Kuwait looks to the cloud as power grid feels the strain

Kuwait has invited bids to construct three power substations that will supply electricity to Google Cloud data storage centres

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

Venezuela holds 70% of Latin America's natural gas reserves, which it could export to Colombia and Trinidad to increase revenues.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

From the affordability crisis and the data center boom, to the US government’s campaign to reinvigorate the Venezuelan oil market, energy is dominating headlines in unusual ways. And...

Find out more about our upcoming and past events.

The Center on Global Energy Policy at Columbia University SIPA's Women in Energy initiative and Accenture invite you to join us for an evening of conversation and networking...

Commentary by Pierpaolo Cazzola • November 24, 2025

This commentary represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. This commentary was funded through a gift from G. Leonard Baker, Jr. More information is available at Our Partners.

The global automotive industry is undergoing a historic transformation. Electric vehicles (EVs)—including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs)—are rapidly gaining market share worldwide. China has experienced the deepest transformation, followed by Europe—despite considerable heterogeneity within it—and by the US.

BEVs account for most EV sales globally, but PHEVs have experienced particularly dynamic growth in recent years.[i] Once viewed as a transitional technology favored by legacy automakers, PHEVs have now become central to China’s domestic EV market growth and to its industrial strategy. Chinese automakers embraced PHEVs and extended-range electric vehicles (EREVs) as a way to complement BEVs to expand their global reach, effectively leveraging the advantages offered by a deeply rooted and competitive battery supply chain.

The overall global shift to EVs raises a critical question for US automakers and policymakers: Should EVs be defended, ignored, or strategically supported, and if so, which ones?

Because of the scale and pervasiveness of this technological transition, accelerating the shift to EVs would strengthen the resilience of the US auto sector. Instead of policies that focus solely on incremental improvements to internal combustion engine vehicles (ICEVs), those that support PHEVs, which retain an internal combustion engine, can play a transitional role to fully battery-powered cars. However, securing resilient industrial leadership will ultimately depend on advancing BEVs and reducing the risks of overdependence on concentrated battery value chains.

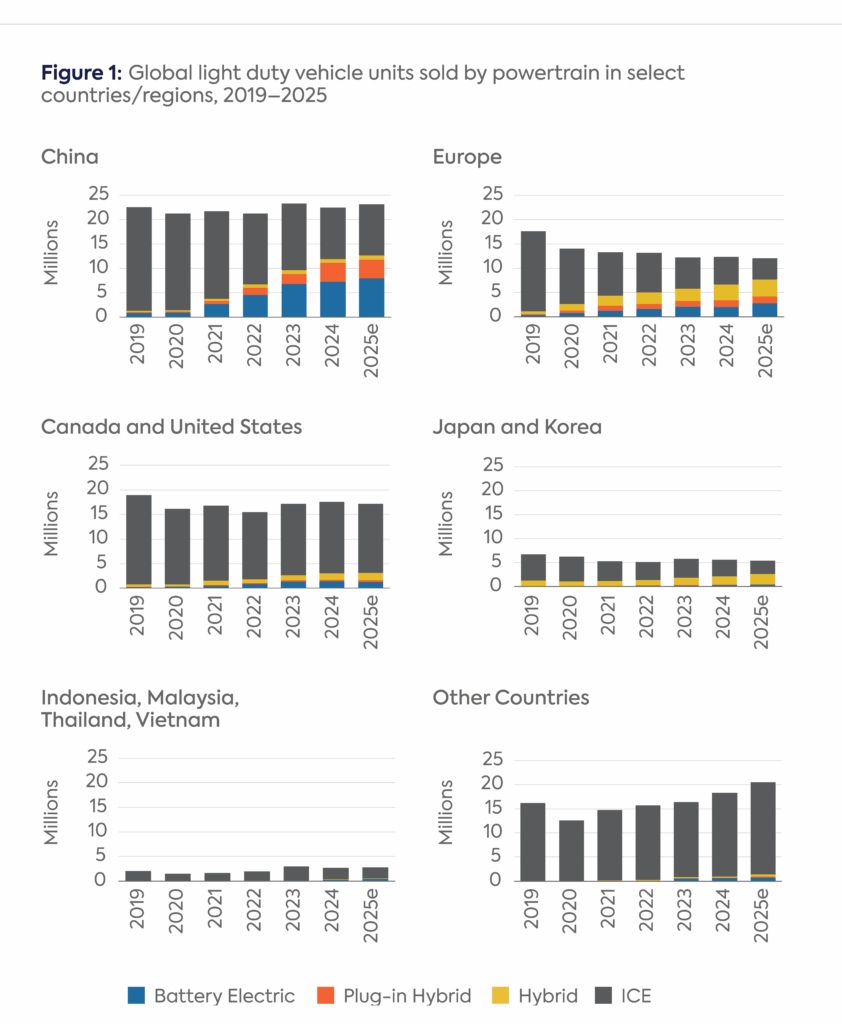

In many regions of the world, the car market has developed in markedly new directions in recent years (see Figure 1). In 2024 plug-in vehicles—both BEVs and PHEVs—accounted for roughly one in five new cars sold worldwide.[ii] Estimates for 2025 point toward increasing market share and a total of roughly 20 million electric cars sold.[iii] Yet beneath this aggregate figure lies striking regional differences in both technology choice and adoption speed.

Note: “e” indicates that the value is an estimate based on partial-year data and is therefore forward-looking.

Source: Estimate based on International Energy Agency, EV Volumes, BloombergNEF, Global Fuel Economy Initiative, European Environment Agency, European Automobile Manufacturers Association, European Alternative Fuels Observatory, Allianz, New AutoMotive, S&P Global, ING, PwC and Strategy&, JATO Dynamics and Japanese Automotive Manufacturers Association.[iv]

China has experienced the deepest transformation. In 2024 it represented about 60 percent of global EV sales, with BEVs making up the bulk of EV deliveries but PHEVs growing rapidly (see Figure 1). BYD, an automobile manufacturing company headquartered in China, led in total EV sales globally and outsold Tesla on BEVs alone in late 2024.[v] China’s grip on battery manufacturing—from raw material processing to cell production[vi]—enables low costs and high volumes across both BEVs and PHEVs.

Europe is the second key pole of electrification globally in terms of sales and domestic manufacturing, though with marked heterogeneity among countries and with remaining reliance on China in its battery value chain.[vii] Nordic countries such as Norway, Sweden, and Denmark are at the forefront of the electrification of the car fleet in the EU, with EVs, and in particular BEVs, already having high market shares.[viii] In contrast, several countries in southern and eastern Europe—including Cyprus, Greece, Italy, and much of central and eastern Europe—lag behind, constrained by lower incomes, higher sensitivity to vehicle purchase prices, and, in the case of Italy, high electricity prices.[ix] Within the EU’s regulatory framework, PHEVs have played a transitional role between ICEVs and BEVs. However, as regulatory signals and tax incentives evolve and charging expands, consumer demand is favoring BEVs.

The United States presents a different picture. EVs accounted for 10 percent of its car sales in 2024. BEVs are clearly ahead of PHEVs in terms of new car registrations, representing about 80 percent of total electric car sales that year.[x] This aligns with the outsize role of Tesla in shaping consumer preferences, brand perception, and charging infrastructure.[xi]

While some legacy automakers continue to offer PHEVs, US demand for PHEVs versus ICEVs is structurally constrained by relatively low gasoline prices, resulting in limited space for cost savings from PHEVs. The US capital market also tends to place a significantly higher premium (in terms of market capitalization per unit of vehicle sold) on companies that focus on BEVs rather than PHEVs (and other combustion-based technologies).

The Korean car market has seen EVs rise to nearly 15 percent in 2024 and 2025, with 2025 developments pointing toward an increased focus on BEVs and a stagnation of PHEV sales.[xii] Japan has a technology mix in its domestic market that remained strongly centered on ICEVs and hybrids,[xiii] in line with the focus of its main automakers and concerns about limitations in access to battery material supplies. It recorded limited EV market demand compared with other major developed economies.

From Southeast Asia to parts of Latin America and Africa, there has been a rapid acceleration in EV adoption.[xiv] Much of this expansion is directly or indirectly linked to Chinese investment, both in vehicles (via exports or local assembly) and infrastructure (including charging and battery plants). In markets such as Brazil, Indonesia, Thailand, and parts of Africa, Chinese EVs are gaining market share, while Western automakers are subject to a competitive disadvantage because they focus more on premium segments (which are less affordable) and have lower EV sales volumes overall compared with Chinese competitors.[xv] In other cases, such as Vietnam, the growth in EV market shares was paired with the rise of domestic EV manufacturers. However, they still rely, at least in part, on Chinese battery suppliers.[xvi]

In short, while EV sales are increasing globally, the global EV map remains uneven. China is leading in sales of both BEVs and PHEVs, whereas Europe has a high share of BEV purchases within its electric car market, especially in the North, with a patchier picture elsewhere. The US is BEV-heavy but has a relatively narrow overall EV share. Korea tracks EU developments, with some lag, while Japan maintains a focus on hybrids. Emerging markets are entering the race largely on the back of Chinese industrial and financial support.

The EV transition is not only about technology but also about economics, geopolitics, and climate commitments.

For China, EVs are part of a broader attempt to dominate a future-defining industry.[xvii] For Europe, they are a necessity to preserve automotive leadership while meeting climate obligations.[xviii] For the US, they represent a challenge to the legacy automotive manufacturing and oil sectors—long central to its industrial base—while at the same time offering a pathway to offset risks of net industrial capacity losses, which becomes essential if the US market also shifts toward electrification. Investments in batteries and related supply chains are not just about cars; they are also about commanding value-added industries of the future and industrial production that matters for national security and defense.

For net oil importers, EVs are a strategic hedge against oil dependence. China, the EU, India, and many African, Latin American, and Southeast Asian countries rely heavily on imported crude and refined products. Reducing oil dependence through electrification—as well as the associated energy efficiency improvements of EVs, which consume about one quarter of the final energy needed by a comparable combustion car[xix]—is therefore an economic and security imperative for countries in these circumstances.

Building a competitive battery value chain also offers resource security if it can leverage—as in the case of oil supplies—a reliable network of global partners. And contrary to oil, battery materials will become increasingly available in economies using BEVs once the vehicles reach the end of their useful life through recycling.

EV adoption is also propelled by emissions regulations, climate targets, and clean air priorities—such as China’s “new energy vehicle” mandates and the EU’s CO₂ emission standards—as EVs have lower life-cycle emissions than alternative technologies.[xx] The US corporate average fuel economy (CAFE) standard, state-level “zero emission vehicle” (ZEV) standards developed in California and other states, and other instruments supporting EV demand and infrastructure development were also driven by climate policy goals, though these are now the object of major revisions by the Trump administration.

Importantly, the strength of these three drivers varies: Concerns about energy security and industrial goals tend to reinforce each other in China and the EU, resulting in policies that have supported the EV transition. In the EU, additional synergies came from a strong determination to act on climate. In the US, abundant domestic oil has blunted the energy security case, and while climate was a clear driver of prior policy action on EVs, the current administration does not support policies addressing climate change.[xxi] Despite such headwinds, industrial competitiveness and the promotion of innovation have long been a focus of US policy, and recent trade policy decisions seem to suggest that interest remains in supporting domestically produced EVs and achieving greater diversification of battery supply chains.[xxii] However, this interest comes with a reduced pace and scale for the EV transition, and hence also with delays in emission reductions.

The role of PHEVs has evolved markedly over the past decade. In a first phase, they were mainly part of a defensive strategy by legacy original equipment manufacturers (OEMs) In a second phase, growing pressures from BEVs and increasing evidence about the limits of PHEVs to promote energy diversification and reduce greenhouse gas (GHG) emissions challenged the effectiveness of this initial strategy. A third, more recent phase is a Chinese offensive strategy to leverage its competitive advantage in batteries and gain global market share.

Initially, PHEVs were developed largely by incumbent automakers as a hedge against BEVs. Legacy manufacturers, heavily invested in ICEV platforms, saw PHEVs as a way to meet regulatory targets without committing to the cost and risk of full battery electrification. In Europe, policy incentives also encouraged this strategy.

PHEVs lost traction and policy support, however, as BEV sales grew (fueled by Tesla and Chinese pure-play EV makers) and critiques pointed to low energy diversification and climate benefits of PHEVs, which run much less than initially expected in all-electric mode. These critiques were backed by strong evidence[xxiii] and confirmed by official data collection,[xxiv] which led to policy revisions in the EU[xxv] and the US.[xxvi]

Since 2022, however, PHEVs have experienced a resurgence, especially in China. Unlike the earlier defensive stance by legacy OEMs in Europe, China’s recent PHEV surge reflects a more offensive strategy. With world-leading battery production, Chinese OEMs such as BYD have launched PHEVs with large batteries and long electric ranges—including in the form of EREVs—ensuring more frequent all-electric operation. Domestic demand soared because of total cost of ownership advantages compared with ICEV, partial eligibility for preferential licensing in Chinese cities,[xxvii] improvements in battery technologies needed in PHEVs,[xxviii] and the introduction of new models with larger batteries and fast-charging capabilities.[xxix] Lower upfront prices for PHEVs compared with BEVs in a few market segments[xxx] may also have played a role. Consumer interest in the flexibility that PHEVs offer compared with BEVs may also have supported demand growth, especially where there is limited cost-effective charging infrastructure.[xxxi] Importantly, exports of PHEVs and EREVs can also provide an avenue to bypass tariffs or countervailing duties, as those tend to focus on BEVs.

By now the fulcrum of PHEV market development has shifted decisively to China. What was once a transitional technology favored by legacy Western OEMs is now being redefined by Chinese firms as a competitive instrument, integrated with global trade strategy and industrial policy.

In the US, the structural outlook for PHEVs is limited, while the outlook for BEVs is also weaker than it was before recent policy reversals. Factors that influence market developments include the following:

In China, structural drivers behind increased electrification remain strong, despite challenges emerging from increased competition and significant overcapacity. BEVs are therefore bound to continue to account for millions of units sold, as they have in the recent past. PHEV and EREV shares may continue to expand over the next 5 to 10 years, thanks to the same drivers that favored their recent increase, both in terms of domestic demand and utility in circumventing trade barriers when supply is geared toward exports (if the focus of trade barriers on BEVs does not change). The new generation of Chinese PHEVs—including EREVs equipped with larger batteries—is also particularly well suited to meeting requirements regarding all-electric driving shares, which are now also being tightened domestically.[xxxii]

BEVs are bound to see continued market share increases in Europe. This is driven by policy, particularly the regulation requiring zero carbon dioxide emissions by 2035. It is also driven by economics, including EV technology cost reductions, high oil import dependency, high fuel taxation, the introduction of carbon pricing, and the use of differentiated taxation based on the environmental performance of vehicles, which favors BEVs.

PHEVs have faced declining incentives, especially for models with low all-electric range, because of tightened regulatory requirements.[xxxiii] They are also subject to equity-related challenges, as they have solely been deployed in premium segments, steering incentives meant to support demand creation for EVs toward wealthier people.[xxxiv]

Future policy action will remain focused on road transport electrification, as indicated by the announced proposals regarding corporate fleets,[xxxv] even if revisions to existing regulations are also being considered. Recent announcements regarding smaller, more affordable EVs will help diversify the offer of BEVs and are not likely to favor PHEVs, given their focus on larger and heavier cars.[xxxvi] However, revising the 2035 emission reduction requirements toward greater technological neutrality[xxxvii] could offer opportunities for a greater share of PHEVs in the European EV market than in the current policy framework.

In emerging markets, Chinese EVs are likely going to continue to be cheaper than those from other suppliers, especially for BEVs.[xxxviii] PHEVs may see growing demand where charging infrastructure is limited and where policy requirements for larger battery capacities and higher all-electric driving shares are not yet adopted (while Chinese EREVs can gain interest in cases where this tightening is already in place).

The outlook for Korea points toward an overall EV market share increase that remains less dynamic than in the EU, but with a strengthened focus on BEVs.[xxxix] Japan is expected to continue facing challenges in stimulating domestic EV demand.[xl] However, the export-oriented nature of Korean and Japanese automotive industries and the risks of market share losses in Asia are likely to strengthen the case for greater diversification of their power train offerings toward EVs.

Overall, and especially as batteries get cheaper and charging more widespread, BEVs are more likely to capture the bulk of the EV market growth. However, PHEVs can gain relevance as a strategy for navigating trade-related barriers and in markets that still have limited charging infrastructure. Versions with larger battery capacities are likely to gain more ground as batteries keep improving, costs decline, and policies require growing all-electric ranges.

The current US administration rolled back or paused major federal targets, programs, incentives, and infrastructure deployment investments aimed at accelerating EV adoption.[xli] It rescinded the waiver that allowed California and other states to set EV-related requirements[xlii] and proposed to remove the foundation of what allows the Environmental Protection Agency (EPA) to regulate GHG emission standards for vehicles.[xliii] This pullback places a greater focus on protecting traditional internal combustion manufacturing than on leading new technology developments, even as interest remains for diversifying EV battery supply chains. These policy decisions are exacerbated by tariffs applied to US allies, making the competitive challenge from China and other global automakers that are not subject to the same policy reversal (despite the risk of some degree of rollback induced by US policy shifts, especially in Europe) more acute for the US.

Recognizing the scale of the global transformation that is profoundly reshaping the automotive industry—driven by economics and energy/resource security in addition to environmental considerations—is a key prerequisite to improve the competitiveness of US OEMs in this shifting landscape. Doing so is crucial to leverage existing capacity in the automotive sector and support investments in new industrial assets. To do so, US policymakers could enact policies that accomplish the following:

Pierpaolo Cazzola is a Non-Resident Fellow at the Center on Global Energy Policy at Columbia University’s School of International and Public Affairs. His research area lies at the intersection of transport, energy, innovation and climate policy. Pierpaolo is also the Director of the European Transport and Energy Research Centre of the Institute of Transportation Studies at the University of California, Davis.

Pierpaolo supports European institutions, multilateral development banks and intergovernmental organisations in the analysis of energy, mobility, climate and innovation policy.

Prior to the current assignments, Pierpaolo spent more than 20 years working internationally at the intersection of transport, energy and environmental sustainability.

During the year 2022, he was appointed by Minister Enrico Giovannini as an advisor of the Italian Ministry for Infrastructure and Sustainable Mobility, in the context of its “structure for the ecological transition of mobility and infrastructures” (STEMI). This was tasked to elaborate policy recommendations on transport decarbonisation, including in the framework of the implementation of the European Green Deal.

Pierpaolo was advisor on energy, technology and environmental sustainability for the International Transport Forum (2019-2022), transport lead in the Energy Technology Policy Division of the International Energy Agency (2014-2019), coordinator of the Electric Vehicles Initiative of the Clean Energy Ministerial (2016-2019), Secretary of the Working Party on Pollution and Energy of the World Forum for the Harmonization of Vehicle Regulations (WP.29) of the United Nations (2011-2014), fellow at the Institute of Prospective Technological Studies of the Joint Research Centre of the European Commission (2010-2011), analyst on material flows at the Environment Directorate of the Organisation for Economic Cooperation and Development (2010) and transport and energy analyst at the International Energy Agency (2004-2010), where he began his career working on energy balances and CO2 emission statistics (2001-2004).

Pierpaolo holds a Master in energy economics from the Institut Français du Pétrole et Énergies Nouvelles (IFP School, France, 2001), a Master in Aerospace Engineering from the Politecnico di Torino (Italy, 2000) and a Bachelor of Engineering in Aeronautics from the University of Glasgow (United Kingdom, 1999).

[i] International Energy Agency. “Global EV Outlook 2025.” 2025. https://www.iea.org/reports/global-ev-outlook-2025.

[ii] Ibid.

[iii] Ibid.; S&P Global. “S&P Global Mobility Forecasts 89.6M Auto Sales Worldwide in 2025.” 2025. News Release Archive. https://press.spglobal.com/2024-12-20-S-P-Global-Mobility-forecasts-89-6M-auto-sales-worldwide-in-2025; EV Volumes. “EV-Volumes—the Electric Vehicle World Sales Database.” 2025. https://ev-volumes.com; BloombergNEF. “Electric Vehicle Outlook—BloombergNEF.” 2025. https://about.bnef.com/insights/clean-transport/electric-vehicle-outlook.

[iv] International Energy Agency. “Global EV Outlook 2025.” 2025. https://www.iea.org/reports/global-ev-outlook-2025; EV Volumes. “EV-Volumes—the Electric Vehicle World Sales Database.” 2025. https://ev-volumes.com; BloombergNEF. “Electric Vehicle Outlook.” 2025. https://about.bnef.com/insights/clean-transport/electric-vehicle-outlook; Cazzola, P., Paoli, L., and Teter, J. “Trends in the Global Vehicle Fleet 2023.” 2023. Global Fuel Economy Initiative. https://www.globalfueleconomy.org/resources/trends-in-the-global-vehicle-fleet-2023; European Environment Agency. “CO2 Emissions from New Passenger Cars.” n.d. https://co2cars.apps.eea.europa.eu; ACEA—European Automobile Manufacturers Association. “New EU Car Registrations.” 2024. https://www.acea.auto/figure/new-passenger-car-registrations-in-eu; ACEA—European Automobile Manufacturers’ Association. “Global New Car Registrations.” 2024. https://www.acea.auto/figure/new-passenger-car-registrations-in-units; European Alternative Fuels Observatory. “EU27 + UK, Norway, Iceland, Switzerland, Turkey, Liechtenstein—Vehicles and Fleet.” n.d. https://alternative-fuels-observatory.ec.europa.eu/transport-mode/road/eu27-uk-norway-iceland-switzerland-turkey-liechtenstein/vehicles-and-fleet; International Energy Agency. “Global EV Outlook 2024.” 2024. https://www.iea.org/reports/global-ev-outlook-2024; Cozzi, L. and Petropoulos, A. “SUVs Are Setting New Sales Records Each Year—and So Are Their Emissions.” International Energy Agency. 2024. https://www.iea.org/commentaries/suvs-are-setting-new-sales-records-each-year-and-so-are-their-emissions; Kuhanathan, A., Gröschl, J., Latorre, M., Lemerle, M. et al. “Review of Global Auto Outlook: Steering Through Turbulence.” Allianz Research. 2024. https://www.allianz.com/content/dam/onemarketing/azcom/Allianz_com/economic-research/publications/specials/en/2024/march/2024-03-21-Automotive-AZ.pdf; Dejean, G. and Kuhanathan, A. “How Europe Can Take Back the Wheel in the Global Auto Sector.” Allianz Trade Corporate. 2024. https://www.allianz-trade.com/en_global/news-insights/economic-insights/europe-global-auto-sector.html; New AutoMotive. “Global Electric Vehicle Tracker.” n.d. https://newautomotive.org/global-ev-tracker; S&P Global. “S&P Global Mobility Forecasts 89.6M Auto Sales Worldwide in 2025.” 2025. News Release Archive. https://press.spglobal.com/2024-12-20-S-P-Global-Mobility-forecasts-89-6M-auto-sales-worldwide-in-2025; Luman, Rico. “Global Car Market: Sales Resilient Despite Tariffs.” ING Think. 2025. https://think.ing.com/articles/global-car-market-sales-resilient-despite-tariffs; Wimmer, H. and Neuhausen, J. “Electric Vehicle Sales Review Q3-2025.” PwC and Strategy&. 2025. https://www.strategyand.pwc.com/de/en/electric-vehicle-sales-review-q3-2025.html; Tomoshige, Y. “Japan’s Automotive Electrification Trends (2025 H1).” JATO Dynamics. 2025. https://www.jato.com/resources/news-and-insights/japans-automotive-electrification-trends-2025-h1; Japanese Automotive Manufacturers Association. “The Motor Industry of Japan.” 2025. https://www.jama.or.jp/english/reports/docs/MIoJ2025_e.pdf.

[v] Autovista24. “What Are the Global EV Market’s Most Successful Brands?” 2025. https://autovista24.autovistagroup.com/news/what-are-the-global-ev-markets-most-successful-brands.

[vi] International Energy Agency. “Global Critical Minerals Outlook 2025.” 2025. https://www.iea.org/reports/global-critical-minerals-outlook-2025.

[vii] Ibid.

[viii] European Alternative Fuels Observatory. “EU27 + UK, Norway, Iceland, Switzerland, Turkey, Liechtenstein—Vehicles and Fleet.” n.d. https://alternative-fuels-observatory.ec.europa.eu/transport-mode/road/eu27-uk-norway-iceland-switzerland-turkey-liechtenstein/vehicles-and-fleet.

[ix] European Alternative Fuels Observatory. “Electric Vehicle Recharging Prices.” n.d. https://alternative-fuels-observatory.ec.europa.eu/consumer-portal/electric-vehicle-recharging-prices.

[x] Argonne National Laboratory. “EV Model Availability and Sales.” 2024. https://www.anl.gov/ev-facts/model-sales.

[xi] Argonne National Laboratory. “Light Duty Electric Drive Vehicles Monthly Sales Updates.” n.d. https://www.anl.gov/esia/light-duty-electric-drive-vehicles-monthly-sales-updates.

[xii] Wimmer, H. and Neuhausen, J. “Electric Vehicle Sales Review Q3-2025.” PwC and Strategy&. 2025. https://www.strategyand.pwc.com/de/en/electric-vehicle-sales-review-q3-2025.html.

[xiii] Tomoshige, Y. “Japan’s Automotive Electrification Trends (2025 H1).” JATO Dynamics. 2025. https://www.jato.com/resources/news-and-insights/japans-automotive-electrification-trends-2025-h1.

[xiv] Fadhil, I., and Chang S. “Global Electric Vehicle Market Monitor for Light-Duty Vehicles in Key Markets, 2025 H1.” International Council on Clean Transportation. n.d. https://theicct.org/wp-content/uploads/2025/09/ID-448-%E2%80%93-EV-Market-Monitor-H1-2025_research-brief_final.pdf.

[xv] Cazzola. P., Teter, J. and Craglia, M. “Small and Electric—the International Case to Move Away from Combustion SUVs.” Working Paper 25. Global Fuel Economy Initiative. 2025. https://www.globalfueleconomy.org/resources/gfei-working-paper-25-small-and-electric-the-international-case-to-move-away-from-combustion-suvs.

[xvi] Nguyen, D. “VinFast Partners Chinese Company for Making Electric Car Batteries.” VnExpress International. 2021. https://e.vnexpress.net/news/business/companies/vinfast-partners-chinese-company-for-making-electric-car-batteries-4344912.html; Best Magazine. “Vinfast Acquires Sister Battery Company Vines Energy Solutions.” 2023. https://www.bestmag.co.uk/vinfast-acquires-sister-battery-company-vines-energy-solutions/.

[xvii] Johnston, R. “Industrial Policy Nationalism: How Worried Should We Be?” Center on Global Energy Policy, Columbia University. 2023. https://www.energypolicy.columbia.edu/industrial-policy-nationalism-how-worried-should-we-be.

[xviii] van Wieringen, K. and Chahri, S. “The Future of European Electric Vehicles.” European Parliamentary Research Service. 2024. https://www.europarl.europa.eu/RegData/etudes/IDAN/2024/762873/EPRS_IDA(2024)762873_EN.pdf.

[xix] International Energy Agency. “Fuel Economy in Major Car Markets: Technology and Policy Drivers 2005–2017.” 2019. https://www.iea.org/reports/fuel-economy-in-major-car-markets; Cazzola, P., Paoli, L. and Teter, J. “Trends in the Global Vehicle Fleet 2023.” 2023. https://www.globalfueleconomy.org/resources/trends-in-the-global-vehicle-fleet-2023.

[xx] International Energy Agency. “Global EV Outlook 2019.” 2019. https://www.iea.org/reports/global-ev-outlook-2019; Bieker, G. “A Global Comparison of the Life-Cycle Greenhouse Gas Emissions of Combustion Engine and Electric Passenger Cars.” International Council on Clean Transportation. 2021. https://theicct.org/publication/a-global-comparison-of-the-life-cycle-greenhouse-gas-emissions-of-combustion-engine-and-electric-passenger-cars; United States Environmental Protection Agency. “Electric Vehicle Myths.” 2025. https://www.epa.gov/greenvehicles/electric-vehicle-myths.

[xxi] A report released in summer 2025 to support deregulating GHG emissions by the Environmental Protection Agency deemed CO2 as “less damaging economically than commonly believed” (see: Christy, J., Curry, J., Koonin, S., McKitrick, R. et al. “A Critical Review of Impacts of Greenhouse

Gas Emissions on the U.S. Climate.” 2025. https://www.energy.gov/sites/default/files/2025-07/DOE_Critical_Review_of_Impacts_of_GHG_Emissions_on_the_US_Climate_July_2025.pdf). Despite major critiques regarding this stance (see Nature. “Climate Impacts Are Real—Denying This Is Self-Defeating.” 2025. https://doi.org/10.1038/d41586-025-02868-1and Dessler, A. and Kopp, R. E. “Climate Experts’ Review of the DOE Climate Working Group Report.” 2025.

https://doi.org/10.22541/essoar.175745244.41950365/v2) and court cases that are not concluded, this reveals the extent of the reversal in the way climate is taken into consideration in current US policymaking.

[xxii] Renshaw, J., and Kirkham, C. “Exclusive: Trump Transition Team to Roll Back Biden EV, Emissions Policies.” Reuters. 2024. https://www.reuters.com/business/autos-transportation/trump-transition-team-plans-sweeping-rollback-biden-ev-emissions-policies-2024-12-16; Oxford Institute for Energy Studies. “2025 EVs and Battery Supply Chains Issues and Impacts.” Forum. Issue 144. 2025. https://www.oxfordenergy.org/publications/2025-evs-and-battery-supply-chains-issues-and-impacts-issue-144.

[xxiii] Plötz, P., and Jöhrens., J. “Realistic Test Cycle Utility Factors for Plug-in Hybrid Electric Vehicles in Europe.” 2021. https://www.isi.fraunhofer.de/content/dam/isi/dokumente/cce/2021/BMU_Kurzpapier_UF_final.pdf; key elements providing evidence for policy revisions emerged from Isenstadt, A., Yang, Z., Searle, S., and German, J. “Real World Usage of Plug-In Hybrid Vehicles in the United States.” International Council on Clean Transportation. 2022. https://theicct.org/wp-content/uploads/2022/12/real-world-phev-us-dec22.pdf. Despite a critique to some aspects of this work (see Hamza, K., and Laberteaux, K. “On the Need for Revisions of Utility Factor Curves for Plug-In Hybrids in the US.” 2024. https://public-laberteaux.s3.amazonaws.com/2024_SAE_WCX_Fuelly_and_BAR.pdf), the fundamental considerations regarding all-electric driving shares of PHEVs that are lower than initially expected remain.

[xxiv] European Commission. “First Commission Report on Real-World CO2 Emissions of Cars and Vans Using Data from On-Board Fuel Consumption Monitoring Devices.” 2024. https://climate.ec.europa.eu/news-your-voice/news/first-commission-report-real-world-co2-emissions-cars-and-vans-using-data-board-fuel-consumption-2024-03-18_en.

[xxv] European Union. “Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019 Setting CO2 Emission Performance Standards for New Passenger Cars and for New Light Commercial Vehicles, and Repealing Regulations (EC) No 443/2009 and (EU) No 510/2011.” 2019. https://eur-lex.europa.eu/eli/reg/2019/631/oj/eng; European Commission. “Commission Regulation (EU) 2023/443 of 8 February 2023 Amending Regulation (EU) 2017/1151 as Regards the Emission Type Approval Procedures for Light Passenger and Commercial Vehicles.” 2023. https://eur-lex.europa.eu/eli/reg/2023/443/oj/eng.

[xxvi] United States Environmental Protection Agency. “Multi-Pollutant Emissions Standards for Model Years 2027 and Later Light-Duty and Medium-Duty Vehicles.” Federal Register 89, no. 76 (2024). https://www.govinfo.gov/content/pkg/FR-2024-04-18/pdf/2024-06214.pdf.

[xxvii] Wang, Zhenpo. Parallel Hybrid Electric Vehicles. Springer, 2023. https://doi.org/10.1007/978-981-99-6411-6_8.

[xxviii] CBEA. “PHEV新车来势汹汹!插混电池竞‘速’升级-独家观察-电池中国网.” 2024. http://m.cbea.com/djgc/202405/023127.html.

[xxix] Wang, Zhenpo. Parallel Hybrid Electric Vehicles. Springer, 2023. https://doi.org/10.1007/978-981-99-6411-6_8; Oxford Institute for Energy Studies. “2025 EVs and Battery Supply Chains Issues and Impacts.” Forum. Issue 144. 2025. https://www.oxfordenergy.org/publications/2025-evs-and-battery-supply-chains-issues-and-impacts-issue-144.

[xxx] International Energy Agency. “Global EV Outlook 2025.” 2025. https://www.iea.org/reports/global-ev-outlook-2025.

[xxxi] Oxford Institute for Energy Studies. “2025 EVs and Battery Supply Chains Issues and Impacts.” Forum. Issue 144. 2025. https://www.oxfordenergy.org/publications/2025-evs-and-battery-supply-chains-issues-and-impacts-issue-144.

[xxxii] Miao, L. “China Adjusts NEV Tax Break Policy: PHEV Must Exceed 100 Km Electric Range.” CarNewsChina.com. 2025. https://carnewschina.com/2025/10/11/china-adjusts-nev-tax-break-policy-phev-must-exceed-100-km-electric-range/.

[xxxiii] European Commission. “Commission Regulation (EU) 2023/443 of 8 February 2023 Amending Regulation (EU) 2017/1151 as Regards the Emission Type Approval Procedures for Light Passenger and Commercial Vehicles.” 2023. https://eur-lex.europa.eu/eli/reg/2023/443/oj/eng.

[xxxiv] This is an issue shared by BEVs, even if recent market developments start pointing toward a greater diversification of models, including smaller and cheaper BEVs. Cheaper BEVs are partly a response to policy decisions in the EU such as price caps to access EV purchase incentives, social leasing programs specifically targeting demand creation for EVs in cheaper market segments, and the flattening of the weight-based distribution of tailpipe emission reduction requirements (see: European Commission. “Commission Implementing Decision (EU) 2023/1623 of 3 August 2023 Specifying the Values Relating to the Performance of Manufacturers and Pools of Manufacturers of New Passenger Cars and New Light Commercial Vehicles for the Calendar Year 2021 and the Values to Be Used for the Calculation of the Specific Emission Targets from 2025 Onwards, Pursuant to Regulation (EU) 2019/631 of the European Parliament and of the Council and Correcting Implementing Decision (EU) 2022/2087.” 2023. https://eur-lex.europa.eu/eli/dec_impl/2023/1623/oj/eng).

[xxxv] European Union. “Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions—Decarbonise Corporate Fleets.” 2025. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52025DC0096.

[xxxvi] Von der Leyen. “2025 State of the Union Address.” European Commission. 2025. https://ec.europa.eu/commission/presscorner/detail/ov/SPEECH_25_2053.

[xxxvii] European Council. “Proposal for a Regulation of the European Parliament and of the Council Amending Regulation (EU) 2021/1119 Establishing the Framework for Achieving Climate Neutrality—General Approach.” 2025. https://data.consilium.europa.eu/doc/document/ST-14960-2025-INIT/en/pdf.

[xxxviii] International Energy Agency. “Global EV Outlook 2025.” 2025. https://www.iea.org/reports/global-ev-outlook-2025.

[xxxix] Wimmer, H., and Neuhausen, J. “Electric Vehicle Sales Review Q3-2025.” PwC and Strategy&. 2025. https://www.strategyand.pwc.com/de/en/electric-vehicle-sales-review-q3-2025.html.

[xl] Tomoshige, Y. “Japan’s Automotive Electrification Trends (2025 H1).” JATO Dynamics. 2025. https://www.jato.com/resources/news-and-insights/japans-automotive-electrification-trends-2025-h1.

[xli] The White House. “Unleashing American Energy.” 2025. https://www.whitehouse.gov/presidential-actions/2025/01/unleashing-american-energy/.

[xlii] United States Environmental Protection Agency. “EPA Administrator Zeldin Celebrates President Trump Officially Ending California’s Vehicle Waivers, Delivering Another Major Blow to the EV Mandate.” 2025. https://www.epa.gov/newsreleases/epa-administrator-zeldin-celebrates-president-trump-officially-ending-californias.

[xliii] United States Environmental Protection Agency. “EPA Releases Proposal to Rescind Obama-Era Endangerment Finding, Regulations That Paved the Way for Electric Vehicle Mandates.” 2025. https://www.epa.gov/newsreleases/epa-releases-proposal-rescind-obama-era-endangerment-finding-regulations-paved-way.

[xliv] Brunelli, K., Yejin Lee, L., and Moerenhout, T. “Lithium in the Energy Transition: Roundtable Report.” Center on Global Energy Policy, Columbia University. 2024. https://www.energypolicy.columbia.edu/publications/lithium-in-the-energy-transition-roundtable-report.

[xlv] Moerenhout, T. “Developing Midstream Segments of the North American Minerals and Battery Supply Chain: Roundtable Summary.” Center on Global Energy Policy, Columbia University. 2024. https://www.energypolicy.columbia.edu/publications/developing-midstream-segments-of-the-north-american-minerals-and-battery-supply-chain-roundtable-summary/.

As the US and Europe navigate a difficult and uneven shift toward full battery electric vehicles (BEVs), the US and EU auto markets are under heavy pressure.

High political walls are hurting an industry vital to the character of the country.

Full report

Commentary by Pierpaolo Cazzola • November 24, 2025