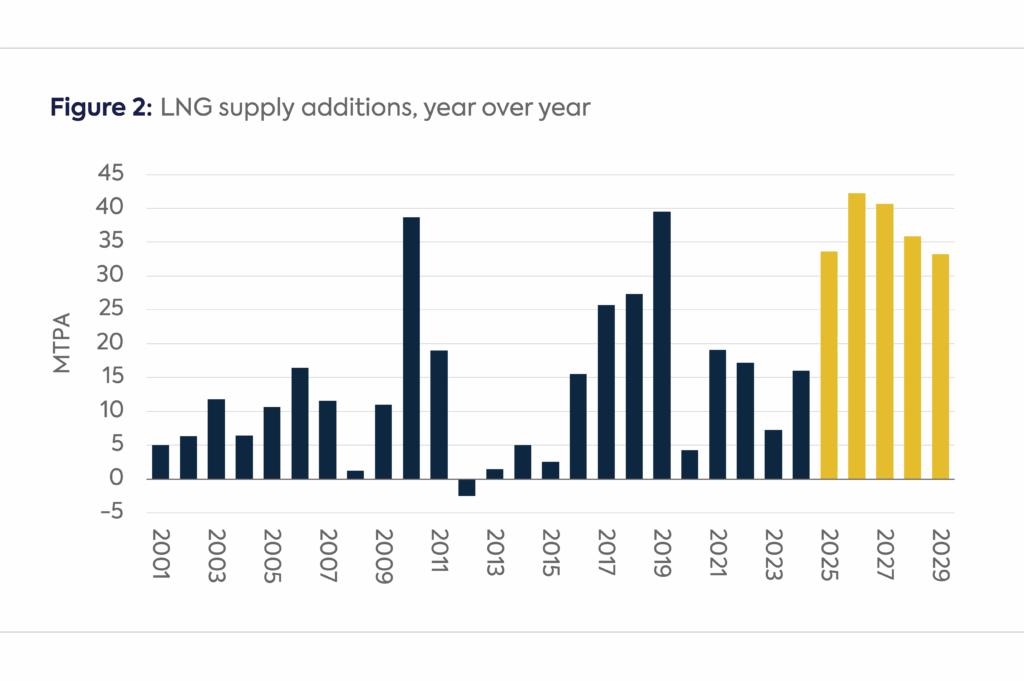

The EU’s market power is immense and growing, largely because global gas investment since Russia’s 2022 invasion of Ukraine has operated on the presumption that Russian pipeline gas exports will eventually be permanently offline. This assumption, central to policies like REPowerEU that aim to reduce dependency on Russian fossil fuels, emboldened the LNG industry to sanction a historic wave of new projects. An unprecedented 40% increase in global LNG capacity is expected by 2030 (see Figure 2).

Soure: S&P Global Commodity Insights, LNG Contracts, accessed July 25, 2025, https://plattsconnect.spglobal.com/#platts/powerbi?dashboardName=LNGContractsPlus&tab=Tenders.

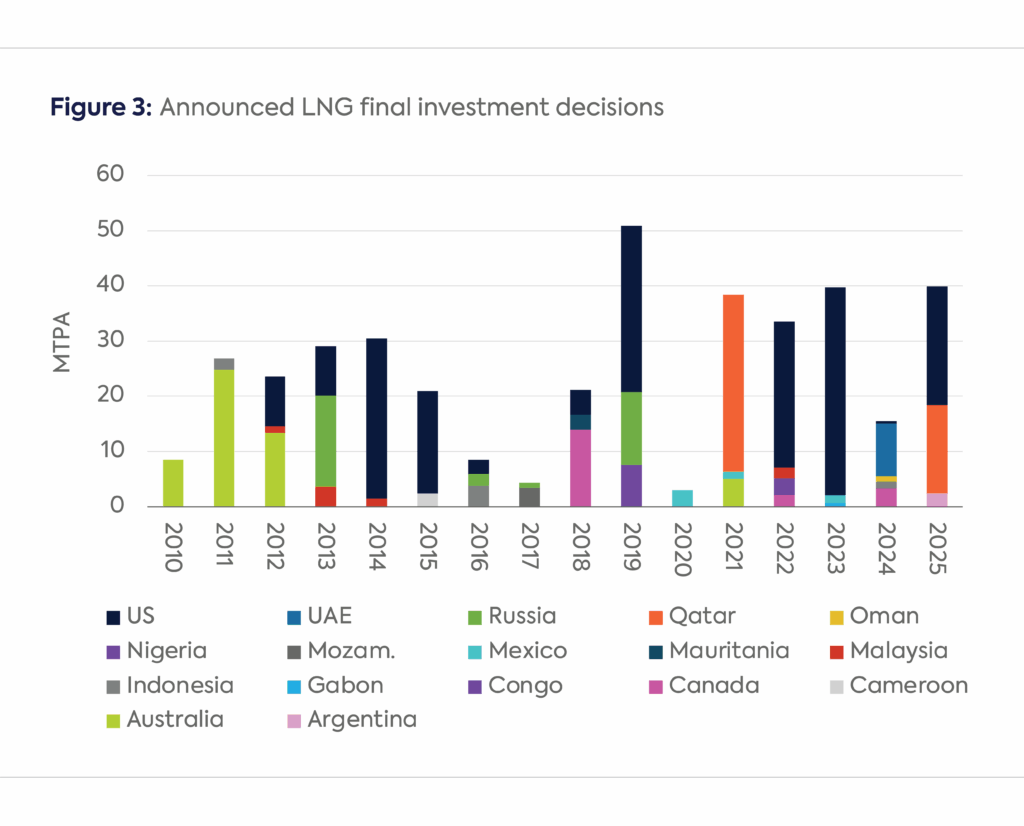

Around 40% of this new capacity had already reached a final investment decision (FID) before the invasion, but the rest was given a financial confidence boost by the loss of Russian gas. This surge in FIDs for new liquefaction capacity may create a situation where new supply outstrips market demand signals. Despite this, and the possibility of losing out to lower cost alternatives like renewables and coal, the industry does not appear to be pausing to assess when LNG demand might crest; instead, it is pushing forward to build even more. Based on quarterly reports of various companies through the first half of 2025, the author estimates that at least 75 million metric tons per year (MTPA) of LNG will reach FID status this year alone, with commissioning dates on these projects ranging from 2030 to 2036 (see Figure 3).

Note: 2025 includes year-to-date through June 30.

Source: S&P Global Commodity Insights, accessed July 25, 2025, https://plattsconnect.spglobal.com.

While the LNG industry expands aggressively, Russia still has the largest source of spare production capacity in the world, having cut its pipeline exports to EU countries by almost 90% since the war began. Reintroducing 100–125 bcm/yr of pipeline gas would be highly disruptive, flooding a European market where gas demand has declined 20% since 2021 and 27% since 2004.

The world’s highest-cost gas supply (new LNG) is now competing for the same market space as one of the world’s lowest-cost supply (Russian pipeline gas). Despite being cheap to produce, some Russian pipeline gas has been sold to European buyers at spot prices for at least one decade. The EU’s decision on Russian gas could determine whether global gas markets would be flooded or not and therefore whether spot prices in Europe and Asia sustain at $9/million British thermal units or fall to $4[3] for extended periods. This, in turn, will directly impact whether US LNG export facilities run at 90% capacity utilization or are forced down to what the author estimates would be 50%, as it will be US LNG exports on which the market will balance.

Whether as an entity or among its members, the EU is in a position to wield this power actively, by managing Russian gas flows on a short-term basis, or passively, with an “all-or-nothing” approach. A more likely outcome is a policy that caps dependence on Russian imports but allows flexibility to manage market shocks like colder-than-normal weather or an LNG supply disruption. The EU could even leverage this position, perhaps allowing a more liberalized import policy in a post-war scenario to help fund Ukraine’s reconstruction.

This ability to influence global gas balances on an active basis could rival that of state-owned giants like QatarEnergy, which, despite its own massive expansion, has historically preferred the stability of long-term contracts and not taken an active role in the spot market. Russia, of course, is not a passive actor. However, its need for political influence, revenue, and limited alternative export markets—namely relying on China or funding costly new LNG projects—constrains its leverage against an empowered EU.

The consequences of the EU’s choices are far-reaching. Cheaper, more abundant gas could slow the uptake of renewables and alter the course of the energy transition. Paradoxically, by positioning itself to control the flow of Russian pipeline gas, the EU also gains some control over the profitability and operating capacity of the burgeoning US LNG export industry, which will be forced to balance the global market until a demand response occurs in markets like Southeast Asia. Whether such a demand response is sustainable once prices rise again will be another key balancing factor going forward. With EU gas demand falling and its seasonal storage capacity rivalling the US, its emerging policy decisions that will influence how much gas the continent will need and from where it will buy it mark a major change in its relationship to the global gas market.

[1] The EU produced 12% of its own gas in 2024.

[2] Export figures do not include Turkey and its two pipelines from Russia: Turkstream (32 bcm/yr) and Bluestream (16 bcm/yr). Figure is based on current estimates of usable capacity on gas pipelines going through Poland (33 bcm/yr) and Ukraine (67–90 bcm/yr). The Nordstream pipelines, each 55 bcm/yr, are assumed to be closed indefinitely due to damage.

[3] Four dollars was the price prior to the buildup to the Russian invasion and the price at which the author estimates it is reasonable to still make money sending LNG from the US to Europe.

Geopolitical uncertainty associated with Russian gas exports could swing the range of those exports by an estimated 150 bcm per year.

As the host of COP30, Brazil has an unprecedented platform to demonstrate its climate leadership.

CGEP scholars reflect on some of the standout issues of the day during this year's Climate Week

Gulf Cooperation Council (GCC) countries have not only the world's lowest costs for oil and gas production but also the lowest costs for electricity generated from renewable energy sources.