Kuwait looks to the cloud as power grid feels the strain

Kuwait has invited bids to construct three power substations that will supply electricity to Google Cloud data storage centres

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

Venezuela holds 70% of Latin America's natural gas reserves, which it could export to Colombia and Trinidad to increase revenues.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

From the affordability crisis and the data center boom, to the US government’s campaign to reinvigorate the Venezuelan oil market, energy is dominating headlines in unusual ways. And...

Find out more about our upcoming and past events.

The Center on Global Energy Policy at Columbia University SIPA's Women in Energy initiative and Accenture invite you to join us for an evening of conversation and networking...

Reports by Luisa Palacios, Gautam Jain & Preetha Jenarthan • June 30, 2025

This working paper represents the research and views of the authors. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. This working paper was funded through a grant from EDF. More information is available at Our Partners.

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc.

Foundations and Individual Donors

Anonymous

Anonymous

Aphorism Foundation

the bedari collective

Children’s Investment Fund Foundation

David Leuschen

Mike and Sofia Segal

Kimberly and Scott Sheffield

Bernard and Anne Spitzer Charitable Trust

Ray Rothrock

The authors would like to express their most sincere gratitude to Christophe McGlade (IEA), Gianni Lorenzato (World Bank), Meredith Block (PIMCO), Dominic Watson (EDF), TJ Conway (RMI), Elena Nikolova (RMI), Chandra Gopinathan, Ana Diaz (CBI), Anna Creed (CBI), Cindy Levy (McKinsey), and Sarika Chandhok (McKinsey) for their very thoughtful and detailed comments on an earlier draft of this paper.

The authors would also like to thank the members of the Methane Finance Working Group for their valuable insights during the six discussion sessions chaired by the authors, which informed large sections of this paper. The authors are further grateful to the members of the Finance Working Group who agreed to share their time and expertise in follow-up bilateral sessions.

Finally, the authors would like to thank all the members of the Steering Committee of the Methane Finance Working Group—which, besides CGEP, consisted of EDF, CBI, RMI, and Atlantic Council, as well as McKinsey as a knowledge partner—for a meaningful partnership in the advancement of pragmatic solutions for abating methane emissions. Meredith Block deserves particular recognition for her incredible leadership and partnership.

This working paper represents the research and views of the authors. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to

further revision.

This working paper was funded through a grant from EDF. More information is available

at https://energypolicy.columbia.edu/about/partners.

Human-caused methane emissions have contributed to at least one quarter of global warming since the preindustrial era.[1] Since methane is 80 times more potent than carbon dioxide (CO2) in trapping heat over the first two decades after its release, abating methane is considered a critical near-term strategy for reducing emissions.[2]

Even with the urgent need for action, methane emissions from the energy sector reached a near-record high in 2023, largely driven by the oil and gas industry.[3] To limit global temperature rise to 1.5 degrees Celsius, methane emissions from the oil and gas sector must fall by at least 75 percent by 2030. This is a pivotal condition for the global energy sector to reach net zero by 2050, as outlined in the International Energy Agency (IEA) Net Zero Emissions by 2050 Scenario (NZE Scenario).[4]

The United Nations Framework Convention on Climate Change has identified methane abatement from the oil and gas sector as one of the most cost-effective strategies to rapidly reduce the rate of warming and contribute substantially to global efforts to limit the temperature rise to 1.5 degrees Celsius.[5] However, capital deployment for methane abatement is falling short of the pace needed to meet the 2030 reduction conditions despite favorable economics and recent policy support.

In response to the growing urgency to address methane emissions, a strong consensus emerged at the 2023 United Nations Climate Change Conference (COP28) in Dubai regarding the critical need to increase investments in methane abatement efforts within the oil and gas sector.

Why was the Methane Finance Working Group convened? Three key initiatives came out of COP28 to encourage the prioritization of methane abatement, focusing on commitments, technical expertise, and capital deployment. First, the Oil & Gas Decarbonization Charter (OGDC), a global industry charter outlining commitments, including methane abatement targets, was launched to transition the sector to low-carbon operations and accelerate climate action.[6] Second, the World Bank’s Global Flaring and Methane Reduction Partnership (GFMR) launched a multi-donor trust fund composed of governments, oil companies, and multilateral organizations committed to ending routine gas flaring at oil production sites across the world and reducing methane emissions from the oil and gas sector to near zero by 2030.[7] Lastly, the Methane Finance Working Group (MFWG) was launched to create a blueprint for scaling financing and driving investments in methane abatement projects across the oil and gas industry that should also simultaneously support the fulfillment of OGDC commitments and amplify GFMR capital.

While inclusive of the entire value chain, the Guidance for Including Methane Abatement in Oil and Gas Debt Structuring (the Guidance) has been designed to include national oil companies (NOCs), which are responsible for over half of global oil production.[8]

What was the goal of the Methane Financing Working Group? The Methane Financing Working Group aimed to leverage global financial markets to drive capital toward methane emissions reduction projects in the oil and gas sector that align with the methane and flaring reductions outlined in the IEA’s NZE Scenario. The objective was to develop voluntary guidance that is viewed as credible from a climate perspective, utilizing broadly established market mechanisms already familiar to capital seekers and capital providers alike. To achieve this, the Working Group served as a forum for various stakeholders in the oil and gas sector—including oil and gas operators, solution providers, financial institutions, civil society, academics, and climate science experts—to discuss the opportunities and challenges of scaling investments for methane emissions abatement globally.

What is the Methane Finance Working Group’s first deliverable? The Working Group has developed voluntary guidance for debt-financing structures commonly used in global capital markets to facilitate large-scale capital deployment for methane reduction. The Guidance is a consolidation of the Working Group’s initial findings and recommendations.

The Guidance targets short- to mid-term real economy emissions reductions and is designed for use by capital seekers, providers, and other stakeholders. While the Guidance primarily supports the bond and loan markets, it could also apply to private credit and project finance. Drawing on the proven ability of broadly defined sustainable finance structures—specifically thematic or labeled instruments—to scale financing, the Working Group considered three financing structures for methane abatement initiatives: key performance indicator (KPI)-linked, use-of-proceeds (UoP), and conventional (unlabeled) instruments with covenants. The Guidance provides details for structuring the first two types of instruments specifically for targeting methane abatement, and this document covers the Working Group discussions on all three types of instruments.

Which stakeholders does the Guidance target? The Guidance is designed to accommodate the governance, technical capacity, and capital structure of capital seekers and counterparties, including emerging and frontier market NOCs, well-capitalized NOCs based mostly in developed countries, international oil companies (IOCs), independent exploration and production companies (E&Ps), oilfield services providers, multilateral development institutions, incorporated joint ventures, special purpose vehicles, midstream operators, oil and gas investors, asset managers, asset owners, and financial intermediaries. The Guidance also targets financial intermediaries who consider themselves to be climate-aligned, recognizing the importance of maintaining asset integrity and improving production efficiency for both fiduciary and climate risk management considerations.

What were the Working Group’s structure and guardrails? The Working Group’s structure and guardrails were designed to ensure effective collaboration and outcomes across its Technical, Financial, and Industry working groups. The Environmental Defense Fund (EDF) and Climate Bonds Initiative (CBI) co-chaired the Technical Working Group, and the Financial Working Group was chaired by the Center on Global Energy Policy (CGEP) at Columbia University’s School of International and Public Affairs, with RMI as the facilitator. The Industry Working Group was chaired by the Atlantic Council, with McKinsey as a knowledge partner. Regarding the three working groups:

Ultimately, the Working Group sought to facilitate faster deployment of capital at scale to significantly reduce methane emissions across the oil and gas value chain, creating an ecosystem where capital seekers, providers, and structuring agents can confidently engage in transactions that fulfill fiduciary responsibilities, align with scientific consensus, and produce robust and verifiable emission reductions.

The IEA lists several actions that must be taken by 2030 to achieve net-zero emissions in the energy sector globally by 2050 and limit the temperature increase to 1.5 degrees Celsius. As outlined previously, one of the required key actions is reducing methane emissions from the oil and gas sector by approximately 75 percent.[11] Methane emission reduction is cited at the same level of importance as a threefold increase in the capacity of renewables-based electricity generation, doubling the rate of energy efficiency improvements, and considerable increases in electrification (see Figure 1).[12] Substantially reducing methane emissions from the oil and gas sector by 2030 was also a key commitment made at COP28.[13]

Source: “Net Zero Roadmap: A Global Pathway to Keep the 1.5°C Goal in Reach,” International Energy Agency, September 2023, p. 108, https://www.iea.org/reports/net-zero-roadmap-a-global-pathway-to-keep-the-15-0c-goal-in-reach.

Reducing emissions from the oil and gas industry holds the largest abatement potential relative to any other anthropogenic activity. Existing technologies are capable of abating most of the emissions in the sector,[14] with about 50 percent of such mitigating measures at a low cost, and some even at a negative cost.[15] Despite its high potential as a critical enabler of the IEA’s NZE Scenario, the world is not on track to meet the 75 percent methane emission reduction in the oil and gas sector by 2030. According to the IEA’s methane tracker, methane emissions from fossil fuels are not yet declining, with the 2023 level of emissions about the same as in 2019.[16]

For the oil and gas sector to take effective action against this invisible challenge, a better understanding of the obstacles to mobilizing capital into methane abatement solutions is needed, particularly in emerging markets.[17] Some of the obstacles to deploying capital for methane abatement in the sector include lack of regulation and cost of capital but also lack of financial incentives to undertake these methane abatement projects. The lack of financial incentives might be associated with internal competition within a firm for investment resources vis-à-vis other projects with higher profitability, lack of understanding of the costs associated with such projects, and/or lack of appetite to finance the infrastructure needed to recover the vented and flared gas.[18]

What is the investment gap in this critical decarbonization vector? In 2023, the IEA estimated that about USD 100 billion in cumulative spending will be needed for a 75 percent reduction in methane emissions in the oil and gas sector by 2030.[19] In 2024, McKinsey & Company estimated that the spending required to eliminate methane emissions is even higher, at around USD 200 billion by 2030, including the cost of building the infrastructure to bring the recovered methane to existing pipelines.[20] These estimates translate into USD 14–33 billion in annual capital deployment for methane abatement in the sector through 2030. However, according to Climate Policy Initiative’s (CPI) estimates, based on publicly available data, only USD 11 million of average annual investments were identified for methane abatement in the oil and gas industry for the 2021–2022 period.[21]

The low level of spending reported by CPI might, in large part, reflect a lack of up-to-date and transparent data, the absence of standardized reporting frameworks, and the difficulty in distinguishing methane abatement investments from routine operational expenditures across the industry. This underscores the urgency of better disclosures about methane abatement spending, which the Methane Finance Working Group seeks to address. Notwithstanding the probable underreporting of spending toward methane reduction, the gap in capital deployment is likely considerable in this critical decarbonization lever, with one of the highest global warming reduction benefits per dollar invested.[22]

This gap in capital deployment stands in stark contrast to the growing pledges and commitments around methane abatement by the industry (see Figure 4 in section 2.3 about methane pledges). A more focused approach is thus needed to ensure transparency around oil and gas companies’ methane abatement spending and the investments they are prepared to undertake to reduce methane emissions.

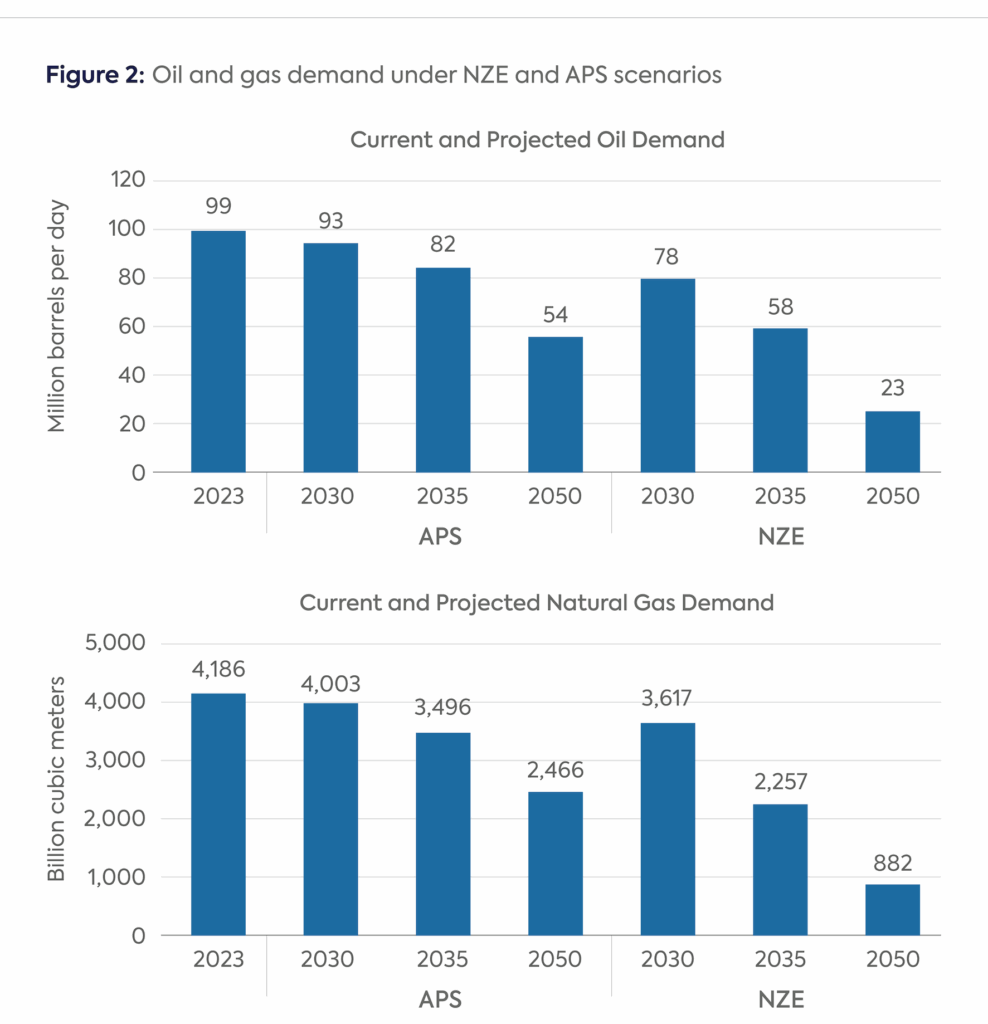

Even under the NZE Scenario, a substantial amount of oil and gas will still be consumed globally in the next decade. To have a chance of staying within reach of the target of limiting temperature increase to 1.5 degrees or even two degrees Celsius by 2050, oil and gas should be produced with near-zero methane emissions.[23] According to the IEA’s World Energy Outlook 2024 (WEO), oil demand aligned with the NZE Scenario is expected to be around 78 million barrels per day (b/d) by 2030 and almost 58 million b/d by 2035 versus 99 million b/d in 2023 (see Figure 2). Regarding natural gas, the IEA’s latest WEO foresees demand at 3,617 billion cubic meters (bcm) by 2030 and 2,257 bcm by 2035, consistent with the NZE Scenario versus 4186 bcm in 2023.[24]

The oil and gas consumption expected under the various 2030 energy transition scenarios makes methane abatement a critical and urgent action for limiting temperature rises.

Note: APS refers to IEA’s Announced Pledges Scenario, which is based on countries implementing their national climate commitments in full and on time. Source: “World Energy Outlook 2024,” International Energy Agency, October 2024, https://www.iea.org/reports/world-energy-outlook-2024.

In line with the IEA, the Working Group concluded that targeted actions to tackle methane emissions from fossil fuel production are essential “to limit the risk of crossing irreversible climate tipping points” even in the NZE Scenario.[25] However, methane abatement in the oil and gas sector is even more critical in the context of much higher fossil fuel use, which is the current trajectory that the world is on, avoiding roughly 0.1 degrees Celsius warming in 2050, comparable to eliminating all CO2 emissions from all heavy industry globally.[26]

It is beyond the scope of this guidance to determine which countries, basins, and companies should be producing the oil and gas that the world will need by 2030, 2035, 2040, or 2050 under NZE or any other energy transition scenario and, thus, where the financing and the investments for such activities will or should take place. Rather, the Methane Finance Working Group’s goal is to encourage capital deployment to decarbonize supply by providing best practices and guardrails for methane-abating activities.

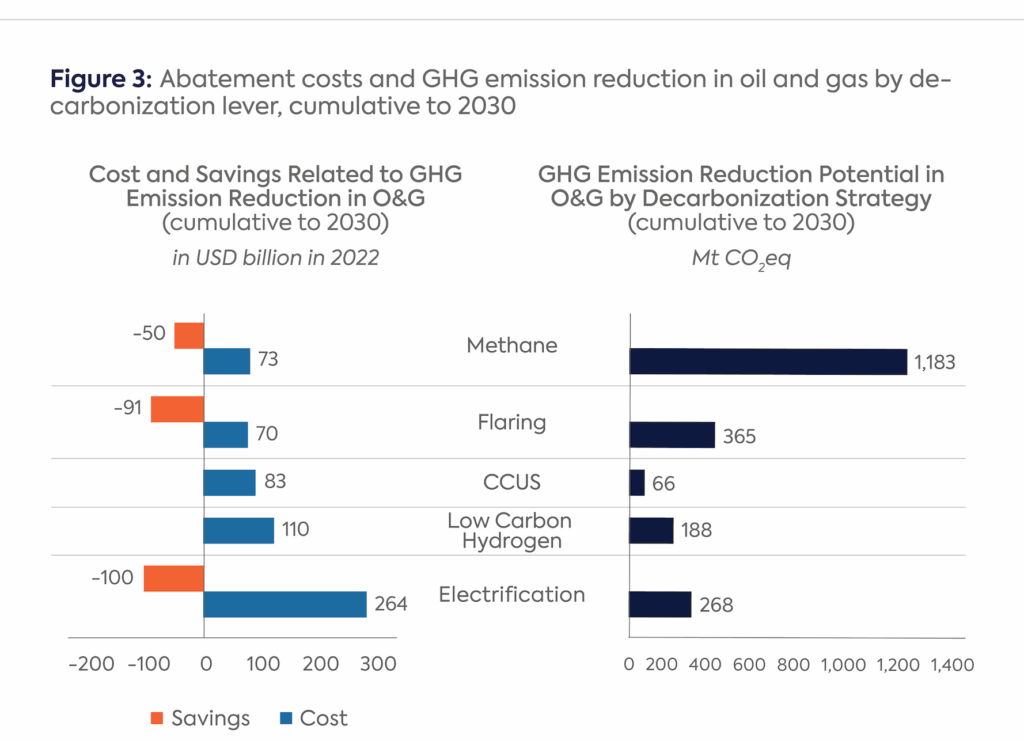

Of all the decarbonization levers the oil and gas industry has to reduce its GHG emissions, including CCUS, low-carbon hydrogen, electrification, and reducing methane emissions, the last is the most effective, as shown in Figure 3.[27]

The Guidance includes a series of abatement measures for methane specifically, as part of the proposed financial structures, that are in line with the IEA’s recommendations. These solutions include boosting operational excellence at extraction sites by increasing the energy efficiency of processes; monitoring and capturing methane venting, including leaks; capturing and storing combustion gases or directly vented CO2;and reducing flaring. The World Bank has highlighted the critical relationship between flaring and methane emissions, given the risk of the potentially more adverse impact of inefficient flares (i.e., unlit) on methane emissions than currently estimated.[28]

Source: “Cost and Savings in the Net Zero Scenario, 2030,” International Energy Agency, May 2023, https://www.iea.org/data-and-statistics/charts/cost-and-savings-in-the-net-zero-scenario-2030; “Emissions Reductions in the Net Zero Scenario, 2030,” International Energy Agency, May 2023, https://www.iea.org/data-and-statistics/charts/emissions-reductions-in-the-net-zero-scenario-2030.

The needed reduction in methane emissions by 2030 assumes that the available methane abatement technologies are deployed across all oil and gas production, processing, and transport facilities by 2030 so that the industry-wide emission intensity converges with that of the world’s best operators today.[29] It is important to note that the IEA assumes that around 30 percent of the methane emissions reduction in the NZE stems from the fall in oil and gas demand over this period, which means methane abatement projects and activities need to be deployed to achieve the remaining 70 percent reduction. As explained earlier, in the current oil demand trajectory, which is not aligned with a 30 percent decline in demand, abating methane in the supply of oil and gas globally is even more critical.

Oil and gas companies with a net-zero target by 2050―encompassing scopes 1, 2, and 3 emissions—account for less than 6 percent of the global oil production.[30] However, achieving a 75 percent reduction in methane emissions would require increasing capital deployment for methane emissions reduction projects globally. As explained earlier, the IEA has stated that reductions in fossil fuel use alone―even in the NZE Scenario―do not achieve deep enough cuts in methane emissions to reach levels consistent with limiting warming to 1.5 degrees Celsius and that additional, targeted actions to tackle methane emissions from fossil fuel production and use are essential.

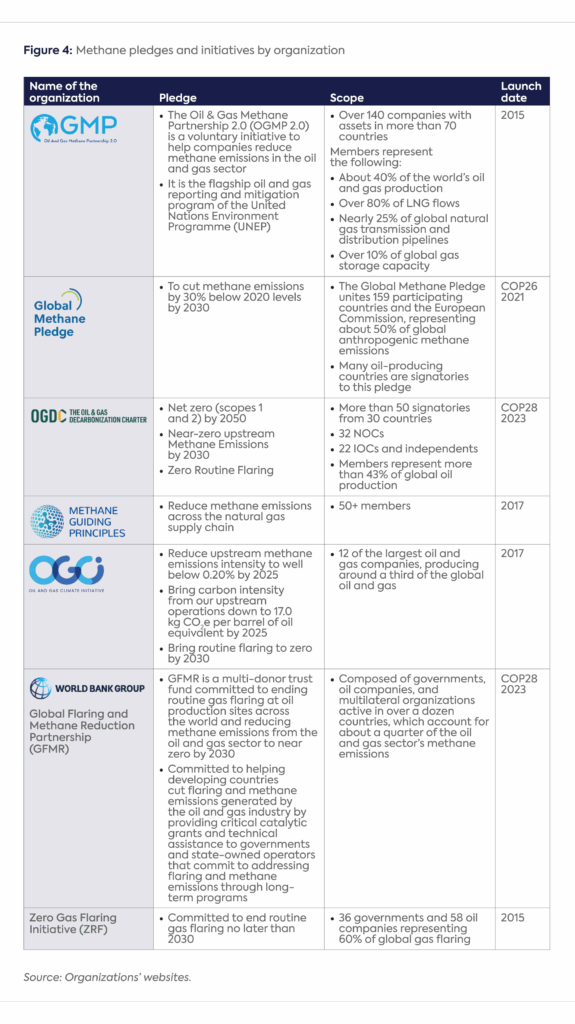

Currently, oil and gas companies with pledges to reduce methane emissions in their oil and gas operations represent a growing universe and present an opportunity to transition from pledges into action (see Figure 4). Recent commitments include the Global Methane Pledge, which has participation from 159 countries, and the OGDC, which has over 50 signatories—30 of whom had not previously engaged in other international initiatives aimed at mitigating methane emissions and flaring, including many NOCs—illustrating a growing collective effort to combat methane emissions. Despite the progress made, capital being deployed for methane abatement in the oil and gas sector is falling short of the pace required to meet the 2030 target.

To implement methane commitments, companies must deploy capital for methane-abating projects and activities, including measurement. Capital markets should encourage the prioritization of spending on abatement, as companies seek external financing through the regular course of business. Unfortunately, the capital deployment for methane abatement is alarmingly low, not well understood, and not prioritized, partly because of a lack of incentives for companies and countries to pursue methane emission reductions.[31] UNEP, in its methane report, states that “achieving global climate goals hinges on a decisive shift from ambition to action.”[32] This guidance seeks to help with the critical piece of this puzzle: ensuring that capital from the private sector is deployed to translate ambition into actionable methane abatement activities in the oil and gas sector.

The IEA has identified a range of potential sources of financing to support methane abatement, including governments, development finance institutions, commercial banks, and the private sector.[33] Specifically, the IEA sees opportunities to link funding currently provided to the oil and gas industry—directly or indirectly—to methane abatement through the issuance of securities, which can be tied to sustainability.

Similarly, the World Bank’s GFMR has identified a variety of sources that include oil and gas companies, oil service operators, governments, development finance institutions, commercial banks, private capital funds, and strategic investment funds.[34] Among the potential instruments for flaring and methane reduction by investors, the World Bank cites green bonds and loans, transition bonds and loans, and sustainability-linked debt as instruments that could be deployed for such purposes. The bank does acknowledge, though, that their application for flaring reduction and methane abatement may be difficult because of the prevailing green bond and loan standards.

The Guidance seeks to put these recommendations into practice and support capital deployment by expanding the current scope of thematic or labeled debt to include specific features targeting flaring and methane emission reductions in sustainable debt instruments issued by the oil and gas sector. The Methane Finance Working Group developed guidance aligned with International Capital Market Association (ICMA) guidelines for green, sustainability, and sustainability-linked instruments and seeks alignment with relevant components of the Climate Transition Finance Handbook.[35]

This chapter aims to provide a brief introduction to the asset class, along with the different incentives and challenges that capital providers and seekers in the oil and gas industry face when using these instruments, as a precursor to the taxonomy of methane abatement features applicable to thematic instruments, which are detailed in the Guidance.

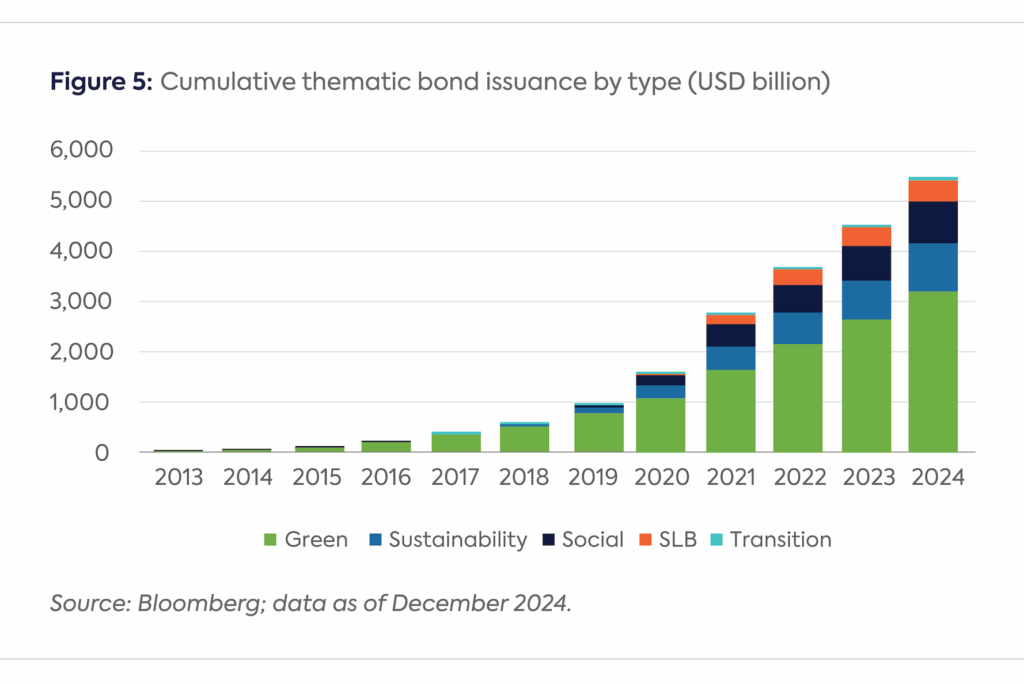

Although the first thematic bond―known as a Climate Awareness Bond―was issued in 2007,[36] the asset class did not gain broad acceptance among the investor and issuer community until the ICMA released the “Green Bond Principles” in 2015. One of the most important purposes these principles served was to provide assurance to investors by lowering “greenwashing risk,” which occurs when an entity uses sustainability as a pretext to gain market access and raise funds it might otherwise not have, but does not follow through on its promises. As the asset class gained credibility among investors, it expanded substantially in the ensuing period: both in terms of the amounts of thematic bonds issued and the types of bonds. Based on Bloomberg data, around $5.5 trillion of such bonds have been issued through Q4 2024 (Figure 5), with expectations that the asset class will continue to grow in the coming years[37]; despite the rapid expansion, the asset class comprises only about 4 percent of the global fixed income market, indicating room for growth.[38]

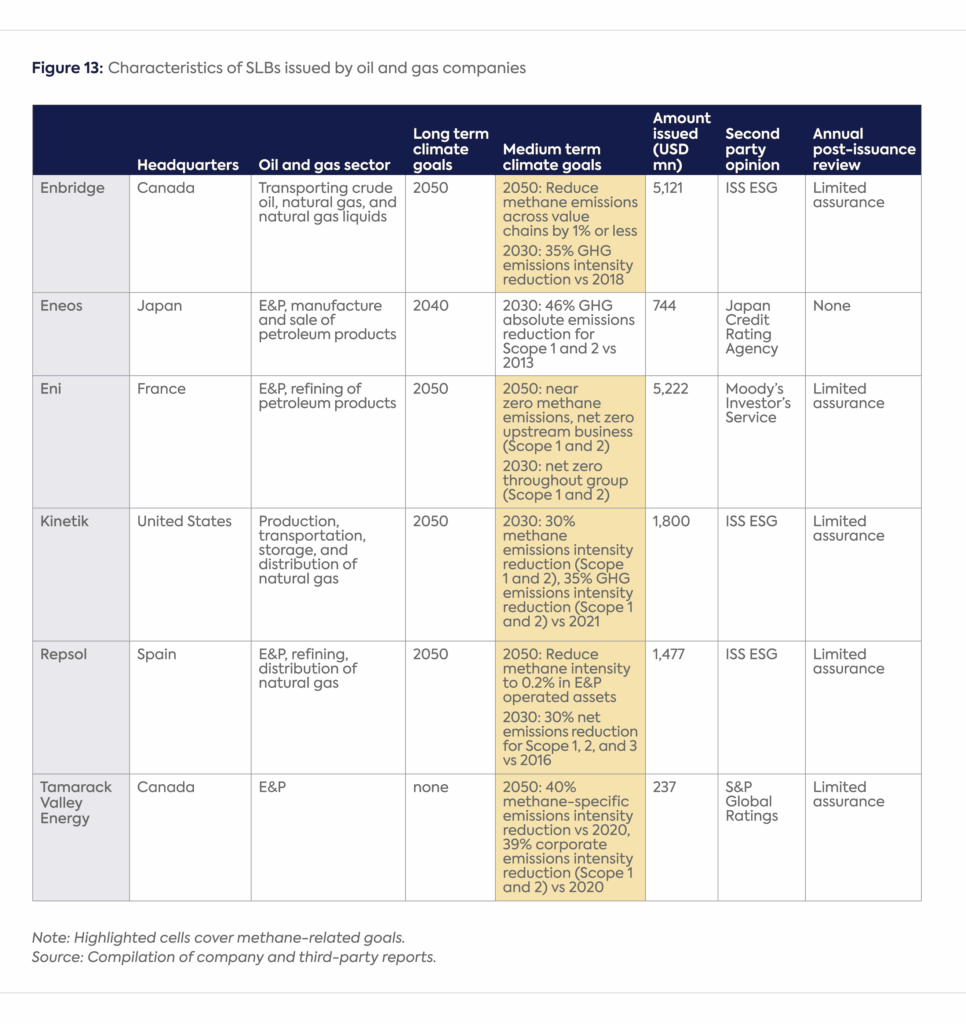

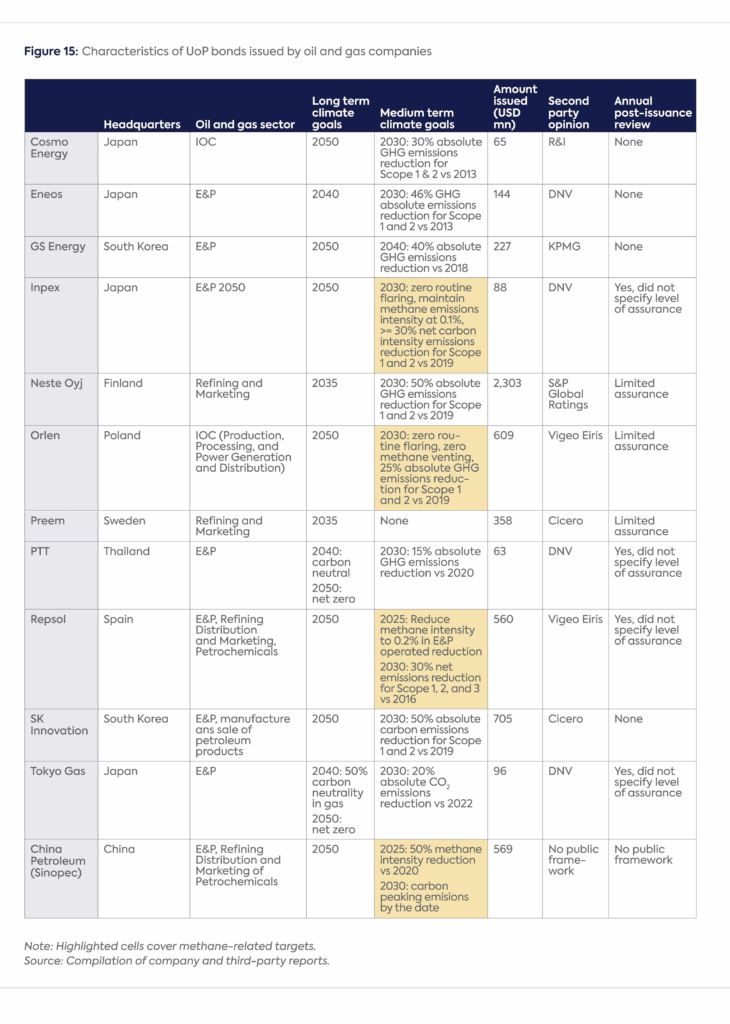

There are two broad categories of thematic bonds (or loans): use-of-proceeds (UoP) bonds and key performance indicator (KPI) bonds.[39] The funds raised by UoP bonds are tied to specific types of projects, unlike KPI bonds, whose proceeds are not earmarked for any specific projects or activities, but the bond issuer is expected to meet prespecified sustainability performance targets. The UoP bonds are further classified based on the type of projects covered: Green bond proceeds are directed toward environmental sustainability projects, social bonds fund projects targeting social issues, and sustainability bonds cover both environmental and social projects. Similarly, the most common type of KPI bonds are sustainability-linked bonds (SLBs), which typically have a penalty attached in the form of an increase in interest payments if the prespecified targets are not met. In addition, there are transition bonds, which target funding for the greening of brown sectors and can be either UoP or KPI type. Among these different types of labeled bonds, green bonds, sustainability bonds, and SLBs are the most relevant from the point of view of methane abatement in the oil and gas sector.

The most important reason for considering thematic instruments for methane abatement is their broad acceptance by investors as a means of meeting sustainability goals with low greenwashing risk while providing financial returns, as can be demonstrated by the strong growth of the asset class (Figure 5). ICMA’s green bond and SLB principles have played a significant role in lowering the greenwashing risk and providing assurance to investors, supported by the annual reporting requirement, along with the recommended pre-issuance and post-issuance external verifications.[40]

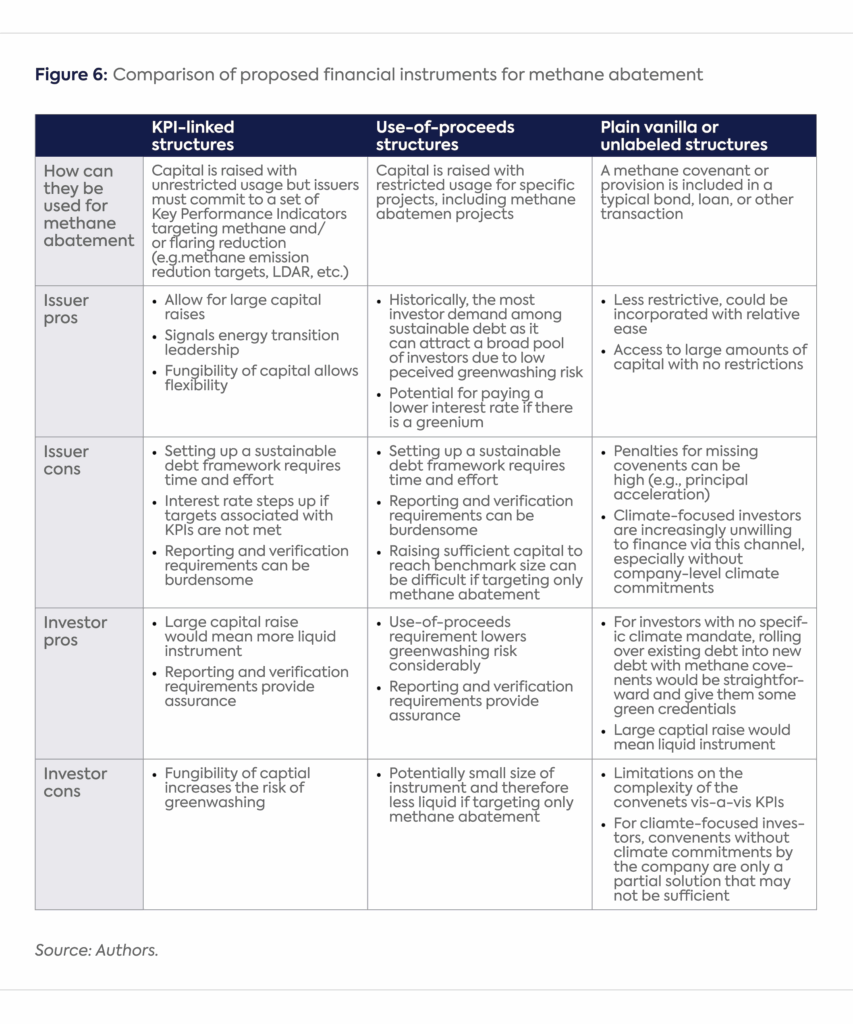

Figure 6 briefly describes how methane reduction features could be incorporated into thematic bonds and compares these instruments with conventional bonds, which can also be used by incorporating covenants targeting methane abatement. However, as the table shows, each instrument offers both advantages and disadvantages from the point of view of investors and issuers. It’s important to point out that the pros and cons highlighted in the table are not necessarily specific to methane reduction but apply more broadly to these instruments.

The Guidance proposed by the Methane Finance Working Group builds on the general description of the different instruments covered in Figure 6 to provide enhanced credibility for oil and gas capital seekers looking to issue thematic instruments. While ICMA has overseen the creation of a helpful framework that makes thematic bonds much more acceptable to investors, the eligible sectors in the guidance are intentionally described very broadly. To provide further assurance to investors, greater specificity may be valuable by complementing ICMA’s principles with sector-level guidance from relevant capital market authorities or international organizations. For example, the EU taxonomy for sustainable activities[41] and the Climate Bonds Initiative’s Climate Bonds Standard and Certification Scheme[42] include more detailed taxonomies of eligible investments. In a similar vein, the Guidance includes recommendations for issuers and investors to assess the scope of instruments that include methane abatement activities and targets.

Historically, there have been low levels of capital deployment in methane abatement in the oil and gas sector. There is a general lack of interest among capital seekers (oil and gas companies) and capital providers (investors) because of structural constraints such as a lack of financial incentives for countries and companies to mitigate methane, the effort needed leading to lack of interest to develop a pipeline of quality projects for methane reduction, prioritization given the opportunity cost of developing a methane project pipeline especially with projects competing internally for capital, and a lack of proper methane measurements, reporting, and verification.[43]

To encourage the faster deployment of capital at scale, the Guidance proposes UoP and KPI taxonomies that lead to real economy emission reductions via methane abatement activities and projects. Further, many of the recommendations in the Guidance improve production efficiency―a benefit for both capital seekers and their debt holders. While not covered in the Guidance, this working paper also includes a broad set of guidelines for using conventional instruments by incorporating appropriate covenants or provisions in the bond or loan indentures. Among capital providers, those without any specific sustainability mandates, conventional bonds with covenants targeting methane would likely be acceptable, as their focus tends to be more on the credit quality of the issuer.

The financing and capital allocation strategies of entities within the oil and gas industry are significantly influenced by their structural and operational characteristics. There is an underinvestment in methane abatement despite its significance in meeting net-zero goals. This underinvestment is driven by specific constraints that will require targeted incentives to overcome, depending on the type of capital seekers broadly categorized as NOCs, IOCs, independent operators, midstream operators, refinery and marketing companies, and oilfield services companies (OFSCs).

The motivations of each type of capital seeker in accessing the sustainable debt markets for methane abatement are discussed below.

Given the limitations and constraints that oil and gas companies face when issuing green bonds and SLBs, for some, adding methane-related conditionalities to conventional bonds might be the best way forward, as discussed in chapter 4.

To better understand the various perspectives of capital providers, the Methane Finance Working Group’s subgroup, FWG, conducted six working sessions with over 50 capital providers in each session, from over a hundred participants in total, and separately organized around 40 bilateral discussions. Capital providers include financial asset owners, asset managers, banks, debt capital markets specialists, and structuring agents. The goal of these sessions was to understand the interest in deploying capital for methane abatement projects, the barriers that various institutions face in participating in labeled transactions from oil and gas companies, the types of financial structures that could be used to address these concerns, and the potential demand for these types of structures. Once the stakeholders agreed on the main impediments, the Working Group focused on resolving those challenges where feasible to create an enabling financial ecosystem for these transactions.

Capital providers often face challenges investing in the oil and gas sector because of misalignment with broader climate goals and pledges. Additionally, emerging regulations regarding fund labeling in the EU may limit the ability of banks, financial asset owners, and financial asset managers to participate in labeled financing structures dedicated to the decarbonization of oil and gas companies. Through its discussions, the FWG brainstormed various ways to build credibility and guardrails into the Guidance to give market participants additional confidence that these transactions have a high likelihood of leading to real and tangible reductions in methane emissions. The main takeaways from those discussions are as follows:

As discussed earlier, participants in the Methane Finance Working Group raised concerns regarding greenwashing. These concerns might arise if a company commits to the KPIs of an SLB but fails to achieve any meaningful reductions in methane emissions with minimal penalties or if the applicable projects are defined too loosely for UoP bonds. Similarly, another related concern cited was the fungibility of capital—that is, part of the proceeds raised using a KPI instrument could lead to additional oil and gas production.

While fungibility and greenwashing risks certainly exist, and investors need to be vigilant about them, the likelihood that the instruments with features recommended in the Guidance are used for that purpose should be low for the reasons cited below, which are expanded in the sections that follow:

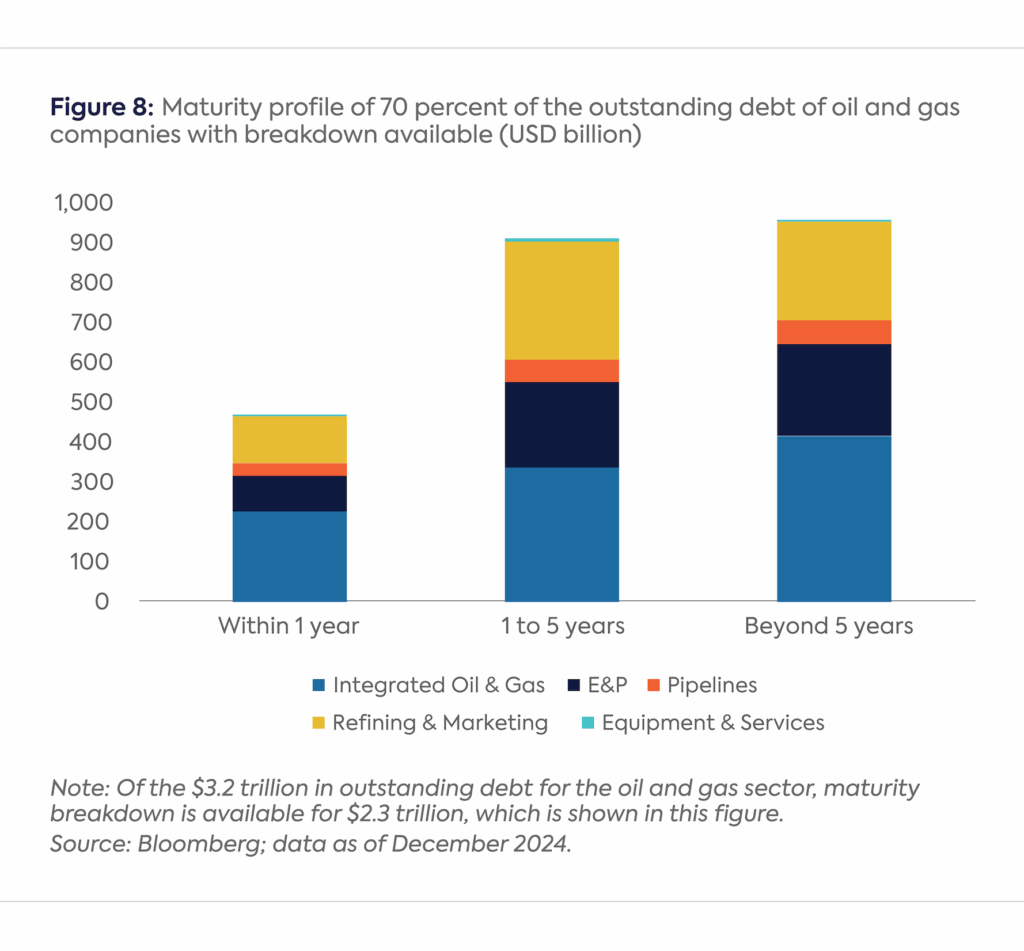

As mentioned at the outset, the total financing needed for methane abatement in the oil and gas sector is estimated to be between $100 and $200 billion. In comparison, the total debt—covering short-term and long-term bonds and loans of the sector—is around $3.2 trillion (Figure 7).

Although some individual companies could face difficulties in accessing additional financing, for the sector as a whole, the total capital that needs to be deployed for methane abatement financing is less than 6 percent of the outstanding debt. In other words, even if the entire estimated amount of $100–$200 billion needed for methane abatement is raised via debt, its impact on the sector’s capital allocation strategy should not be material and unlikely to be the driver for increased oil and gas production.

The need for increased borrowing for methane abatement can be further diminished by attaching methane reduction requirements to some of the existing debt that is getting rolled over, either as conventional instruments with covenants (as discussed in Chapter 4) or thematic instruments (as described in the Guidance). Indeed, given how large the rollover amount is, no new debt needs to be raised to specifically target methane reduction. Of the $3.2 trillion outstanding debt for the oil and gas sector, data on maturity breakdown is available for companies with $2.3 trillion of debt outstanding. For the companies for which the breakdown is available, almost 60% of the debt matures in under five years (Figure 8) or before the 2030 timeline used in the net-zero scenario for achieving a 75 percent reduction in methane emissions. At least some, if not most, of this maturing debt will likely be rolled over. There is thus an opportunity to attach methane abatement requirements, in new labeled or unlabeled debt, to as much of the bonds or loans being rolled over as possible. This is an important reason why this working paper suggests including methane abatement conditions in conventional instruments, as discussed in chapter 4, when labeled instruments are not viable either because of the lack of demand from investors or because it is not feasible for the capital seeker to issue these bonds.

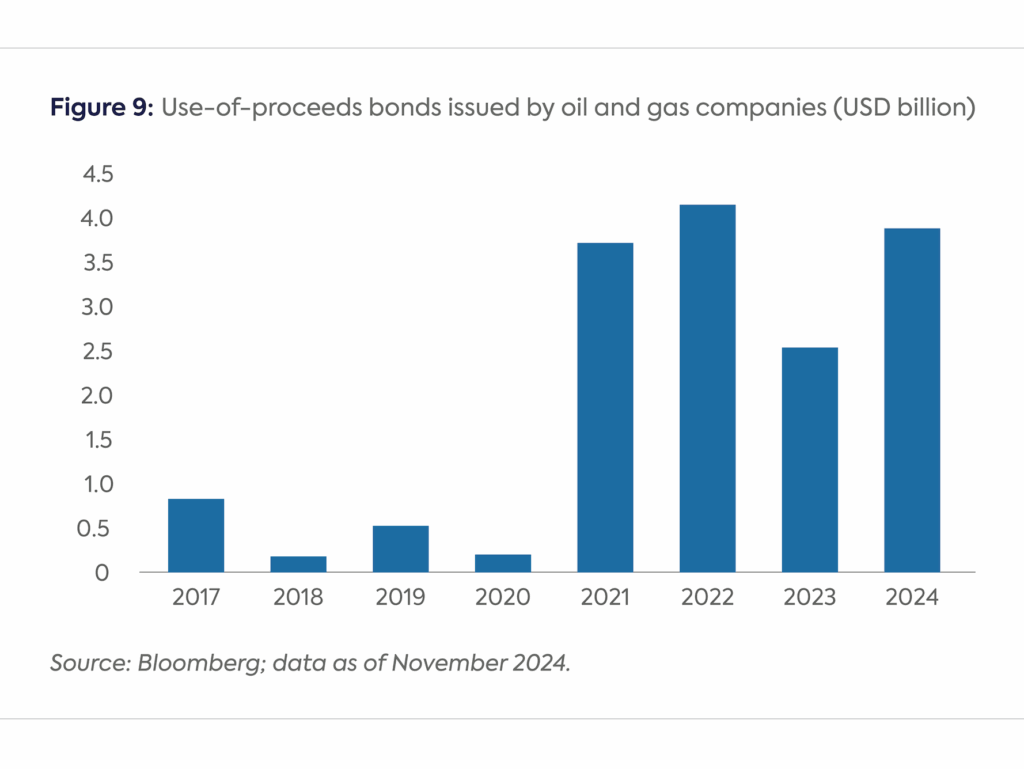

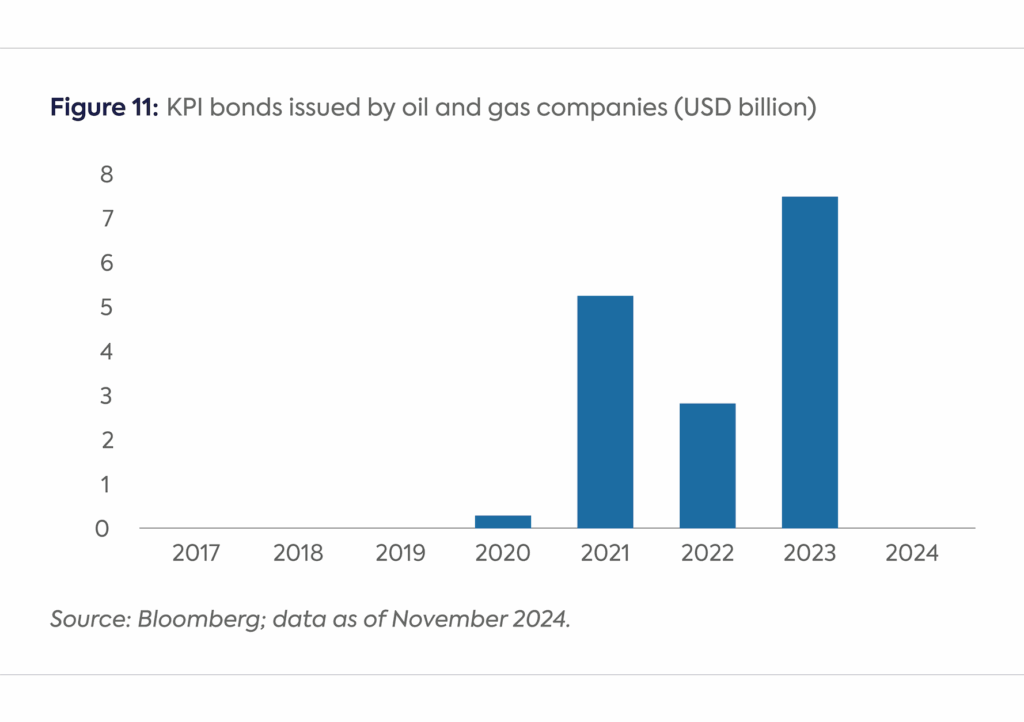

The proposal for oil and gas companies to issue thematic bonds to finance methane abatement activities and projects is not entirely new. Many oil and gas companies have successfully issued thematic bonds, especially since 2021, albeit they have not targeted methane, except for one bond that included reducing methane emission intensity among its KPIs. Nevertheless, previous issuances by the sector are important to analyze for the following reasons:

Several considerations, derived from the Methane Finance Working Group’s discussions with capital providers in the FWG, could either enable or impede financing for methane abatement projects in the sustainable debt market. These include the adaptability of financial structures to diverse issuer needs, the clarity and simplicity of KPIs, the accuracy of baseline data, and the design of accountability mechanisms that prevent greenwashing. By addressing these factors, the market can create more effective and scalable solutions for methane abatement. Knowing this, these factors were incorporated into the detailed technical recommendations for KPI and UoP instruments provided in the Guidance.

The following sections expand on these considerations based on the FWG discussions:

Thematic bonds and loans are the preferred approaches to finance methane abatement, given the success of the asset class in supporting the energy transition due to the strong buy-in from investors and the rigorous governance, reporting, and external verification requirements built into their design. However, when labeled instruments are not feasible for a capital seeker to issue, this working paper[55] suggests including covenants or provisions targeting methane abatement in bonds, loans, and other conventional financial instruments.[56] In other words, if issuing a sustainable bond or loan is not a viable option, an alternative might be to attach conditionalities to conventional instruments for lowering methane emissions. This is particularly relevant given that the oil and gas sector currently has more than $3 trillion of outstanding debt. Of this, for companies with $2.3 trillion of debt for which maturity breakdown is available, 60 percent is coming due before 2030. At least some―if not most―of which is likely to be rolled over (Figure 8).

Before exploring how these types of conditionalities could work with conventional instruments, the next section presents some of the challenges and opportunities of pursuing methane objectives through conventional finance.

Below are some of the highlights from the FWG roundtable discussions on introducing methane abatement conditionalities into conventional transactions:

Based on investor feedback, therefore, a prudent step would be to provide guidelines for conditions covering methane emission reductions that can be attached to debt rollovers. Two possible approaches―neither of which has been implemented in any bond transaction thus far―can be taken to link methane abatement to conventional finance transactions.

The following sections examine these two approaches in more detail and provide high-level examples of how they could work in practice.

As mentioned earlier, if a conventional transaction is the only available option, then one approach to reducing methane emissions could be to attach pre-issuance conditions. Specifically, a prerequisite to issuance could be to condition lending to a set of activities or steps that need to be taken that embed methane abatement into the capital seekers’ corporate practices. One such activity is becoming a member of one or more of the global methane initiatives listed in Figure 4 in Chapter 2, with a particular preference for the OGMP 2.0. This type of conditionality could center not only on pledges to reduce methane emissions as part of such membership but also on reporting requirements and alignment that are part of any of the existing voluntary corporate or national initiatives.

The UoP guidelines incorporate a list of key national-level methane initiatives, which include membership to OGMP 2.0,[58] Zero Routine Flaring by 2030 (ZRF) Initiative,[59] OGCI Aiming for Zero Methane Emissions,[60] OGDC,[61] and the Global Methane Pledge. Such membership requirements could also include reporting on methane emissions to investors if not already disclosed; for example, under the technical guidance of OGMP 2.0, asset or basin-level reporting on methane emissions is often not publicly disclosed to investors, only top-line corporate numbers.[62]

The suggested pre-requirements are in line with those required by the World Bank’s GFMR, which includes measuring and reporting emissions through the OGMP 2.0 framework, achieving near-zero absolute methane emissions by 2030 by reducing methane intensity to below 0.2 percent, and achieving zero routine flaring by 2030.[63]

The UoP recommendations (see the Guidance) also suggest a couple of actions that NOCs, in particular, could take. These include incorporating methane reduction targets into sustainability reporting commitments for the NOCs that currently have not done so, particularly those not listed on stock exchanges.

Since methane abatement action in EMDEs requires alignment with the shareholder government, the best path forward―particularly for engaging with capital providers―is to align sovereign borrowing with the action of the NOC on methane. Specifically,

Covenants and lending provisions can be used to incorporate methane emissions reporting and abatement requirements into a bond or loan indenture. Covenants are legally binding agreements reached between lenders and borrowers, which clearly outline what an issuer can or cannot do. They are typically meant to protect investors from the issuer overextending itself while allowing the issuer to run its business without undue restrictions.[64] As such, covenants are commonly used in bond issuance to regulate certain actions, such as paying dividends, incurring debt, and entering into a transaction with an affiliate. Historically, covenants have not encompassed climate-related clauses, and the suggestion in this working paper to do so is still untested.

Nevertheless, since climate can be a major financial risk to businesses, some investors have started proposing that climate provisions be included as covenants in unlabeled debt.[65] Some of these suggestions include requiring climate reporting linked to the issuer’s transition plan, barring investments in high-emission businesses with transition risks, restricting new emission-intensive lines of business, capping nongreen capital expenditures, and limiting the change of control to high-emitting companies with no transition plans, among others. The same covenants can be tailored to specifically target methane abatement as well.

Reporting covenants, for example, are standard in many corporate bonds. While reporting covenants have been typically used for requiring the publication of timely financial information, they could be modified to include methane reporting and even linked to some of the KPIs proposed in the Guidance. These types of reporting covenants are particularly useful in the case of NOCs since these bonds are generally not registered with the SEC. Moreover, many NOCs are 100 percent owned by their governments and thus are not listed on stock exchanges, avoiding the reporting requirements of listed oil and gas companies. Other covenants that could be adapted for methane abatement include restricting investments in oil and gas assets or mergers with companies that do not include methane abatement plans.[66]

Besides covenants in bonds, methane abatement provisions can be incorporated into any type of financing structure between a bank or lending institution and an oil and gas capital seeker. The Methane Finance Working Group’s goal is to make methane provisions the norm in any kind of lending facility.

The following are reasons why lending provisions in conventional transactions can represent a particularly promising route for methane action:

One of the complications of including covenants or provisions linked to methane abatement is the attached penalty for not meeting the legally enforceable conditions for issuing the debt. As mentioned earlier, not meeting covenants and provisions typically results in harsh penalties, including a technical default, which seems quite extreme in the context of methane abatement and unlikely to be adopted by capital seekers. However, there are examples of high-yield bonds with softer penalties. For instance, not meeting a covenant can result in restrictions on a company’s ability to secure future debt with company assets (“limitation on liens”), not exceeding a specified leverage ratio (“limitation on indebtedness”), and limiting cash outflows, including dividends, acquisitions, and investments by the company (“limitation on restricted payments”).[68] Similar softer penalties for noncompliance―such as a small increase in interest payments in line with KPI-linked instruments―would be appropriate when targeting methane emission reductions and would align with the objective of the Methane Finance Working Group.

[1] UNEP, “Facts About Methane,” https://www.unep.org/explore-topics/energy/facts-about-methane.

[2] Core Writing Team, Hoesung Lee, and José Romero, eds., “Climate Change 2023 Synthesis Report: Summary for Policymakers,” 2023, Intergovernmental Panel on Climate Change, pp. 1–34, https://www.ipcc.ch/report/ar6/syr/downloads/report/IPCC_AR6_SYR_SPM.pdf.

[3] “Global Methane Tracker 2024,” International Energy Agency, March 2024, https://www.iea.org/reports/global-methane-tracker-2024.

[4] Ibid.

[5] “Global Methane Assessment: Benefits and Costs of Mitigating Methane Emissions,” United Nations Environment Programme, May 6, 2021, https://www.unep.org/resources/report/global-methane-assessment-benefits-and-costs-mitigating-methane-emissions.

[6] “Oil & Gas Decarbonization Charter Launched to Accelerate Climate Action,” COP28, December 2, 2023, https://www.ogdc.org/wp-content/uploads/2024/03/COP28-OG-Decarbonization-Charter.pdf .

[7] GFMR focuses on providing grant funding, technical assistance, policy and regulatory reform advisory services, institutional strengthening, and mobilizing financing to support action by governments and operators, thereby jump-starting the deployment of flaring and methane reduction solutions. See GFMR’s website: https://www.worldbank.org/en/programs/gasflaringreduction/brief/ggfr-to-evolve-to-the-global-flaring-methane-reduction-partnership.

[8] “The Oil and Gas Industry in Net Zero Transitions,” International Energy Agency, November 2023, https://www.iea.org/reports/the-oil-and-gas-industry-in-net-zero-transitions.

[9] “Emissions from Oil and Gas Operations in Net Zero Transitions,” International Energy Agency, May 2023, https://www.iea.org/reports/emissions-from-oil-and-gas-operations-in-net-zero-transitions.

[10] “The Imperative of Cutting Methane from Fossil Fuels,” International Energy Agency, October 2023, p. 3, https://www.iea.org/reports/the-imperative-of-cutting-methane-from-fossil-fuels.

[11] “The Oil and Gas Industry in Net Zero Transitions,” International Energy Agency, November 2023, https://www.iea.org/reports/the-oil-and-gas-industry-in-net-zero-transitions.

[12] “Net Zero Roadmap: A Global Pathway to Keep the 1.5 °C Goal in Reach,” International Energy Agency, September 2023, p. 108, https://www.iea.org/reports/net-zero-roadmap-a-global-pathway-to-keep-the-15-0c-goal-in-reach.

[13] “Global Stocktake,” COP28, December 12, 2023, https://unfccc.int/sites/default/files/resource/cma2023_L17_adv.pdf.

[14] McKinsey estimates that existing technology can abate 80 to 90 percent of total upstream emissions today. See Gustaw Szarek et al., “The True Cost of Methane Abatement: A Crucial Step in the Oil and Gas Decarbonization,” McKinsey, November 2024, https://www.mckinsey.com/industries/oil-and-gas/our-insights/the-true-cost-of-methane-abatement-a-crucial-step-in-oil-and-gas-decarbonization.

[15] “Global Methane Tracker 2024,” International Energy Agency, March 2024, https://www.iea.org/reports/global-methane-tracker-2024.

[16] Methane emissions from fossil fuels stood around 120 metric tons in 2023, unchanged since 2019, with the oil and gas sector representing about 2/3. See “Methane Emissions from Energy, 2000–2023,” International Energy Agency, March 2024, https://www.iea.org/data-and-statistics/charts/methane-emissions-from-energy-2000-2023.

[17] “Barriers and Solutions to Scaling-Up Methane Finance,” Clean Air Task Force, June 2023, https://www.catf.us/resource/barriers-solutions-scaling-up-methane-finance/.

[18] IEA (2025), Global Methane Tracker 2025, IEA, Paris https://www.iea.org/reports/global-methane-tracker-2025.

[19] “Global Methane Tracker 2023,” International Energy Agency, February 2023, https://www.iea.org/reports/global-methane-tracker-2023.

[20] McKinsey’s recent assessment of $200 billion of investment toward methane abatement (which includes flared gas) by 2030 assumes $80 billion in technological and operational excellence to reduce methane leakage and flaring. However, McKinsey estimates about $120 billion in additional investments at the upstream level to build new infrastructure to evacuate the associated gas recovered. See Gustaw Szarek et al., “The True Cost of Methane Abatement: A Crucial Step in the Oil and Gas Decarbonization,” McKinsey, November 2024, https://www.mckinsey.com/industries/oil-and-gas/our-insights/the-true-cost-of-methane-abatement-a-crucial-step-in-oil-and-gas-decarbonization.

[21] Financing flows for overall methane abatement increased by 18 percent in 2022, but only around $11 million were identified as methane finance in the fossil fuels industry, less than 1 percent of the methane financed tracked. (This amounted to only two methane finance transactions.) See Pedro de Aragão Fernandes et al., “Landscape of Methane Abatement Finance 2023,” Climate Policy Initiative, November 30, 2023, https://www.climatepolicyinitiative.org/publication/landscape-of-methane-abatement-finance-2023/.

[22] Pedro de Aragão Fernandes et al., “Landscape of Methane Abatement Finance 2023,” Climate Policy Initiative, November 30, 2023, https://www.climatepolicyinitiative.org/publication/landscape-of-methane-abatement-finance-2023/.

[23] This is according to OGMP 2.0, which refers to the “near-zero” emission intensity of the Oil and Gas Climate Initiative collective average target for upstream operations of 0.25 percent by 2025.

[24] For a discussion about oil and gas demand under different decarbonization scenarios, including NZE, see “World Energy Outlook 2024,” International Energy Agency, October 2024, https://www.iea.org/reports/world-energy-outlook-2024.

[25] “The Imperative of Cutting Methane from Fossil Fuels,” International Energy Agency, October 2023, https://www.iea.org/reports/the-imperative-of-cutting-methane-from-fossil-fuels.

[26] Ibid.

[27] The IEA estimates cumulative spending requirements of about $600 billion for decarbonizing oil and gas operations between 2022 and 2030 in line with NZE scenarios. Such decarbonization measures include methane abatement; eliminating nonemergency flaring; electrifying upstream facilities with low-emission electricity; equipping oil and gas processes with carbon capture, utilisation and storage; and expanding low-emission electrolysis in refining.

[28] Conventional estimates of methane emissions from gas flaring assume a “methane destruction efficiency” of 98 percent, which means that 98 percent of the methane in the flare gas stream is combusted and converted to carbon dioxide and water, and 2 percent of the methane is directly released into the atmosphere unburned. They also assume that flares are lit and operating properly all the time. The World Bank argues that if the effective destruction efficiency of flares is just 1 percent lower (97 percent rather than 98 percent), the resulting methane emissions would increase by 50 percent, and “if the effective destruction efficiency is 4 percent lower (94 percent), the methane emissions from gas flaring would be triple conventional estimates.” See “Global Gas Flaring Tracker Report,” World Bank, June 20, 2024, p. 16, https://thedocs.worldbank.org/en/doc/d01b4aebd8a10513c0e341de5e1f652e-0400072024/original/Global-Gas-Flaring-Tracker-Report-June-20-2024.pdf.

[29] The NZE assumes that the global average methane intensity of natural gas supply falls from around 1.4 percent in 2022 to 0.5 percent in 2030 and 0.1 percent in 2050; for oil, the methane emissions intensity falls from 1.3 percent in 2022 to 0.3 percent in 2030 and 0.05 percent in 2050.

[30] These estimates are based on oil and gas companies that currently have net-zero targets, including scope 1, 2, and 3 emissions, as reported by Bloomberg data and their reported production data as of 2024, also based on Bloomberg and accessed in November 2024.

[31] “World Bank Steps Up Efforts to Address Methane Emissions,” World Bank, December 4, 2023, https://www.worldbank.org/en/news/factsheet/2023/12/04/world-bank-steps-up-efforts-to-address-methane-emissions.

[32] “Eyes on Methane,” United Nations Environment Programme, November 2024, p. 11, https://www.unep.org/resources/eye-methane-2024.

[33] “Financing Reductions in Oil and Gas Methane Emissions,” International Energy Agency, 2023, https://www.iea.org/reports/financing-reductions-in-oil-and-gas-methane-emissions.

[34] Gianni Lorenzato et al., “Financing Solutions to Reduce Natural Gas Flaring and Methane Emissions,” World Bank, March 28, 2022, https://www.worldbank.org/en/programs/gasflaringreduction/publication/financing-solutions-to-reduce-natural-gas-flaring-and-methane-emissions.

[35] “Climate Transition Finance Handbook,” International Capital Market Association, 2023, https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/climate-transition-finance-handbook/.

[36] “Climate and Sustainability Awareness Bonds,” European Investment Bank, 2018, https://www.eib.org/en/investor-relations/cab/index.htm.

[37] Patrice Cochelin, Bryan Popoola, and Emmanuel Volland, “Sustainable Bond Issuance to Approach $1 Trillion in 2024,” S&P Global Ratings, February 13, 2024, https://www.spglobal.com/_assets/documents/ratings/research/101593071.pdf.

[38] Gautam Jain, “Thematic Bonds: Financing Net-Zero Transition in Emerging Market and Developing Economies,” Center on Global Energy Policy, Columbia University, December 12, 2022, https://www.energypolicy.columbia.edu/publications/thematic-bonds-financing-net-zero-transition-emerging-market-and-developing-economies/

[39] Ibid.

[40] “Green Bond Principles,” International Capital Market Association, June 2021, https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/green-bond-principles-gbp/ and “Sustainability-Linked Bond Principles,” International Capital Market Association, June 2020, https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/sustainability-linked-bond-principles-slbp/.

[41] “EU Taxonomy for Sustainable Activities,” European Commission, accessed December 2024, https://finance.ec.europa.eu/sustainable-finance/tools-and-standards/eu-taxonomy-sustainable-activities_en.

[42] “Certification Under the Climate Bonds Standard,” Climate Bonds Initiative, accessed December 2024, https://www.climatebonds.net/certification.

[43] “Barriers and Solutions to Scaling-Up Methane Finance,” Clean Air Task Force, June 2023, https://www.catf.us/resource/barriers-solutions-scaling-up-methane-finance/.

[44] Luisa Palacios and Catarina Vidotto Caricati, “Assessing ESG Risks in National Oil Companies: Transcending ESG Ratings with a Better Understanding of Governance,” Center on Global Energy Policy, Columbia University, May 18, 2023, https://www.energypolicy.columbia.edu/publications/assessing-esg-risks-in-national-oil-companies-transcending-esg-ratings-with-a-better-understanding-of-governance/.

[45] Ibid.

[46] Ibid.

[47] Andrew Howell and Pavel Laberko, “Can Investors Spur National Oil Companies Toward Methane Action?” World Economic Forum, July 2024, https://www.weforum.org/stories/2024/07/can-investors-spur-national-oil-companies-toward-methane-action/.

[48] Stephanie Saunier and Torleif Haugland, “Methane Action at National Oil Companies: A Call for Ambitious Methane Reduction Targets,” Environmental Defense Fund, March 24, 2024, https://business.edf.org/wp-content/blogs.dir/90/files/Methane-Action-at-NOCs_March-24.pdf and Andrew Howell and Pavel Laberko, “Can Investors Spur National Oil Companies Toward Methane Action?” World Economic Forum, July 2024, https://www.weforum.org/stories/2024/07/can-investors-spur-national-oil-companies-toward-methane-action/.

[49] “The Oil and Gas Industry in Net Zero Transitions,” International Energy Agency, November 2023, https://iea.blob.core.windows.net/assets/f065ae5e-94ed-4fcb-8f17-8ceffde8bdd2/TheOilandGasIndustryinNetZeroTransitions.pdf.

[50] Gautam Jain and Luisa Palacios, “Investing in Oil and Gas Transition Assets En Route to Net Zero,” Center on Global Energy Policy, Columbia University, March 2, 2023, https://www.energypolicy.columbia.edu/publications/investing-in-oil-and-gas-transition-assets-en-route-to-net-zero/.

[51] Andrew Baxter, Annika Squires, and Clare Staib-Kaufman, “Shared Duty: National, International Oil Companies Bound Together by Methane Obligations,” Environmental Defense Fund, accessed December 2024, https://business.edf.org/wp-content/blogs.dir/90/files//EDF-Shared-Duty-JV-IOC-NOC.pdf.

[52] “Oil and Gas Industry: A Research Guide,” Library of Congress, accessed December 2024, https://guides.loc.gov/oil-and-gas-industry/companies.

[53] Bradford J. Sandler et al., “Distressed Investor Considerations in E&P Oil and Gas Restructurings,” 2020, https://www.pszjlaw.com/wp-content/uploads/2020/07/564_Distressed-Investor-Considerations-in-E_P-Oil-and-Gas-Restructurings.pdf.

[54] Saud Al-Fattah, “The Role of National and International Oil Companies in the Petroleum Industry,” United States Association for Energy Economics, July 28, 2013, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2299878.

[55] This chapter lays out a broad framework for incorporating covenants and provisions in conventional instruments, but more work needs to be done in this space for it to be included in the Guidance, as it is currently not.

[56] This chapter lays out a broad framework for incorporating covenants and provisions in conventional instruments, but more work needs to be done in this space for it to be included in the Guidance, as it is currently not.

[57] Gautam Jain, “A Potential Path for Alleviating Currency Risk in Emerging Market Green Bonds,” Center on Global Energy Policy, Columbia University, September 7, 2023, https://www.energypolicy.columbia.edu/publications/a-potential-path-for-alleviating-currency-risk-in-emerging-market-green-bonds/.

[58] “The Oil & Gas Methane Partnership 2.0,” Oil and Gas Methane Partnership 2.0, accessed December 2024, https://ogmpartnership.com/.

[59] “Zero Routine Flaring by 2030 (ZRF),” World Bank Group, accessed December 2024, https://www.worldbank.org/en/programs/zero-routine-flaring-by-2030.

[60] “OGCI Members Aim for Zero Methane Emissions from Oil and Gas Operations by 2030,” Oil and Gas Climate Initiative, March 8, 2022, https://www.ogci.com/news/ogci-members-aim-for-zero-methane-emissions-from-oil-and-gas-operations-by-2030.

[61] “The Oil and Gas Decarbonization Charter,” Oil and Gas Climate Initiative, accessed December 2024, https://www.ogdc.org/about/.

[62] “Technical Guidance Documents,” Oil and Gas Methane Partnership 2.0, accessed December 2024, https://ogmpartnership.com/wp-content/uploads/2023/02/Level-1-and-level-2-TGD-Approved-by-SG_1.pdf.

[63] “Global Flaring and Methane Reduction Partnership (GFMR),” World Bank Group, accessed December 2024, https://www.worldbank.org/en/programs/gasflaringreduction/methane-explained.

[64] David Azarkh and Stephanie Rowan, “High Yield Indentures: Typical Covenants,” LexisNexis, December 6, 2019, https://www.stblaw.com/docs/default-source/related-link-pdfs/lexis-nexis_high-yield-indentures_azarkh-rowan.pdf and James McDonald and Riley Graebner, “High-Yield Bonds: An Introduction to

Material Covenants and Terms,” Butterworths Journal of International Banking and Financial Law, April 2014, https://www.skadden.com/-/media/files/publications/2014/04/mcdonaldgraebnerhybcovenants(2).pdf.

[65] “Net Zero Bondholder Stewardship: The Potential for Unlabelled Debt,” Institutional Investors Group on Climate Change, September 23, 2024, p. 7, https://www.iigcc.org/resources/bondholder-stewardship-potential-unlabelled-debt-discussion-paper.

[66] For more examples of covenants that could be adapted for methane-related requirements, see “Net Zero Bondholder Stewardship: The Potential for Unlabelled Debt,” Institutional Investors Group on Climate Change, September 23, 2024, https://www.iigcc.org/resources/bondholder-stewardship-potential-unlabelled-debt-discussion-paper.

[67] Gissell Lopez and Ben Ratner, “The Methane Emissions Opportunity: Our Perspective on Leveraging Technology in Continuous Improvement in the Oil & Gas Sector,” JPMorgan Chase, November 2023, https://www.jpmorgan.com/content/dam/jpm/cib/complex/content/redesign-custom-builds/carbon-compass/JPMC_methane.pdf.

[68] “Introduction to High Yield Bond Covenants,” Western Asset Management, June 6, 2011, https://www.westernasset.com/us/en/pdfs/whitepapers/introduction-to-high-yield-bond-covenants-2011-06.pdf.

Models can predict catastrophic or modest damages from climate change, but not which of these futures is coming.

On November 6, 2025, in the lead-up to the annual UN Conference of the Parties (COP30), the Center on Global Energy Policy (CGEP) at Columbia University SIPA convened a roundtable on project-based carbon credit markets (PCCMs) in São Paulo, Brazil—a country that both hosted this year’s COP and is well-positioned to shape the next phase of global carbon markets by leveraging its experience in nature-based solutions.

Full report

Reports by Luisa Palacios, Gautam Jain & Preetha Jenarthan • June 30, 2025