Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Campus open to active affiliate Columbia University ID (CUID) holders and approved guests only.

Columbia students, faculty, and staff can use the guest registration portal to register up to two same-day guests. Alumni can use the portal to register for campus same-day access as well. Learn more below.

This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

World leaders are meeting in New York this month at the request of the United Nations Secretary-General António Guterres to discuss the state of global ambition on climate change.

Following the rollback of key climate provisions from the Inflation Reduction Act, the debate over America's energy future is increasingly contentious. The passage of the One Big Beautiful...

The Center on Global Energy Policy at Columbia University SIPA's Women in Energy initiative, in collaboration with the Columbia Policy Institute, invites you to join us for Exploring...

Event

• International Affairs Building,

Columbia SIPA

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

Acknowledgement: The authors are grateful to the anonymous reviewers for their valuable comments and the Center on Global Energy Policy publications team for their invaluable editorial work. The authors would also like to thank Arliza Nathania for her feedback.

Qatar is entering the world’s next LNG expansion phase with a large share of uncontracted supply, and how it will navigate this phase is the central uncertainty in the LNG market.

To date, Qatar has stuck to a rigid stance of favoring long-term contracts with destination clauses.

Going forward, Qatar could expand supply aggressively and thereby depress prices or manage volumes to sustain higher prices. Either approach would significantly influence long-term demand trajectories and competitors’ expansion plans.

As of mid-2025, approximately 360 billion cubic meters per year (bcm/y) of liquefied natural gas (LNG) export capacity is expected to come online globally between 2025 and the early 2030s. After the US, the second-largest expansion (88 bcm/y) will come from Qatar, currently the world’s third-largest LNG exporter behind the US and Australia.[1]

This commentary analyzes the current state of Qatar’s LNG contracts, the country’s role in the upcoming global LNG expansion, and its past use of the spot and short-term market. It then explores three possible market and policy options that the Qataris could decide to pursue:

Engage in active market management

Incentivize demand

Adopt an aggressive market share strategy

Qatar’s decision is a wildcard for the future of LNG and gas in general. Each of these scenarios would have considerable implications for global gas price levels during the upcoming oversupply period, revenues for Qatar LNG, the outlook for competitive LNG supply, and the long-term path of LNG demand growth. Depending on whether Qatar withholds volumes from the market, tries to incentivize demand, or floods the market, it could either maintain higher prices or strongly deepen the oversupply by pushing prices to lower levels, potentially derailing competitors’ plans.

Qatar’s Current Contractual LNG Commitments

Qatar differs from most other LNG-exporting countries in two ways. First, the country is entering a new phase of LNG expansion with significant uncontracted volumes,[2] though Qatari authorities intend to market most of this LNG under long-term contracts rather than resorting to the spot market, a goal that has proven somewhat elusive thus far. Second, its entire LNG export and marketing strategy is centralized under a single state-owned entity, QatarEnergy, which gives the country unparalleled control and coordination over its gas exports.[3]

Qatar also plays a distinct role in the global LNG market. With its massive reserves — 23.8 trillion cubic meters (tcm) as of 2024[4] — situated in a single location, it has served as the singular low-cost LNG supplier, built on the back on long-term, oil-indexed contracts. The country has used this strategic position to define and preserve its own LNG strategy over the past 28 years, when it first started exporting LNG to Japan, even as the world has moved to more flexible, shorter and spot-indexed contracts. This strategy preserves some of the bedrock characteristics of the LNG business that had existed up to that point: sign oil-indexed long-term contracts with fixed destination clauses and create a working model that is as integrated as possible.

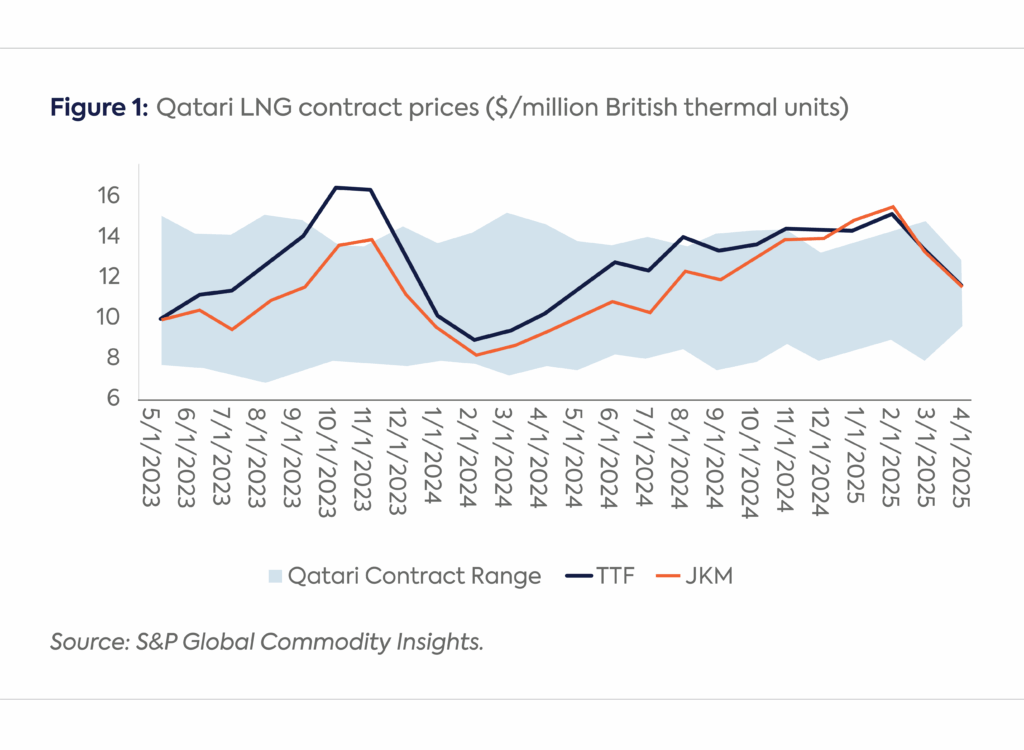

Qatar’s fealty to oil-indexed contracts always derived from the Qatari government’s underlying belief that it was setting the central tendency price for global LNG.[5] Various regional spot prices such as Europe’s Title Transfer Facility (TTF) and Asia’s Japanese Korea Marker (JKM) were considered more secondary prices oscillating around the Qatari level. Qatar itself bilaterally negotiates a wide range of oil-indexed prices (see Figure 1).

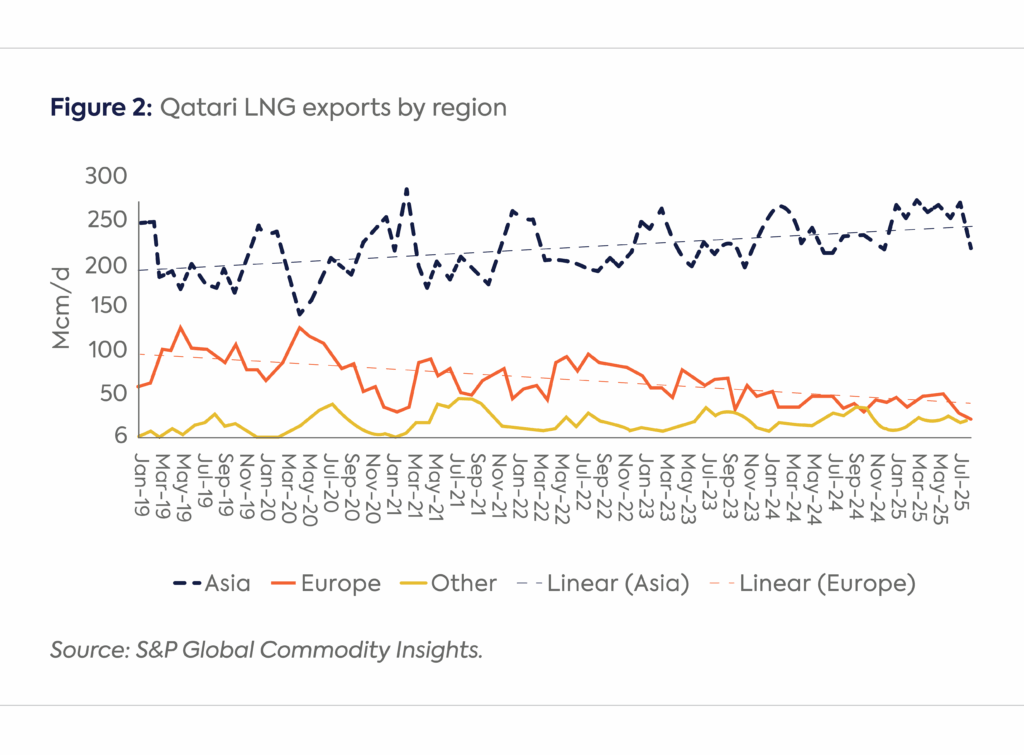

Qatar now sells most of its LNG in Asia — a trend that is likely to continue (Figure 2). Asian buyers have a history of signing long-term deals and more readily accepting oil-indexed prices compared with other buyers, though European buyers may have warmed up to the idea after Russia’s invasion of Ukraine forced them to assess options other than spot-indexed gas supplies.

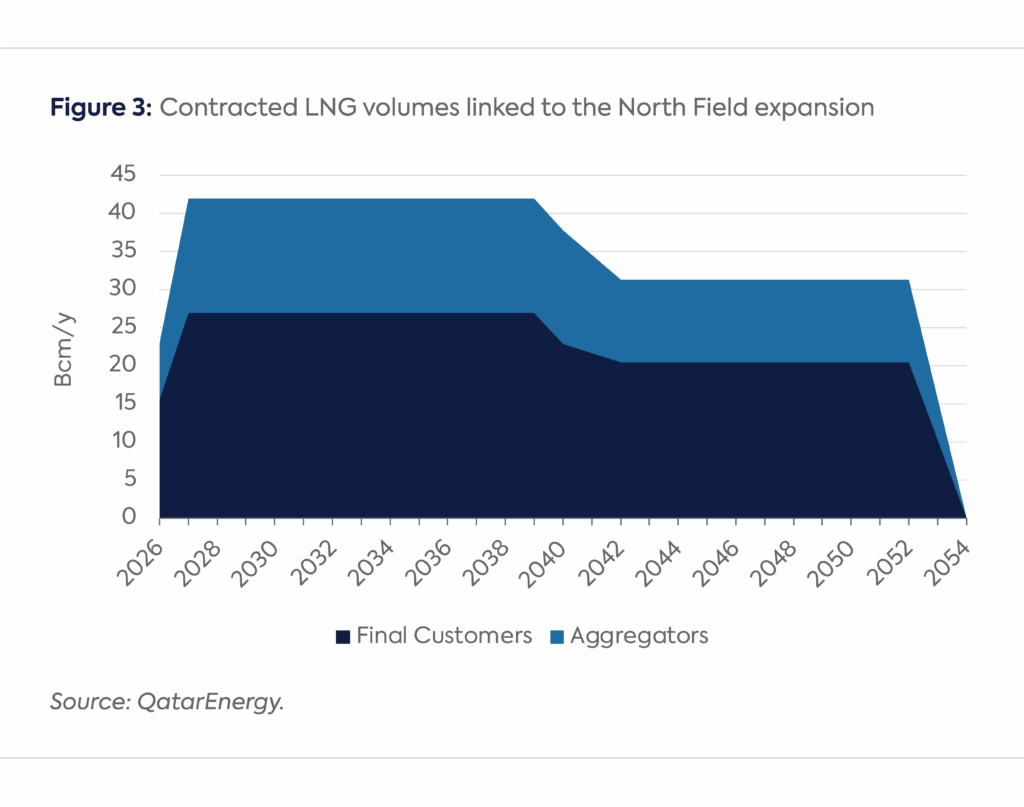

QatarEnergy currently manages 105 bcm/y of LNG under long-term contracts ranging in length from 10 to 25 years. Most existing contracts do not expire until the 2030s, but some existing buyers, such as Pakistan, may be exploring the idea of reducing existing volumes.[6] New contracts covering new capacity begin in 2026. QatarEnergy will be bringing 105 bcm/y of capacity to the market from Qatar (88 bcm/y) and the US (Golden Pass, 17 bcm/y, all uncontracted). In Qatar, only 27 bcm/y has been signed with Asian and European end-users, and only 15 bcm/y with aggregators (e.g., Shell and ConocoPhillips), which will need to re-sell the LNG to buyers (see Figure 3). Therefore, 78 bcm/y (75% of the total) is either not contracted at all or contracted with a buyer that needs to re-sell it.

Why Qatar Matters in the Current LNG Wave

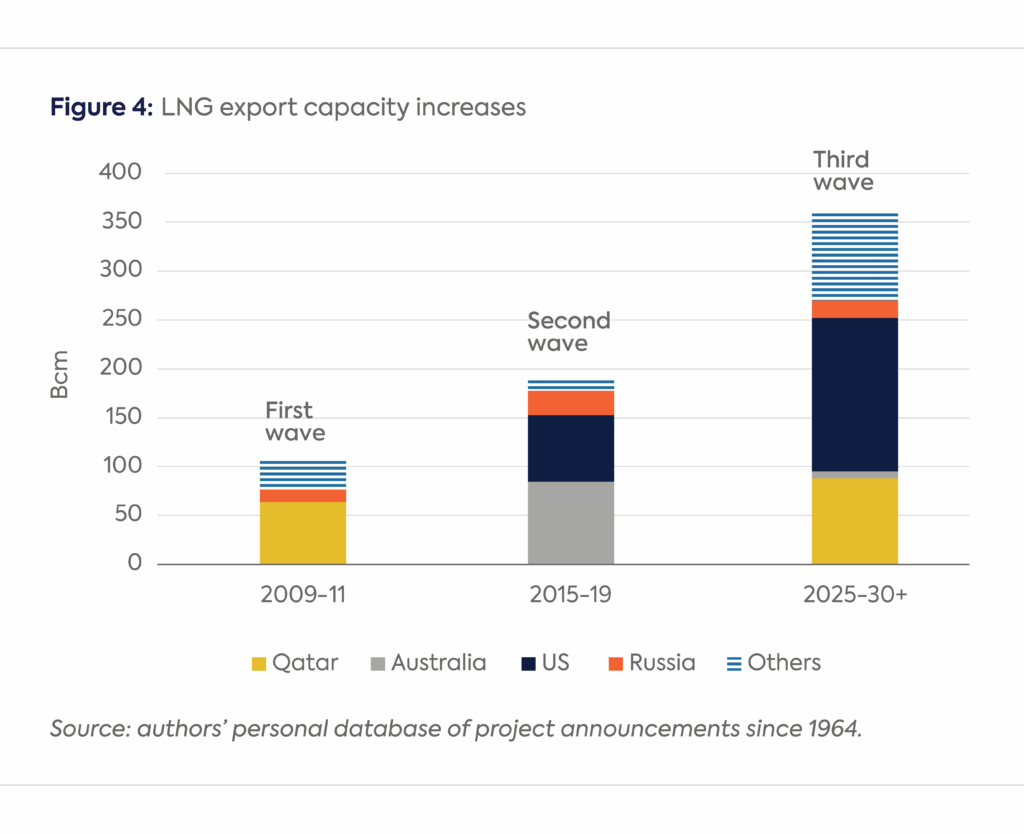

The world is currently witnessing an unprecedented surge in under construction or already committed LNG export capacity: 360 bcm/y as of the time of writing. This increase is significantly greater than the approximately 100 bcm/y added during the first LNG wave (2009–11), and the 200 bcm/y added during the second one (2015–19) (see Figure 4). Some uncertainties remain around Russia’s Arctic LNG 2, currently under sanctions, and the mothballed Mozambique LNG project.[7] For context, global LNG trade reached 550 bcm in 2024[8] and is likely to increase by around 50 percent by the early 2030s even if these two projects (45 bcm/y) do not move ahead and accounting for supply declines from existing LNG projects.[9]

The US and Qatar are expected to account for two-thirds of this third wave. Once the LNG projects under construction and committed are completed, US LNG export capacity will exceed Qatar’s by 45 percent. Although there is growing competition between US and Qatari LNG, QatarEnergy holds 70 percent of the US-based 18-mtpa Golden Pass project, while US ExxonMobil — the other shareholder in Golden Pass LNG — has shares in several Qatari LNG trains, resulting in mutual penetration. While Qatar holds substantial domestic gas reserves, any effort to expand its LNG export capacity would face the significant challenge of securing more long-term LNG contracts.

Qatar’s Inadvertent Experience with Spot LNG Trade

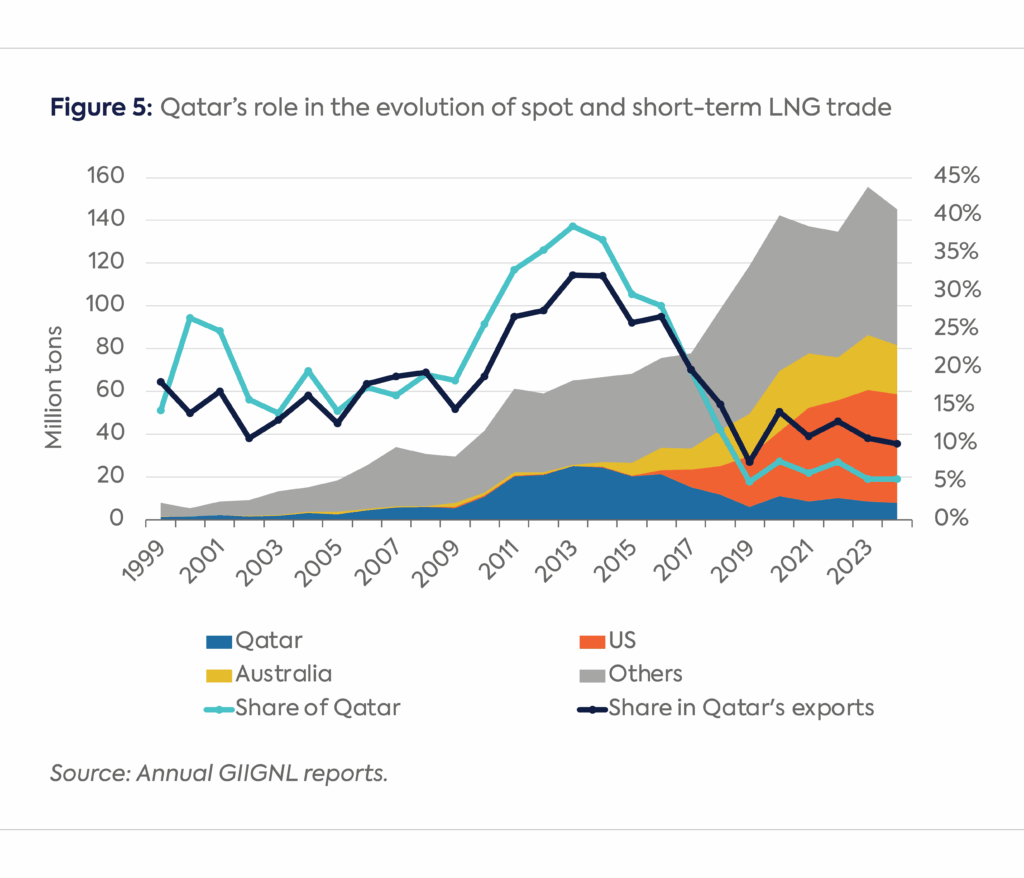

Despite its long-standing emphasis on long-term contracts, Qatar has extensive experience with spot and short-term markets. From early on, Qatar was delivering spot cargoes to the US (CMS), Spain (Enagás), France (Gaz de France), Korea (Kogas), and other countries due to a ramp up structure in Qatar’s contracts that let buyers work their way up to full commitments over an extended period of time.[10] Qatar then played a determinative role in the rise in spot and short-term trade during the early 2010s, which more than doubled between 2009 and 2014, with Qatar accounting for half the increase. The country’s share in total spot and short-term LNG trade peaked at 39 percent in 2013 (See Figure 5).

This role for Qatar was hardly a deliberate choice, however. When Qatar reached final investment decision (FID) on six 8-mtpa mega-trains in 2004–5, the output from Qatargas III, Qatargas IV,[11] and RasGas III’s two trains[12] was originally largely destined for North America. But just when Qatari LNG export facilities came online, the rapid expansion of US shale gas production between 2005 and 2010 dramatically reduced the US’s need for LNG imports. In response, Qatar activated diversion rights in its contracts with the US, allowing it to redirect the volumes to other markets. Nevertheless, Qatar remained committed to its existing strategy by signing around 26 bcm/y of new long-term contracts with Asian and European companies with start dates between 2014 and 2020. Qatar now plays a limited role in spot and short-term LNG trade.

Qatar’s Three Options and Their Implications

With around 75 percent of its new LNG capacity uncontracted by end users, and amid growing competition from US gas, Qatar could pursue one of three options to navigate potential global oversupply, each of which would have far-reaching implications for global LNG markets.

Engage in active market management. In this scenario, QatarEnergy would restrict exports at the currently contracted volumes plus an additional 10 percent sold under spot contracts, maintaining a market strategy focused on long-term agreements (see Figure 1). Consequently, the company would delay the start-up of LNG trains with uncontracted LNG supply, mirroring its actions in 2009 when LNG trade lagged capacity expansion due to unfavorable market conditions.[13]

As the gap between contracted Qatari LNG and capacity expected to come online widens, the amount of LNG volumes withheld from the market between 2026 and 2030 would increase sharply, potentially softening the downward pressure on prices expected from the global LNG oversupply. The strategy hinges on the assumption that consumers, anticipating more affordable LNG, would be more amenable to sign long-term deals with Qatar. One crucial question is whether Qatar would be willing to adopt more flexible destination terms, which are a major requirement for many buyers. The country could also position itself as a supplier of LNG with very low methane emissions thanks to the simplicity of its gas and LNG infrastructure — especially compared with its main rival, the US.

If LNG importers were to remain reticent to buy from Qatar, however, the impact on the country’s revenues could be significant. While revenues from contracted LNG would be relatively protected — as they are largely oil-indexed — the effect on spot LNG sales could be sizable, even if spot prices remain elevated (compared to current assumptions). This strategy could also backfire if more alternative suppliers take FID between 2026 and 2030, further reducing Qatar’s long-term sales opportunities.

Recent developments in Qatar and the US point toward this scenario. In May 2025, QatarEnergy’s CEO announced that the North Field East expansion would begin in mid-2026, instead of the previously planned late 2025.[14] Meanwhile the US Golden Pass project received a three-year extension (to November 2029) from the Federal Energy Regulatory Committee for bringing its three trains into service.[15]

Incentivize demand. Under this scenario, Qatar would lower prices and maximize the flexibility — timing and volume — of LNG offtakes. The lower end of price indexations in new contracts (ranging from 10.25 to 13.2% Brent) would spur more demand. Since lifting and liquefaction costs combined are below $2/mmBtu, with voyage costs to Northeast Asia adding another $1 to 2/mmBtu, Qatar could still make profits with a 6 percent slope at $70/bbl Brent or a 7 percent slope at $60/bbl Brent.

Contract flexibility is also enticing for buyers, given expectations that the spot market will grow. LNG contracts are typically based on an average and total contract quantity (ACQ and TCQ). Some contracts have a minimum contract quantity (MCQ), which allows buyers to nominate down to 90 percent of their monthly allotment based on the ACQ. Lowering the MCQ to 80 percent, while allowing buyers to make up the difference on the TCQ over an extended period (3 to 5 years after the contract expires), would allow buyers to ease the pain of higher prices. Conversely, allowing buyers to nominate upward by 10 to 20 percent per month in a lower price environment would also be enticing.

Another option is to target specific end-use sectors, with consumption restricted and tied to price. An indexation at 7 to 9 percent would foster higher power sector use, particularly in countries willing to impose a carbon price on coal and gas use. Qatar could also stimulate demand by investing in downstream infrastructure to support higher industrial or commercial use. For example, it could allocate part of its LNG contract proceeds to developing LNG import terminals and pipeline links to industrial hubs through sovereign guarantees or low-risk loans that reduce investment risk.

Offering buyers lower prices and more flexibility is not without risks. Until now, QatarEnergy has been resistant to sell volumes at low prices, with exceptions tied to the wealth of the buyer country and the geopolitical advantages garnered. Ceding more price discovery to the spot gas market will affect margins and potentially expose Qatar to competition with its own re-sold cargos. It could also send a signal that lower prices are sustainable, which could in turn not only delay FIDs from other LNG projects globally, but also affect Qatar’s own expansion plans. Finally, lowering prices could undermine Qatar’s ability to renegotiate with existing customers, who now feel they have been overpaying on previously signed contracts. Older contracts have re-openers that are reviewed every 3 to 5 years and triggered by significant changes in market conditions. The upside of a more price-friendly, less rigid contract structure for Qatar, as for the Saudis back in the 1980s, is that ceding the idea of a central tendency price to the spot market reduces the potential spotlight on the country, justified or not, as an intentional price manipulator.

Adopt an aggressive market share strategy. Under this scenario, QatarEnergy would opt to sell all uncontracted volumes on the spot market, accelerate the commissioning of its LNG trains, and abandon its restrictive destination terms, encouraging buyers to contract on a spot or short-term basis. In practice, this would mean that the six trains from its North Field East and South Expansion projects would come online sequentially every three months, bringing 65 bcm/y of new LNG capacity to the market between mid-2026 and late 2027. The trains from the North Field West expansion, sanctioned in 2024, would follow, starting in 2028. Meanwhile, the three trains of the Golden Pass facility would start between late 2025 and late 2026.

This strategy aims to create a demand shock by strongly lowering gas spot prices, thereby also undercutting US LNG and potentially forcing shut ins. It would resemble OPEC’s 2015 strategy to squeeze higher-cost US shale oil producers out of the market.[16] The approach would be particularly effective if Henry Hub gas prices were in the $4 to 5/mmBtu range, driven by increased gas demand from US-based data centers.

While revenues from contracted LNG would not be impacted in this case either, spot sales would generate lower unit revenues, despite higher volumes — though potentially still outperforming revenues under the conservative “active market management” scenario. That QatarEnergy’s LNG export capacity spans both the US and Qatar makes market coordination more challenging. The strategy’s longer-term objective would be to create sustainable demand growth, setting the stage for new long-term contracts (10 to 20 years) signed in the late 2020s and early 2030s, like the mid-2010s cycle.

Conclusion

Qatar has many policy levers at its disposal to successfully navigate potential oversupply over the next five years. While its role in the market has traditionally been passive, it will need to become more active in the spot market, given that 75 percent of its capacity is either uncontracted or in the hands of aggregators. Qatar’s decisions carry massive implications for all stakeholders in the broader LNG market, potentially deepening the oversupply by pushing prices to very low levels or maintaining higher prices, incentivizing long-term gas and LNG demand, and derailing competitors’ expansion plans.