Trump delayed a global carbon tax. Now he wants to finish the fight.

American officials are drafting a diplomatic cable that warns dozens of countries against adopting a climate fee on the shipping industry.

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

In January 2026, the UK government publicly released an intelligence report analyzing the security implications of global environmental destruction.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

President Trump has aggressively used tariffs as an economic tool, but a US Supreme Court decision on Friday struck down his sweeping tariffs, bringing new uncertainty. The court,...

Find out more about our upcoming and past events.

Join us for an in-person event exploring careers and opportunities in the rapidly evolving electric vehicle and sustainable transportation ecosystem.

Commentary by Trevor Sutton, Sally Qiu & Evelyne Williams • October 30, 2025

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

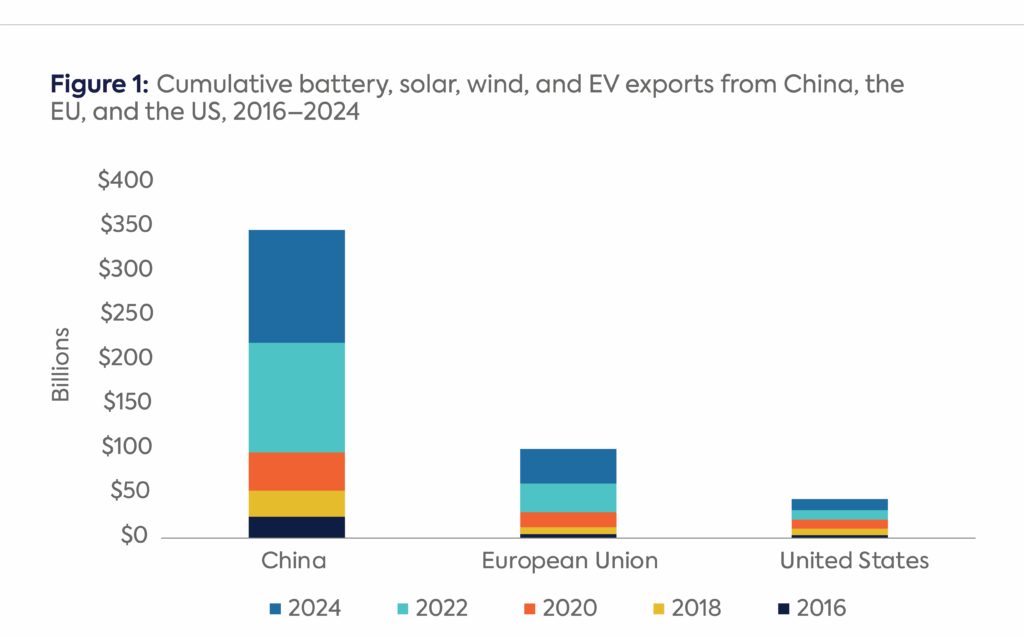

The global clean energy economy today looks starkly different than it did even 10 years ago. Not only have production and deployment of clean energy technologies expanded significantly, the geographic distribution of clean energy manufacturers, resellers, and end-users has shifted dramatically. In 2015, clean energy supply chains were somewhat diversified.[i] Today, China is by far the largest producer of most of the intermediary and finished goods that feed into global solar, wind, battery, and electric vehicle (EV) supply chains—in many cases accounting for a majority of global production.[ii] (See Figure 1).

Note: *US data for 2022 and 2024 are estimated from EIA growth numbers and Comtrade data and should be taken as purely illustrative.

Source: UN Comtrade Database, accessed October 28, 2025, https://comtradeplus.un.org; EMBER, China’s Solar PV Export Explorer, accessed October 28, 2025, https://ember-energy.org/data/chinas-solar-pv-export-explorer; EIA, 2022 Annual Solar Photovoltaic Module Shipments Report, 2023, https://www.eia.gov/renewable/annual/solar_photo; European Commission, Eurostat, “International Trade in Products Related to Green Energy,” accessed October 28, 2025,

https://ec.europa.eu/eurostat/statistics-explained/index.php?title=International_trade_in_products_related_to_green_energy

These tectonic shifts in a sector poised to become one of the principal engines of global economic growth have occurred against deteriorating US-China relations and are causing growing concern among US leaders about the US-China bilateral trade deficit. Minimizing the flow of Chinese or Chinese-affiliated clean energy products into US markets has become a bipartisan project, with major implications for both global energy supply chains and the clean energy transition for the United States and China.

But the impact of US trade hawkishness is not limited to the bilateral relationship. Third countries that serve as nodes along clean energy supply chains have been significantly affected by US-China trade tensions. In some cases, these third countries have benefited economically from a diversification of Chinese and US investment and supply chains. Yet growing US concerns about tariff circumvention and the Trump administration’s mercurial approach to tariffs have injected uncertainty into the durability of those investment and supply chain relationships, and left countries with ties to both Chinese and US markets feeling squeezed.

This commentary examines how instability in US-China trade ties is shaping investment and trade in clean energy goods around the world and assesses the implications of China’s growing energy engagement in third countries for US policymakers.

Since the Obama administration, the United States has steadily increased market barriers on a range of Chinese clean energy goods, substantially decreasing the short-term cost competitiveness of those goods and, in some cases, reducing import volumes to a trickle. In response, Chinese manufacturers have recalibrated their commercial strategies to focus on more receptive markets, increasing supply, lowering prices, and accelerating clean energy adoption.

Between 2021 and 2024, emerging markets accounted for 70% of the growth in China’s export of solar, wind, and EV products. In 2024, nearly half of these exports went to the Global South, matching exports to developed countries.[iii] This influx has helped lower clean energy prices and transform energy systems in many developing economies, especially those without significant domestic clean energy industries.[iv] For example, Pakistan, one of the largest Asian importers of Chinese solar panels, imported enough in 2024 to expand its power capacity by one-third. In Africa, too, cheap solar panels are helping countries lessen their reliance on hydropower following the worst mid-season drought in more than a century.[v]

China has reinforced its shift to non-US markets through trade agreements and policy initiatives. Participation in frameworks like the Regional Comprehensive Economic Partnership (RCEP) has reduced barriers to trade in clean energy technologies and energy-efficient appliances to Southeast Asia.[vi] Since 2021, renewable energy investment has also become a new policy focus of China’s Belt and Road Initiative (BRI).[vii] In the first half of 2025, BRI green energy engagement reached US$9.7 billion across wind, solar, and waste-to-energy projects—an increase of US$4.2 billion from 2024—adding an estimated 11.9 gigawatts (GW) of green energy.[viii]

Amid ongoing US-China trade tensions, both advanced and emerging economies are positioning themselves as reliable partners for Chinese clean-tech investment. European OECD members now constitute the largest destination for China’s exports and overseas manufacturing investments by value (not without consequences to European producers, as discussed below).[ix] Meanwhile, a number of resource-rich countries in the Global South are angling to be strategic players in the global clean energy transition by pursuing policies that not only attract upstream (raw goods) but also midstream (processing and refining) investment that build local manufacturing capacity as a means to break out of extractive economic relationships.

Indonesia, for example, has leveraged its vast nickel reserves, a key input into EV batteries, by banning raw ore exports and requiring local processing, drawing major Chinese investment into smelting and battery precursor production.[x] Officials in other mineral-rich countries are likely to seek to replicate Indonesia’s success in shifting Chinese investment strategy away from raw mineral exports to local minerals processing. For example, South Africa, which produces about 70% of global platinum-group metals and has vast manganese, vanadium, and chromium reserves, is prioritizing local value-add through its 2025 Critical Mineral Strategy, with China as a likely partner.[xi]

Alongside this surge in Chinese exports and investment, US-backed financing is expanding as Washington seeks to counterbalance Beijing’s influence and mitigate Beijing’s chokehold on critical materials. Through the International Development Finance Corporation, the US has provided a US$150 million loan for Mozambique’s Balama graphite mine[xii] and helped broker an agreement between the Democratic Republic of Congo and Zambia to develop an EV battery supply chain tapping their cobalt and nickel reserves.[xiii] More recently, the Trump administration announced a multi-billion dollar partnership with Australia to reduce US dependence on Chinese exports of rare earth materials following Beijing’s imposition of stringent export controls on them in response to US tariffs in October.[xiv]

While the Biden administration steadily increased market barriers on Chinese imports and expanded US-backed financing, it also created (now largely obsolete) incentives for the adoption of clean energy technologies alongside new supply chain relationships to meet growing American demand for these products. Such initiatives included the Inflation Reduction Act’s clean energy investment and production tax credits, and rebates on EVs.

Pairing trade barriers on China with subsidies for clean energy generation and low-carbon technologies created lucrative market opportunities for clean energy firms in some third countries, particularly in the solar sector. Exporters based in Southeast Asia currently account for more than 90 percent of imports of solar products into the United States,[xv] despite being dwarfed by Chinese solar manufacturing and exports at a global level.

With respect to lithium batteries, Korea and Japan have become the second and third largest suppliers to the United States, although China continues to dominate.[xvi] Finally, although foreign-made EVs remain a small share of total sales in the United States, prohibitive tariffs on Chinese EVs mean that non-Chinese producers will not have to compete with low-cost Chinese brands.

The benefits described above come with associated risks and liabilities that have grown more pronounced since the start of the second Trump administration.

An influx of low-cost Chinese solar panels, batteries, and EVs—widely attributed to overproduction and associated surplus capacity in China’s domestic market—threatens to undercut domestic manufacturing capabilities in many importing countries, undermining their long-term industrial development and contributing to premature deindustrialization.[xvii]

Countries that aim to build local clean-tech industries have struggled to compete with China’s scale-driven cost advantages. As of 2024, Chinese automakers accounted for one in four EVs sold in Europe, with prices roughly 20% below European models.[xviii] In Thailand, Chinese brands now hold over 70% of the EV market.[xix] Governments from Bangkok to Brussels are responding with tariffs, anti-subsidy investigations, and incentives to protect domestic industry.[xx]

Another risk is growing dependence on Chinese clean energy equipment and financing, which creates structural and strategic vulnerabilities beyond trade relations. Between 2023 and 2024, China announced US$58 billion in overseas clean energy manufacturing projects, along with US$24 billion in overseas power generation and storage deals, largely in South Asia, the Middle East, and North Africa.[xxi] The sheer scale of these investments and export volumes has increased the risk of supply chain disruptions for importing countries and raised concerns about exposure to Chinese retaliatory measures and economic coercion.

Consider the challenge now facing Indonesia. Jakarta’s efforts to promote investment into value-added activities in its nickel sector have come with a cost: Chinese companies now dominate the sector, controlling an estimated 75% of domestic nickel operations.[xxii] During the Biden administration, Indonesia sought to diversify its partnerships and was considering limits on future Chinese project ownership to comply with US trade rules. These efforts to rebalance its supply chain partnerships are now facing major headwinds with the partial repeal of the IRA.[xxiii]

Similarly, the opportunities many third countries identified in the US market are beginning to look illusory. The recent omnibus reconciliation bill repealed or significantly curtailed many of the most important tax credits under the IRA and substantially expanded the scope of the “foreign entities of concern” restrictions on subsidy eligibility.[xxiv] These changes will inevitably suppress demand for imported clean energy products and undercut the commercial logic of additional investment into US renewable power generation and EV supply chains.

Compounding these challenges, the Trump administration’s assertive use of tariffs has cast a pall around US-focused export strategies in third countries. Steep tariffs on countries angling to compete with China as global manufacturing powerhouses have led multinational firms to pause and reconsider their plans to shift production out of China.[xxv] To add to the uncertainty, multiple US courts have found that the legal basis the White House has invoked for most of these tariffs, the International Emergency Economic Powers Act (IEEPA), is invalid.[xxvi] The tariffs remain in force for the time being, with final resolution likely to come with a decision from the US Supreme Court, expected in early November.

Perhaps the biggest whipsaw has been for countries that benefited from Chinese investment into their domestic manufacturing sectors that, in turn, supplied US firms. In July 2025, the White House issued an executive order adjusting previous tariffs imposed under IEEPA, which included a declaration that “goods transshipped to evade applicable duties [i.e., tariffs]” would be subject to a 40% tariff.[xxvii] Neither “transshipment” nor “duty evasion” are terms with clear legal meaning under IEEPA or other trade and customs authorities, and could conceivably encompass a broad range of practices.[xxviii] US political trade “deals” with Cambodia, Malaysia, Thailand, and Vietnam announced in October all reference cooperation on “duty evasion” but do not clarify how such evasion should be assessed or what rules of origin would apply to goods shipped from those four countries.[xxix]

Southeast Asian countries that import Chinese components and re-export will be particularly exposed to this new transshipment policy, but the impacts will likely be felt more broadly. The Malaysian solar industry, which drew billions in Chinese investment during the first Trump administration only to crater in the wake of Biden administration tariffs, offers a worrying precedent for regional actors in this regard.[xxx]

For US policymakers seeking a high degree of decoupling from Chinese-linked clean energy supply chains—or to limit deployment of clean energy technologies in general—the current state of affairs may be desirable. Chinese and third country exporters of clean energy supply chains are likely to pull back from supplying the US market in the face of uncertainty over tariffs and subsidies, leading to slower deployment of clean energy infrastructure in the United States and higher prices for clean energy goods. But dwindling points of entry for Chinese firms into US-bound supply chains are likely to accelerate Chinese investment and trade partnerships outside North America, potentially undercutting US efforts to blunt China’s influence in the Global South.[xxxi]

If policymakers’ goal is to replace Chinese and Chinese-linked clean energy supply chains with alternatives from third countries, current US policy is counterproductive. As of this writing, many third countries face actual or prospective economywide tariffs similar to and even higher than those on Chinese goods, making it difficult for them to compete on price.[xxxii] Rather than seeking partnerships with aspiring clean energy manufacturing hubs like India and Brazil, for example, the administration has imposed a baseline tariff of 50% on both countries’ exports under IEEPA, relative to China’s 30% (current as of October 29, 2025).[xxxiii] To exacerbate matters, the administration has justified its IEEPA tariffs on non-Chinese imports with shifting rationales, making it difficult for exporters to feel confident in the stability of current tariff rates and leaving trading partners uncertain about what measures, if any, they could adopt to receive more favorable treatment.

US policymakers interested in building alternatives to Chinese-exclusive clean energy supply chains could encourage the White House to clearly define the scope of the transshipment-related tariff policy authorized in President Trump’s executive order. They could also go a step further and propose linking actual or threatened imposition of those tariffs to tightened rules of origin on implicated goods, which third country governments could leverage to demand Chinese investment lead to more value-added activity, upskilling, and technology transfer, similar to what Indonesia achieved in its nickel sector.

A second, complementary approach would be to agree to tariff-rate quotas on specific clean energy goods on a country-by-country basis, similar to what was achieved with textiles under the (now defunct) Multi-Fibre Agreement.[xxxiv] Under this scheme, third countries would have reliable low-tariff access to the United States only up to a mutually agreed upon quantity of goods, allowing the US to control the geographic distribution of clean energy imports and discouraging Chinese investors from cycling from one country to another to avoid US anti-circumvention and anti-transshipment measures.

Rather than antagonizing longstanding trade partners with high tariffs, Washington’s strategic interests may be better served by coordinating with select third countries on addressing the extreme concentration of global clean energy supply chains. The goal of such coordination would be twofold: building resilience to future disruptions and shocks by diversifying sources of key clean energy goods and ensuring future clean energy investment does not flow disproportionately to Chinese firms at the expense of other market players.

Trevor Sutton, a Senior Research Associate at CGEP, focuses on the intersection of trade, climate, and industrial policy and leads the center’s Program on Trade and the Clean Energy Transition. Trevor previously served as Research Director of the Remaking Global Trade for a Sustainable Future Project and was a co-author of a seminar report on trade system reform, the Villars Framework for a Sustainable Trade System. He has also served in various roles at the Center for American Progress, most recently as a Senior Fellow for Energy and Environment, and the United Nations. Prior to these positions, Trevor served as a judicial clerk on the U.S. Court of Appeals for the District of Columbia Circuit. Trevor has a BA from Stanford University, a JD from Yale Law School, and an MPhil from Oxford University, where he was a Marshall Scholar.

Sally Qiu is a senior research associate at the Center on Global Energy Policy (CGEP) at Columbia University. In this role, she supports the center’s Inaugural Fellow David Sandalow, in work related to US-China energy and climate policy, as well as the AI-Energy Program. She is a co-author of the Guide to Chinese Climate Policy (2022) and a chapter contributor to the annual China Energy Transformation Outlook (CETO).

Sally founded and co-directs the Fashion, Energy, and Climate Network at the Columbia Climate School, a collaborative program that assesses and addresses the complex relationship between the fashion industry, energy transition, and climate change. The network brings together industry stakeholders, policymakers, and researchers to develop systematic, solution-oriented approaches to decarbonizing the fashion industry.

Previously, at Columbia’s School of International and Public Affairs (SIPA), she supported former dean Merit Janow on research, case studies, and events related to U.S.-China trade relations, foreign direct investment, and digital innovation.

She also worked as an environmental statistics consultant at the United Nations Food and Agriculture Organization (FAO), where she contributed to FAOSTAT databases and publications on greenhouse gas emissions from global food systems. She provided research and analysis on global energy efficiency standards at the ClimateWorks Foundation and supported the clean energy transition projects in Asia-Pacific during her time at the UN Economic and Social Commission for Asia and the Pacific (UNESCAP) in Bangkok.

Sally’s passion for sustainability began during her undergraduate years, when she volunteered in Fiji and Mexico, participating in local community development projects and sea turtle conservation. Beyond her professional work, she is currently pursuing a part-time degree in fashion design at Parsons School of Design, further integrating her interest in sustainability with design and innovation.

Sally holds a Master of Science in Public Policy and Management from Carnegie Mellon University, with a focus on energy policy and data analytics, and a Bachelor of Arts in History and Environmental Geoscience from DePauw University, where she was a Rector Scholar.

Evelyne Williams is a Research Associate at Center on Global Energy Policy at Columbia University SIPA, where she focuses on the intersection of international trade, energy, and decarbonization. She most recently served as a Foreign Affairs Officer in the U.S. Department of State’s Office of Global Change, where she was the deputy lead negotiator on carbon pricing at the International Maritime Organization (IMO) and represented the United States in international climate negotiations under the UN Framework Convention on Climate Change (UNFCCC) and the Organisation for Economic Co-operation and Development (OECD).

A recipient of the State Department’s Colin Powell Leadership Program fellowship for emerging policy leaders, Evelyne also held roles at the U.S. Mission to the United Nations in New York, the Office of the Geographer and Global Issues, and the Humanitarian Information Unit, where she contributed to socio-economic and climate-related policy initiatives.

Raised in Puerto Rico and the U.S. Virgin Islands, Evelyne has a longstanding interest in island economies, economic policy, and climate resilience. As a student at Columbia, she led a property tax reform and infrastructure resilience initiative in Puerto Rico and collaborated on the development of a graduate course on international monetary policy with Professor Richard Clarida. Earlier in her career, she interned at the U.S. Department of Commerce’s International Trade Administration, supporting export strategies for U.S. firms.

Evelyne holds a Bachelor of Arts in Economics with Distinction from Barnard College, Columbia University, and has pursued a Master of International Affairs at Columbia’s School of International and Public Affairs.

[i]OECD. Special Report on Solar PV Global Supply Chains. International Energy Association, August 26, 2022. https://doi.org/10.1787/9e8b0121-en.; Global Wind Report: Annual Market Update, Global Wind Energy Council,2015. http://large.stanford.edu/courses/2016/ph240/basutkar2/docs/GWEC-Global-Wind-Report_2016.pdf ; Pillot, Christophe. “The Rechargeable Battery Market and Main Trends 2014-2025.” Aviance Energy, October 6, 2015. https://rechargebatteries.org/wp-content/uploads/2020/02/Tutorial-C.-Pillot-Oct-2015.pdf

[ii] “China Building Twice as Much Wind and Solar as Rest of World Combined.” Yale Environment 360, July 11, 2024. https://e360.yale.edu/digest/china-wind-solar-double-world

[iii] Myllyvirta, Lauri and Thieriot, Hubert. “Why China’s Clean Energy Need not Fear Us Tariffs” Dialogue Earth, January 9, 2025. https://dialogue.earth/en/energy/why-chinas-clean-energy-need-not-fear-us-tariffs/

[iv] Mazzocco, Ilaria. “Analyzing the Impact of the U.S.-China Trade War on China’s Energy Transition.” Center for Strategic and International Studies, April 22, 2025. https://www.csis.org/analysis/analyzing-impact-us-china-trade-war-chinas-energy-transition

[v] “Cheap Chinese Solar Panels Sparking a Renewable Boom in the Global South.” Yale Environment 360, February 25, 2025. https://e360.yale.edu/digest/china-solar-global-south; “World’s largest electric carmaker BYD accelerates expansion drive in Africa” Business Insider, June 7, 2025. https://africa.businessinsider.com/local/markets/worlds-largest-electric-carmaker-byd-accelerates-expansion-drive-in-africa/zm4l7fz

[vi] Motohashi, Kazuyuki “RCEP for green and sustainable development.” China Daily, July 26, 2024.https://www.chinadailyhk.com/hk/article/589073

[vii] “Lights On or Off? Chinese Solar and Wind Companies in Sub-Saharan Africa.” Wilson Center, November 22, 2024. https://www.wilsoncenter.org/blog-post/lights-or-chinese-solar-and-wind-companies-sub-saharan-africa; NRDC, Opinions on Promoting Green Development in the Joint Construction of the Belt and Road Initiative (Development and Reform Commission Opening Up [2022] No. 408).National Development and Reform Commission, Ministry of Foreign Affairs, Ministry of Ecology and Environment, and Ministry of Commerce, March 28, 2022. https://www.ndrc.gov.cn/xxgk/zcfb/tz/202203/t20220328_1320629_ext.html

[viii] Nedopil Wang, Christoph. “China Belt and Road Initiative (BRI) investment report 2025 H1.” Green Finance and Development Center, July 17, 2025. https://greenfdc.org/china-belt-and-road-initiative-bri-investment-report-2025-h1/

[ix] Patel, Anika. “China Briefing 24 July 2025: EU-China Climate Statement; World’s Largest Megadam; Clean-Tech Exports.” Carbon Brief, July 24, 2025. https://www.carbonbrief.org/china-briefing-24-july-2025-eu-china-climate-statement-worlds-largest-megadam-clean-tech-exports/.

[x] Woldorff, Daniel. “Indonesia’s nickel industry is the ‘poster child of tradeoffs’ for the battery economy.” Latitude Media, March 13, 2024. https://www.latitudemedia.com/news/indonesias-nickel-industry-is-the-poster-child-of-tradeoffs-for-the-battery-economy/ ; Marcilly, Julien and Simmons, Bradford. “Lessons for African mineral producers from the Indonesian experience.” Atlantic Council, September 23, 2024. https://www.atlanticcouncil.org/in-depth-research-reports/lessons-for-african-mineral-producers-from-the-indonesian-experience/

[xi] Games, Dianna. “South Africa’s bold green energy ambitions.” African Business, January 8th, 2025. https://african.business/2025/01/quick-reads/south-africas-bold-green-energy-ambitions; “South Africa’s Critical Minerals Strategy: A New Mining Frontier.” Bishop Fraser Attorneys, June 24, 2025. https://bishopfraser.co.za/south-africa-critical-minerals-strategy-2025/; Republic of South Africa, Critical Minerals and Metals Strategy South Africa. Mineral & Petroleum Resources Department, May 30, 2025. https://www.gov.za/sites/default/files/gcis_document/202505/critical-minerals-and-metals-strategy-south-africa-2025.pdf

[xii]Webb, Mariaan. “$150m DFC loan for Africa graphite mine.” Mining Weekly, November 1, 2024. https://www.miningweekly.com/article/150m-dfc-loan-for-africa-graphite-mine-2024-11-01

[xiii] Soulé, Folashadé. “What a U.S.-DRC-Zambia Electric Vehicle Batteries Deal Reveals About the New U.S. Approach Toward Africa.” Carnegie Endowment for International Peace, August 21, 2023. https://carnegieendowment.org/research/2023/08/what-a-us-drc-zambia-electric-vehicle-batteries-deal-reveals-about-the-new-us-approach-toward-africa?lang=en

[xiv] Sherman, Natalie, “U.S, and China sign rare earths deal to counter Chinese dominance.” BBC, October 20, 2025. https://www.bbc.com/news/articles/cly9kvrdk2xo

[xv] Hauber, Grant. “U.S. trade uncertainty presents domestic opportunities for Southeast Asian renewables suppliers.” Institute for Energy Economics and Financial Analysis, April 24, 2025. https://ieefa.org/resources/us-trade-uncertainty-presents-domestic-opportunities-southeast-asian-renewables-suppliers

[xvi] “China Dominates the Lithium-ion Battery Supply Chain, but Europe is on the Rise.” Bloomberg NEF, September 16, 2020 https://about.bnef.com/insights/clean-energy/china-dominates-the-lithium-ion-battery-supply-chain-but-europe-is-on-the-rise/

[xvii] Crooks, Ed. “China’s solar growth sends module prices plummeting.”Wood Mackenzie, April 5, 2024. https://www.woodmac.com/blogs/energy-pulse/chinas-solar-growth-sends-module-prices-plummeting/ ; Dutta, Aparajita. “3 Solar Stocks to Watch Amid Poor Residential Installation Trend.” Nasdaq, April 1, 2025. https://www.nasdaq.com/articles/3-solar-stocks-watch-amid-poor-residential-installation-trend

[xviii] Tagliapietra, Simone; Trasi, Cecilia; Sebastian, Gregor. “A smart European strategy for electric vehicle investment from China.” Brugel, July 16, 2025. https://www.bruegel.org/policy-brief/smart-european-strategy-electric-vehicle-investment-china

[xix] Setboonsarng, Chayut and Staporncharnchai, Thanadech. “Analysis-China’s intense EV rivalry tests Thailand’s local production goals” Global Banking and Finance Review, July 4, 2025. https://www.globalbankingandfinance.com/UK-THAILAND-AUTOS-EV-NETA-656825e1-2b81-4bed-a446-9beba3a440da

[xx] “Tax Shifts Props up the Auto Industry” Bangkok Post, August 2, 2025. ”https://www.bangkokpost.com/business/motoring/3079933/tax-shift-props-up-the-auto-industry ; “EU, China will look into setting minimum prices on electric vehicles, EU says.” Reuters, April 10, 2025. https://www.reuters.com/business/autos-transportation/eu-china-start-talks-lifting-eu-tariffs-chinese-electric-vehicles-handelsblatt-2025-04-10/

[xxi] Myllyvirta, Lauri. “China’s clean-energy exports in 2024 alone will cut overseas CO2 by 1%.” Carbon Brief, July 22, 2025. https://www.carbonbrief.org/analysis-chinas-clean-energy-exports-in-2024-alone-will-cut-overseas-co2-by-1/.

[xxii] “Chinese firms control around 75% of Indonesian nickel capacity, report finds.” Reuters, February 5, 2025. https://www.reuters.com/markets/commodities/chinese-firms-control-around-75-indonesian-nickel-capacity-report-finds-2025-02-05/.

[xxiii] “Indonesia Looks to Lower Dependence on China for Nickel Production.” Asia Pacific Foundation of Canada, August 2, 2024. https://www.asiapacific.ca/asia-watch/indonesia-looks-lower-dependence-china-nickel-production.

[xxiv] One Big Beautiful Bill Act, H.R. 1, 119th Cong.(codified at Pub. L. 119‑21, 139 Stat. 72), July 4, 2025. https://www.congress.gov/bill/119th-congress/house-bill/1.

[xxv] Emont, Jon. “Trump’s Tariffs Stymie India’s Bid to Steal Manufacturing From China.” Wall Street Journal, August 13, 2025. https://www.wsj.com/economy/trade/trumps-tariffs-stymie-indias-bid-to-steal-manufacturing-from-china-d526f0fe.

[xxvi] V.O.S. Selections, Inc. v. Trump. United States Court of Appeals for the Federal Circuit. Nos. 2025-1812, 2025-1813. Order filed May 29, 2025. ; Knauth, Dietrich, Raymond, Nate and Hals, Tom. “Most Trump tariffs are not legal, US appeals court rules” Reuters, August 30, 2025. https://www.reuters.com/legal/government/most-trump-tariffs-are-not-legal-us-appeals-court-rules-2025-08-30/.

[xxvii] Presidential Actions. Further Modifying The Reciprocal Tariff Rates. The White House, July 31, 2025. https://www.whitehouse.gov/presidential-actions/2025/07/further-modifying-the-reciprocal-tariff-rates/.

[xxviii] Transshipment, which generally refers to the routing of goods through intermediate destinations, is extremely common in global supply chains and has numerous legitimate commercial applications. Tariff evasion, meanwhile, could plausibly refer not only to clearly illegal acts like smuggling and fraudulent customs declarations but also more ambiguous scenarios such as disputes over whether a good originates from a particular country under applicable rules of origin.

[xxix] Fact Sheet: The United States and Thailand Reach a Framework for an Agreement on Reciprocal Trade, Office of the U.S. Trade Representative, October 2025. https://ustr.gov/about/policy-offices/press-office/fact-sheets/2025/october/fact-sheet-united-states-and-thailand-reach-framework-agreement-reciprocal-trade; Fact Sheet: The United States and Vietnam Reach a Framework for an Agreement on Reciprocal, Fair, and Balanced Trade. Office of the U.S. Trade Representative, October 2025. https://ustr.gov/about/policy-offices/press-office/fact-sheets/2025/october/fact-sheet-united-states-and-viet-nam-reach-framework-agreement-reciprocal-fair-and-balanced-trade; Fact Sheet: The United States and Malaysia Reach an Agreement on Reciprocal Trade, Office of the U.S. Trade Representative, October 2025. https://ustr.gov/about/policy-offices/press-office/fact-sheets/2025/october/fact-sheet-united-states-and-malaysia-reach-agreement-reciprocal-trade; Fact Sheet: The United States and Cambodia Reach an Agreement on Reciprocal Trade. U.S, Trade Representative’s Office, October 2025. https://ustr.gov/about/policy-offices/press-office/fact-sheets/2025/october/fact-sheet-united-states-and-cambodia-reach-agreement-reciprocal-trade.

[xxx] Stevenson, Alexandra and Saieed, Zunaira. “What’s It Like to Deal With Brutal U.S. Tariffs? Ask Malaysia.” The New York Times, August 4, 2025. https://www.nytimes.com/2025/08/04/business/malaysia-solar-china.html.

[xxxi] Golden, Katerine. “Inside the United States’ plan to compete with China in the Global South.” Atlantic Council, February 23, 2024. https://www.atlanticcouncil.org/blogs/new-atlanticist/inside-the-united-states-plan-to-compete-with-china-in-the-global-south/.

[xxxii] Travelli, Alex. “Trump’s Tariffs Will Crush India’s Exporters, Threatening Livelihoods.” The New York Times, August 18, 2025. https://www.nytimes.com/2025/08/18/business/trump-tariffs-india-economy.html.

[xxxiii] Executive Order No. 14323, Addressing Threats to the United States by the Government of Brazil, The White House, July 30, 2025. https://www.whitehouse.gov/presidential-actions/2025/07/addressing-threats-to-the-us/ ; Fact Sheet, President Donald J. Trump Addresses Threats to the United States by the Government of the Russian Federation. The White House, August 6, 2025. https://www.whitehouse.gov/fact-sheets/2025/08/fact-sheet-president-donald-j-trump-addresses-threats-to-the-united-states-by-the-government-of-the-russian-federation/. The 30% tariff reflects a 20% tariff imposed under Executive Order 14228 (March 3, 2025) and a 10% tariff imposed under Executive Order 14298 (May 12, 2025) and extended under Executive Order 14334 (August 11, 2025). Some Chinese clean energy exports are subject to additional tariffs levied under other legal authorities than the IEEPA, such as Section 232 of the Trade Expansion Act of 1962 and Section 301 of the Trade Act of 1974.

[xxxiv] MacDonald, Stephen. “The World Bids Farewell to the Multifiber Arrangement.” Economic Research Service,U.S. Department of Agriculture, February 1, 2006. https://www.ers.usda.gov/amber-waves/2006/february/the-world-bids-farewell-to-the-multifiber-arrangement.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Two trade agreements recently negotiated by the Trump administration contain novel and coercive provisions with little precedent in US trade policy or the global trade system.

In the last six weeks, the Chinese government has made several bold moves related to its trade relations.

Full report

Commentary by Trevor Sutton, Sally Qiu & Evelyne Williams • October 30, 2025