This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The conflict in Iran is a reminder of how quickly global energy markets can be disrupted. It also underscores why advances in things like battery technology — from...

This roundtable is open only to currently enrolled Columbia University students. To register, you must sign in with your UNI. Join the Center on Global Energy Policy’s Women...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave, New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision.

Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available here. Rare cases of sponsored projects are clearly indicated.

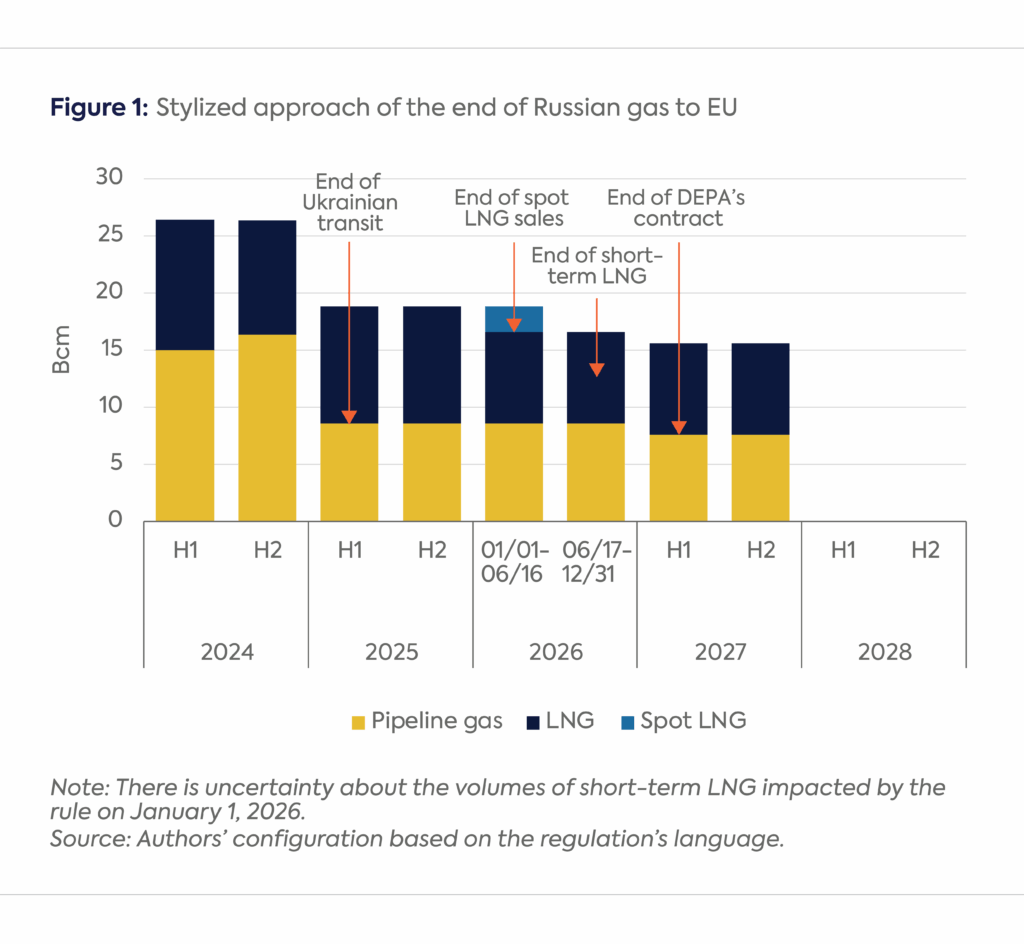

The European Commission (EC) published a proposed regulation on June 17 to end Russian gas imports by the end of 2027; this followed the initial roadmap to do so, presented on May 6. Since the Russian invasion of Ukraine in 2022, the EU has sought to end imports of Russian fossil fuels to not add to Russian coffers by purchasing such exports. In 2024, however, EU countries imported approximately 31 billion cubic meters (bcm) of Russian pipeline gas and 21.5 bcm of LNG. Since Russian gas transit through Ukraine (15 bcm) ended in January 2025, the TurkStream pipeline remains the EU’s only pipeline link, while Russian LNG flows have remained steady compared to last year. Based on current trends, Russian gas exports to the EU are expected to drop to between 35 and 39 bcm in 2025.

This blog analyses the EC’s approach for its proposed regulation and highlights the key pitfalls that still need to be avoided in the medium term. The timing reflects a combination of improving supply fundamentals, legal maneuvering to bypass unanimity, and a desire to lock in policy direction ahead of potential geopolitical shifts—especially in Washington.

Navigating EU and Global LNG Market Restrictions

The EC faced four main hurdles in determining a path forward to cease Russian gas imports. First, Hungary and Slovakia—two landlocked countries still importing Russian gas—were likely to oppose sanctions, which require unanimity. The proposed regulation is therefore based on the Treaty on the Functioning of the EU, specifically Article 207 (trade policy) and Article 194(2) (energy policy). This legal basis means that only a qualified majority will be required in the Council of the European Union during the adoption process with the European Parliament. Framing it as a trade and energy market measure rather than a sanctions regime reduces legal retaliation risk from third countries and avoids sanction fatigue within the EU. Using Article 207 and 194(2) creates legal clarity and simplifies enforcement, unlike traditional sanctions packages that suffer from fragmentation due to exemptions and national discretion.

Gas markets remain relatively tight, with European gas prices still double their 2015–19 average. But the expected arrival of ample LNG supplies to global markets by 2026–27 should enable Europe to access alternative sources. The staged approach in the regulation adds flexibility: Russian gas imports under new contracts (signed after June 17, 2025) and Russian users’ access to EU LNG terminal services (except those under long-term contracts signed before June 17, 2025) will be banned from January 2026, and those under existing short-term contracts by June 17, 2026 (except for deliveries to landlocked countries). All Russian gas imports will cease by the end of 2027.

The third hurdle is concern about exposing European companies with long-term contracts to lawsuits. Companies must disclose detailed contractual information to the EC and national authorities—likely to help anticipate legal risks—while some countries urged the EC to consider compensation mechanisms. But such support would be costly (1 bcm of Russian LNG at €25/megawatt hour would amount to nearly €300 million/year).

Finally, ongoing speculation about potential US participation in Ukraine’s gas system or NordStream 2 infrastructure raises concerns that the EU could end up dependent on Russian gas routed through US intermediaries.

What It Means for Markets and Companies

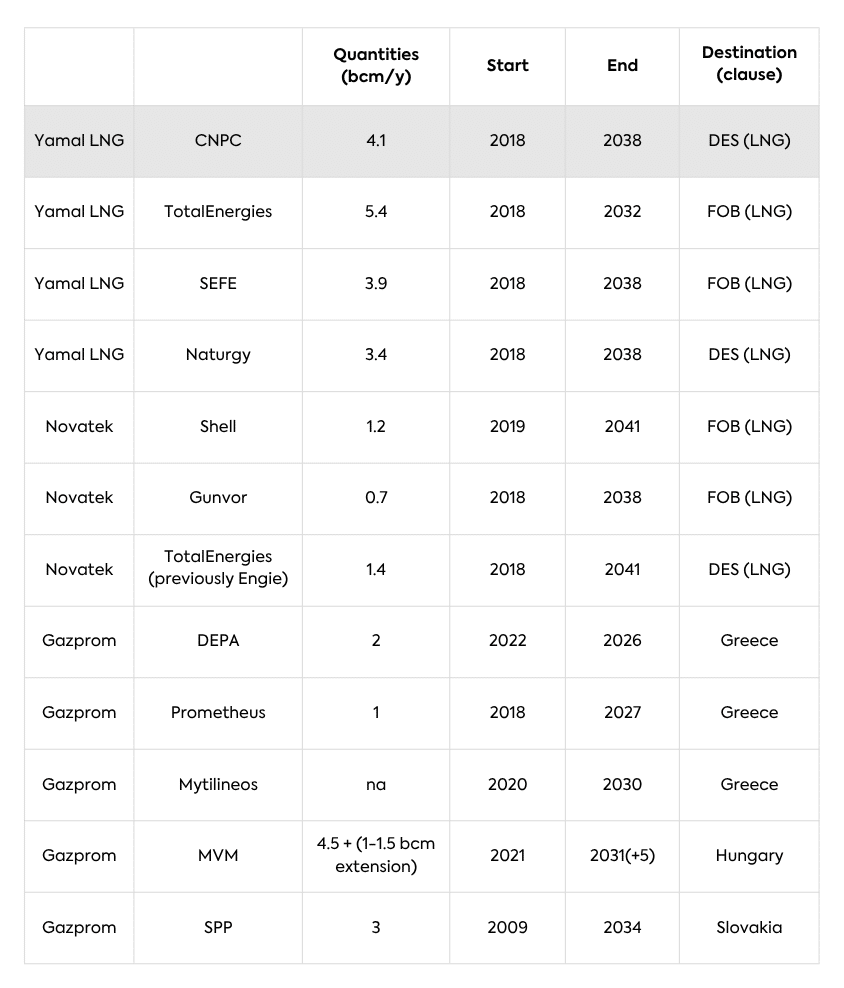

A number of European companies still hold long-term contracts with Russian companies (see Table 1). Except for two contracts with Greece’s DEPA and Prometheus, all extend beyond 2027 and will fall under the ban.

In its initial roadmap, the EC assumed that anything not on long-term contracts—around two-thirds of total volumes to Europe—was supplied on a short-term (spot) basis. The phaseout of existing spot contracts has been postponed to mid-June 2026 (instead of the end of 2025), except for those serving landlocked countries and linked to long-term contracts. This change is therefore likely to affect mostly spot LNG from January 2026, but leaves uncertainty about what is spot and short-term LNG for the period till June 17, 2026 (see Figure 1). Meanwhile the remaining 16 bcm/y of contracted Russian LNG would have to stop by the end of 2027. This delay may reflect both the revised mid-2026 start date for North Field’s expansion and concerns about curbing imports during winter. Given the ongoing Israel-Iran conflict, this caution may be warranted.

Most of Gazprom’s contracts with European companies have expired, been terminated (such as OMV), or been suspended. Absent a peace process, it remains unclear how companies will recover compensation awarded through arbitrations if no Russian gas is flowing to Europe. For example, Uniper ended its long-term contract after winning an arbitration ruling and is now seeking to recover the €13 billion awarded in compensation. Some companies may attempt to argue force majeure based on government action, but the legal landscape remains unsettled. The cost of litigation and risk of unenforceable rulings will weigh heavily on firms with Russian LNG exposure.

It is also uncertain whether companies holding LNG contracts will be shielded from legal and market exposure. Arbitrators could argue that LNG supplies are fungible (especially free on board [FOB] contracts) and can be diverted to other markets. However, the ban on transshipment may complicate logistics unless all operations can be shifted to alternative locations. Otherwise, Chinese CNPC could argue that European sanctions prevent them from either transshipping or selling cargoes in Europe.

Table 1: Current (not terminated) long-term contracts with Russia

Notes: CNPC contract is for deliveries to China.DES: delivered ex ship, FOB: free on board.

If supplies through TurkStream end, two key issues will arise. First, Gazprom currently supplies gas to Serbia (2.2 bcm), North Macedonia, and Bosnia and Herzegovina. These contracts seem to be extended on a short-term basis, as countries seek alternative supplies. However, the countries may still wish to maintain these supplies or preserve the same pricing terms. Additionally, running TurkStream at a lower load factor would raise per-unit transportation costs.

Second, under-utilized infrastructure will remain. Turkey, which also imports Russian gas, could import through TurkStream’s second string to support its ambition of becoming a regional hub—particularly as its long-term contract with Iran ends in 2026. This raises the risk of a swap between TurkStream gas and domestic Sakarya field production, potentially creating a leakage problem for Europe. Turkey has proven adept at exploiting grey zones in energy geopolitics. Its role as a commercial “relabeling” hub could allow Russian molecules to re-enter the EU under Turkish or even Azerbaijani branding, especially via hub-based mechanisms. The EC regulation marks a shift in EU gas market governance: intertwining energy security with compliance obligations. Mandatory disclosure represents a notable departure from decades of commercial confidentiality. Meanwhile the EC still lacks full transparency on all Russian-linked contracts, especially those routed through intermediaries or disguised spot-linked cargoes.

The ban will not dismantle existing infrastructure, such as Austria’s Baumgarten hub, which remains physically capable of receiving Russian gas via Slovakia. This raises enforcement questions: without strict origin tracking, indirect flows or swaps may reintroduce Russian gas under different labels. Without a robust verification and certification system, enforcement may rely heavily on national authorities—leaving room for political divergence, especially from Hungary, Slovakia, and Austria.

Conclusion

The proposed regulation to end Russian gas supplies comes at a time when peace talks over Ukraine remain stalled. This regulation marks a definitive end to the “Wandel durch Handel” era, which tied Germany to Russia through the sale of Russian gas. The regulation also sends a preemptive signal: regardless of who occupies the White House, the EU is formally closing the chapter on its dependency on Russian gas—legally, commercially, and symbolically. More broadly, this regulation reinforces the EU’s longer-term trajectory toward strategic autonomy, not just in defense and technology but in the energy domain as well.

When the Iran War disrupted shipping through the Strait of Hormuz and tightened global gas balances, a familiar assumption quickly resurfaced: Russia, possessing the largest proven natural gas reserves in the world, would inevitably emerge as one of the principal beneficiaries.